Geopolitics Is the Unmodelled Variable Sitting Inside Every Value Chain

The firms that map it will define the research standard for the next cycle.

The most important risk in a portfolio today is not on any factor model. It has no beta, no volatility surface, and no credit spread. It is the geopolitical architecture underneath the value chain — and it is being reconstructed faster than capital allocation frameworks are built to absorb.

Why This Matters

Valuations still assume a world that no longer exists: Most discounted cash flow models embed supply-chain cost assumptions built on the post-Cold War order: frictionless sourcing, rule-based arbitration, and stable trade corridors. That order is dissolving.

The transmission channels have multiplied: Oil was once the primary geopolitical shock absorber. Today the list includes semiconductors, rare earths, battery inputs, undersea cables, and satellite infrastructure — and disruption in any one of them cascades non-linearly through modern production networks.

The research gap is not analytical: The firms that build proprietary geopolitical mapping into their investment process will systematically identify risks and opportunities that consensus-driven research cannot reach.

The Core Shift: From Peripheral Noise to Structural Variable

For three decades after the end of the Cold War, geopolitics was a second-order consideration for most allocators. Trade barriers fell steadily, cross-border capital flowed on price signals alone, and the assumption underpinning globalisation that commercial integration would moderate political conflict, held well enough to be institutionalised in valuation practice.

That assumption no longer holds. The evidence is no longer disputed. A CEPR study published in February 2026 found that geopolitical risk now functions as a core strategic variable, shaping investment, sourcing, and production decisions across multinational firms. The post-Cold War framework, built on peripheral geopolitics, has given way to a world in which political friction directly alters cash flow trajectories.

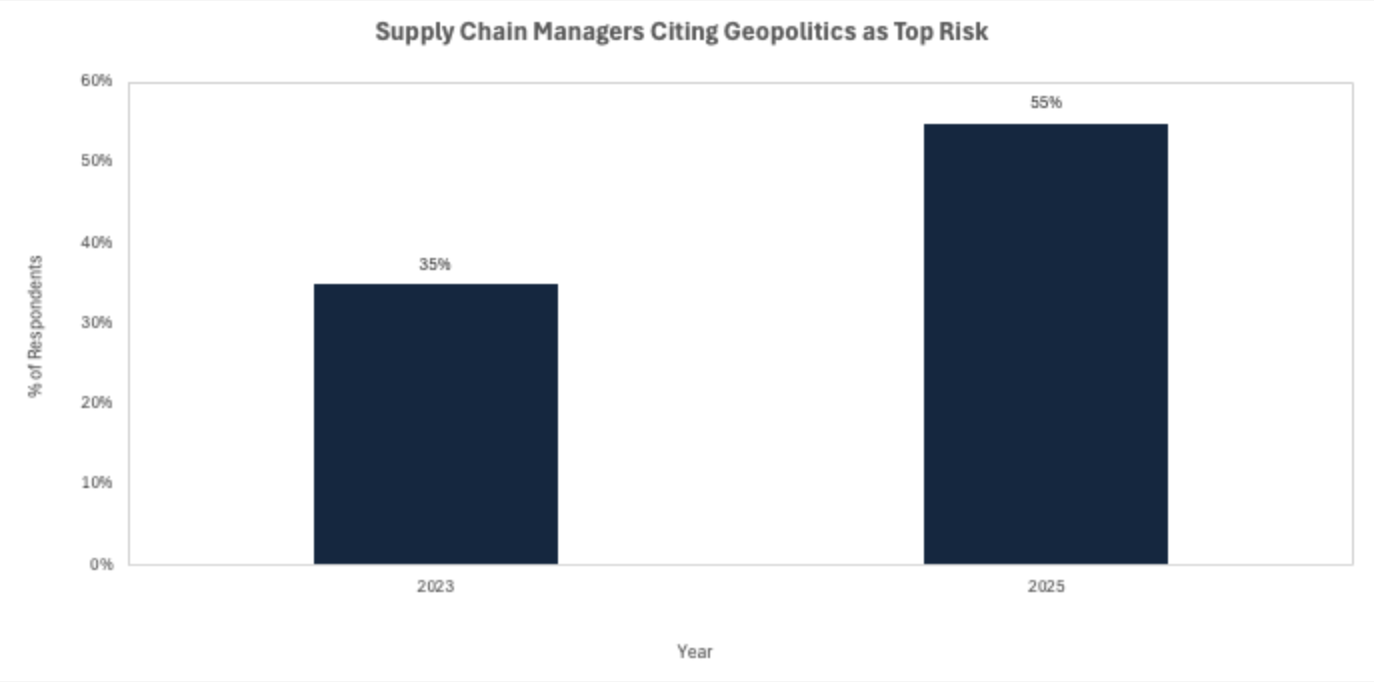

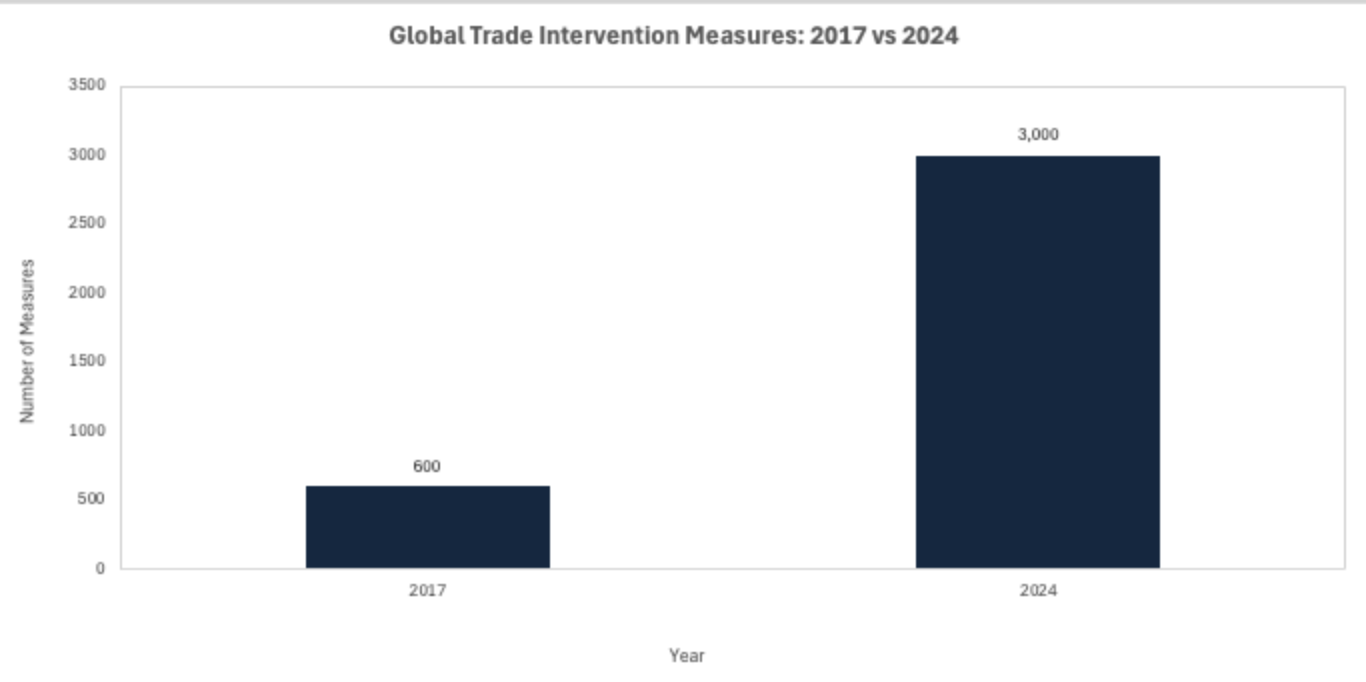

The numbers reinforce the structural nature of the shift. Global trade intervention measures rose from roughly 600 in 2017 to more than 3,000 by 2024, a fivefold increase in seven years. Among supply chain managers surveyed in 2025, 55% cited geopolitical factors as their top concern, up from 35% just two years earlier. These are not cyclical spikes; they reflect the cumulative effect of the US-China trade war, the weaponisation of energy infrastructure in the Russia-Ukraine conflict, Red Sea routing disruptions, and a broadening regime of export controls and investment screening.

The share of supply chain managers identifying geopolitical risk as their primary concern rose from 35% in 2023 to 55% in 2025. The acceleration reflects accumulated policy actions, tariffs, export controls, and sanctions rather than any single event. Source: Risk Management Magazine, 2025.

The Non-Obvious Mechanism: Value Chain Topology as Hidden Risk Exposure

The consensus view of geopolitical risk focuses on headline events: a tariff announcement, a diplomatic rupture, a conflict escalation. This is the wrong unit of analysis. What matters for investors is not the event itself but the topology of the value chain through which the shock propagates.

A firm with 40% of its component sourcing routed through a single geography sits on a fundamentally different risk profile from one with distributed nodes, even if their reported financials look identical. The risk is structural, not cyclical and it is invisible to any model that treats supply chain as a black box. MSCI research has found that high geopolitical risk is associated with lower equity returns and higher forecast volatilities over the past 30 years, and that geopolitical risk measures provide information beyond the VIX particularly for the energy, materials, and consumer services sectors. The more likely read is that standard volatility measures are systematically late to price geopolitical topology risk because they capture market sentiment, not underlying operational exposure.

The second-order effect that consensus has not followed to its conclusion concerns working capital. As firms respond to geopolitical fragmentation by building higher inventory buffers near consumption points, the capital tied up in working capital rises structurally across entire sectors. This is not a temporary efficiency loss; it is a permanent reallocation of capital from productive deployment to buffer stock. The firms that map which of their portfolio companies are most exposed to this dynamic will identify balance sheet stress before it surfaces in earnings.

Trade intervention measures rose from approximately 600 in 2017 to more than 3,000 by 2024, driven by tariffs, export controls, investment screening, and sanctions regimes. The compounding effect on supply-chain operating models is not yet fully reflected in sector valuations. Source: Delphos Insights, 2026.

Investor Implications: Mapping the Capital Reallocation

The structural disruption of value chains by geopolitics creates identifiable winners and losers but the investment case is more nuanced than a simple beneficiary list. Morgan Stanley's Institute for Sustainable Investing noted in April 2026 that a multi-year global capital expenditure cycle has begun, and that the most durable opportunity lies in owning the enablers of a more complex, distributed system: capital goods firms tied to automation, engineering and logistics providers facilitating regional diversification, and energy and resource infrastructure supporting more localised production.

The cash flow implication is threefold. First, margins for firms that have not restructured their supply chain topology will compress as input cost volatility rises and buffer stock requirements increase. The cost is not a one-time write-down; it compounds annually. Second, the cost of capital rises asymmetrically: firms with concentrated geopolitical exposure face higher equity risk premia, while those with demonstrated supply chain resilience attract a structural premium that is not yet systematically priced. Third, timing risk is material. A one standard deviation increase in geopolitical tensions reduces bilateral cross-border capital allocations by 15%, a liquidity effect triggered entirely by political friction, independent of underlying fundamentals.

The balance sheet question is equally important. Geopolitical risks erode resilience through client concentration and inventory liquidity deterioration, with non-state-owned firms showing particular vulnerability. For investors in private markets, this makes supply chain topology diligence a prerequisite rather than a nice-to-have. The firms that have not conducted this mapping are not managing this risk, they are carrying it without knowing.

What is not yet reflected in valuations is the full cost of sustained fragmentation. Markets have priced the headline events. They have not priced the cumulative operational cost of a world in which supply chain resilience requires active management rather than passive assumption.

Near-Term Catalysts and Policy Outlook

The near-term risk asymmetry is skewed towards further fragmentation rather than stabilisation: the policy instruments of geopolitical competition, tariffs, export controls, investment screening, and industrial subsidies are entrenched across multiple administrations and jurisdictions, and no electoral cycle in any major economy currently offers a credible path back to the post-Cold War trade architecture.

0–3 month window: US tariff policy under the Trump administration remains the most immediate variable. Further escalation or selective carve-outs will directly affect component cost models in sectors including consumer electronics, automotive, and capital goods. Separately, the EU's Carbon Border Adjustment Mechanism (CBAM) is introducing a new compliance dimension into supply chain traceability, with the full levy phase commencing in 2026.

3–12 month window: The more consequential dynamic is the acceleration of supply chain rewiring towards ASEAN and near-shore geographies. CEPR evidence from Japanese multinationals confirms that firms exposed to rising geopolitical tensions are actively adding import sources outside China and establishing manufacturing affiliates in ASEAN economies.

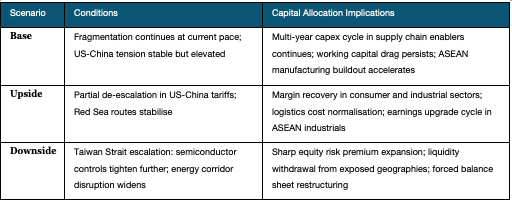

The scenarios below are offered as a structuring tool for stress-testing portfolio exposure, not as forecasts:

Conclusion

Geopolitics has not become more unpredictable; it has become more structural. The distinction matters enormously for investment practice. Cyclical risk can be hedged at the margin. Structural risk requires a different architecture of analysis, one that maps value chain topology, identifies capital exposed to sustained fragmentation, and prices geopolitical transition as a permanent feature of the operating environment rather than an intermittent disturbance.

The firms building this analytical infrastructure now are not being cautious. They are positioning for the research standard of the next cycle. Those that continue to rely on models built for the post-Cold War world are not conservative, they are carrying unmodelled risk on every line of their portfolio. The geopolitical variable is inside every value chain. The question is whether it is mapped or invisible.

References

CEPR VoxEU — "Geopolitical Risk and Supply Chain Diversification" — February 2026

Morgan Stanley Institute for Sustainable Investing — "Geopolitical Risk Is the New Normal" — April 2026

MSCI — "Understanding Geopolitical Risk in Investments" — August 2024

Risk Management Magazine — "Geopolitical Risk and Inflation Top Supply Chain Concerns in 2025" — June 2025

Delphos Insights — "Geopolitical Risk in Emerging Markets: Capital Allocation in 2026" — March 2026

Russell Investments — "From Headlines to Portfolio Impact: Investing Through Geopolitical Risk" — March 2026

S&P Global — "Top Geopolitical Risks of 2025" — February 2025

ScienceDirect — "The Rising Cost of Turmoil: Geopolitical Crises and Supply Chain Risk" — 2025

Disclaimer

This article is for information and discussion only and does not constitute investment advice or a recommendation.