The Textile Recycling Bottleneck: Why Fibre-to-Fibre Is Still a Capital Problem, Not a Technology Problem

The chemistry largely works. The economics do not. Understanding why that gap persists — and what it will take to close it — matters far more than the next laboratory breakthrough.

The fashion industry has a convenient story about textile recycling: the technology is not ready yet. Once the science matures, circularity will follow. That story is wrong, and the industry knows it. The real constraint is not chemistry; it is capital structure, feedstock economics, and the absence of a price signal that makes recycled fibre commercially viable against its virgin competitor.

Why This Matters

Less than 1% of global textile waste is recycled fibre-to-fibre (F2F) in a closed loop, not because the technology does not exist, but because the economics are structurally broken without policy intervention

Renewcell's 2024 bankruptcy, the sector's most instructive failure was not a technology collapse; it was a financing collapse, caused by an inability to secure predictable offtake and sufficient liquidity

The EU's revised Waste Framework Directive entered into force in October 2025, mandating Extended Producer Responsibility (EPR) schemes by April 2028: the first policy architecture capable of changing the cost calculus

The Core Shift

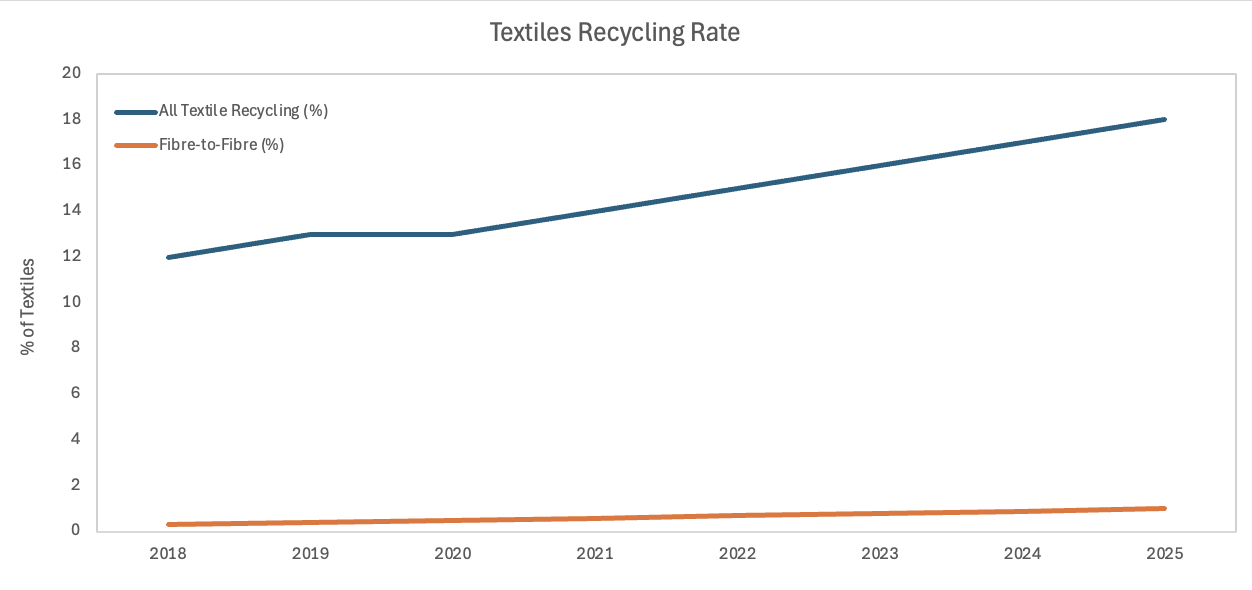

Textile recycling is not a niche experiment. Globally, the fashion industry produces roughly 92 million tonnes of textile waste annually, of which 87% is landfilled or incinerated. The recycling that does occur is overwhelmingly mechanical downcycling — shredding old garments into insulation or industrial rags — not the closed-loop F2F recovery that would actually displace virgin fibre demand. McKinsey estimated in 2022 that an 18–26% F2F recycling rate was achievable by 2030 under the right conditions, but today the global rate sits below 1%.

Global textile recycling rates — all methods versus true fibre-to-fibre closed loop, 2018–2025. The gap between the two lines is not a technology gap; it is a commercial viability gap.Sources: EU Horizon Europe Partnership documentation; McKinsey & Company, Scaling Textile Recycling in Europe, 2022

What has changed is the regulatory scaffolding. The EU's revised Waste Framework Directive, Directive (EU) 2025/1892, entered into force on 16 October 2025, establishing mandatory EPR schemes that will require producers — including non-EU brands selling via e-commerce — to fund collection, sorting, and recycling of every textile product they place on the European market. Member states have until June 2027 to transpose the Directive into national law and until April 2028 to have EPR schemes operational. This is the architecture. The price signal it creates will determine whether circularity follows.

The Non-Obvious Mechanism

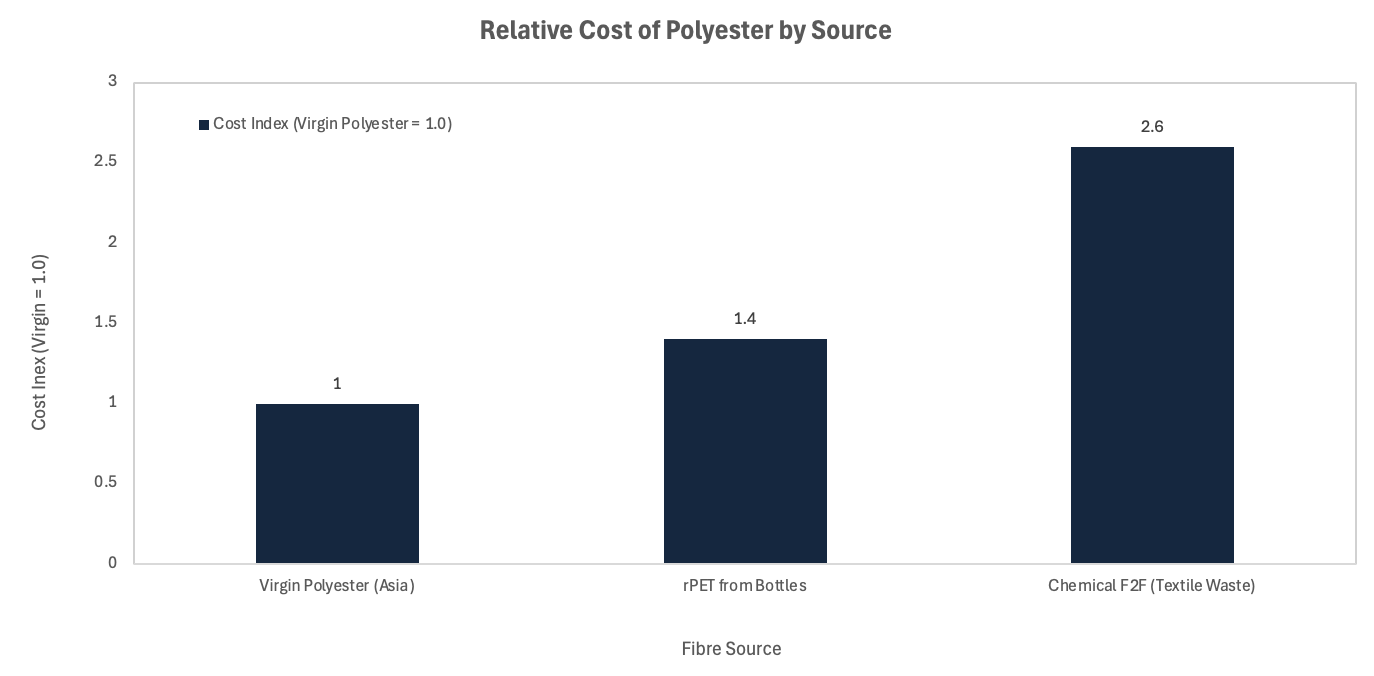

The surface explanation for why F2F recycling has not scaled is cost: chemical recycling from post-consumer textile waste currently costs approximately 2.6 times more than virgin polyester from Asia, and roughly 1.9 times more than recycled polyester derived from plastic bottles (rPET). That cost differential is real and well-documented by Systemiq's analysis and the work of Professors Corvellec and Stowell at Lund University. But focusing on cost alone misses the deeper mechanism.[4]

Relative production cost index for polyester by source (virgin = 1.0). The cost gap between F2F chemical recycling and virgin fibre is not a temporary scale disadvantage; it reflects the structural economics of feedstock preparation and process chemistry at current volumes.Sources: Systemiq analysis, Sophie Herrmann; Corvellec & Stowell, Lund University / Lancaster University, 2024

The structural problem is a double-sided market failure. On the input side, chemical recycling requires clean, consistently sorted, high-volume feedstock. Post-consumer textile waste is the precise opposite: blended fibres, mixed contaminants, unstandardised collection streams. Ali Harlin of VTT Technical Research Centre estimates that Europe could sustain at most five to ten chemical recycling plants, each needing the output of approximately ten mechanical sorting facilities to maintain adequate feedstock supply. On the output side, brands have historically been able to substitute rPET from bottles at a lower cost premium, giving them a plausible "recycled content" claim without committing to the harder and more expensive textile-to-textile route. The bottle-rPET ceiling is not a technological convenience; it is a structural subsidy to the status quo that makes F2F appear uncompetitive even when it is not, once full lifecycle costs are priced in.

Investor and Stakeholder Implications

The F2F sector has attracted over $250 million in venture investment across players including Circ, Syre, and Infinited Fiber Company. Yet aggregate funding at that level is insufficient for a capital-intensive sector that requires industrial-scale plants, each demanding consistent multi-year feedstock supply and guaranteed offtake before a bank will lend against the asset. The Renewcell bankruptcy in February 2024 is the clearest data point: the company's Circulose technology worked; what it lacked was sufficient financing to sustain operations through a period of zero sales — a month it recorded in November 2023 — while waiting for the market to develop.

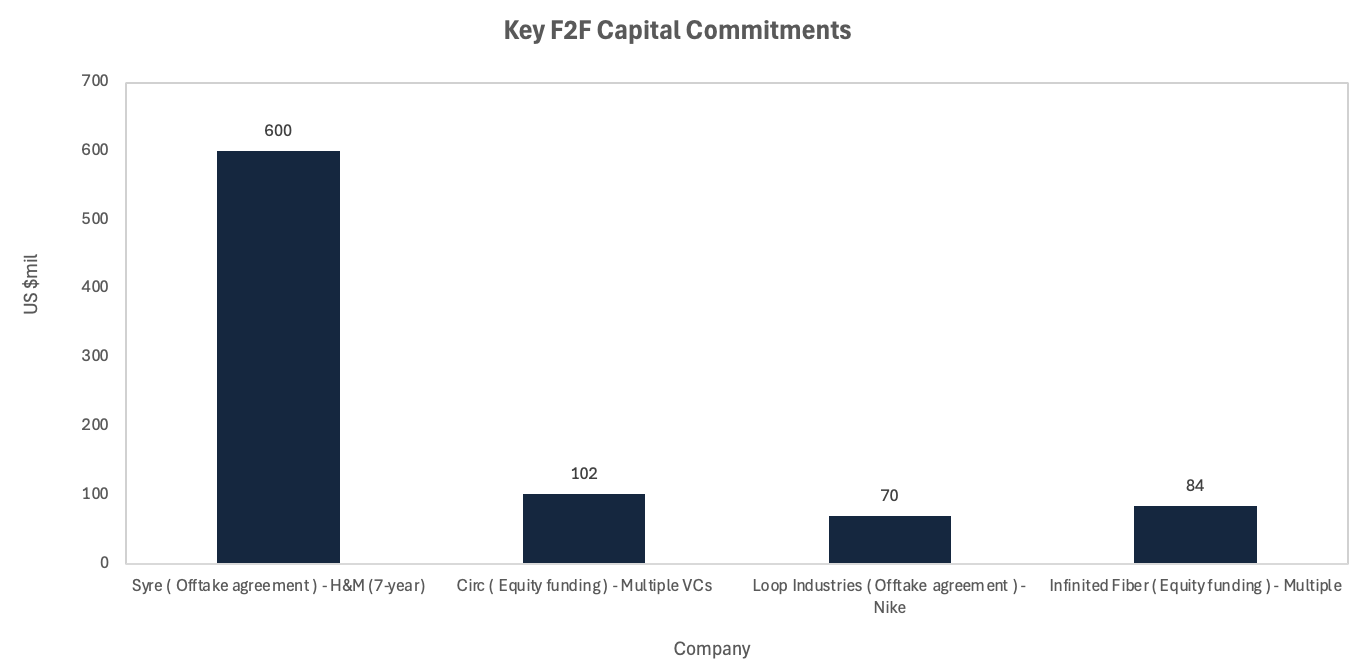

Selected F2F capital commitments and brand offtake agreements, 2024–2025 (USD millions). The offtake agreement — a long-term guaranteed purchase contract — is now the critical financing instrument, converting future recycled fibre demand into bankable revenue against which lenders can advance capital.Sources: Company announcements, 2024–2025; Forbes, November 2025; Vogue, December 2025

The implication for investors is structural, not cyclical. The players that survive the current consolidation period will be those who secured offtake agreements before regulatory mandates drove brands into a feedstock scarcity scramble. H&M's co-founding of Syre, backed by a $600 million seven-year offtake commitment, reflects a brand-level read that recycled feedstock will become strategically scarce as mandatory recycled-content targets arrive. Nike's simultaneous deals with both Syre and Loop Industries signal the same logic: diversify supply before open-market access becomes constrained. For investors in the space, the project finance playbook from infrastructure and renewables is the correct analogy: revenue certainty precedes debt capacity, and debt capacity is what builds the plant. Equity alone cannot finance this sector to scale.

The balance sheet risk is asymmetric. Brands without offtake agreements face not just regulatory non-compliance exposure under the EU's EPR framework, but material supply risk if early movers lock up capacity. The brands absorbing that risk are doing so knowingly: the more likely read of the current offtake wave is a strategic land-grab, not a sustainability gesture.

Near-Term Catalysts and Policy Outlook

The next 12 months represent the narrowest window of commercial asymmetry this sector has offered: EPR obligations are locked in, but supply is still thin and first-mover advantage in offtake capacity is real.

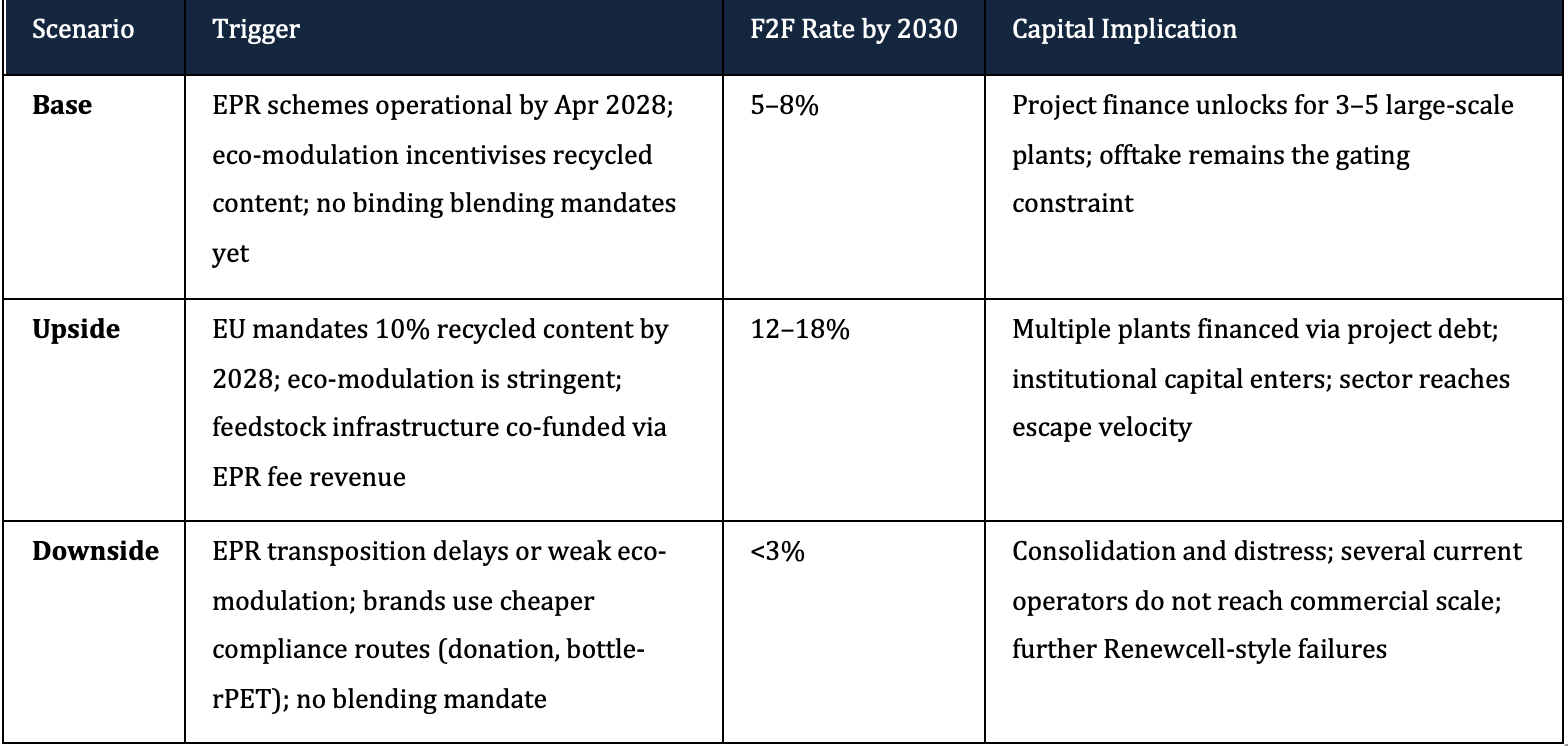

0–3 month window (May–August 2026). National transposition of the EU Waste Framework Directive is underway across Member States, with the 20-month clock running from the October 2025 entry into force. Expect early-mover jurisdictions — France, Germany, the Netherlands — to publish draft transposition frameworks. Watch particularly for the eco-modulation methodology embedded in EPR fee structures; if eco-modulation is weighted towards recyclability and recycled-content targets, it creates an immediate cost differential that changes brand procurement incentives. Separately, the EU's consideration of mandatory recycled-content requirements — 10% by 2028, 15% by 2030, 30% by 2035 — is the regulatory catalyst the sector's project financiers are waiting for. Any formal consultation launch in this window materially de-risks the investment case for plants currently in development.

3–12 month window (September 2026–April 2027). Circ's first full-scale facility, supported by over $100 million in investment and secured offtake agreements with Selenis in Portugal and Sanyou Chemical Fiber in China, is targeting commissioning. If the plant hits nameplate capacity, it will be the first large-scale data point on whether F2F chemical recycling can operate commercially rather than at pilot scale. Circulose (Renewcell's successor) is executing on binding offtake agreements with H&M, Mango, and Tangshan Sanyou, having explicitly shifted strategy away from the open-market model that preceded the bankruptcy. The feedstock question — clean, sorted, consistent supply at volume — remains unresolved for most operators. Brands that signed offtake agreements without locking in feedstock supply chains are exposed.

The structural case is that mandatory recycled-content targets, not technology improvement, determine the outcome.

Conclusion

The textile recycling sector's fundamental problem is not scientific; it is structural. The economics of fibre-to-fibre recycling cannot close against virgin polyester without a policy instrument that prices the externality — either through EPR fee eco-modulation, mandatory blending targets, or a carbon mechanism that reflects the full cost of virgin fibre production. The EU's revised Waste Framework Directive provides the first credible architecture for that pricing shift, but its commercial effect depends entirely on how Member States design their eco-modulation parameters and whether mandatory recycled-content requirements follow.

The Renewcell collapse, read correctly, is not a warning about technology risk; it is a warning about sequencing risk. The company built the plant before the market existed and before the regulatory floor was in place. The current cohort — Circ, Syre, Loop Industries, Samsara, Circulose — has drawn the right lesson: secure offtake first, then build. That is project finance logic applied to a sector that previously operated on venture logic, and it is what separates the current generation of operators from their predecessors.

The geopolitical overlay is underappreciated. Polyester production is heavily concentrated in China; virgin polyester pricing is, in part, a function of Chinese overcapacity and energy subsidies. Any F2F operator in Europe or the United States is structurally competing against a subsidised incumbent. That reality does not change with more efficient chemistry. It changes only when the policy floor raises the floor cost of the linear alternative — which is precisely what a well-designed EPR regime, combined with a carbon border adjustment, begins to do.

The sector that emerges from the current consolidation period will look less like the venture-backed textile startups of 2018–2022 and more like infrastructure: long-dated assets, contracted revenue streams, institutional debt, and returns that are modest but defensible. That is not a weakness. It is the shape of a market that has finally been properly capitalised.

References

EU Horizon Europe Partnership documentation — Circular, Biobased Textiles — 2024

McKinsey & Company — Scaling Textile Recycling in Europe: Turning Waste into Value — July 2022

Systemiq / Sophie Herrmann — The Textile Recycling Breakthrough: Why Policy Must Lead the Scale-Up of Polyester Recycling — May 2025

Corvellec, H. & Stowell, A. (Lund University / Lancaster University) — Renewcell Bankruptcy Analysis — referenced in The Fashion Globe, March 2026

European Commission — Revised Waste Framework Directive (EU) 2025/1892 enters into force — October 2025

Verdant Law — EU Adopts New Textile EPR Requirements — January 2026

Fashion for Good — Solving the Feedstock Gap: Unlocking Post-Consumer Textile Recycling — April 2026

BCG — Spinning Textile Waste into Value — August 2025

Forbes / Roomy Khan — The $20 Billion Textile Recycling Inflection: Mandates Hit and Nike Bets Big — November 2025

The Interline — Fashion and Beauty's Race to Lock In Recycled Inputs — October 2025

The Fashion Globe — Renewcell Bankruptcy Exposes the High Cost of Recycled Polyester — March 2026

Brydges et al. — Textile Recycling: Positive Change or Toxic Truth? — EU Transition Pathways, 2025

Fiber Journal — Investments Cue Optimism for Circular Textiles That Can Scale — February 2026

Disclaimer: This article is for information and discussion only and does not constitute investment advice or a recommendation.