The Market Is Growing. The Margins Are Not. What Resale Gets Wrong About Its Own Investment Case

The secondhand market is one of the fastest-growing segments in consumer goods. That growth is real, verifiable, and structural. The investment case built on top of it is something else entirely.

Why This Matters

The resale market reached $256bn in 2025 and is growing at over 12% annually — but most platforms extracting value from that growth are not profitable.

GMV (Gross Merchandise Value) is the metric the sector leads with. It is not revenue. Revenue is not profit. Family offices conflating the three are buying the narrative, not the business.

The most durable value in this sector is not sitting in the platforms. It is accumulating in the infrastructure layer — authentication, logistics, and the brands that own the original supply.

The Core Shift

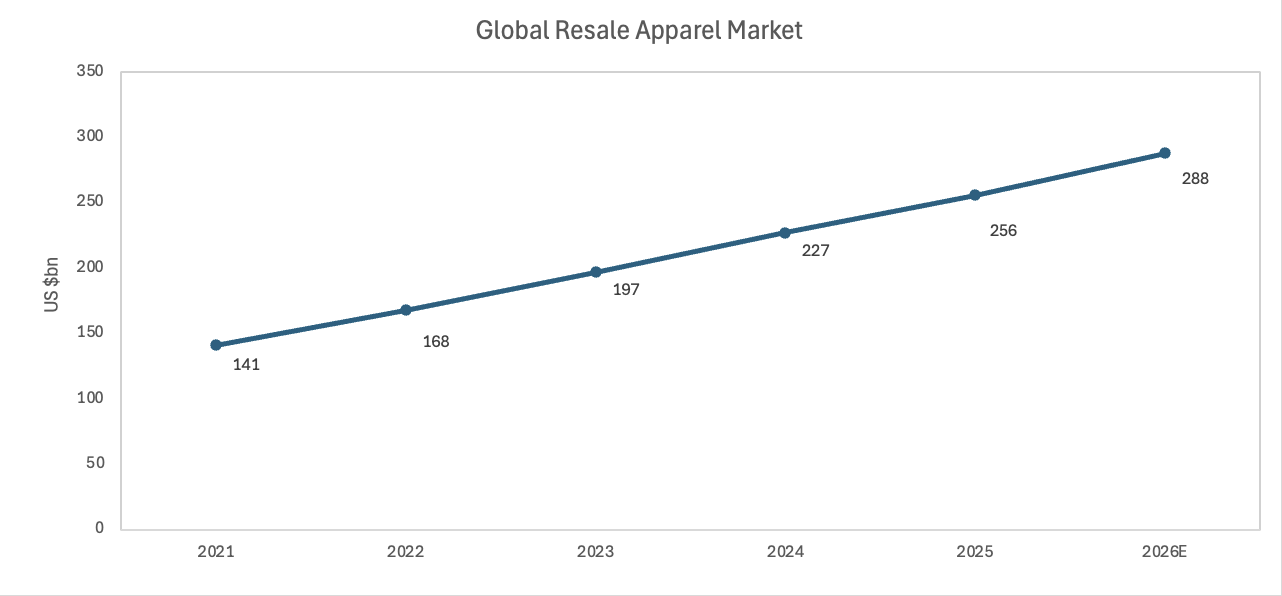

The global secondhand apparel market grew from $141bn in 2021 to $256bn in 2025, an 82% increase in four years. ThredUp forecasts a further 12.5% rise to $288bn in 2026. Extend that to the broader secondhand product market and the figures are larger still: $475bn in 2025, projected to reach $854bn by 2030 at a compound annual growth rate (CAGR) of 12.4%.

The structural drivers are not subtle. A generation of consumers has been conditioned to see secondhand as aspirational rather than compromised. Inflation and tariff pressure have made price-conscious shopping socially acceptable at every income level. EU sustainability regulation, including the incoming digital product passport (DPP), is beginning to formalise the resale economy as policy infrastructure, not just consumer preference. These forces do not reverse easily.

Structural growth across the second-hand apparel sector. 82% expansion from 2021 to 2025, with momentum continuing into 2026E. Source: ThredUp Resale Report 2026

The Non-Obvious Mechanism

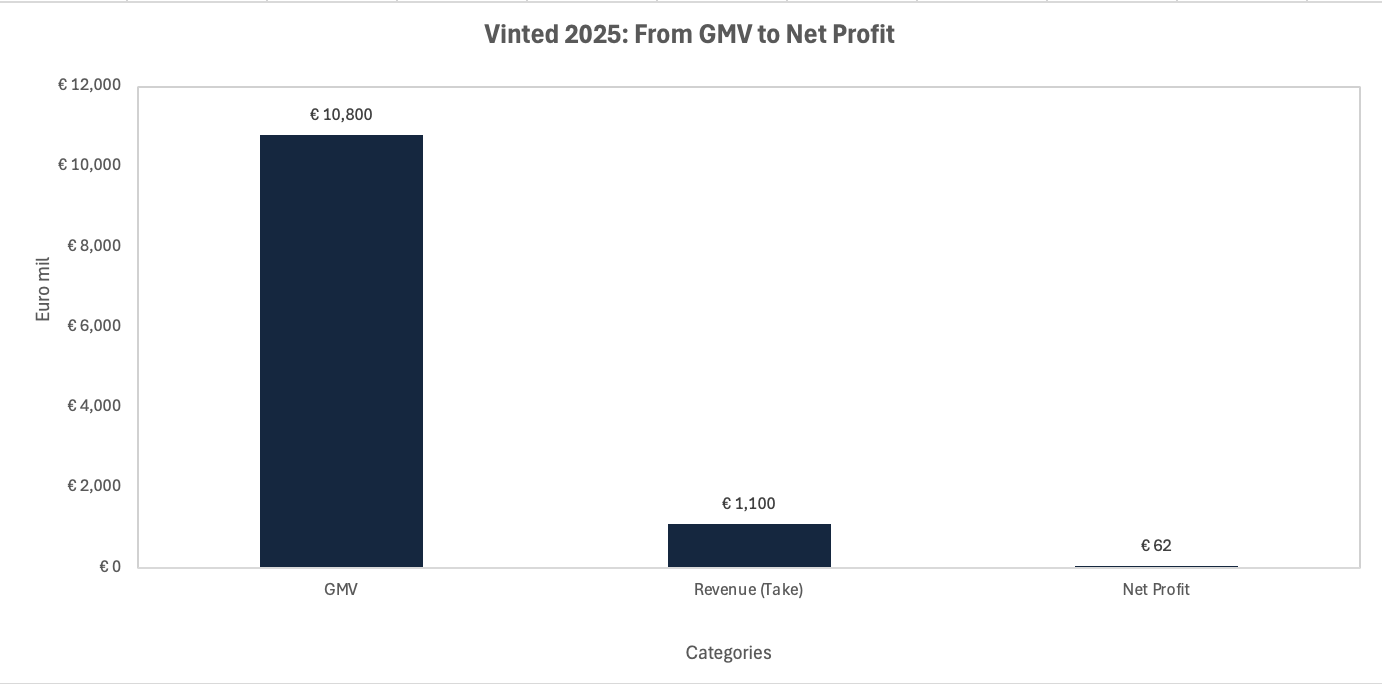

Here is what the headline numbers conceal. Vinted — the most financially successful large-scale resale platform in the world — grew its GMV by 47% year-on-year to €10.8bn in 2025. Its revenue reached €1.1bn. Its net profit came in at €62m. That is a net margin of 5.7% on revenue, and 0.6% on GMV. The number most cited in pitch decks — the €10.8bn — and the number that matters to a capital allocator are separated by a factor of 174.[4][5]

The mechanism is structural, not cyclical. Resale platforms earn a take rate — typically a commission or buyer protection fee — on transactions between third parties. Vinted's effective take rate on its €10.8bn GMV is roughly 10%, producing €1.1bn in revenue. From that revenue, it must fund authentication, customer service, logistics coordination, fraud prevention, payment processing, and geographic expansion. Profitability declined in 2025 even as GMV surged, precisely because scale requires reinvestment at a pace that outruns margin.

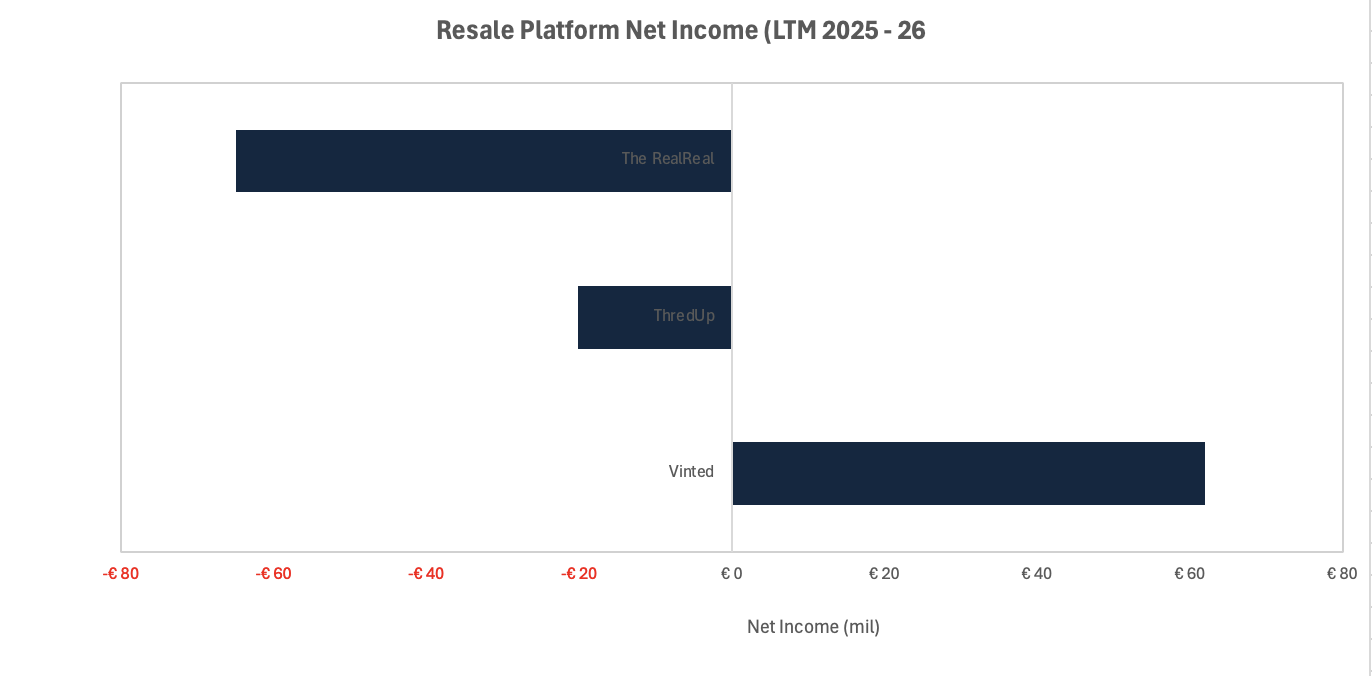

The listed platforms make this even clearer. ThredUp reported a net loss of $6.5m in Q1 2026, continuing a multi-year loss trajectory despite cumulative GMV growth that would, on paper, suggest a thriving business. The RealReal's stock fell nearly 17% immediately after its Q1 2026 earnings release, with revenue on a declining trend. Both companies are operating in a market growing at double digits annually and still cannot deliver a consistent bottom line. The reason is not management failure. It is that the cost of sourcing, sorting, authenticating, and fulfilling individual secondhand items at scale does not compress the way software unit economics do.

99.4% attrition from gross merchandise value to net profit. The headline number most cited in pitch decks bears almost no relationship to returns. Source: Vinted Financial Results 2025.

A market growing at 12% annually. Three of its most prominent platforms remain structurally loss-making or marginally profitable. Sources: Company filings, Simply Wall St, LinkedIn.

Investor Implications

For family offices and high-net-worth (HNW) investors, the framing matters enormously. If you are looking at public equities in this space, you are buying into businesses that have spent years and substantial capital proving that top-line growth in resale does not automatically translate to earnings power. ThredUp's stock rose over 460% in 2025 on resale sentiment, then fell sharply as the underlying financials reasserted themselves. That is not a sector re-rating. That is a narrative trade.

The more durable value is assembling in three adjacent areas that the narrative tends to overlook.

Authentication infrastructure: As luxury resale volumes grow, the cost of verification and fraud prevention scales with them. Companies and technologies that sit between the buyer's trust requirement and the platform's fulfilment obligation are extracting margin without carrying inventory risk. This includes third-party grading services and AI-assisted authentication tools now being embedded across platforms.

Logistics and reverse supply chain: Secondhand commerce is, structurally, a logistics problem. Each item is unique, requires individual assessment, and moves through a non-standardised supply chain. The operators solving this at scale — whether through owned infrastructure or third-party networks — hold a structural advantage that is harder to replicate than a marketplace brand.

Incumbent luxury and retail brands: Brands that own the original supply have an underappreciated position. Their pre-owned items circulate through resale channels at a price that either reinforces or dilutes the primary market valuation. Those that integrate resale as a brand-controlled channel — rather than ceding it to third-party platforms — retain margin, data, and customer relationships. The investment case here is not a resale play. It is a brand durability play that happens to benefit from the resale tailwind.

Private exposure, accessed through direct stakes in authentication or logistics businesses, is likely to offer a more compelling risk-adjusted entry than public platform equities at current valuations. ThredUp carries a 2.1x price-to-sales (P/S) multiple while still loss-making. That is not a margin-of-safety entry point for a capital-preserving allocator.

Near-Term Catalysts and Policy Outlook

The near-term asymmetry of risk is skewed toward the downside for platform equities and toward the upside for infrastructure and brand plays.

In the 0–3 month window, US tariff policy is the immediate variable. Tariffs on imported new goods have accelerated consumer migration toward secondhand, providing a demand tailwind that has been widely cited by resale platforms. The risk is that this tailwind is tariff-driven and therefore reversible; any policy reversal or tariff negotiation that lowers new-goods prices will compress the value gap that is currently driving secondhand demand. The demand case becomes less structural and more contingent on a policy environment that is, by definition, unstable.

In the 3–12 month window, EU digital product passport regulation begins to sharpen the competitive field. Brands and platforms that can provide verifiable provenance data will be better positioned as DPP requirements are phased in across apparel and textiles. This is a genuine structural catalyst for well-capitalised incumbents; it is a compliance cost for smaller platforms operating on thin margins. Regulatory tailwinds do not distribute evenly.

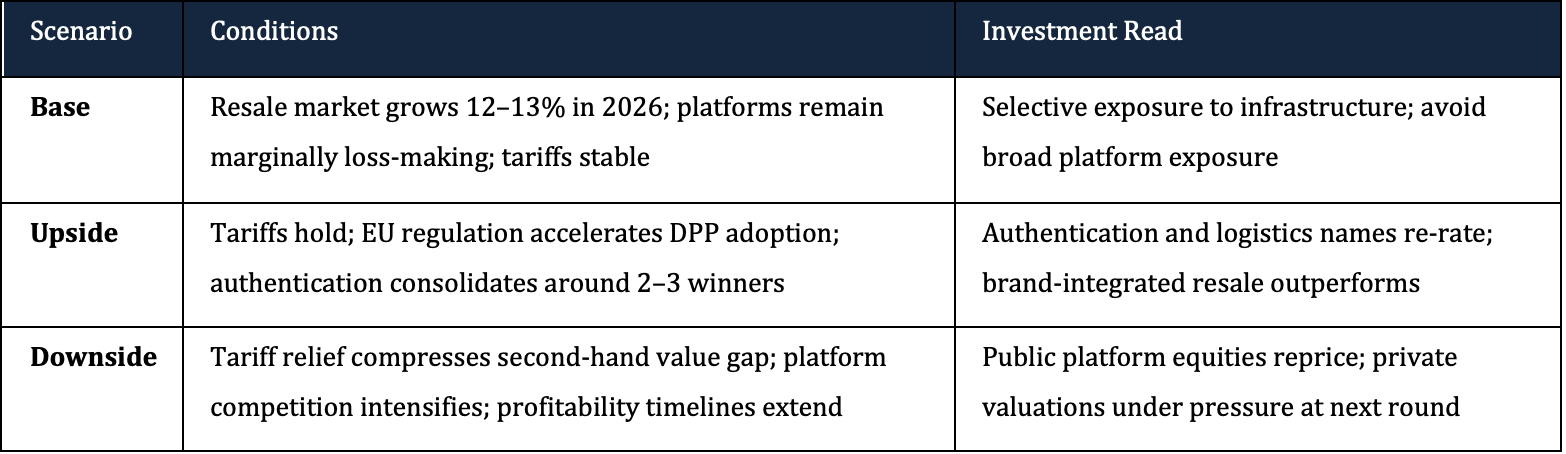

The scenario range for platform investors over this horizon is as follows:

Conclusion

The structural case for second-hand as a consumer and policy phenomenon is sound. The financial case for most platforms currently absorbing capital on the back of that phenomenon is not. Vinted, the sector's most operationally capable player, converted 0.6% of its GMV into net profit in 2025 — and profitability declined even as volumes surged. The listed alternatives are worse.

For family offices and HNW investors, the discipline required is to separate the trend from the vehicle. Riding the resale wave through brand-integrated plays, authentication infrastructure, or selective private stakes in logistics is a coherent strategy. Buying loss-making platforms at elevated multiples because the headline GMV number is impressive is not. The market is growing. The margins confirm exactly why that growth has not yet translated into a clean investment case. Capital that does not make this distinction will find itself owning the narrative rather than the returns.

References

Vinted – Financial Results 2025 – April 2026

ThredUp – Resale as a Service and Q1 2026 Earnings – May 2026

ThredUp – Resale Report 2026

The Business Research Company – Second-Hand Product Market Report 2026 – January 2026

The RealReal – Q1 2026 Earnings – May 2026

Retail Gazette – "Vinted confirms 38% growth YoY as reselling market booms" – April 2026

FashionUnited – "What second-hand fashion offers luxury brands, and vice versa" – April 2025

Modern Retail – "Resale is winning in the tariff economy" – August 2025

Simply Wall St – "ThredUp losses narrow to US$20.2m LTM" – May 2026

LinkedIn / Luca Cipiccia – "ThredUp vs The RealReal: 2026 Outlook" – January 2026

This article is for information and discussion only and does not constitute investment advice or a recommendation.