Carbon at the Border, Risk in the Shadows: Why CBAM and ECB Climate Tests Will Rewrite Transition Cash Flows

Author: Justin Kew

Europe's carbon border tax that went live in January 2026 is arriving at the exact moment bank supervisors are stress‑testing who is allowed to carry transition risk, and at what price of capital.

The ECB's 2026 thematic reverse stress test, with results due in summer 2026 and bank submissions falling in Q2 will, for the first time, require 110 directly supervised institutions to identify the geopolitical scenarios that could deplete their Common Equity Tier 1 (CET1) capital by at least 300 basis points. This exercise runs concurrently with CBAM's definitive enforcement phase, which came into force on 1 January 2026 and requires importers of covered goods to purchase and surrender carbon certificates at EU borders. Separately, the ECB confirmed in July 2025 that a climate factor will be introduced into its collateral framework from the second half of 2026, applying haircuts to corporate bonds from high-emission sectors used as collateral in refinancing operations. Together, these three forces, CBAM enforcement, reverse stress-test submissions and climate-adjusted collateral constitute the first moment at which transition risk stops being a reporting obligation and starts functioning as a determinant of funding cost and capital capacity.

Portfolio managers who are pricing transition exposure primarily through subsidy and deployment growth will miss this. The capital channel, how climate and CBAM interact to reshape bank lending appetite, collateral eligibility and cost of funding is where the repricing will actually occur.

Why this matters ?

The ECB's Q2 2026 reverse stress test asks 110 banks to define their own 300bp CET1 depletion scenario, making geopolitical and transition shocks directly legible in capital planning, not just scenario analysis.

CBAM certificates, priced against ETS levels that oscillated between EUR 61 and EUR 83 per tonne through 2025, now represent a live, enforceable landed cost for high-emission imports, feeding into credit risk models for transition-exposed borrowers.

From H2 2026, the ECB's new climate factor will apply additional haircuts to high-emission corporate bonds used as collateral in refinancing operations, tightening funding conditions for banks with concentrated brown-asset exposure. hedging and robust disclosure while penalising developers reliant on opaque, shadow‑finance‑linked imports.

What is changing?

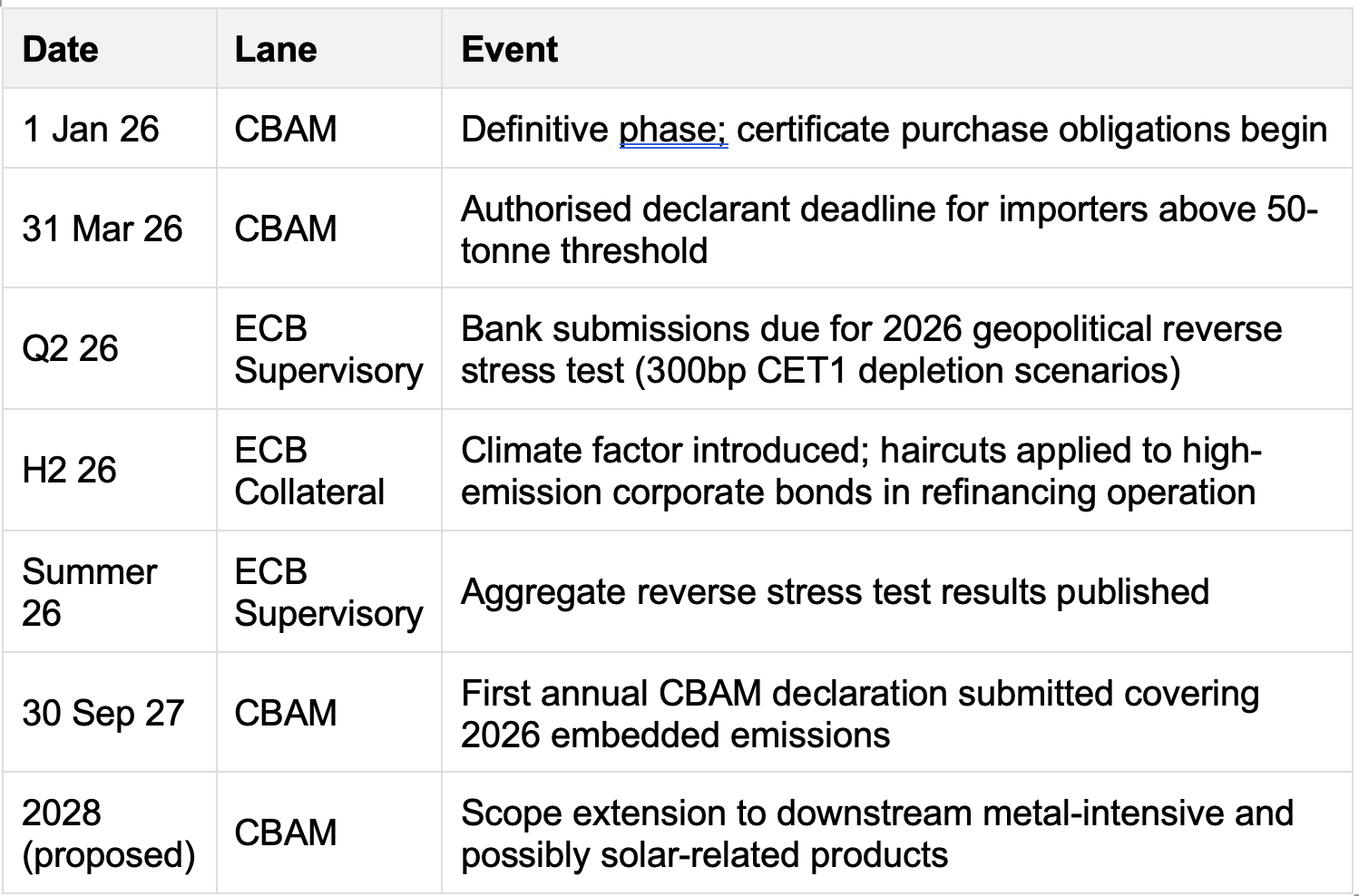

CBAM entered its definitive phase on 1 January 2026. Importers of covered goods primarily steel, aluminium, cement, fertilisers, electricity and hydrogen, must now hold authorised declarant status and purchase CBAM certificates reflecting verified embedded emissions at the point of customs clearance. Importers above the 50-tonne threshold must complete authorisation by 31 March 2026, making this month's deadline the first hard sorting mechanism between compliant and non-compliant import channels. The first annual CBAM declaration, covering all 2026 imports, falls on 30 September 2027, but the cost exposure is accruing now, from the moment goods enter EU customs.

In parallel, banking supervisors are tightening the connective tissue between climate risk and capital. The ECB's December 2025 announcement confirmed that 2026 supervisory priorities require banks to manage climate and nature-related risks prudently, alongside geopolitical resilience and operational soundness. The 2026 thematic reverse stress test, which began at the start of 2026, with bank returns due in Q2 pushes institutions to interrogate their own vulnerabilities, asking where geopolitical disruptions (including supply-chain fragmentation and carbon-cost shocks) could trigger a 300bp CET1 hit. Beyond this, the climate factor announced for the collateral framework from H2 2026 will introduce an explicit, issuer-level risk discount on marketable assets from energy-intensive or high-emission sectors, directly affecting the cost and volume of central bank refinancing available to banks carrying such exposure.

The CRR3 framework, now in force from January 2026, additionally requires banks to develop and implement transition risk plans and gives supervisors the authority to require reductions in climate exposure, a backstop that supplements stress testing with binding supervisory discretion.

Chart 1 – CBAM timeline and phases.

CBAM enforcement and ECB capital/collateral tightening are converging in the same 12-month window, creating the first period in which transition risk functions simultaneously as a border cost, a capital planning variable and a collateral constraint.

Sources: European Commission DG TAXUD, ECB Banking Supervision, Banking

The non‑obvious mechanism

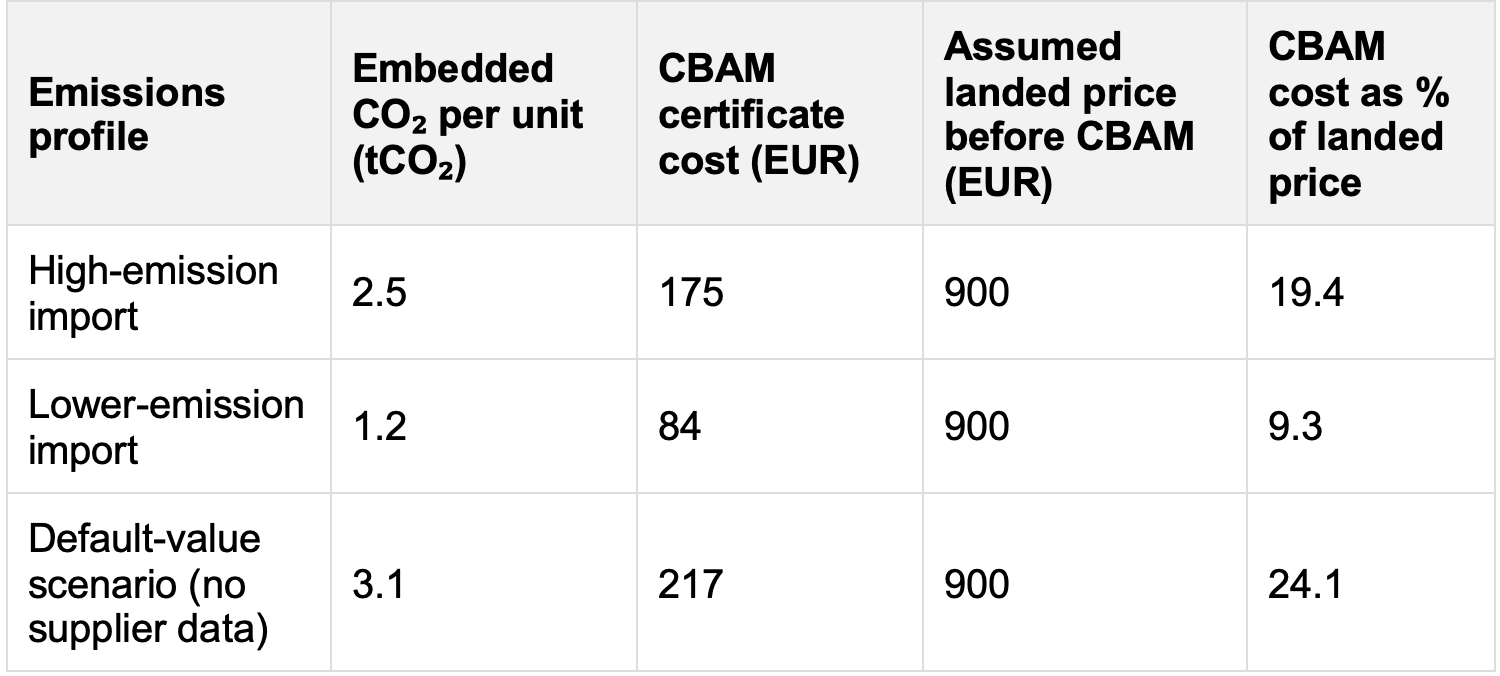

The non‑obvious mechanism is that CBAM’s enforcement does not simply raise average import prices; it selectively compresses margins on high‑emission, low‑transparency imports while shifting bargaining power and inventory risk across supply chains. Importers now need verified embedded emissions data from non‑EU suppliers to avoid conservative default values, which can significantly increase the notional carbon content of goods and therefore the number of certificates to be surrendered. For Asian solar and battery value chains where upstream power is often coal‑heavy and emissions data may be fragmented, this creates an additional “data‑driven” carbon premium, over and above any raw ETS price pass‑through.

At the same time, ECB‑aligned climate stress testing will push banks to reassess counterparties exposed to high transition risk, including developers whose business models rely on imported components facing rising CBAM liabilities and potential delays or penalties. Under these scenarios, banks may shorten tenors, increase pricing or tighten covenants for transition‑heavy borrowers, effectively increasing their cost of capital relative to better‑hedged, EU‑domiciled firms with clearer emissions data and CBAM compliance systems. The combined effect is a form of geoeconomic arbitrage: capital‑rich, disclosure‑strong actors in the EU can monetise CBAM‑induced scarcity and stress‑test‑driven repricing, while more opaque, often shadow‑finance‑dependent developers in other blocs absorb higher financing and compliance costs.

Chart 2 – CBAM cost channel into landed price

Given equal border prices, imports with higher embedded emissions face a larger CBAM cost share in the landed price, tightening margins for suppliers with coal‑heavy production.

Sources: European Commission DG TAXUD, ESMC analysis.

What investors are missing

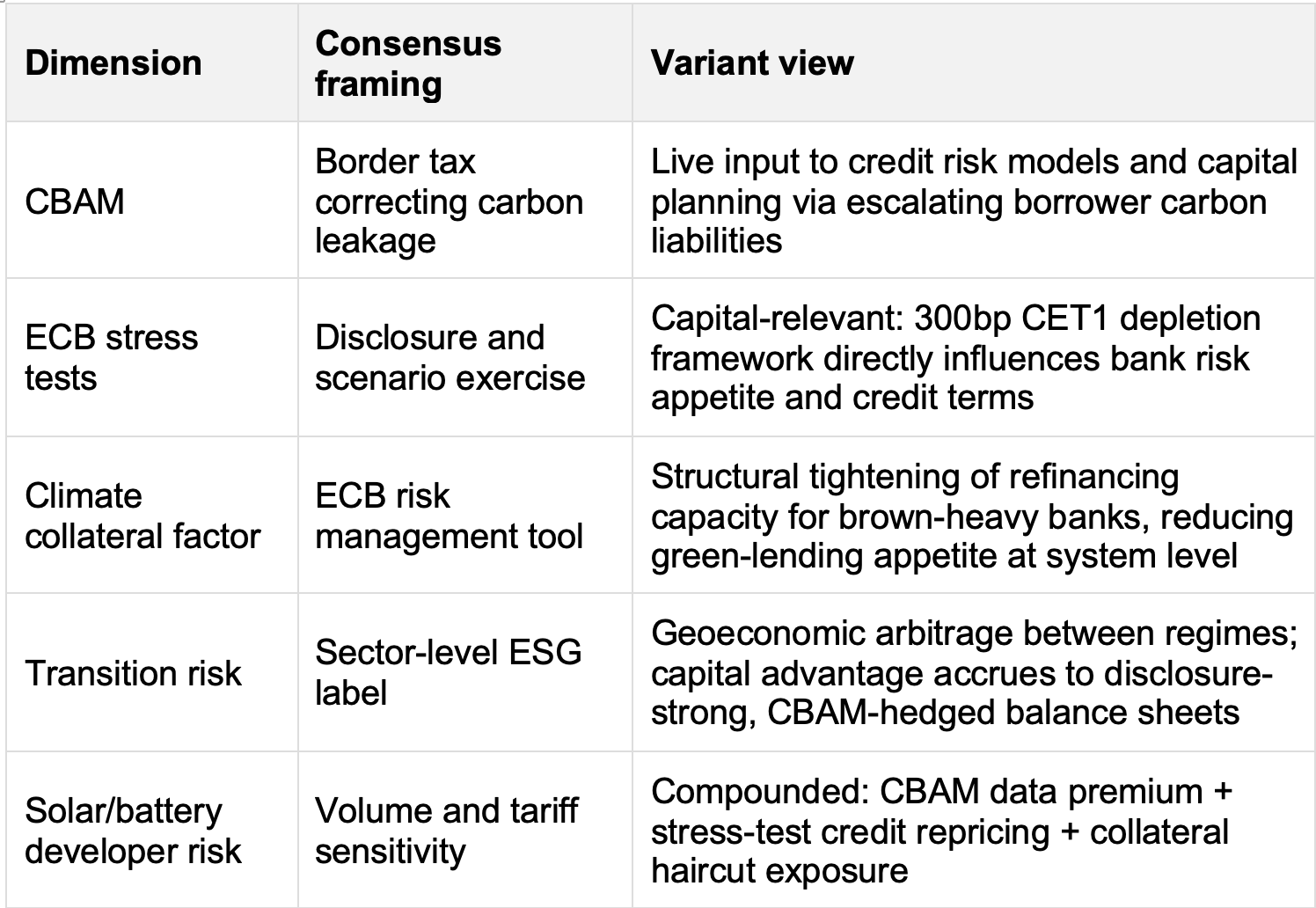

The dominant portfolio framing on transition risk remains asset-class-level: overweight green technology, underweight fossil fuels, track subsidy flows. What this misses is that CBAM and supervisory capital reform have introduced a second dimension, the balance-sheet and funding-cost dimension that acts orthogonally to the subsidy story.

Three things are being systematically under-priced:

The credit-cost channel: Banks that are serious about their Q2 2026 reverse stress test submissions will be mapping supply-chain concentration and carbon-cost escalation as potential contributors to a 300bp CET1 hit. Borrowers who cannot demonstrate CBAM compliance, emissions data quality, or supply-chain diversification are likely to be identified as contributors to adverse scenarios. This may translate gradually and individually, not systemically into shorter tenors, higher pricing or tighter covenants on project finance and corporate credit for the most exposed developers.

The collateral channel: From H2 2026, banks with high-emission bonds in their collateral pools face larger ECB haircuts, reducing their refinancing headroom. This is not a crisis instrument it is a slow, structural tightening of funding conditions that disadvantages banks concentrated in brown sectors and that, in turn, reduces their appetite to extend credit to CBAM-exposed counterparties.

The data-scarcity premium: CBAM requires verified embedded emissions data from suppliers. Where this is unavailable, as is often the case for complex supply chains from Asia or other non-EU jurisdictions, default values apply, which are set conservatively high. This data-scarcity premium is not static; it compounds as CBAM scope extends and as banks incorporate emissions data quality into their credit assessments. Developers who have not invested in supply-chain data infrastructure will face a rising cost disadvantage relative to those who have.

Why this matters now

Three near-term catalysts are converging in the same window.

March 2026: The authorised declarant deadline requires CBAM importers above the 50-tonne threshold to secure compliance status or face disruption at the border, forcing an immediate sorting of supply chains. Companies that have not completed this process are exposed to penalties, customs delays and, crucially, an inability to provide the emissions documentation now expected by climate-aware lenders.

Q2 2026: Bank submissions for the ECB's geopolitical reverse stress test are due. Institutions that have invested in granular sector and counterparty risk data will be better placed to construct credible scenarios; those that have not may reveal data gaps to supervisors, increasing supervisory pressure and near-term capital conservatism. The results will be published in summer 2026, giving investors a systemic read on which institutions are most exposed to transition-linked scenarios.

H2 2026: The ECB's climate collateral factor takes effect. This is the moment at which the supervisory signal becomes a direct funding constraint where haircuts apply, collateral pools are reassessed and bank treasury teams will be re-pricing the cost of holding transition-heavy assets on their balance sheets.

Together, these three dates define a 12-month window in which the rules of transition finance are being rewritten in real time, with outcomes that will persist in lending standards, collateral practices and credit pricing well beyond 2026.

Policy outlook

The direction of travel is clear; the pace and breadth remain the key variables.

Base case: CBAM enforcement continues as legislated, with scope extension consultations advancing towards an eventual 2028 expansion to downstream metal-intensive and solar-related components. ECB supervisory priorities for 2026–2028 maintain climate and nature risk management as an explicit priority, with progressive integration of climate factors into collateral and Pillar 2 guidance. Stress-test methodologies continue to absorb transition scenarios, making climate-adjusted credit underwriting the expected norm for significant institutions by 2027–2028.

Upside: Faster-than-expected expansion of CBAM scope and an earlier introduction of explicit climate capital buffers or penalising risk weights for high-emission exposures, accelerating the repricing of transition risk into bank lending rates.

Downside: Geopolitical and trade tensions (particularly US tariff re-escalation or bilateral pressure on CBAM from major exporters) prompt delays or carve-outs in CBAM scope extensions, and political constraints slow the pace of climate integration into bank capital frameworks.

For investors, the downside scenario does not reverse the direction — it extends the timeline. The structural forces are legislative and supervisory, not discretionary.

Sector, supply‑chain and asset‑level implications

Aluminium and steel: Already directly covered by CBAM, producers and mid-stream processors sourcing from high-emission, non-EU producers face an immediate cost increase that flows through to downstream buyers including clean energy infrastructure, grid equipment and EV manufacturing. European aluminium associations have already flagged the risk of production displacement as import patterns adjust.

Solar and solar thermal: Not yet in CBAM's definitive scope for key components, but consultation is active and the industry is lobbying for extension. More immediately, the aluminium and steel inputs used in mounting systems, racking and collectors are already covered, so cost pressure is already transmitting upstream. Developers procuring under long-term fixed-price contracts with high-emission, non-EU suppliers are most at risk of margin compression as certificate costs accrue.

Battery and storage supply chains: Mineral-intensive, geographically concentrated in processing outside the EU, and exposed to both direct CBAM costs on steel and aluminium inputs and the indirect data-quality premium. Supply chains that rely on opaque mid-stream processors — particularly those linked to shadow or non-bank finance — face the highest compound risk: CBAM cost escalation, bank credit tightening, and potential collateral ineligibility for lenders subject to the ECB's climate haircut regime.

Winners: EU-domiciled firms and project developers with integrated emissions data, CBAM authorisation systems, low-emission supply chains and diversified bank relationships whose lenders can demonstrate stress-test resilience. These firms effectively carry a lower CBAM-adjusted cost base and a more favourable credit risk profile simultaneously.

Geopolitical and geoeconomic overlay

CBAM is, structurally, a geoeconomic instrument masquerading as a climate policy. By pricing embedded carbon at the border, it rewards regulatory alignment with EU standards and penalises divergence, creating a carbon-adjusted terms-of-trade differential between the EU and major goods exporters. For China, the dominant supplier of aluminium, solar components and battery mid-stream processing. The choice is between absorbing the CBAM cost in margins, investing in low-emission production, or ceding market share in EU-bound supply chains.

The ECB's concurrent move to integrate geopolitical risk into the 2026 reverse stress test makes this link explicit at the bank level: supply-chain disruption and carbon-cost escalation driven by geoeconomic fragmentation are the precise scenarios that institutions are being asked to internalise in their capital planning. This alignment between trade policy and supervisory expectations is not coincidental. It reflects a deliberate EU strategy to hard-wire energy and industrial security into financial regulation.

For investors, the geoeconomic overlay implies that transition risk cannot be assessed at the asset level alone. The jurisdictional mix of a project's supply chain, the regulatory alignment of its financiers, and the supervisory health of the banks providing credit all determine the actual risk-adjusted return. Portfolios that treat these as secondary factors behind deployment volumes and subsidy support are mis-allocating risk.

Conclusion

The non-consensus takeaway is this: the energy transition's central risk in 2026 is not whether deployment continues. It will but which balance sheets end up warehousing the transition risk that CBAM and ECB supervisory capital reform are systematically flushing out of compliant channels. The structural read-across is clear: capital advantages accrue to firms and lenders that have invested in CBAM compliance, emissions data infrastructure and supply-chain diversification, and that can demonstrate this to supervisors and credit committees. The cyclical read-across is equally clear: the Q2 2026 reverse stress test submissions, the H2 2026 collateral factor implementation, and the March 2026 authorised declarant deadline are the near-term forcing functions that will reveal which participants are exposed and which are not.

Investors who reframe transition risk as a geoeconomic arbitrage, governed by regulatory regime alignment, balance-sheet quality and supervisory capital expectations will be positioned to identify the real winners. Those who continue to treat it as a sector-level ESG label will find the repricing arrives before the narrative catches up.

This article is for information and discussion only and does not constitute investment advice or a recommendation.

References

European Commission, DG TAXUD – Carbon Border Adjustment Mechanism – 2025/2026.

Coolset – How to calculate CBAM costs as an importer in 2026 – 2026.

CO2-IQ – CBAM costs for imported goods from 2026 – 2024/2025.

ECB Banking Supervision – ECB to assess banks' stress testing capabilities to capture geopolitical risk – December 2025.

ECB Banking Supervision – Supervisory priorities 2026–28 – November 2025.

ECB Banking Supervision – ECB keeps capital requirements broadly stable for 2026 – November 2025.

Banking.Vision – ECB climate factor 2026: New risk discount changes refinancing operations – August 2025.

KPMG – Reverse Stress Testing: ECB 2026 thematic stress test – 2025.

A&O Shearman FinReg – ECB to conduct geopolitical risk reverse stress test – 2025.

ECB Macroprudential Bulletin – Integrating climate risk into the 2025 EU-wide stress test – November 2025.

Green Central Banking – EU stress test reveals financial impacts of transition risks – December 2024.

Solar Heat Europe – Consultation on the CBAM extension – February 2026.

ESMC – Solar products to be included in EU CBAM – September 2025.

European Aluminium – Trade policy to protect the EU aluminium industry – February 2026.

Inside Energy & Environment – EU CBAM Commission proposes expansion to complex metal products – February 2026.

SEB Group – Capital replacement and transition arbitrage – 2021.

ScienceDirect – Geoeconomics of the transition to net-zero energy and industrial systems – 2025.