Circularity Is Not a Strategy: Why Fashion's Capital Flows Are Still Chasing the Wrong Metrics

The industry has convinced itself that recycling programmes and resale pilots constitute a circular economy. They do not. The real problem is structural, and capital is flowing to the wrong place at the wrong time.

Why This Matters

Fashion's circularity narrative rests on a $460 billion miscalculation; the economic assumptions underpinning current business models do not survive basic scrutiny.

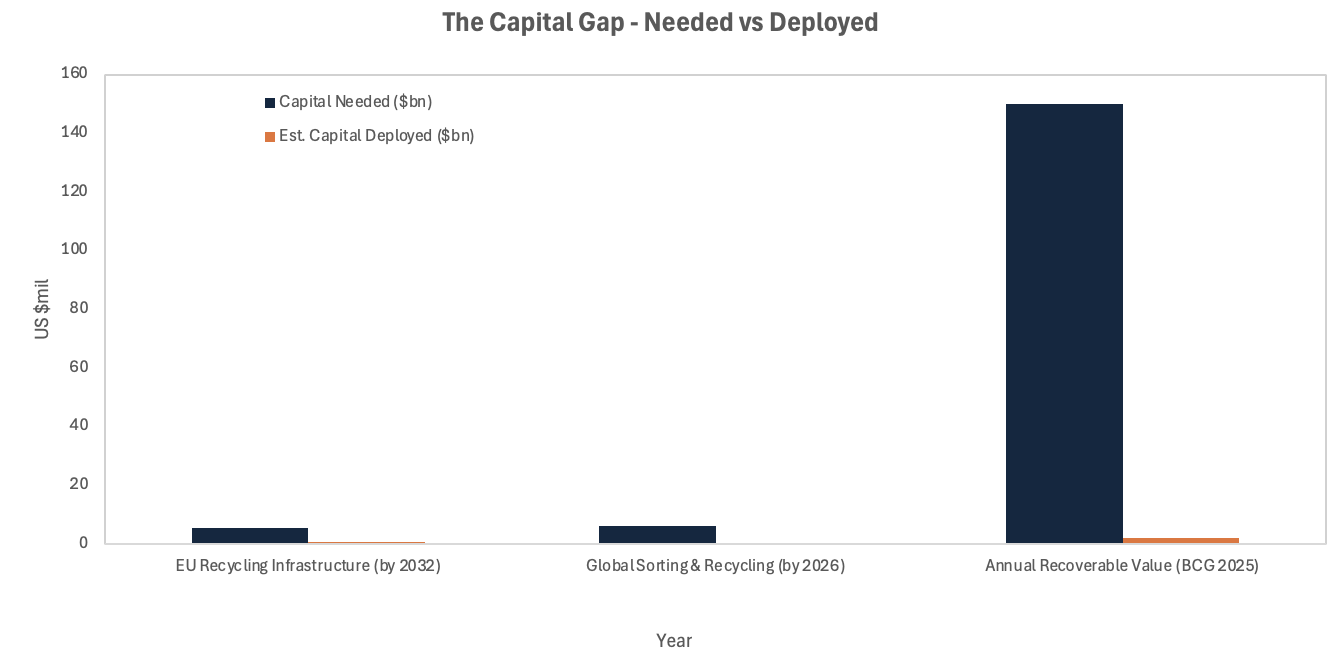

Under 1% of global textile waste is recycled into new fibre; the infrastructure to change that requires $5–7 billion, which has not been committed.

European regulation is tightening fast: brands that have treated circularity as a marketing signal face hard compliance costs from July 2026, not a reputational soft landing.

The Core Shift

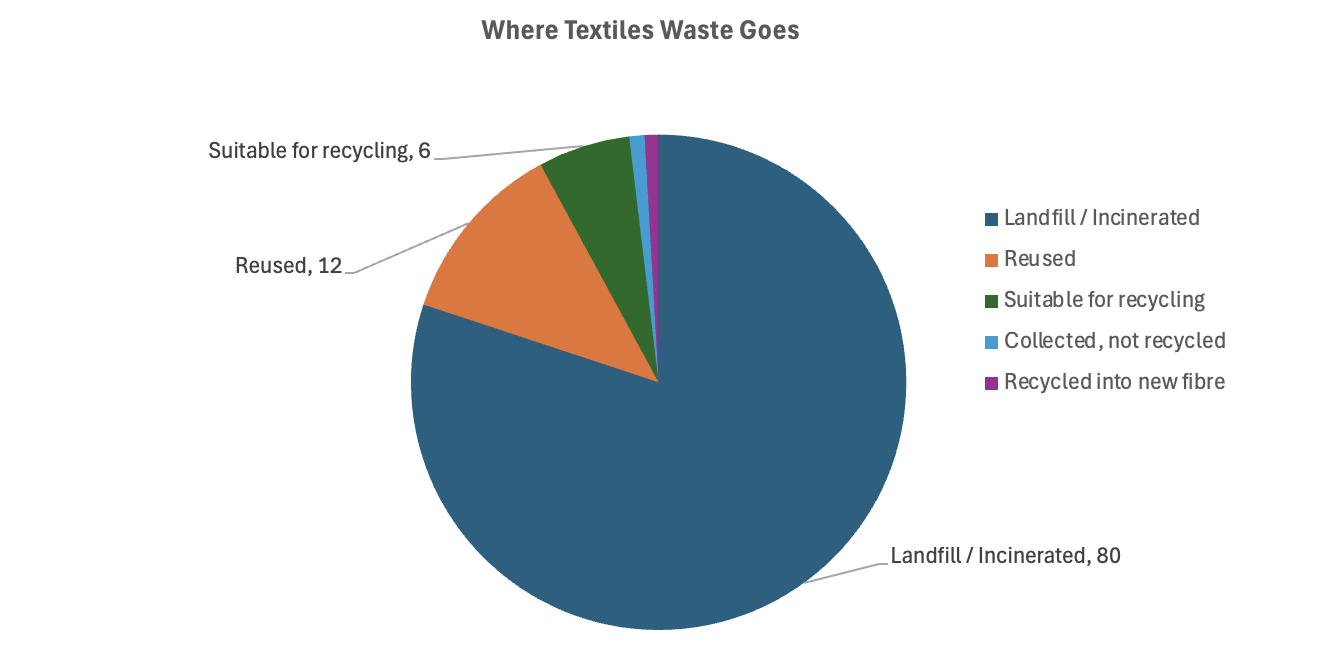

The global fashion industry generates roughly 120 million metric tons of textile waste annually, of which 80% ends up in landfill or is incinerated. Less than 1% is processed back into new fibre. That figure has not materially moved in a decade despite a proliferation of sustainability commitments, take-back schemes, and recycled-content targets. The uncomfortable read is that circularity in fashion has functioned primarily as a marketing construct, not a production discipline.

What is changing is the regulatory environment, not the industry's voluntary behaviour. The EU's Ecodesign for Sustainable Products Regulation (ESPR) entered into force in July 2024, making textiles one of its first priority product categories. From 19 July 2026, large companies face a binding ban on the destruction of unsold apparel, accessories, and footwear. This is not a target; it is a prohibition with national authority oversight. Overproduction, which the industry has never seriously addressed, is now a compliance risk, not merely a reputational one.

Source: BCG, Spinning Textile Waste into Value, August 2025

The Non-Obvious Mechanism

The standard circularity narrative identifies the problem as insufficient recycling infrastructure and points to investment in sorting and processing capacity as the solution. That is half the story, and it is the less important half. Research published in Frontiers in Sustainability found that the $500 billion economic savings figure repeatedly cited by the Ellen MacArthur Foundation and McKinsey to justify circular fashion investment overstates the benefit by roughly $460 billion. Circular business models such as resale and rental generate lower margins than new production; if they succeed in reducing new production, revenues contract; if they merely supplement it, environmental benefits are negligible. Either outcome undermines the investment thesis as currently constructed.

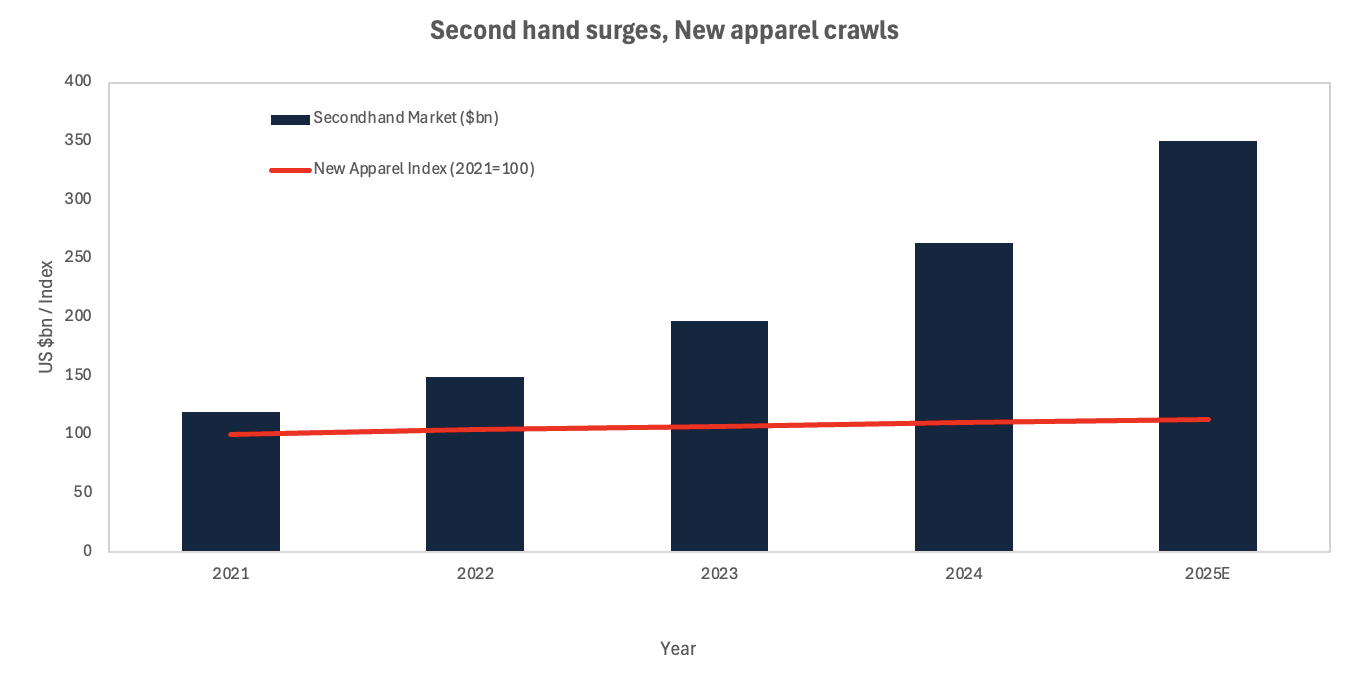

The second-order effect consensus has not followed to its conclusion is this: the growth of secondhand and rental markets is real and accelerating, with global secondhand apparel reaching an estimated $350 billion in 2025, growing two to three times faster than new clothing sales. But that growth is not reducing total clothing volumes produced. Fast fashion continues to expand production, using the secondhand market as a reputational halo while inventory cycles shorten. Resale is growing alongside new production, not instead of it. The rebound effect, familiar from energy economics, is operative here: lower cost-per-wear encourages more total consumption, not less.

Sources: ThredUp, Bain & Company

Investor Implications

Capital allocation in fashion circularity faces a structural mismatch. The $5–7 billion needed globally to build industrial-scale sorting and recycling infrastructure has not been committed, yet the EU has simultaneously mandated separate textile collection across all member states effective January 2025. The resulting deadlock is familiar: recyclers will not invest in capacity without guaranteed offtake from brands; brands will not commit to offtake without existing recycled fibre supply at cost parity. Both are waiting for the other to move first. This is not a failure of technology or awareness; it is a prisoner's dilemma that only regulatory compulsion or patient capital with long time horizons can break.

The cost of capital implications are not yet reflected in most fashion valuations. Extended Producer Responsibility (EPR) schemes expected across the EU by 2026–2027 will introduce fee structures that internalise disposal costs brands currently externalise. For businesses running high inventory-to-sales ratios, the liability embedded in unsold stock has just changed character. Analysts pricing these companies on gross margin trajectories and comparable-store sales are, in the structural case, looking at the wrong metrics.

The investors better positioned in this transition are those with exposure to: industrial sorting and mechanical recycling firms where EPR fee flows will create stable revenue visibility; brands with low inventory buffers and design-led demand generation that insulates them from the overproduction compliance risk; and logistics operators building reverse supply chain capacity, which remains underinvested across every major market.

Sources: BCG / EU Commission / industry estimates

Near-Term Catalysts and Policy Outlook

The risk asymmetry over the next 12–18 months is skewed to the downside for brands that have treated circularity commitments as reputational insurance rather than operational planning. The ESPR unsold goods ban on large companies takes effect in July 2026; brands without compliant inventory protocols and documented alternatives to destruction face enforcement exposure immediately. The EU Commission's standardised disclosure format for unsold consumer goods applies from February 2027, and many existing enterprise resource planning systems cannot generate the required disclosures at the required granularity.

Over the 3–12 month window, EU member states are transposing EPR obligations at different speeds, creating short-term jurisdictional arbitrage that will narrow by 2027. Brands that engage early in EPR scheme governance stand to shape fee structures in ways that favour their existing models; those that wait will inherit obligations they did not negotiate. The Digital Product Passport (DPP), which requires lifecycle and sustainability data accessible across the value chain, will reshape sourcing due diligence standards from 2027 and create a new tier of supplier risk, particularly at tier-two and tier-three in South and Southeast Asia.

The current policy trajectory, absent a reversal of enforcement intent, points to the following scenario range. The base case assumes EPR fees introduced by 2027, partial DPP compliance, and recycled fibre supply growing but remaining below cost parity with virgin material: mid-tier fast fashion margins compress by 200–400 basis points and recycling infrastructure firms attract capital at premium multiples. The upside case, contingent on EPR fees catalysing the $5 billion-plus infrastructure commitment and long-term brand offtake agreements, would unlock an estimated $50 billion or more in annual recoverable raw material value, creating a viable asset class in circular textiles bonds. The downside case is enforcement inconsistency across member states, brands absorbing EPR fees without changing production volumes, and circularity discourse collapsing into compliance theatre, with institutional capital retreating to safer adjacent ESG plays.

Conclusion

The structural case on fashion circularity is not that the industry is on the wrong path; it is that the path optimises for the wrong variable. Recycling rates and resale market size are outputs of a functioning circular system, not proxies for one. Capital chasing those metrics is, at best, early in a long cycle; at worst, funding rebranded linearity. The real signal to watch is who commits capital to the unsexy middle of the value chain: sorting infrastructure, EPR governance, and offtake agreements for recycled fibre. That is where the durable transition gets funded or, if capital stays in the front-end, where it stalls.

The geopolitical overlay matters here too. The EU is setting the global compliance standard by market weight, but manufacturing remains concentrated in South and Southeast Asia. The DPP will, in practice, impose EU lifecycle accounting standards on suppliers who have no regulatory incentive to build that data capability except as a condition of market access. The transition cost will be borne unevenly. Brands and investors that have mapped their supply chain exposure at tier-two and tier-three level will absorb it more efficiently. Those who have not are carrying a risk that does not yet show in their disclosures.

References

BCG – Spinning Textile Waste into Value – August 2025

Loughborough University London / Frontiers in Sustainability – Circular Fashion Economic Analysis – March 2025

FashionUnited – The Myth of Circular Fashion Economics: A $450 Billion Miscalculation – March 2025

EU Commission – ESPR Unsold Goods Delegated Act – February 2026

EU Commission / justfashionproject.eu – ESPR Implementation Roadmap – January 2026

EU Textile Waste Directive / EPR Updates – January 2025

ThredUp / Bain & Company – Secondhand Apparel Market Sizing – 2025

Sustainability Directory – Infrastructure Funding Gap Delays Textile Recycling Goals – September 2025

UKFT – CFIN Report 2025 – October 2025

HM Foundation – Why Fashion Is Less Circular Than Ever – March 2026

Disclaimer

This article is for information and discussion only and does not constitute investment advice or a recommendation.