When Beijing Writes the Rules: How China’s 15th Plan Reprices Foreign Capital

Author: Justin Kew

China’s 15th Five‑Year Plan is less about adding more capacity and more about who writes the rules that make foreign technology and capital acceptable worldwide.

The 15th Five‑Year Plan (15FYP), adopted on the March 2026 sessions, hard‑codes “new quality productive forces” centred on artificial intelligence, advanced chips, humanoid robotics and clean energy, and backs this with an economy‑wide “AI+” deployment drive. At the same time, China has moved from a high‑level Global AI Governance Initiative to a concrete Global AI Governance Action Plan, while the United States has partially reversed earlier AI‑chip export bans and the European Union has slowed elements of its AI Act to protect competitiveness. The approach is not a story of clean decoupling but of rules competition with expected cash flows and cost of capital are being reshaped by AI‑centred technical, data and sustainability standards rather than by capacity cycles alone.

Why this matters?

China’s 15FYP elevates AI, advanced chips, robotics and clean energy into “new quality productive forces”, embedding AI and standards deep into industrial and social policy.

China’s Global AI Governance Action Plan and outward standards push now operate alongside a looser but politicised US AI‑chip regime and a more flexible EU AI Act, creating a three‑cornered standards contest.

The main risk for foreign capital is not simply overcapacity, but being locked into one politicised standards bloc, with stranded‑standards risk across EVs, data centres, grids, industrial automation and AI infrastructure.

What is changing?

The 15FYP, covering 2026‑2030, formalises a pivot from high‑speed to high‑quality growth and defines new quality productive forces in explicitly technological terms: AI, advanced semiconductors, humanoid robotics, quantum information, new‑energy vehicles, clean energy (including nuclear fusion) and 6G. The plan is backed by an economy‑wide “AI+” strategy that aims to integrate AI into manufacturing, energy, transport, agriculture, education and public services, with cross‑ministry implementation focused on AI’s impact on jobs, distribution and social stability.

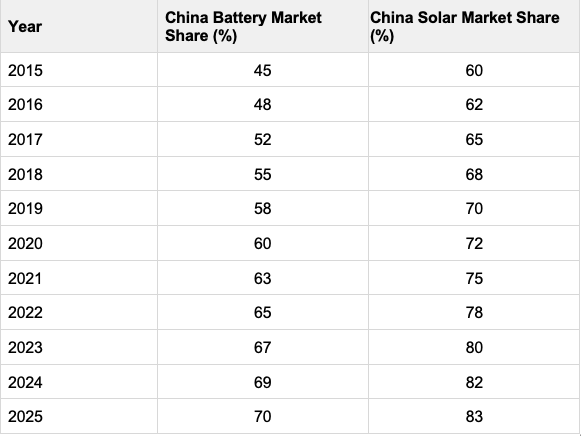

China already dominates capacity in several of these sectors: public and industry estimates suggest that by 2025 it accounts for around 70% of global lithium‑ion battery manufacturing capacity and more than 80% of solar module manufacturing. These are directionally reflected in the datasets below.

China share of global EV battery & solar capacity

On AI, Beijing has built a layered domestic regime: algorithm‑filing and recommendation‑system rules, data‑security and localisation requirements, sectoral guidance on AI in finance and healthcare, and targeted regulations on generative AI services. In 2025–2026, this was extended outward via a Global AI Governance Action Plan that operationalises the 2023 Global AI Governance Initiative, setting out 13 areas including standards cooperation, “safe and controllable” AI, infrastructure connectivity and support for the Global South.

Alongside these moves, China has tightened export controls on critical technologies – including certain rare earths, semiconductor equipment, advanced EV battery chemistries and AI‑relevant geospatial data and uses licensing to manage outward transfer of sensitive know‑how. Indicative counts of Chinese tech‑export‑control and standards‑related events show a steady increase.

Externally, constraints have shifted. The Trump administration in early 2026 moved from a near‑blanket presumption of denial for top‑end AI chips to a licensing regime allowing certain exports to China, subject to high tariffs and case‑by‑case national‑security review, while exploring new rules to require US authorisation for some foreign investments in China’s AI and chip sectors. In Europe, the EU AI Act has been supplemented and partly slowed via a “Digital Omnibus” and related measures that delay some obligations for high‑risk systems and introduce flexibilities on data and scaling to preserve competitiveness, even as Brussels continues to project its regulatory model.

Meanwhile, trade‑defence measures in green sectors have continued to rise, with more anti‑subsidy and anti‑dumping cases targeting Chinese EVs, batteries and solar. The constructed series below illustrates the broad direction.

Together, these moves mean that the 15FYP does not simply extend China’s capacity race; it embeds capacity inside an increasingly dense regime of AI‑centred technical, data and sustainability standards designed to shape both domestic and external value chains.

The non‑obvious mechanism

The non‑obvious mechanism is that AI turns standards into the main transmission channel through which Chinese policy affects foreign balance sheets. China’s dominance in batteries, solar and key manufacturing inputs gives Beijing leverage to define detailed technical and environmental standards on battery chemistries, charging protocols, grid‑code requirements, cybersecurity for connected vehicles, recyclability thresholds, that de facto determine admissible components and data flows. The 15FYP’s “AI+” mandate extends this logic across sectors, making AI systems and data‑governance rules a structural part of industrial policy rather than an add‑on.

These standards travel along three under‑appreciated paths:

First, they are bundled with Chinese‑financed infrastructure under Belt and Road‑type initiatives and newer platforms, where grid, port, rail, smart‑city and data‑centre projects come with Chinese equipment, software and governance norms embedded.

Second, Chinese firms and officials are increasingly active in international standards bodies and multilateral AI discussions – from ITU and ISO working groups to UN and regional forums, where they push for “inclusive” governance and “technology neutrality” consistent with domestic frameworks.

Third, many emerging‑market regulators, facing scarce capacity, treat Chinese and EU technical norms as reference points, creating overlapping or competing compliance regimes.

AI amplifies all three channels. China’s domestic AI governance including algorithm filing, AIGC rules, security and ethics guidance attaches conditions to how models are trained and deployed; when these models power smart EVs, industrial robots, grid management systems or public‑service platforms abroad, their embedded governance constraints shape host‑country data and security practices. Open‑weight models such as DeepSeek, which attracted attention in 2025 for delivering strong performance at relatively low training cost, also function as a standards play by seeding Chinese AI architectures and tooling as global defaults for downstream developers.

For foreign capital, the result is a standards shock: cash flows depend less on relative capacity and more on compatibility with one of at least two, and increasingly three, evolving standards blocs (US, EU, China), each with its own AI, data and security rules. A platform optimised for EU safety, privacy and sustainability rules may not meet Chinese connectivity or data‑localisation requirements without costly re‑engineering, while Chinese‑origin AI systems may face security or subsidy‑origin barriers in OECD markets. This raises CAPEX and OPEX for dual‑compliance product lines, compresses returns on legacy assets and redistributes bargaining power in components, IP licensing and data access.

What investors are missing?

Consensus attention still clusters around:

overcapacity in EVs, solar and batteries;

trade‑defence headlines and tariffs; and

a relatively binary US–China “chip war” narrative.

A more variant view emphasises that constraints have become more subtle and more standards‑driven.

First, US policy has shifted from simple denial to a mix of licensing, tariffs and potential outbound‑investment controls, which may ease near‑term compute scarcity for Chinese AI developers while preserving Washington’s leverage over future licensing and maintenance, a complex risk profile rather than a clean cut‑off.

Second, the EU is consciously rebalancing its AI‑regulation timetable and data rules to protect scale and competitiveness, even as it seeks to export the “Brussels effect”; this raises the probability of a three‑cornered standards competition rather than a pure US–China binary.

Third, China’s Global AI Governance Action Plan and infrastructure diplomacy mean that, in many high‑growth markets, Chinese AI and infrastructure standards are the most practical default.

The capital market under‑prices stranded‑standards risk: the possibility that specific technologies like battery chemistries, inverter designs, industrial‑robot interfaces, smart‑meter platforms, AI model architectures become locked into one regulatory bloc and cannot be easily re‑certified or monetised in others. This is particularly acute in private‑market valuations, where revenue models often extrapolate from one jurisdiction without fully stress‑testing regulatory portability and cross‑regime compliance costs.

Why this matters now?

Several catalysts between now and the late 2020s will test these mechanisms. In China, implementation documents and sectoral plans under the 15FYP will roll out through 2026‑2027, specifying quantitative targets for AI penetration, industrial upgrading, clean‑tech deployment and “secure and controllable” supply chains, together with detailed technical and data standards. The Global AI Governance Action Plan will be operationalised via pilot projects and cooperation agreements in Asia, Africa and the Middle East, visibly locking in standards and infrastructure packages.

In advanced economies, the EU AI Act’s obligations for high‑risk systems will phase in towards 2027, interacting with sector‑specific rules such as data, cybersecurity and supply‑chain‑due‑diligence legislation. In the United States, further rule‑making on AI‑chip exports and outbound investment screening is under discussion, and the political durability of the Trump administration’s 2026 liberalisation is uncertain. Each of these decision points is likely to trigger episodic repricing for firms and assets whose business models hinge on cross‑bloc AI, data and technical compatibility.

Policy outlook

Base case (2026–2030): China pursues a hedged integration strategy in which “new quality productive forces” and AI‑centred standards are pushed aggressively at home and through South–South partnerships, while avoiding an explicit break with OECD economies. The United States maintains a licensing‑plus‑tariffs AI‑chip regime and expands outbound‑investment screening selectively, preserving leverage but not fully cutting China off from advanced compute. The EU AI Act is implemented with delays and adjustments, continuing to project influence but with more flexibility than initially signalled.

Upside for partial convergence: Under a more co‑operative environment, there is scope for narrow mutual recognition in areas such as autonomous‑vehicle safety, some cybersecurity baselines or climate‑related reporting, reducing dual‑compliance burdens for multi‑bloc firms. Limited alignment in AI‑safety principles under UN or OECD processes could marginally lower policy‑driven volatility around AI deployments.

Downside: If rivalry escalates, AI and data could be fully securitised: both blocs treat AI infrastructure as critical national‑security assets, restrict cross‑border deployments, harden data‑localisation rules and expand blacklists on hardware and software in critical infrastructure. This would likely bifurcate value chains into incompatible ecosystems by the late 2020s, with significant write‑downs for cross‑bloc JVs, stranded AI‑infrastructure assets and higher cost of capital for firms trying to serve both sides.

Indicative timelines

2026: 15FYP enters into force; first batch of sectoral plans and AI+ implementation documents published; US AI‑chip export policy reset with licensing and tariffs.

2026–2027: Global AI Governance Action Plan pilots roll out; EU AI Act and related measures phase in; expanded Chinese standards and export‑control lists in strategic sectors.

2028–2030: Clearer crystallisation of standards blocs; potential pockets of mutual recognition or, in downside scenarios, more explicit techno‑security partitioning.

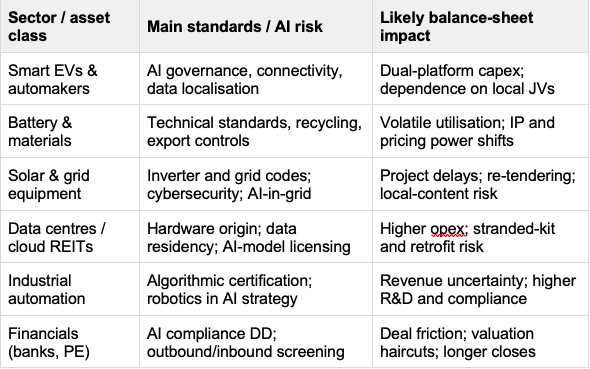

Sector, supply‑chain and asset‑level implications

Key sectoral transmission channels

Four mechanisms matter most for cash flows and cost of capital.

Contractual and technical stickiness: Once infrastructure is built to Chinese standards with embedded AI, switching ecosystems can be prohibitively expensive, locking in future revenue for Chinese suppliers but creating path‑dependency and stranded‑asset risk for host sponsors.

Regulatory gating: Access to Chinese demand, particularly in autos, industrial equipment and AI‑enabled services, will depend on compliance with domestic AI, data and technical rules, favouring firms willing to adapt product design and data governance.

Financing channels: Chinese policy banks and state‑linked lenders can package concessional financing with standards‑compliant technology and AI systems, displacing commercial lenders and reshaping risk allocation on large projects.

Political‑risk migration: Western political‑risk premia may attach to domestic firms heavily embedded in Chinese standards ecosystems, not just to Chinese counterparties, affecting ratings, spreads and equity multiples.

Within capital structures, common equity of firms making large, irreversible bets on one standards bloc carries the most convexity, while senior secured debt on essential infrastructure may benefit from stronger host‑state support but face novel covenant and restructuring complexity around origin, data and security‑related clauses.

Geopolitical overlay

Geopolitically, the 15FYP and the Global AI Governance Action Plan position China as a provider of “intelligent infrastructure” and AI governance templates to the Global South, framed in terms of sovereignty, development and digital‑divide reduction. For many emerging economies, Chinese packages that combine hardware, software, AI capabilities, training and finance can appear more immediately actionable than slower, more fragmented Western offerings, especially in power, transport and digital public infrastructure.

The decisive question for foreign capital is where swing markets – in South‑East Asia, the Gulf, Africa and Latin America – align their standards and AI regulatory reference points. Choices made over the next decade will set default technical norms, influence how courts and regulators treat disputes, and shape recovery prospects for cross‑border projects that straddle competing standards blocs.

Conclusion

By 2030, the binding constraint for many foreign‑invested assets exposed to China is unlikely to be tariffs or headline market access, but compatibility with one of several politicised AI‑centred standards ecosystems. The 15FYP’s combination of “new quality productive forces”, AI+ integration and outward‑facing AI governance means that AI and standards, rather than capacity and trade alone, will increasingly determine which cash flows are realisable, how volatile they are and what cost of capital they bear.

Structurally, this points to higher compliance and capex burdens, wider dispersion of cost of capital between mono‑ and multi‑standards firms, and a rising premium on legal and regulatory due diligence in underwriting. Cyclically, repricing shocks are likely to cluster around policy milestones – export‑control decisions, standards releases, AI‑governance updates and trade‑defence rulings – rather than purely around demand surprises or macro cycles.

This article is for information and discussion only and does not constitute investment advice or a recommendation.

References

China Briefing – China’s 15th Five‑Year Plan: Key Insights for Foreign Investors – 2026

Chinese Embassy in the US – The 15th Five‑Year Plan: China’s blueprint for a brighter future – 2026

State Council / Xinhua – What to watch at China’s Two Sessions as new plan begins – 2026

The China Academy – China’s 2026 Two Sessions: 15th FYP to Prioritise AI and Robotics – 2026

CGTN – Two Sessions 2026: How China’s 15th Five‑Year Plan can drive modernisation – 2026

ANSI – China Announces Action Plan for Global AI Governance – 2025

Mayer Brown – Artificial Intelligence: A Brave New World – China formulates AI global governance rules – 2025

East Asia Forum – China resets the path to comprehensive AI governance – 2025

IAPP – Preparing for compliance: Key differences between EU, Chinese AI regulations – 2025

Agenda Pública – Anti‑scale regulations: China and Europe’s rivalry over AI – 2026

VU Amsterdam – Tackling regulatory gaps in AI: The European and Chinese approach – 2026

BISI – Trump Reverses US AI Chip Export Policy to China – 2026

Economic Times – US mulls new rules for AI chip exports – 2026

CFR – The New AI Chip Export Policy to China – 2026

CSIS – Dual Circulation and China’s New Hedged Integration Strategy – 2026

Carbon Brief – Q&A: What does China’s 15th Five‑Year Plan mean for climate change? – 2026

20th CPC Report – Full text of the report to the 20th National Congress – 2022

BatteryTech Online / SMM – China Imposes / Tightens Export Controls on EV Battery Tech – 2025–2026

EV and solar sector analyses – Various industry and media sources on China’s clean‑tech dominance – 2025

Foreign Policy / M&G – DeepSeek and China’s AI landscape – 2025–2026

USSC – “Intelligent everything”: China’s policy to supercha