The Missing Middle: Southeast Asia's PE Rebound Is Bypassing the Market That Matters Most

The recovery in Southeast Asian private equity is real. The story being told about it is not.

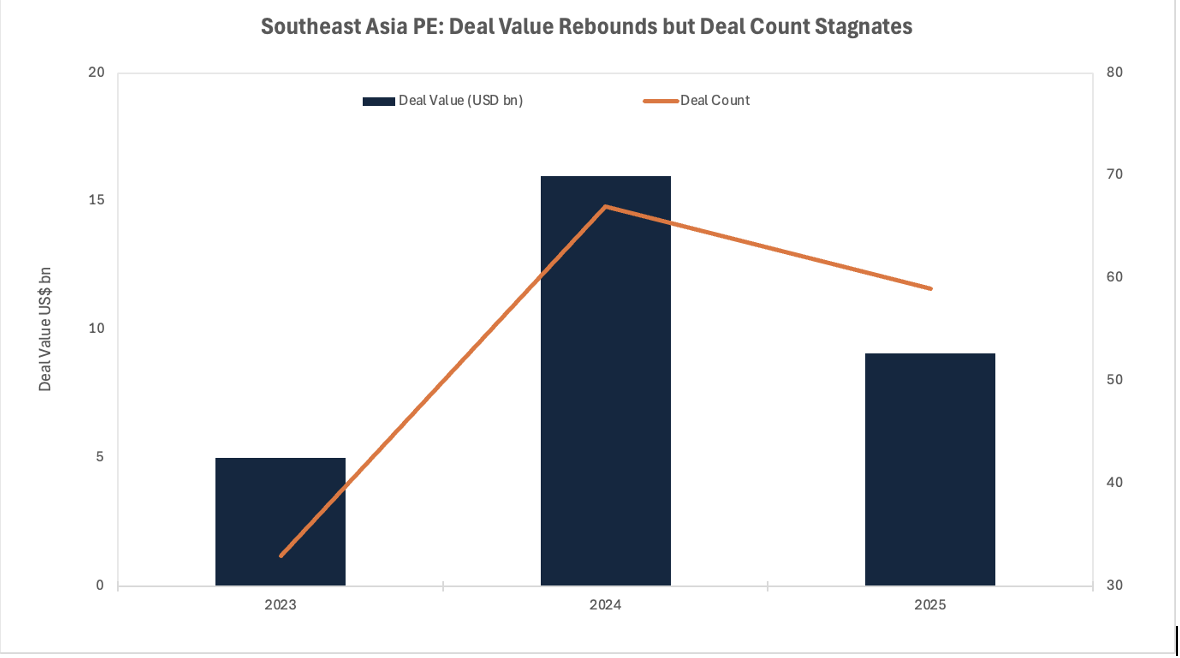

Private equity (PE) deal value in Southeast Asia surged 221% year-on-year in 2024 to reach $16 billion across 67 transactions, before moderating to $9.1 billion in 2025. Allocators interpreting this as a clean recovery are reading the wrong signal.

The rebound is concentrated in large-cap and digital infrastructure transactions, while the sub-$150 million mid-market, where the region's most asymmetric return potential sits, remains starved of credentialed advisory intermediation.

The constraint is not capital. It is the pipeline.

Why This Matters

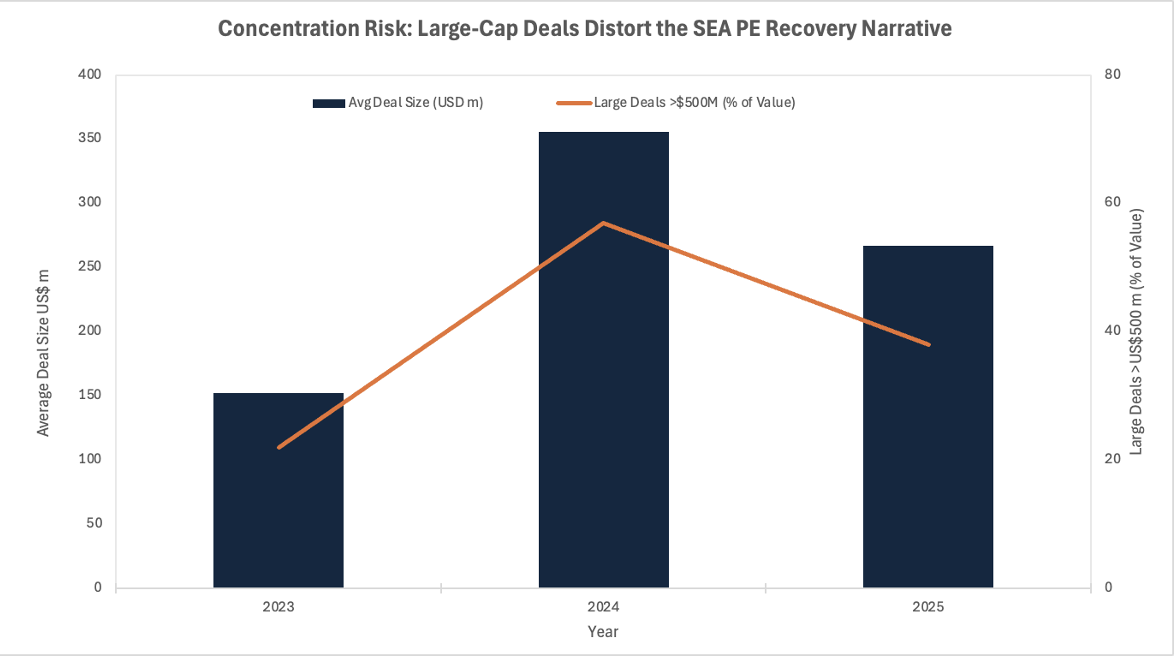

Recovery skewed to the top: large deals above $500 million represented 57% of 2024 deal value, the highest share on record, masking near-total stagnation in mid-market deal flow

Capital is present; infrastructure is not: Apollo Global Management secured a $1 billion mandate targeting Southeast Asian mid-market companies in 2025, and Temasek's 65 Equity vehicle was established specifically for entrepreneur-led mid-market businesses, yet neither can deploy efficiently without credentialed deal origination capacity

The succession clock is running: an estimated $5.8 trillion in Asia-Pacific family business wealth is set to transfer by the end of this decade, and 85% of companies across the region are family-owned, creating the largest pipeline of potential mid-market transactions in history

The Volume Recovery in Context

Southeast Asia's private capital market recorded deal value of $25 billion in 2024 on a broad definition including venture capital, the fourth-highest level in a decade, according to Praxis Global Alliance. On a private equity-only basis, EY data shows $16 billion deployed across 67 transactions, a 221% rise from 2023. Both figures have been cited extensively by allocators as evidence of structural re-rating.

The composition tells a different story. Large-ticket investments, defined as transactions above $500 million, represented 57% of 2024 deal value, their highest share since tracking began. The rebound was led by Singapore and Indonesia, concentrated in digital infrastructure assets where sovereign wealth funds and global general partners (GPs) can deploy capital at scale with identifiable exit routes. Deal count, the more telling indicator of market breadth, declined 9% across Asia-Pacific in 2024 despite the value surge.

In 2025, the picture sharpened further. EY data from February 2026 shows deal value fell 43% year-on-year to $9.1 billion across 59 transactions, with the average deal size compressing from $356 million to $267 million. The absence of megadeals exposed the thinness of the mid-market pipeline. Practitioners at DealStreetAsia's Indonesia Private Equity and Venture Capital (PE-VC) Summit 2026 confirmed that activity remained robust but exits lagged sharply, suggesting portfolio companies cannot find the liquidity pathways that a deeper intermediary ecosystem would create.

Chart 1: Southeast Asia PE Deal Value (USD bn) and Deal Count, 2023–2025

Deal value surged in 2024 but fell sharply in 2025 once megadeals dried up; deal count barely moved across either direction, confirming that the rebound was driven by deal size, not market breadth.

Sources: EY Southeast Asia Private Equity Pulse (2024 in Review; 2025 Full Year), February 2026.

The Structural Intermediation Gap

The mid-market, broadly defined in Southeast Asia as transactions between $20 million and $150 million, is where the region's economic complexity concentrates. Family-owned businesses account for an estimated 85% of enterprises across Asia-Pacific, and in Indonesia, Thailand, the Philippines and Malaysia, the largest listed companies are overwhelmingly family-controlled. Below the listed tier sits an enormous stratum of privately held, operationally complex businesses whose owners have no reliable mechanism to access institutional capital or achieve a structured exit.

The constraint is not capital availability. Apollo Global Management secured a $1 billion mandate in 2025 for a private credit strategy targeting mid-market companies in Southeast Asia. Temasek's 65 Equity vehicle was established explicitly to invest in entrepreneur-led mid-market businesses across the region. Capital is present and willing. What is absent is the advisory infrastructure to surface, prepare and intermediate these opportunities to institutional buyers.

The deal advisory talent market illuminates the problem precisely. Over the past 12 to 18 months, experienced professionals have been leaving Big 4 advisory firms, including PwC, EY, Deloitte and KPMG, for private equity portfolio companies, family offices and regional boutique firms. The result is a permanent structural mismatch: GPs and independent sponsors need deal-ready managers and directors, yet the market supplies primarily analysts and junior hires. Senior talent, specifically financial due diligence leaders, sector-experienced M&A advisors and integration specialists, is the real bottleneck, not deal appetite.

This creates a compounding dynamic. Underprepared sellers meet undercapitalised intermediaries, produce poorly structured deal materials and arrive at institutional buyers with information asymmetry embedded in the process. GPs lose time on underbaked processes, sellers leave value on the table, and the deal does not close; both sides conclude the market is not ready.

Investor Implications

For allocators with commitments to Southeast Asian private equity funds, the intermediation gap manifests in three direct ways: elevated deal origination costs, compressed deal pipelines and structurally longer hold periods. GPs unable to source efficiently through reliable intermediary networks substitute depth with concentration, which explains why large-cap and platform transactions dominate disclosed deal flow even as the mid-market remains opaque.

The pricing implication is more consequential. In markets where intermediary coverage is thin, sellers lack credible valuation reference points. Credentialed buyers with sector knowledge, regional trust networks and transaction experience consistently secure entry multiples at material discounts to comparable transactions in more intermediated markets. The information rent flows entirely to the buyer, representing a structural form of alpha that does not depend on market timing.

The strategic question for allocators is whether to back GPs building proprietary origination networks, or to look directly at the advisory layer itself as an investable asset. Temasek's 65 Equity model and Creador's track record in Malaysia and Indonesia both point toward the same conclusion: proprietary deal flow generated through advisory infrastructure is the region's most defensible return driver.

Chart 2: Concentration Risk: Average Deal Size vs Large-Cap Share of Value, 2023–2025

The spike in average deal size and large-cap concentration in 2024 confirms that the headline rebound was driven by a small number of outsized transactions, not by a broadening of the mid-market. The 2025 compression to $267 million average, once megadeals disappeared, exposed how thin the underlying pipeline remains.

Sources: EY Southeast Asia Private Equity Pulse; Praxis Global Alliance Southeast Asia Investment Pulse 2025. Note: 2023 and 2025 large-cap share figures are estimates derived from deal value and count data; 2024 figure of 57% is confirmed.

Catalysts and Policy Outlook

The succession dynamic is the most structurally significant near-term catalyst. Business Times Singapore estimates $5.8 trillion in Asia-Pacific wealth will transfer by the end of this decade. Across ASEAN, the succession wave in family conglomerates, historically deferred by patriarchal governance structures and the absence of formalised transition processes, is now arriving. The founder generation that built regional enterprises between the 1980s and 2000s is now in its sixties and seventies, frequently without a credible internal successor, and PE activity in Southeast Asian family businesses has already accelerated in healthcare, consumer and financial services.

Policy signals from ASEAN capital markets development initiatives create secondary tailwinds. Indonesia's Otoritas Jasa Keuangan (OJK) has signalled continued IPO and secondary market access reforms. Malaysia's Bursa Malaysia has invested in its Access, Certainty, Efficiency (ACE) Market to create a listing pathway for growth-stage companies. These mechanisms expand the addressable universe for mid-market intermediation by providing credible exit optionality that intermediaries can present to sellers as part of a transaction rationale.

The base case for 2026 to 2028 is continued PE concentration in large-cap digital infrastructure and healthcare, with the mid-market remaining opaque and under-intermediated. The upside scenario involves boutique advisory capacity building, succession pressure and increasing GP competition for proprietary deal flow compressing the information premium and expanding the addressable universe for institutional capital. The downside scenario, in which tariff escalation and US dollar strengthening suppress Southeast Asian growth expectations, would slow succession-driven transactions and push allocators back toward large-cap defensive positions.

Conclusion

The consensus reading of Southeast Asia's private equity rebound, that the region has re-rated and deal activity is normalising at scale, is accurate at the aggregate level and misleading where it matters. The mid-market intermediation gap is not a temporary friction awaiting correction by market forces. It is a structural feature of a region where trust networks substitute for formal advisory infrastructure, where information asymmetry functions as a competitive moat rather than a market failure, and where the successor generation of business owners has yet to fully arrive at the transaction table.

The non-consensus assertion is this: the most durable alpha available in Southeast Asian private markets over the next decade will accrue not to funds deploying the largest cheques into digital infrastructure platforms, but to those who build or acquire credentialed advisory intermediary capacity at the sub-$150 million level. The intermediation layer is the scarcest resource in the regional ecosystem, and scarcity, when it sits directly in the deal origination stack, is not a market imperfection. It is a return source. Allocators who understand this will look beyond GP fund commitments and ask a more precise question: who controls the pipeline infrastructure, and how do I get economic exposure to it?

References

EY – Southeast Asia Private Equity Pulse: 2024 in Review – 2025

EY – Southeast Asia Private Equity Deal Value Declined in 2025 but Market Regains Momentum – February 2026

Praxis Global Alliance – Southeast Asia Investment Pulse 2025 – September 2025

Bain & Company – Asia-Pacific Private Equity Report 2025 – March 2025

DealStreetAsia – Southeast Asia PE Deals Remain Strong as Exits Fall Behind – February 2026

Business Times Singapore – The US$5.8 Trillion Question: Who Will Inherit Asia's Family Businesses? – January 2026

Moonfare – A Quiet Power Shift Is Underway in Asia-Pacific Private Equity – November 2025

LinkedIn / Deal Advisory Talent Market Analysis – Talent Movement in Deal Advisory Across Southeast Asia – February 2026

ASEAN Business Advisory Council / McKinsey & Company – ASEAN's Private Markets: Coming Together for Growth – September 2025

Fortune / Quadria Capital – Private Equity Is Eyeing Asia's Healthcare Funding Gap – March 2026

Disclaimer: This article is for information and discussion only and does not constitute investment advice or a recommendation.