The New Gatekeepers: How the Industrial Accelerator Act Quietly Tightens Foreign Direct Investment (FDI) and Supply‑Chain Control

Author: Justin Kew

The EU has built a second FDI filter inside the Single Market – not labelled "security” but wielded as industrial policy.

Brussels adopted the Industrial Accelerator Act on 4 March 2026, and beneath the "Made in EU" branding lies a regime that will reshape who can invest where, under what conditions, and with what degree of control. The Act introduces sector‑specific FDI conditions for investments above €100 million in batteries, solar photovoltaics, electric vehicles and critical raw materials, layering on top of the revised FDI Screening Regulation that took effect in 2025. For the first time, foreign capital in strategic sectors faces explicit local‑content, employment and technology‑transfer requirements enforceable at both member‑state and Commission level, with a 49 per cent ownership cap and mandatory joint‑venture structures where the investor's home country controls more than 40 per cent of global manufacturing capacity in the relevant sector.

The market is treating this as permitting reform with a procurement tilt. The mechanism that matters is gatekeeping: the Act creates a parallel screening channel framed as industrial policy, empowers the Commission to review and impose conditions on investments above €1 billion or those with cross‑border impact, and embeds reciprocity into procurement through the Government Procurement Agreement filter, effectively locking non‑Government Procurement Agreement (GPA) signatories out of state‑aid‑backed contracts unless their home markets open in return. This is not about blocking capital; it is about conditioning access so that only capital that builds EU supply‑chain depth and absorbs transition risk on European balance sheets will clear at speed and scale.

Why This Matters

The Act creates a new, sector‑specific FDI regime parallel to security‑based screening, with explicit local‑content, employment and technology‑transfer conditions enforceable by member states and the Commission.

Foreign investors in batteries, EVs, solar and critical raw materials face a 49% ownership cap, mandatory EU joint‑venture partners and a minimum 50% EU workforce where their home country commands more than 40% of global capacity.

The Commission gains power to review investments above €1 billion or with significant cross‑border impact, to require or block conditionalities, and to extend sectoral coverage via delegated acts, moving FDI policy from member‑state to Brussels control.

What Is Changing: From Open Market to Conditional Access

The Industrial Accelerator Act formally took effect as a Commission proposal on 4 March 2026, with Parliament and Council adoption expected by late 2026 or early 2027 and full implementation likely by 2028. The regulation targets six strategic sectors: steel, cement, aluminium, automotive, batteries and net‑zero technologies (solar, wind, heat pumps, electrolysers), with the possibility to extend to chemicals and other energy‑intensive industries via delegated acts. The Act does three things that will change capital allocation and asset pricing: it mandates "Made in EU" and low‑carbon criteria in public procurement and state‑aid schemes for these sectors; it creates a sector‑specific FDI regime with explicit conditions on ownership, employment and technology transfer; and it promises faster, digital permitting through industrial acceleration areas and a one‑stop shop, with the declared goal of lifting manufacturing's share of EU GDP from 14.3 per cent to 20 per cent by 2035.

The FDI provisions apply to investments of at least €100 million by companies from non‑EU countries that control more than 40 per cent of global manufacturing capacity in batteries, solar PV, electric vehicles or critical raw materials. To qualify for approval, such investments must create high‑quality jobs, drive innovation and growth, generate value in the EU through technology and knowledge transfer, comply with local‑content requirements, and guarantee at least 50 per cent employment of EU workers. Where the 40 per cent threshold is met, the Act imposes a 49 per cent cap on foreign ownership and requires a mandatory joint venture with European partners, alongside compulsory technology transfer. Member states retain primary review authority, but the Commission can assess on its own initiative where the investment exceeds €1 billion or has the potential to significantly impact added value creation in the EU, or at the request of a member state where the investment has significant cross‑border impact.

The procurement and state‑aid provisions work in parallel. Public contracts and subsidies for the six strategic sectors will include "Made in EU" and low‑carbon requirements, with equal treatment for bidders from countries that have signed the Government Procurement Agreement or have equivalent bilateral commitments. Non‑GPA signatories, most notably China, face either exclusion or a scoring penalty unless their home markets grant reciprocal access to EU firms. The Act also introduces an International Procurement Instrument mechanism, giving the Commission investigative powers and the ability to impose measures limiting third‑country access if European companies face serious and recurring restrictions abroad and those barriers persist after consultation.

The Non‑Obvious Mechanism: Parallel Screening as Industrial Lever

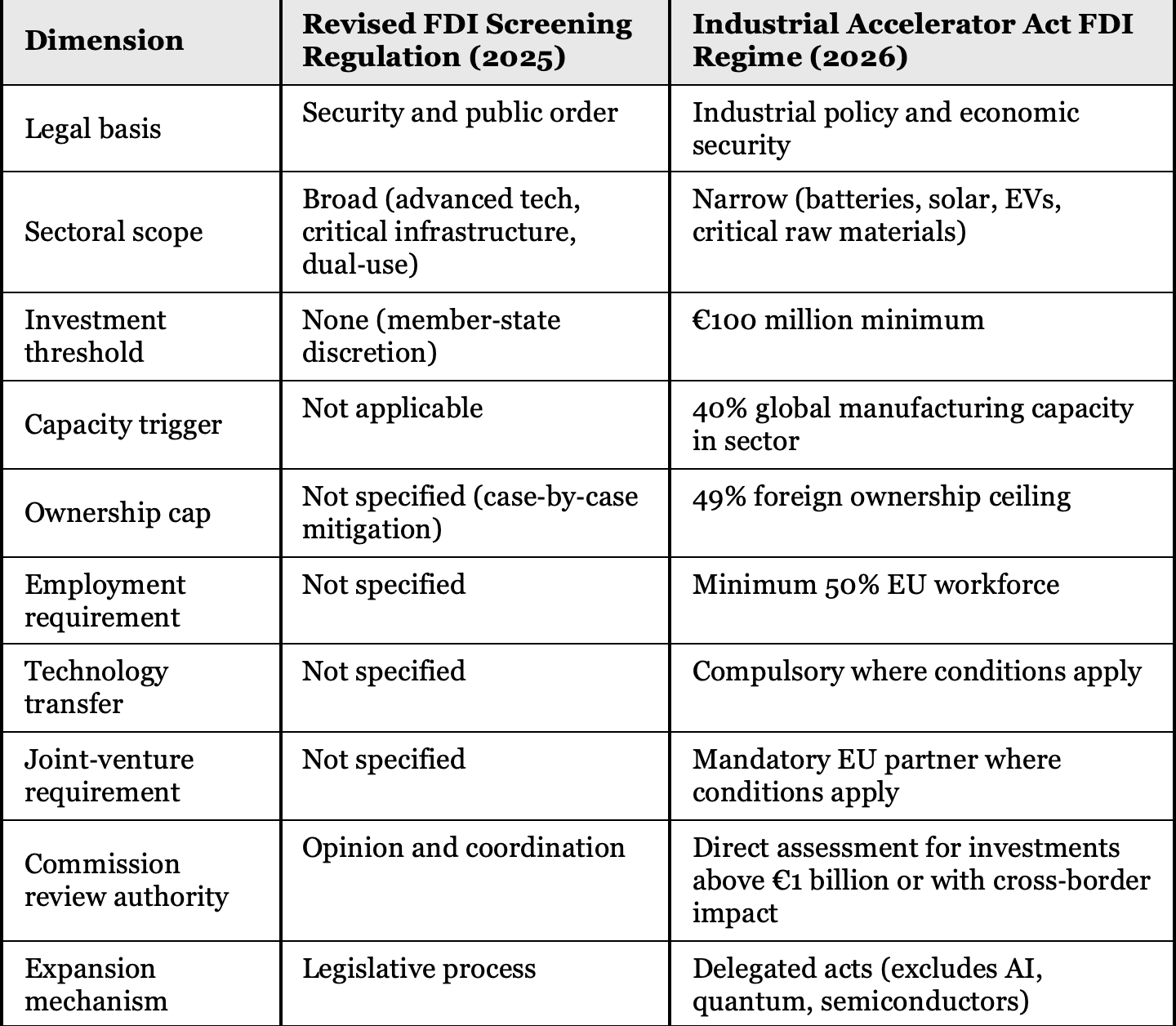

The Industrial Accelerator Act does not replace the revised FDI Screening Regulation, which entered into force in 2025 and establishes mandatory pre‑closing national screening on security and public‑order grounds across all member states, with a 45‑day Phase 1 review and harmonised timelines. Instead, the Act creates a second, parallel screening channel framed explicitly as industrial policy and economic security, not national security. This distinction matters for three reasons: jurisdiction, conditions and enforcement.

Jurisdiction: The revised FDI Screening Regulation covers a broad range of sectors touching security and public order—advanced technologies (semiconductors, AI, quantum), strategic raw materials, dual‑use and military items, critical infrastructure in transport, energy and digital. The Industrial Accelerator Act's FDI regime is narrower: batteries, solar PV, EVs and critical raw materials only, with the Commission empowered to extend coverage via delegated acts that require less involvement from Parliament and Council (though both retain the power to object within two months). Digital technologies, AI, quantum and semiconductors are explicitly excluded from this delegated‑act power, meaning any extension to those sectors requires full legislative process. The narrower scope creates a targeted lever for sectors where the EU faces immediate competitive pressure and supply‑chain dependency, particularly vis‑à‑vis China.

Conditions: The revised FDI Screening Regulation provides for mitigation measures where national security concerns arise, but these are negotiated case‑by‑case and vary across member states. The Industrial Accelerator Act hard‑wires the conditions: local content, employment share, technology transfer, ownership cap, joint‑venture structure. The 40 per cent global capacity threshold is the trigger, and the 49 per cent ownership cap plus mandatory EU partner is the default outcome. This shifts the negotiation from whether conditions apply to how they are calibrated, and it moves the baseline from "open unless security risk" to "conditional unless below threshold".

Enforcement: The Commission's role under the revised FDI Screening Regulation is primarily coordination and opinion; member states retain decision‑making power. Under the Industrial Accelerator Act, the Commission has direct assessment authority for investments above €1 billion or with significant cross‑border impact, and it can require reviewing authorities to apply or not apply some or all conditionalities. This is a material centralisation of FDI policy, moving effective control from member‑state capitals to Brussels for the largest and most strategic investments. The Commission's power to expand sectoral coverage via delegated acts, combined with its direct review authority, creates a ratchet mechanism: once the structure is in place, extending it to adjacent sectors (chemicals, pharmaceuticals, advanced manufacturing) requires only executive action, not fresh legislation.

Table 1: Comparison of FDI regimes: revised FDI Screening Regulation versus Industrial Accelerator Act

What Investors Are Missing: Who Absorbs Transition Risk

The consensus view is that the Act will slow Chinese EV and battery investment into Europe, tilt procurement toward domestic producers, and modestly accelerate permitting for compliant projects. The variant view is that the Act rewrites where transition risk sits in the capital structure and who can extract value from the energy transition in Europe.

Chinese greenfield FDI in Europe rebounded in 2024 to €10 billion, up 47 per cent from 2023, with EV‑related projects pulling in €4.9 billion or 83 per cent of all Chinese greenfield investment.

Hungary attracted 62 per cent of Chinese EV investment in 2024, driven by CATL's €1.6 billion battery plant, BYD's €1.4 billion EV plant, and projects by Sunwoda Electronic and Eve Energy.

Germany and Slovakia were second and third, with Gotion's battery plant and Volvo's EV facility[10]. But 2024 also saw a 79 per cent plunge in newly announced Chinese EV projects, from an average of €15 billion in 2022–2023 to just €3.1 billion and several cancellations, including Svolt Energy's two German battery plants worth €4.2 billion, Nuode's €500 million Belgian battery component plant, and Swedish authorities blocking Putailai's €1.2 billion anode plant.

The Industrial Accelerator Act formalises this slowdown into policy. The 40 per cent global capacity threshold is explicitly designed to capture Chinese battery, solar and EV producers, who dominate global manufacturing in these segments. The 49 per cent ownership cap and mandatory EU joint‑venture partner mean that Chinese investors cannot own a controlling stake or operate independently; they must partner with a European firm that holds majority economic and governance rights. The minimum 50 per cent EU workforce requirement and compulsory technology‑transfer provisions shift both operational control and intellectual‑property risk onto the European side of the joint venture.

This changes the economics for Chinese investors in two ways. First, it caps the return: with a minority stake and shared governance, Chinese firms cannot extract full value from EU market access or subsidies. Second, it raises the entry cost: finding a credible EU joint‑venture partner with manufacturing capability, securing member‑state and Commission approval for the technology‑transfer plan, and structuring employment and local‑content commitments that satisfy both Brussels and the home regulator in Beijing adds time, complexity and negotiation leverage to the European counterparty. For Chinese firms under capital controls and facing domestic overcapacity, the calculus shifts from "invest in Europe to secure market share" to "export from China and absorb tariff cost", particularly as the EU's tariff on Chinese EVs remains in place and the US market becomes less accessible.

The flip side is that European battery, automotive and solar producers gain a structural advantage in their home market, not through direct subsidy but through conditioned access. A European battery producer bidding for a state‑aid‑backed gigafactory project competes on merit; a Chinese producer must find a European partner, cap its ownership, transfer technology and meet employment and local‑content hurdles. The procurement and state‑aid provisions amplify this: public contracts and subsidies in the six strategic sectors embed "Made in EU" and low‑carbon criteria, tilting demand toward domestic or compliant producers. For investors, this means that valuations of European industrial assets in these sectors should reflect not only their standalone cash flows but also their strategic value as joint‑venture partners for foreign entrants, a real‑option premium that did not exist before the Act.

The second‑order effect is on balance sheets. Transition risk in the energy and industrial sectors has historically been distributed across both European and foreign investors: Chinese firms absorbed technology and market risk by building capacity in Europe; European utilities and manufacturers absorbed demand and regulatory risk by purchasing or partnering with foreign suppliers. The Industrial Accelerator Act concentrates transition risk on European balance sheets by requiring that majority ownership, employment and technology reside in the EU. This is a deliberate policy choice—Brussels is effectively saying that European firms and European capital must bear the risk and capture the value of the transition, rather than outsourcing both to foreign investors. This would mean that European industrial equities in batteries, automotive and green tech are no longer just cyclical value plays; they are structural transition exposures with embedded policy support and reduced foreign competition.

Why This Matters Now: Timing, Politics and Enforcement

The Industrial Accelerator Act is a Commission proposal as of 4 March 2026, and its implementation timeline depends on Parliament and Council adoption. Based on recent regulatory precedent, the revised FDI Screening Regulation took roughly 18 months from proposal to entry into force with full implementation is likely by 2028. But three near‑term catalysts matter for capital allocation: the Government Procurement Agreement reciprocity mechanism, the Commission's delegated‑act power, and the interaction with US tariff and subsidy policy.

Reciprocity: The Act grants equal treatment in procurement to countries that have signed the Government Procurement Agreement or have equivalent bilateral commitments. China is not a GPA signatory, and its public procurement market remains largely closed to foreign bidders. The International Procurement Instrument, adopted by the Council in February 2025, gives the Commission investigative powers and the ability to impose scoring penalties or outright exclusion on bidders from countries that restrict EU access. This mechanism is already in force and can be applied immediately to procurement under the Industrial Accelerator Act once it takes effect. For investors, this means that Chinese firms and firms from other non‑GPA countries, face a two‑tier system: restricted access to EU procurement and subsidies via the reciprocity filter, and conditional access to FDI via the ownership and employment caps. The combined effect is to push Chinese investment out of direct ownership and into supply contracts or minority stakes, reducing both control and return.

Delegated acts: The Commission can extend the Act's sectoral coverage to chemicals and other energy‑intensive industries without full legislative process, subject only to a two‑month objection window from Parliament and Council. This creates policy uncertainty for investors in adjacent sectors: if the battery and EV provisions prove effective at conditioning foreign investment, Brussels has a ready mechanism to extend the regime to semiconductors (outside the exclusion), advanced materials, pharmaceuticals or defence manufacturing. The objection threshold is high, both Parliament and Council would need to muster a blocking minority so the practical bar to expansion is low once the political consensus is established.

US policy interaction: The Act's FDI provisions are structurally similar to CFIUS review in the United States, which screens foreign investment for national‑security risk and imposes mitigation measures including ownership limits, governance restrictions and technology controls. But CFIUS jurisdiction is security‑based and applies to all foreign investors; the Industrial Accelerator Act's FDI regime is industrial‑policy‑based and applies primarily to investors from countries with dominant global capacity meaning China. If the US tightens tariffs or export controls on Chinese EVs and batteries, Chinese producers face a choice: invest in Europe under restrictive conditions, or lose access to both the US and EU markets. The Industrial Accelerator Act is betting that Chinese firms will choose restricted access over no access, and that European joint‑venture partners will capture most of the value.

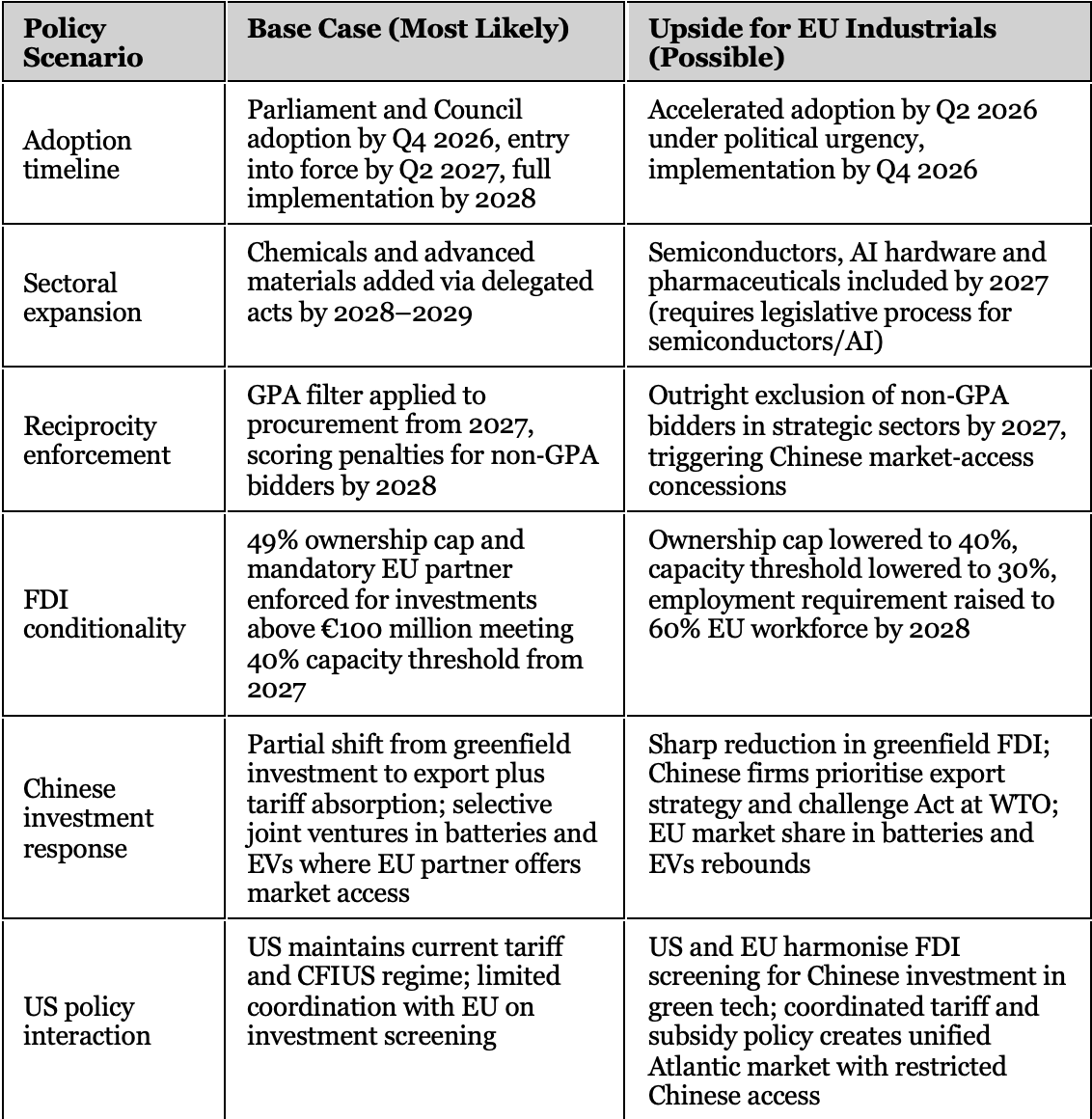

Table 2: Policy outlook and investor scenarios for the Industrial Accelerator Act, 2026–2029

Sector, Supply‑Chain and Asset‑Level Implications

The Industrial Accelerator Act's impact is not uniform across sectors or capital structures. Batteries, automotive and solar are directly in scope; steel, cement and aluminium face procurement and state‑aid conditions but not FDI restrictions (unless capacity concentration triggers thresholds); chemicals and advanced materials face extension risk via delegated acts.

For batteries, the Act entrenches European producers - Northvolt, ACC, Verkor, by restricting Chinese competition and tilting procurement toward EU joint ventures. Chinese battery producers (CATL, BYD, Eve Energy) must either accept minority stakes and technology transfer or scale back European investment. The valuation premium for European battery assets increases because they become necessary joint‑venture partners for any foreign entrant seeking EU market access. The downside risk is execution: if European producers cannot scale capacity or match Chinese cost and performance, the Act protects market share but locks in higher costs and slower technology diffusion.

Automotive: the effect is capital‑structure‑specific. European OEMs with in‑house battery capacity or strategic partnerships with EU producers gain from conditioned foreign competition and procurement preferences. European suppliers in the battery, electric‑motor and power‑electronics value chain benefit from local‑content requirements. Chinese OEMs (BYD, Chery, Geely) face the same restrictions as battery producers: minority stakes, mandatory EU partners, technology transfer. The result is that Chinese EV market share in Europe is likely to be capped by investment restrictions and tariffs, not by product competitiveness. For investors, this means that European OEMs' EV transition risk is reduced by policy, but their long‑term competitiveness depends on whether protected market share translates into innovation and scale.

Solar: the dynamics are similar to batteries, but the capacity concentration is higher: China controls over 80 per cent of global solar PV manufacturing capacity, comfortably exceeding the 40 per cent threshold. European solar producers (Meyer Burger, Enel Green Power) benefit from both procurement preferences and restricted Chinese competition. But European solar capacity is marginal relative to global supply, so the Act's effectiveness depends on whether it can stimulate greenfield investment by European or third‑country producers (US, South Korea, Japan) willing to meet local‑content and employment requirements.

Steel, cement and aluminium: the Act does not impose FDI restrictions but does embed "Made in EU" and low‑carbon criteria in public procurement and state‑aid schemes. This tilts demand toward domestic producers with decarbonisation credentials—integrated steel producers investing in hydrogen‑based direct reduction, cement producers deploying carbon capture, aluminium producers with renewable‑power contracts. The policy signal is clear: public contracts and subsidies will reward low‑carbon EU production, and foreign or high‑carbon producers will face exclusion or scoring penalties. For investors, this creates a two‑tier market: compliant EU producers with access to subsidised demand, and non‑compliant or foreign producers competing on price in the residual private market.

The cross‑cutting implication is supply‑chain resilience. The Act's local‑content and employment requirements are designed to ensure that critical supply‑chain steps—battery‑cell production, solar‑module assembly, steel and aluminium primary production—remain or return to the EU. This reduces import dependency and geopolitical exposure, but it also raises costs and locks in capital. For senior PMs and CIOs, the trade‑off is between short‑term margin compression (higher input costs, capex for compliance) and long‑term structural value (reduced foreign competition, policy‑supported demand, real‑option value as joint‑venture partner).

Conclusion: Structural Shift, Not Cyclical Noise

The Industrial Accelerator Act is the EU's first attempt to hard‑wire industrial policy into FDI and procurement at scale. The non‑consensus takeaway is that the Act does not block foreign capital; it conditions access so that only capital that builds EU supply‑chain depth and accepts minority stakes, technology transfer and employment commitments will clear. This is a structural shift in who absorbs transition risk and who captures value in the European energy and industrial transition.

For investors, the read‑across is that European industrial assets in batteries, automotive, solar and green tech are no longer just cyclical value plays. They are structural transition exposures with embedded policy support, reduced foreign competition and real‑option value as gatekeepers to the EU market. The Act moves FDI policy from member‑state to Brussels control, creates a ratchet mechanism for sectoral expansion via delegated acts, and aligns procurement, subsidy and investment screening into a single industrial‑policy lever. The risk is execution: if European producers cannot scale capacity, match foreign cost and performance, or absorb the capital required to comply, the Act protects market share but locks in higher costs and slower technology diffusion. The opportunity is for investors who can identify which European balance sheets will absorb transition risk, extract policy value, and become indispensable joint‑venture partners in a market where foreign capital increasingly needs local permission to operate.

References

European Commission – Directorate‑General for Internal Market, Industry, Entrepreneurship and SMEs. (2026, March 4). Industrial Accelerator Act. COM(2026)100. https://single-market-economy.ec.europa.eu/publications/industrial-accelerator-act_en

European Commission – Directorate‑General for Communication. (2026, March 4). Commission proposes new measures to boost EU industry and jobs. https://commission.europa.eu/news-and-media/news/commission-proposes-new-measures-boost-eu-industry-and-jobs-2026-03-04_en

Dechert LLP. (2026, March 3). The EU Industrial Accelerator Act: A New FDI Control Regime for Strategic Sectors. https://www.dechert.com/knowledge/onpoint/2026/3/the-eu-industrial-accelerator-act--a-new-fdi-control-regime-for-.html

Paul Hastings LLP. (2026, February 23). The EU Industrial Accelerator Act: What Businesses Need to Know. https://www.paulhastings.com/insights/client-alerts/the-eu-industrial-accelerator-act-what-businesses-need-to-know

Council of the European Union. (2025, February 26). International Procurement Instrument: Council gives green light to new rules promoting reciprocity. https://www.pubaffairsbruxelles.eu/eu-institution-news/international-procurement-instrument-council-gives-green-light-to-new-rules-promoting-reciprocity

Renewable Matter. (2026, March 4). Industrial Accelerator Act: the EU Commission launches the "Made in Europe" plan. https://www.renewablematter.eu/en/industrial-accelerator-act-eu-commission-launches-made-in-europe-plan

Trending Topics. (2026, March 4). EU Launches Industrial Accelerator Act to Double Manufacturing Share by 2035. https://www.trendingtopics.eu/eu-launches-industrial-accelerator-act-to-double-manufacturing-share-by-2035/

·Global Policy Watch. (2026, March 3). New Foreign Investment Screening Regulation: Key Takeaways from the Agreed Compromise Text. https://www.globalpolicywatch.com/2026/03/new-foreign-investment-screening-regulation-key-takeaways-from-the-agreed-compromise-text/

CELIS Institute. (2025, July 21). Tug‑of‑War? Determining the mandatory scope for the new FDI Screening Regulation. https://www.celis.institute/celis-blog/tug-of-war-determining-the-mandatory-scope-for-the-new-fdi-screening-regulation/

Rhodium Group and MERICS. (2025, May 20). Chinese investment rebounds despite growing frictions: Chinese FDI in Europe – 2024 Update. https://merics.org/en/report/chinese-investment-rebounds-despite-growing-frictions-chinese-fdi-europe-2024-update

Center for Strategic and International Studies (CSIS). (2025, July 17). Will the United States Push Europe Toward China?https://www.csis.org/analysis/will-united-states-push-europe-toward-china

White & Case LLP. (2025). Foreign direct investment reviews 2025: United States. https://www.whitecase.com/insight-our-thinking/foreign-direct-investment-reviews-2025-united-states

Bryan Cave Leighton Paisner LLP. (2025, April). The Committee on Foreign Investment in the United States (CFIUS) Handbook. https://www.bipc.com/assets/PDFs/Insights/CFIUS Handbook April 2025 FINAL WEB REV.pdf

This article is for information and discussion only and does not constitute investment advice or a recommendation.