The Materiality Mirage: Why the Next Decade of Alpha Lives at the Intersection of Defence, Climate Resilience, and Critical Minerals

ESG disclosure scores measure what companies say about risk. In defence, mining, and oil and gas, the risk is set by governments and the two are not the same thing.

The financial materiality framework that has governed ESG investing for a decade was designed around a specific and quietly contested assumption: that sustainability factors move asset prices through the same channel as earnings revisions, through discounted cash flow models, cost of equity, and capital allocation decisions made by rational markets. In sectors where the state, not the market ultimately sets the terms of operation, that assumption does not hold. The result is a structural mispricing that most portfolio managers have not yet named, let alone corrected.

Why This Matters

The fiscal floor has shifted: Every major economy is now deploying permanent, treaty-bound defence budgets and resilience mandates simultaneously, this is not stimulus spending; it is a new cost of statehood.

The same 30–40 raw materials underpin all three agendas: Copper, lithium, cobalt, and rare earths are simultaneously critical to weapons platforms, grid storage, and flood-resilient infrastructure. Supply concentration risk is compounding, not diversifying.

Valuations have not caught up with the structural read: Markets are still pricing convergence assets as cyclical commodity plays or government-contract businesses. The more likely read is that a significant re-rating is waiting for a credible policy anchor and several are already in place.

The Framework and Its Assumptions

The Sustainability Accounting Standards Board (SASB), established in 2011 and absorbed into the IFRS Foundation in 2022, built its architecture around a single governing idea: financial materiality. Specifically, SASB standards aim to identify the subset of ESG issues "likely to influence a company's financial condition or operating performance," and to surface those issues through standardised disclosure to investors. The framework was modelled deliberately on the Financial Accounting Standards Board, producing 77 industry-specific standards organised around five sustainability dimensions: environment, social capital, human capital, business model and innovation, and governance.

This is, in the abstract, a coherent and useful exercise. The SASB materiality map for oil and gas exploration and production, for example, runs to 10 disclosure topics and 27 separate accounting metrics. For a sector defined by emissions intensity, water use, and land disturbance, those metrics capture real operational risk. The problem is not the framework's internal logic. The problem is its boundary conditions: SASB, like every major ESG framework, treats materiality as something that flows from markets to companies, as a commercial feedback loop between a firm's activities and the price signals investors send back. In defence, mining, and hydrocarbons, the dominant feedback loop runs through the state, not the market.

How Policy Overrides the Model

Source: MOFCOM Announcements

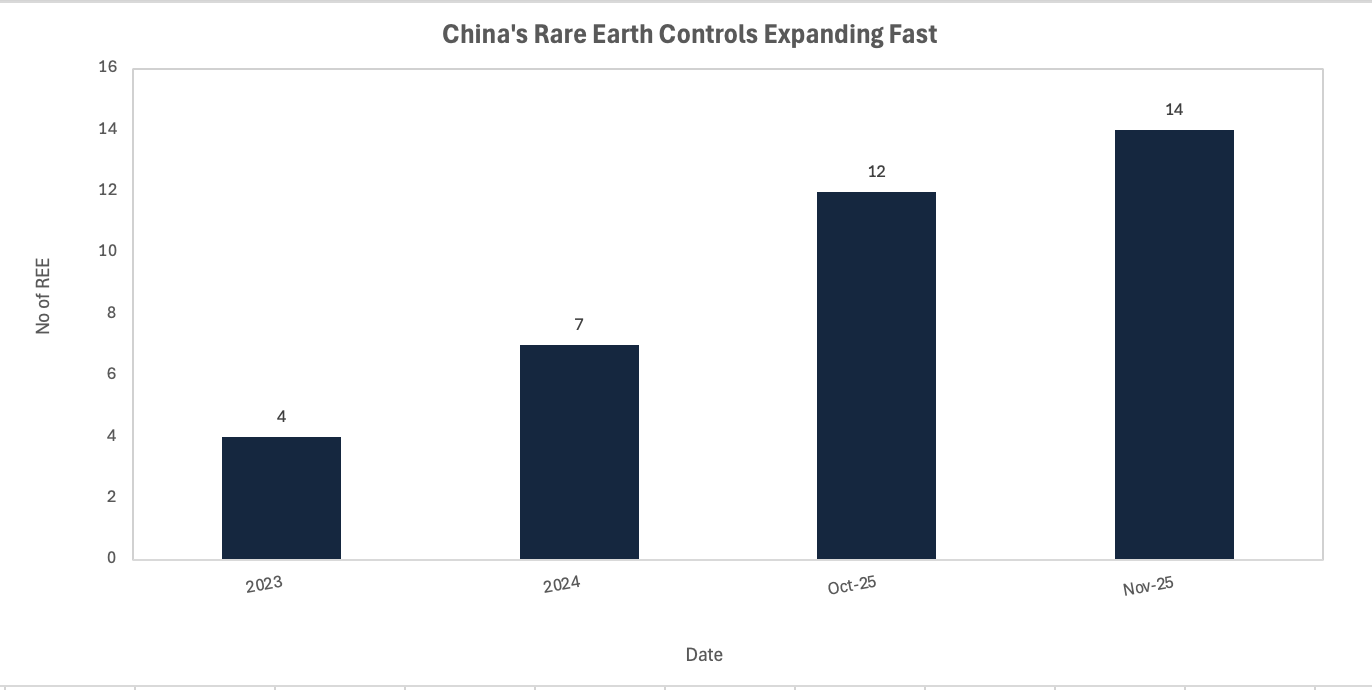

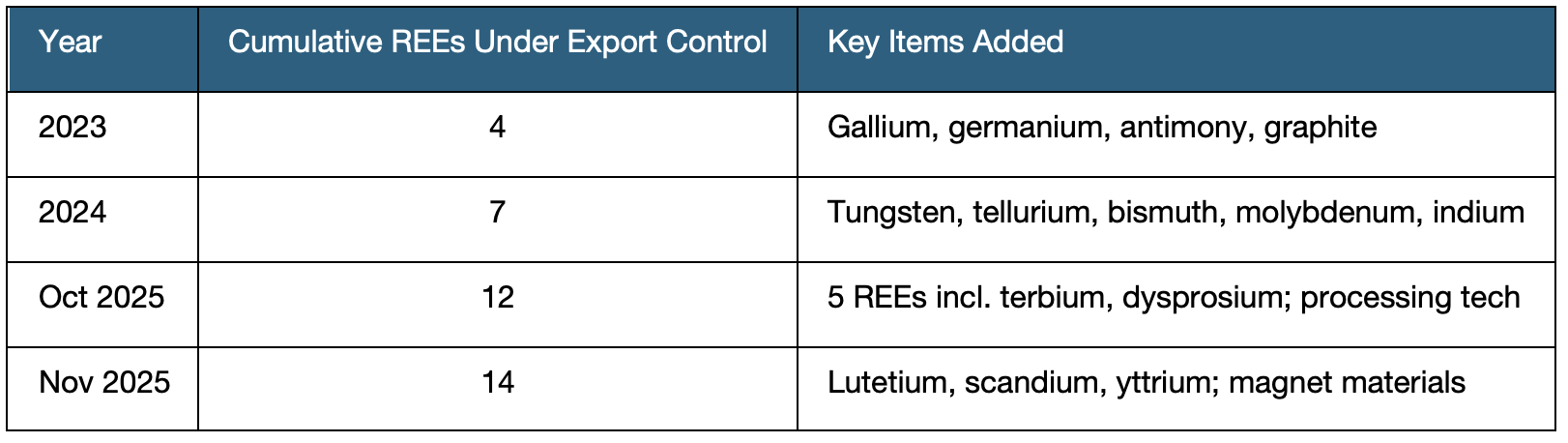

On 9 October 2025, China's Ministry of Commerce issued Announcements No. 61 and 62, expanding its rare earth export control regime to cover 12 of the 17 rare earth elements, including five new additions: terbium, dysprosium, gadolinium, europium, and ytterbium. Critically, the expansion went beyond the elements themselves. China's Announcements No. 55 through 58, entering force on 8 November 2025, extended controls to rare earth processing equipment, auxiliary chemicals, and raw materials used in separation and metallurgical refining. The regime also introduced what practitioners quickly labelled the "0.1 per cent rule": products manufactured abroad that contain Chinese-origin rare earth materials exceeding 0.1 per cent of total value per independently usable unit may also require MOFCOM export approval before onward sale to a third country. A Western defence contractor manufacturing permanent magnets for missiles or radar systems is now, in principle, subject to Chinese export licensing, regardless of where it operates.

This is not a disclosure event. It does not appear in a company's SASB-aligned sustainability report. Terbium and dysprosium are essential for the high-performance permanent magnets used in precision-guided weapons, electric motors, and wind turbine generators. Their restriction is a sovereign act of industrial policy, executed through export control law, and it reshapes the cost structure, supply-chain geography, and strategic risk of every defence and energy-transition manufacturer that sources from China. No ESG score captured that in advance. The broader export control architecture remained largely intact even after China's temporary suspension of some October measures in November 2025, with Announcement 18's additions to the controlled list continuing without interruption.

The CBAM Parallel

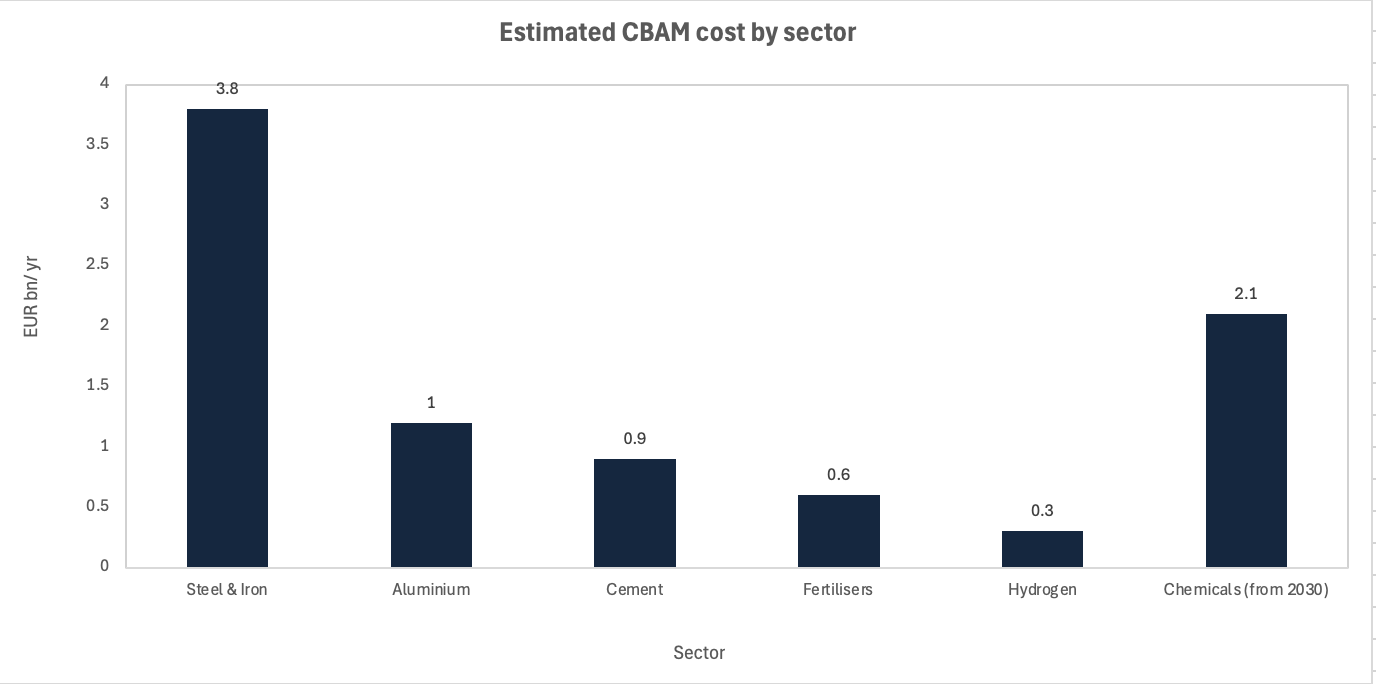

The EU's Carbon Border Adjustment Mechanism provides a second, structurally distinct illustration of the same underlying problem. CBAM entered its definitive compliance phase on 1 January 2026, having completed a transitional reporting-only phase that ran from October 2023 through December 2025. Importers of steel, iron, aluminium, cement, fertilisers, and hydrogen are now required to purchase CBAM certificates priced at the prevailing EU Emissions Trading System (ETS) carbon rate, currently approximately EUR 70 per tonne of CO2 equivalent. The scope expands further: organic chemicals and polymers, covering large swathes of oil and gas downstream activity, are being phased in from 2026, with full extension to all ETS-covered product groups expected by 2030.

CBAM is neither a corporate governance event nor a voluntary climate initiative. It is a carbon tariff, legislated through the EU's "Fit for 55" package and enforced through the EU customs union, with non-compliance fines linked to the weekly average ETS carbon price. The pricing signal did not originate in the ESG framework. It originated in a policy architecture designed by the European Commission to prevent carbon leakage and level the competitive playing field between EU producers and lower-cost foreign competitors. A steel manufacturer importing into Europe now faces a mandatory, non-negotiable cost line that did not exist three years ago, a cost line calibrated not to its ESG disclosure score but to its embedded emissions and the political economy of EU industrial policy. The disclosure score and the certificate cost are measuring different things.

Source: EU Commission estimates based on EUR70/ tonne ETS price

Investor Implications

The structural gap between financial materiality and what might more precisely be called market materiality — the set of factors that actually move prices, allocations, and operating conditions in real-asset sectors — has created a specific and underappreciated exposure in institutional portfolios. Investors who screened out defence on ESG grounds over the past decade did not avoid risk; they avoided a sector that is now attracting sovereign capital, benefiting from emergency NATO spending commitments, and commanding strategic premium in an era of supply-chain militarisation. The more likely read is that ESG screens, applied without a framework for policy-set pricing, have generated return drag without a corresponding reduction in systemic risk. The sector's RUSI-assessed "high" ESG risk rating of 34 per cent compared with 20 per cent for all other industries reflects weapons systems and human-rights considerations, not the supply-chain control risk that China's October 2025 announcements made explicit.

The mining sector presents the same problem from a different direction. SASB's metals and mining standards produce rigorous disclosure on water consumption, tailings management, and community relations. These are genuine operational risks. But they do not capture sovereign resource nationalism, export control regimes, or the reorientation of critical mineral supply chains driven by the US State Department's 2026 Critical Minerals Ministerial, which explicitly framed rare earths as a national security vulnerability following China's 2025 restrictions. An investor holding a critical minerals producer on the basis of its ESG disclosure quality is holding an asset whose primary re-rating catalyst is geopolitical, not operational. The ESG score measures what the company says about its tailings pond. The market is pricing the state's willingness to fund, protect, or restrict the mine.

For oil and gas, CBAM formalises the dynamic. Embedded carbon is now a tariff-able characteristic of a physical product, priced by a sovereign body, and enforced at the border. That is not a market-priced risk. It is a legislated cost that sits above and outside the company's own disclosure obligations. SASB requires detailed Scope 1 emissions disclosure across five categories including flared hydrocarbons and fugitive emissions. The disclosure, however rigorous, does not change the CBAM certificate cost. The certificate cost is set by the ETS auction, which is set by EU climate policy, which is set by member state negotiation and the European Commission's decarbonisation mandate. The chain of causation runs through Brussels, not through the sustainability report.

Near-Term Catalysts and Policy Outlook

The next twelve months are asymmetric: the upside scenarios for policy tightening are more numerous, more concrete, and more near-term than the scenarios for policy relaxation.

0 to 3 months: The immediate watch item is the status of China's suspended October 2025 rare earth controls. The pause on the second wave of restrictions extends until 10 November 2026; the first wave controls and Announcement 18 additions remain in force. Any deterioration in US-China trade relations before November creates the credible risk of reinstatement, with no warning interval built into the regulatory architecture. For CBAM, the first definitive-phase reporting deadline arrives in early 2026, and preliminary compliance data will surface the first hard evidence of who holds unhedged certificate exposure.

3 to 12 months: The EU's CBAM scope expansion, incorporating organic chemicals and polymers, is the most significant near-term extension. For oil and gas downstream producers, this is the moment CBAM crosses from a steel-sector problem into a hydrocarbons-sector problem. Simultaneously, the 2026 US Critical Minerals Ministerial has initiated a multilateral process to build non-Chinese rare earth supply; progress will determine whether Western defence manufacturers can begin to reduce their Announcement 18 licensing exposure, or whether the vulnerability deepens.

The scenario range is wide, and the bridging observation is straightforward: policy is moving faster than portfolio construction.

Conclusion

The financial materiality framework is not wrong. It is incomplete, and the incompleteness is structural rather than accidental. SASB, ISSB, and the broader ESG disclosure architecture were built to surface risks that flow through market mechanisms: reputational cost, regulatory fines, stranded assets priced by the equity market. In sectors where sovereign actors set the terms through export controls, carbon tariffs, defence procurement mandates, and resource nationalism, the relevant materiality is political, not financial, and the pricing signal arrives through policy rather than through the market mechanism the framework assumes. The distinction matters because it changes where the analytical work needs to happen. ESG disclosure tells you what a company has reported. Policy intelligence tells you what a government is about to do. In defence, mining, and oil and gas, the second question is the one that moves the position.

The structural read-across is this: as geopolitical fragmentation accelerates and the state reclaims its role as the dominant setter of terms in strategic sectors, every real-asset framework built on financial materiality alone will systematically underprice policy risk. That is not a flaw in implementation. It is a flaw in the underlying architecture. Correcting it requires a different analytical vocabulary, one that treats export control law, carbon border policy, and sovereign industrial strategy as first-order inputs to asset valuation, not as qualitative overlays to a disclosure score. Investors who make that shift first will not be contrarian. They will simply be accurate.

References

Reuters — "China expands rare earths restrictions, targets defense and chips" — October 2025

Taylor Wessing — "China's Expanded Export Controls on Rare Earths" — October 2025

Clark Hill — "China Hits 'Pause' on Rare-Earth Export Controls and What it Means for Supply Chains" — November 2025

European Parliament Research Service — "China's Rare-Earth Export Restrictions" — November 2025

EU Commission Taxation and Customs Union — "Carbon Border Adjustment Mechanism" — 2026

ICAP — "EU CBAM enters compliance phase and outlines path ahead" — January 2026

Normative — "The EU's Carbon Border Adjustment Mechanism, explained" — 2025

RUSI — "Are ESG Standards the Scapegoat for Stalling Defence Growth?" — September 2025

SASB / IFRS Foundation — "Understanding Sustainability Accounting Standards Board Standards" — 2025

Wolters Kluwer — "SASB Standards for the Oil and Gas Exploration and Production Sector" — 2024

US Department of State — "2026 Critical Minerals Ministerial" — February 2026

CSIS — "Critical Minerals: Research & Analysis" — May 2026

This article is for information and discussion only and does not constitute investment advice or a recommendation.