Who Owns the Ground? Resource Sovereignty and the Collapse of the Western Stewardship Model in Africa

The ground beneath African mining is shifting. The Western institutional playbook, built on conditionality and engagement, is being priced out by a competitor that asks nothing but access.

African governments have entered the most consequential phase of resource nationalism in a generation. They are rewriting mining codes, enforcing local content regulations that came into effect in January 2026, and simultaneously negotiating between two very different models of capital: Western financing tied to Environmental, Social and Governance (ESG) frameworks and Chinese financing tied to infrastructure delivery. The outcome of that negotiation will determine who controls the critical mineral supply chains underpinning the global energy transition for the next thirty years. It is a structural shift that institutional commentary has almost entirely failed to track.

Why This Matters

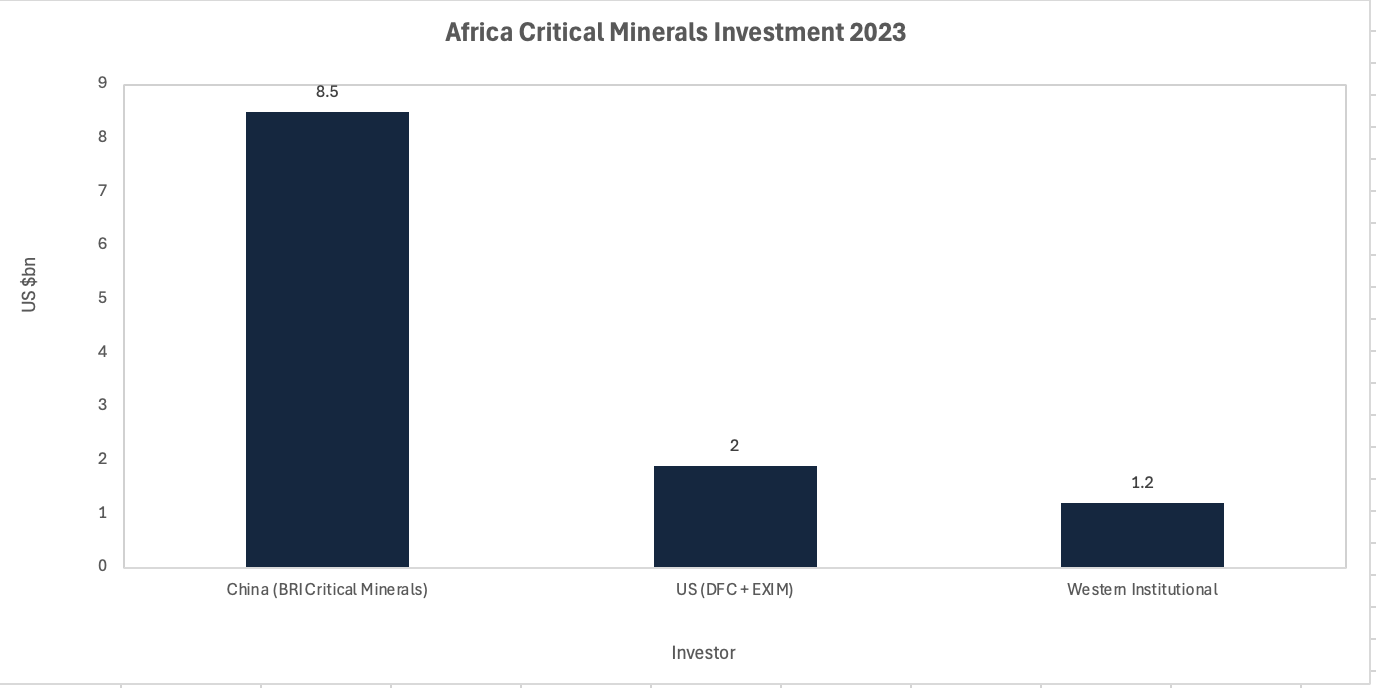

China has committed an estimated $8–10 billion to African critical mineral projects under the Belt and Road Initiative (BRI) since 2023 alone, outspending Western institutional capital in the sector by a factor of more than four to one.

African governments are no longer passive recipients: at least 13 countries have enacted export restrictions since 2023, and sweeping local content regulations came into force across Zambia, the Democratic Republic of the Congo (DRC), Zimbabwe, and Namibia in January 2026.

The Western stewardship model, predicated on ESG conditionality and board-level influence, faces a fundamental competitive disadvantage that is structural, not cyclical, and is unlikely to self-correct without a deliberate change of approach.

The Core Shift

The numbers are unambiguous. In 2023, China's total BRI economic engagement in Africa reached $21.7 billion, with between $8 and $10 billion of that concentrated in critical mineral projects across the DRC, Zambia, Botswana, Mali, Zimbabwe, and Namibia. Against that, the United States invested $7.4 billion in Africa across all sectors, with critical mineral commitments estimated at under $300 million. Western institutional capital is harder to aggregate, but the directional picture is clear: Chinese state-backed capital is outspending the Western private and quasi-public sector by a ratio that makes comparison almost redundant.

Source: Stimson Center / Griffith University BRI Investment Report 2024

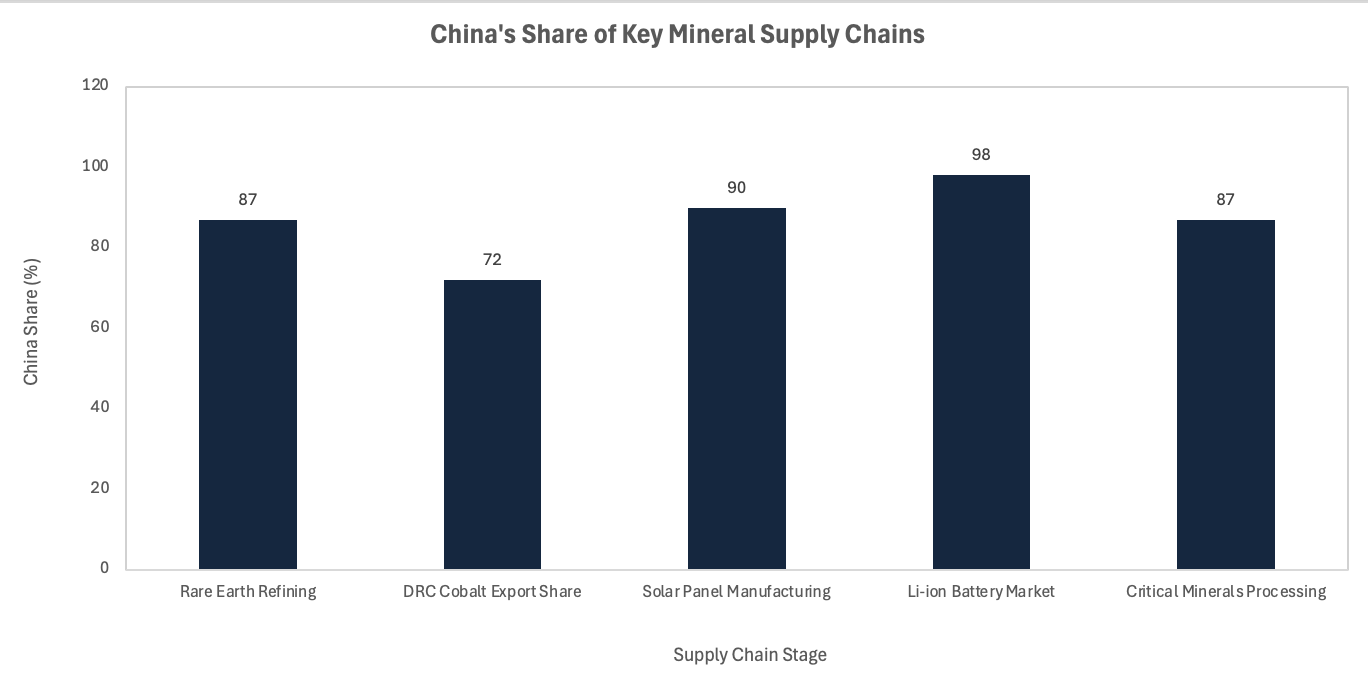

China's position is not merely financial. Chinese firms now control an estimated 87% of global critical minerals processing and refining, nearly 90% of rare earth mine-to-metal processing, and over 70% of DRC cobalt exports. Chinese companies are building one in three and financing one in five major infrastructure projects in Africa, and hold operational roles in over a third of African ports. This is not an investment thesis; it is an embedded logistics architecture. The Chinese position in African resource supply chains has long since passed the point where it can be dislodged by deal-by-deal competition.

Source: Africa Center for Strategic Studies, 2026

At the same time, African governments are not passive actors. Since 2023, at least 13 African countries have enacted export restrictions on raw minerals. Zambia's new Mining Act introduced stricter reporting requirements and expanded local participation mandates. The DRC has revised its Mining Code with tightened localisation rules, requiring more active enforcement of domestic ownership thresholds. Zimbabwe and Namibia have both moved on local content and beneficiation requirements. This wave of regulatory change is not episodic; it reflects a structural shift in the terms on which African governments are willing to grant access.

The Non-Obvious Mechanism

The conventional read is that China is winning on price: cheaper capital, fewer conditions, faster disbursement. That is partially true but misses the more important mechanism. China is winning on architecture. Through resource-backed finance (RBF) arrangements, Chinese state-owned enterprises (SOEs) have embedded themselves not just as investors but as miners, engineers, logistics operators, and long-term buyers simultaneously. The 2008 Sicomines deal in the DRC, expanded to $7 billion in 2024, granted Chinese firms 10 million tonnes of copper and 600,000 tonnes of cobalt over 25 years in exchange for infrastructure delivery. That is not a financing arrangement; it is a long-duration option on a sovereign resource base.

The consequence rarely examined is what this means for Western ESG conditionality as a mechanism of influence. ESG engagement presupposes leverage: a company requires Western capital, needs access to Western-listed markets, or depends on institutional shareholders for governance legitimacy. Strip out those dependencies and the conditionality loses its grip. Chinese financing does not require International Finance Corporation (IFC) performance standards, London Stock Exchange listing, or compliance with Equator Principles. It requires a bilateral agreement with a government that may be more interested in a railway than in a shareholder resolution. The Western stewardship model was not designed for this competitive environment, and it has not adapted.

There is a further dimension that consensus has not yet followed to its conclusion. Chinese technological investment in next-generation battery chemistry, particularly sodium-ion batteries that do not require lithium, and lithium-iron phosphate (LFP) batteries that bypass cobalt, manganese, and nickel, could materially reshape the demand curve for the very minerals over which Western institutions are now scrambling to assert influence. If those technologies scale at the pace Chinese manufacturers are targeting, cobalt-dependent supply chains become partially redundant. African countries that have locked in long-duration RBF deals priced on current mineral demand may find they have over-pledged.

Investor and Stakeholder Implications

For long-term institutional investors, the relevant question is not whether they can compete with Chinese capital for individual mining assets. They largely cannot, on cost of capital alone. The more productive question is where the structural return sits: in extraction, or in the institutions that govern it? The more likely read is that the durable value opportunity for Western capital lies in the mid- and downstream segments that China has not yet fully absorbed: refining capacity built within Africa, battery assembly, and the logistics infrastructure that connects processing to end-use markets.

African governments are themselves creating some of this opening. In 2025, the DRC and Zambia launched a joint transboundary battery and electric vehicle (EV) special economic zone (SEZ) along their shared mining belt, supported by Afreximbank and the United Nations Economic Commission for Africa (UNECA). This is a deliberate attempt to move value-add inland rather than export raw ore. The Nacala Corridor Development Project, financed by Japan, the African Development Bank (AfDB), Malawi, Mozambique, and Zambia under the Tokyo International Conference on African Development (TICAD), demonstrates that shared-financing, multi-stakeholder structures with civil society oversight and strict certification can function as a credible governance model.

The cost of capital advantage that China holds at the extraction stage does not automatically extend to more complex mid-stream industrial projects, which require technical standards, offtake certainty, and investor confidence that multilateral and Western institutions are better positioned to provide. The question for institutional capital is whether it has the patience and the structural mandate to wait for those opportunities to mature, rather than competing on terrain already ceded to Beijing.

Near-Term Catalysts and Policy Outlook

The next twelve months are asymmetric to the downside for Western governance influence: the regulatory tightening already under way will compound if Western capital does not re-engage credibly, and the window for shaping the terms of African resource governance is narrowing rather than widening.

0–3 month window (May–August 2026): The enforcement of January 2026 local content regulations across Zambia and the DRC is moving from legislative to operational. Compliance audits are beginning; companies without credible local employment and procurement plans face licence exposure. Western firms with legacy positions that relied on ESG reputation rather than structural local integration face near-term operational risk. Separately, China extended zero-tariff treatment to all 53 African countries with diplomatic ties from 1 May 2026, deepening trade integration that reinforces Chinese commercial reach.

3–12 month window (September 2026–May 2027): Several African governments are in active renegotiation of legacy RBF deals, following criticism from the African Development Bank in 2024 that such structures systematically undervalue African resources. The DRC government has faced domestic political pressure to make Sicomines terms public. Zambia's Kafue River high court case, filed in September 2025 following the Sino Metals acid spill, is expected to reach preliminary hearings. The outcome will test whether African legal systems can impose material liability on Chinese SOEs, a question with significant implications for the governance premium attached to compliant Western operators. The AU's proposed mineral-producers organisation, if it advances, would shift collective bargaining leverage meaningfully.

The scenario range reflects genuine asymmetry in where pressure is coming from:

Base case: African governments continue to enforce local content rules selectively, applying them to Western firms more readily than to Chinese counterparts with deeper political relationships. Western capital retains a niche in governance-sensitive segments but is structurally marginal to the primary extraction economy. The stewardship gap widens incrementally.

Upside: Legal and reputational pressure from the Kafue case and related environmental incidents creates a demonstrable governance premium for compliant operators. Western institutional capital, particularly from European pension funds subject to Corporate Sustainability Reporting Directive (CSRD) obligations from 2025 reporting cycles, re-engages with African mid-stream projects where Chinese firms face financing constraints. A viable alternative model begins to take shape around the DRC-Zambia SEZ structure.

Downside: US engagement under the Trump administration deprioritises Africa in favour of bilateral mineral deals with Greenland and Ukraine. Without US anchor capital, the Minerals Security Partnership loses operational momentum. African governments, frustrated by slow Western disbursement, accelerate RBF terms with Chinese counterparts on deals that further entrench long-duration supply commitments. The governance window closes faster than the base case implies.

Conclusion

The Western stewardship model has not been defeated in Africa; it has been outpaced by a competitor that understood earlier that resource access is an infrastructure problem, not a governance conversation. The structural case for re-engagement is real: African governments want leverage, they want alternatives, and several are actively constructing the institutional architecture to make multi-stakeholder partnerships viable. But the window is genuinely time-limited. The longer Western institutional capital waits for the governance environment to self-correct, the more it will find that the terms of access have already been set elsewhere, at the mine, at the port, and under the ground.

The cyclical read, that ESG conditions will eventually reassert themselves as Chinese environmental liability accumulates, is wishful. The structural read is harder: Western capital needs to accept that stewardship without competitive capital is commentary, and that the viable governance model in African resource investment is one built around mid-stream industrial co-investment, legal standard-setting, and regional institution-building, not board resolutions in London or New York. That is uncomfortable for how most institutional mandates are currently written. It is also, on the evidence, correct.

References

Africa Center for Strategic Studies – China's Critical Minerals Strategy in Africa – March 2026

Stimson Center – Competing for Africa's Resources: How the US and China Invest in Critical Minerals – May 2026

African Security Analysis – The Chinese Mining Surge in Africa: Strategic Impacts and National Risk Outlook – 2025

AHK Group – Africa Mining Regulatory Reform: What Investors Must Know – April 2026

Green Finance & Development Center – Elevating ESG: Empirical Lessons on Chinese Projects in Africa – September 2023

Law.asia – Analysis of Revised Mining Code in the Democratic Republic of Congo – May 2025

Bowmans Law – Zambia: Local Content Requirements in the Mining Sector – November 2025

Columbia Center on Sustainable Investment (CCSI) – Resource for Infrastructure Deals – November 2025

farmdoc daily / University of Illinois – China's Belt and Road Initiative in Africa – March 2026

Atlantic Council – Responsible Stewardship Models and Africa's Mineral Wealth – October 2025

Griffith University / Christopher Nedopil – China Belt and Road Initiative Investment Report 2023 – February 2024

Disclaimer: This article is for information and discussion only and does not constitute investment advice or a recommendations