The ECB's 2026 Collateral Haircut Will Price What Sell-Side Still Won't

The EU's climate rules are no longer about sustainability ratings: they are about who gets capital, at what cost, and on whose terms.

Europe's climate regulatory architecture has spent four years building infrastructure for disclosure. That phase is ending. The convergence of the EU Taxonomy, the Corporate Sustainability Reporting Directive (CSRD), the European Sustainability Reporting Standards (ESRS), and the forthcoming European Integrated Framework for Climate Resilience signals a structural transition: taxonomy alignment is becoming a prerequisite for competitive capital access, not a merit badge.

The European Central Bank (ECB) is now embedding climate criteria into its collateral framework. The European Green Bond Standard (EUGBS) is gaining market share over incumbent green bond frameworks. And in the fourth quarter of 2026, the Commission will adopt a legislative package that formalises conditionality at the macroeconomic level. The transmission mechanism is already live.

By 2027, it will be systemic.

Why This Matters

Capital repricing: The ECB is introducing a climate factor into its collateral framework for corporate bonds in H2 2026, directly linking taxonomy alignment to the cost of central bank liquidity for non-financial corporations.

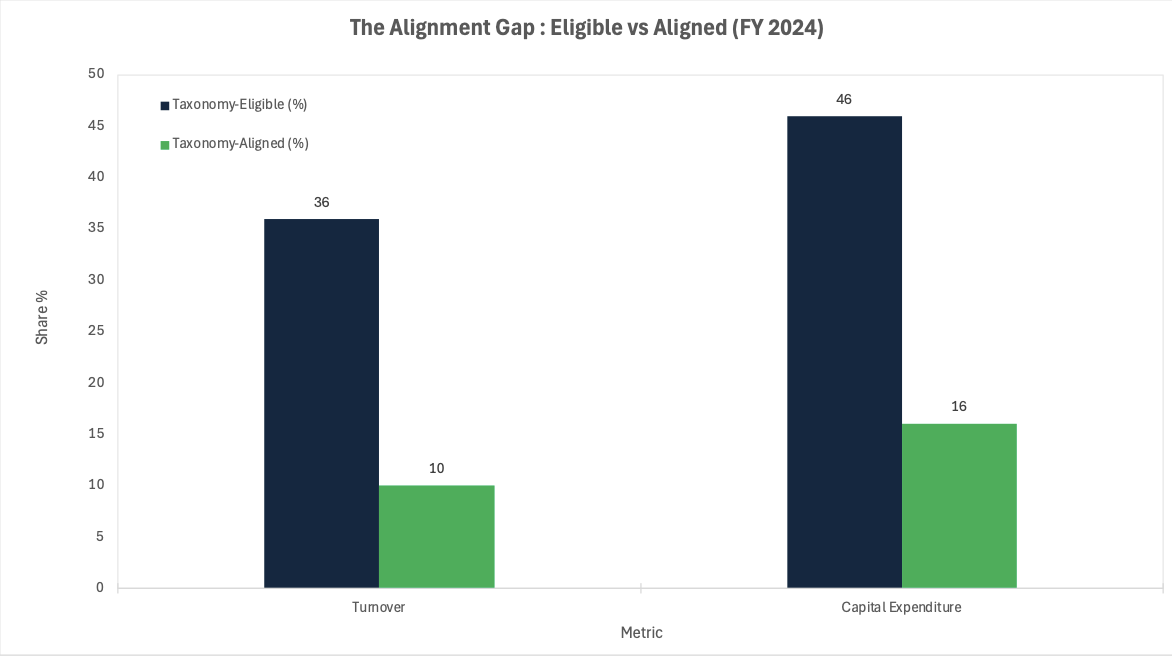

The alignment gap: Only 10% of corporate revenues and 16% of capital expenditure are truly taxonomy-aligned, against eligibility rates of 36% and 46% respectively, a divergence that represents mis-priced transition risk hiding in plain sight.

The gatekeeper mechanism: The forthcoming Integrated Framework for Climate Resilience, expected Q4 2026, will combine legally binding rules with economic instruments, moving the EU from disclosure to conditionality at the systemic level.

The Architecture of Control

The EU's sustainable finance framework is not a single instrument. It is a layered stack of interconnected regulations that together constitute a classification and disclosure infrastructure of unprecedented scope.

The EU Taxonomy defines which economic activities qualify as "sustainable." The CSRD and ESRS mandate that large companies disclose not only how much of their activity is taxonomy-eligible but how much is genuinely taxonomy-aligned: meeting the technical screening criteria, doing no significant harm to other environmental objectives, and complying with minimum social safeguards. The Sustainable Finance Disclosure Regulation (SFDR) extends this logic to financial products, requiring asset managers and insurers to classify their funds according to the sustainability standards of their underlying assets.

The 2025 Omnibus Simplification Package narrowed CSRD scope significantly, raising thresholds to companies with more than 1,000 employees and €450 million in annual revenue, excluding approximately 80 to 90% of previously in-scope companies. This looked like a retreat. It was not. It concentrated disclosure obligations on exactly the corporate counterparties that institutional lenders and bond markets most actively price. The taxonomy's grip on capital markets has not weakened. It has sharpened.

Completing the stack, the European Integrated Framework for Climate Resilience, expected for adoption in Q4 2026, will introduce both non-legislative and legally binding measures governing how Member States and private actors finance climate risk management. Europe lost an estimated €208 billion to extreme weather between 2021 and 2024. The political calculus for binding conditionality has shifted accordingly.

Chart 1 — The Alignment Gap: EU Taxonomy Eligibility vs True Alignment (FY 2024)

Source: EY EU Taxonomy Barometer 2025, 332 non-financial companies across 20 EU countries.

The gap between eligibility and alignment is not a reporting lag. It is the space in which repricing will occur as disclosure quality matures and covenant infrastructure catches up.

The Non-Obvious Mechanism

The conventional narrative frames taxonomy alignment as a reporting burden. That framing is already obsolete. Alignment is becoming a pricing input, and the mechanism operates through three simultaneous channels.

The first is the ECB's collateral framework. Its announcement in September 2025, confirmed for implementation in H2 2026, applies a climate-transition haircut to corporate bonds used as Eurosystem collateral. Assets issued by non-financial corporations carrying elevated transition risk will face reduced collateral value, directly raising the effective funding cost for issuers unable to demonstrate credible alignment. This is not a soft signal. It is a hard monetary policy mechanism and sell-side research has been structurally unable to say so plainly given its exposure to the very corporate issuers affected.

The second channel is the EUGBS. With over €22 billion issued since late 2024, the Standard requires that use of proceeds be taxonomy-aligned. As it gains market share over incumbent green bond frameworks, the pricing benefit of green labelling will concentrate among EUGBS-eligible issuers. Early issuance is dominated by energy producers and utilities: the only sector consistently converting high eligibility into meaningful alignment, given its direct overlap with climate mitigation criteria.

The third channel is sustainability-linked lending covenants. Infrastructure and real asset financing already reference taxonomy metrics in covenant structures. As CSRD disclosures accumulate audit-quality data through 2027 and 2028, the contractual infrastructure for systematic covenant embedding across corporate lending will be in place. The alignment gap quantified in Chart 1 is the basis from which covenant breaches and lending restrictions will be triggered.

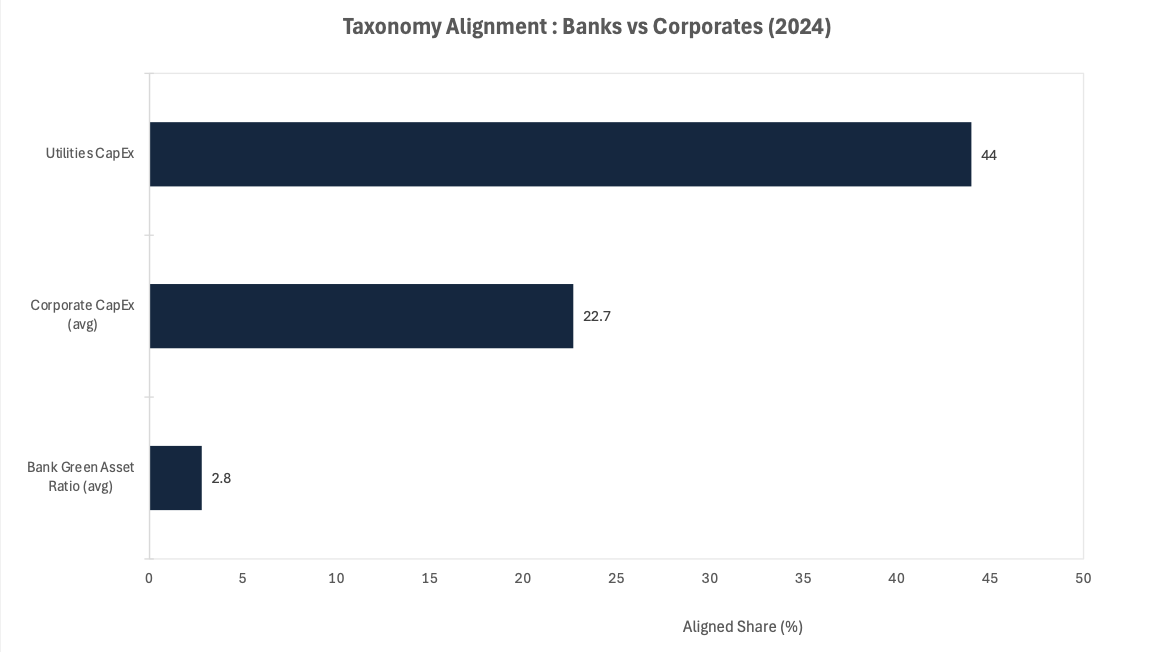

Chart 2 — Taxonomy Alignment Divergence: Banks vs Corporates (2024)

Source: European Commission EU Taxonomy Uptake Report, November 2025. Bank figure represents €816bn of €28 trillion in total covered assets.

The divergence between bank GAR and corporate CapEx alignment means banks are pricing green credentials they have not validated. The correction will be directionally one-way.

Implications for Allocators and Corporates

For capital allocators, the primary question is not which companies have strong environmental, social and governance (ESG) scores. It is which balance sheets will absorb repricing risk as alignment conditionality tightens.

Utilities and renewable energy infrastructure are the structural winners. Their activities align closely with taxonomy climate mitigation criteria, and at 44% CapEx alignment they are already demonstrating the conversion that other sectors struggle to achieve. For infrastructure fund managers, taxonomy-aligned assets will command a growing liquidity premium as the EUGBS and ECB collateral reform reinforce each other. For bond investors, this creates a bifurcated secondary market as taxonomy eligibility becomes a proxy for refinancing risk.

The risk is concentrated in mid-transition industrials, chemicals, materials, and logistics, where eligibility claims are high but alignment conversion is low. Companies in technology and healthcare face a different trap: their activities often fall outside taxonomy coverage entirely, leaving them unable to claim alignment regardless of actual environmental performance.

For CFOs, the reframing required is specific. Taxonomy alignment is a treasury function, not a sustainability function. Covenant risk, collateral haircut exposure, and EUGBS access conditions are balance sheet variables that belong on the CFO's desk, not in the sustainability team's annual report. Private credit managers, unconstrained by GAR reporting obligations or ECB collateral requirements, have a structural opportunity to price alignment risk directly and capture the spread premium as banks reprice away from mis-aligned mid-market borrowers.

Near-Term Catalysts and Policy Outlook

The 2026 to 2028 window contains a dense sequence of catalysts, each tightening conditionality incrementally.

ECB collateral climate factor (H2 2026): Applies to corporate bonds; direct impact on funding cost for non-aligned issuers accessing central bank liquidity.

EU Integrated Framework for Climate Resilience (Q4 2026): Legally binding rules alongside economic instruments; the Reflection Group report that directly informed the framework explicitly calls for embedding resilience metrics into finance flows.

ETS2 carbon pricing (2027): Extends the EU Emissions Trading System to buildings and road transport, covering 75% of EU emissions and adding a direct cost floor to transition-misaligned assets in these sectors.

CSRD Wave 2 full reporting (2027–2028): As the next cohort of companies enters scope, alignment data coverage across EU capital markets deepens substantially, reducing informational asymmetry and accelerating covenant adoption.

Three scenarios:

Base case, repricing is gradual and sector-differentiated, with utilities and renewable infrastructure tightening spreads relative to transition-lagging industrials through 2027.

Upside case, rapid EUGBS adoption and ECB enforcement create a pronounced green premium in the primary bond market within 18 months.

Downside case, protracted delegated act negotiations and political pressure delay conditionality, creating an arbitrage window for mis-aligned issuers through 2028.

Conclusion

The consensus view holds that the Omnibus simplification package represents a dilution of the EU's sustainable finance ambition. This reading mistakes scope narrowing for strategic retreat.

By concentrating disclosure obligations on the most capital-market-relevant counterparties, simplifying taxonomy technical screening criteria to improve usability, and simultaneously hardening ECB collateral rules and EUGBS market infrastructure, the EU has recalibrated rather than reversed. The framework is smaller in administrative reach but more potent in capital market effect.

Taxonomy alignment is becoming a simultaneous proxy for refinancing risk, collateral quality, and green bond access. The cost-of-capital differential between aligned and mis-aligned issuers will not converge until alignment rates rise substantially from their current 10 to 16% levels. That process will take a decade. Allocators who reprice now are not being early: they are avoiding being late.

The geopolitical overlay reinforces the direction of travel. As the United States withdraws from climate financial regulation, EU-aligned institutional capital faces reduced competitive pressure to delay enforcement. The Framework's gatekeeper function will first be tested in European capital markets. The knock-on effects for global issuers seeking EU investor access will follow within the same cycle.

References

European Commission – EU Taxonomy Uptake Report – November 2025

EY – EU Taxonomy Barometer 2025 – 2025

ECB – Climate and Nature Work Update, ecb.europa.eu – January 2026

Banque de France / ECB – ECB Collateral Climate Factor Announcement – September 2025

European Parliament Legislative Train – European Integrated Framework for Climate Resilience – 2026

IEEFA / Solar Quarter – Europe's Green Bond Standard Passes €22bn Mark – February 2026

GRC Report – EU Reflection Group on Climate Resilience Financing – December 2025

AIGovHub – EU CSRD Omnibus Simplification Package – February 2026

European Commission Climate Action Portal – Integrated Framework for Climate Resilience – 2026

ISS Corporate – EU Green Bond Standard Sees Strong 2025 Momentum – November 2025

Disclaimer: This article is for information and discussion only and does not constitute investment advice or a recommendation.