The Settlement Layer: Why Carbon Traceability Is Now a Liability Question, Not an ESG One

The carbon credit that once signalled environmental virtue is now a legal instrument: the infrastructure beneath it determines who bears the loss when it fails.

For family offices and chief investment officers (CIOs) managing multi-generational capital, the voluntary carbon market (VCM) has largely been treated as a peripheral environmental, social and governance (ESG) consideration. That framing is now dangerous.

A convergence of litigation, regulation and market infrastructure development is transforming carbon credits from aspirational commitments into enforceable claims with traceable provenance and defined liability. The question is no longer whether to engage with carbon markets; it is whether the instruments held can withstand legal scrutiny.

Why This Matters

Liability migration: Carbon credits lacking verifiable, on-chain provenance are the subject of active litigation across multiple jurisdictions. The liability does not stay with the issuer; it travels to the last informed holder.

Regulatory bifurcation: The European Union (EU) Green Claims Directive and Article 6 of the Paris Agreement are creating a two-tier market: traceable credits that pass regulatory due diligence, and opaque ones that become contingent liabilities.

Portfolio blind spots: Family offices holding carbon-linked structured products, green bonds, or sustainability-linked loans (SLLs) may be exposed to reputational and financial risk through instruments referencing unverifiable offsets, often several layers removed from the underlying credit.

The Shift Underway

The voluntary carbon market spent the better part of a decade operating on trust. Credits were issued by private registries, verified by third-party auditors under methodologies that varied widely, and purchased by corporations seeking to offset scope 1, 2 or 3 emissions. The system worked as long as no one looked closely.

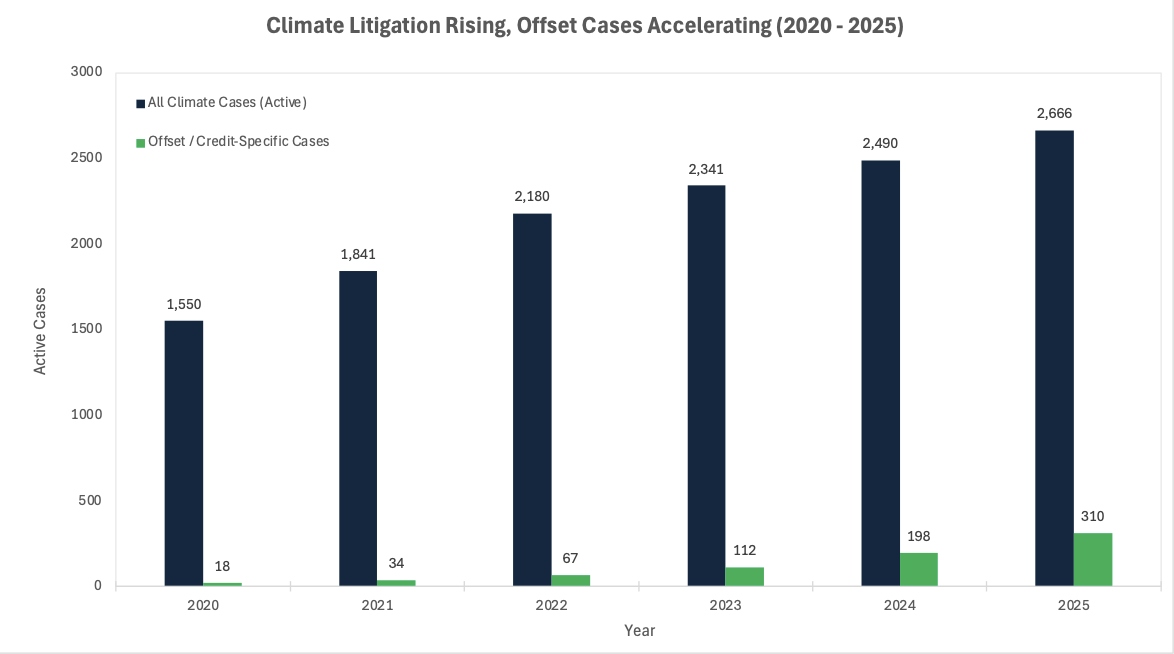

Scrutiny arrived in force from 2023 onwards. Investigative reporting, academic research and a wave of litigation in the United States, Australia and the United Kingdom exposed systematic over-crediting in forestry projects, phantom removals and double-counting across registries. The London School of Economics (LSE) Grantham Research Institute documented a measurable rise in legal challenges to corporate carbon-offsetting claims, with courts increasingly treating offset-backed "net zero" statements as actionable misrepresentations rather than aspirational marketing.

The market has responded, unevenly. The Integrity Council for the Voluntary Carbon Market (ICVCM) published its Core Carbon Principles (CCPs) to establish a quality floor. New blockchain-based registry platforms, including one developed through Cornell University and launched in early 2026, are beginning to provide immutable audit trails for credit issuance, transfer and retirement. The shift from a trust-based system to a verification-based one is structural and irreversible.

Source: Sabin Center for Climate Change Law; LSE Grantham Research Institute

The Non-Obvious Mechanism

The conventional framing treats traceability as a transparency upgrade: better data, cleaner markets, more informed buyers. That framing undersells the structural change underway. Traceability is functioning as a settlement layer, the foundational infrastructure that determines finality of a transaction and the allocation of residual risk.

In traditional financial markets, settlement infrastructure resolves ambiguity about ownership, timing and counterparty exposure. In carbon markets, that function has been absent. When a credit is invalidated, as occurred with several forestry projects under the first wave of Article 6 of the Paris Agreement following COP29 rules agreed in Baku in November 2024, there is no established mechanism for determining who holds the loss. The buyer, broker, registry and issuing project have all contested liability. Courts are beginning to fill the vacuum.

The non-consensus insight is this: traceability infrastructure does not merely reduce uncertainty; it allocates it. A credit with a full, immutable provenance chain assigns residual liability clearly to the last informed holder. A credit without one creates a liability that is diffuse, contested and therefore far more dangerous to institutional holders who cannot argue ignorance. Family offices, which frequently access carbon exposure through funds-of-funds, structured notes or impact vehicles, are often several layers removed from the underlying credit.

As traceability standards harden, the unverifiable portion of the carbon market will not quietly disappear. It will be repriced as a contingent liability, and capital currently allocated to it will need to move or be impaired.

Implications for Family Offices and CIOs

Direct exposure for most family offices is not through outright carbon credit purchases, but through three indirect channels: green bonds where proceeds reference offset purchases; SLLs with carbon-related key performance indicators (KPIs); and private equity or infrastructure fund positions in carbon project developers.

Each channel carries a version of the same risk. If the carbon instrument referenced in an underlying transaction cannot demonstrate traceable provenance under standards now being enforced by the EU Green Claims Directive and ICVCM CCP guidelines, the instrument's ESG classification becomes challengeable. That challenge affects regulatory treatment, refinancing conditions and, increasingly, exit valuations in private markets.

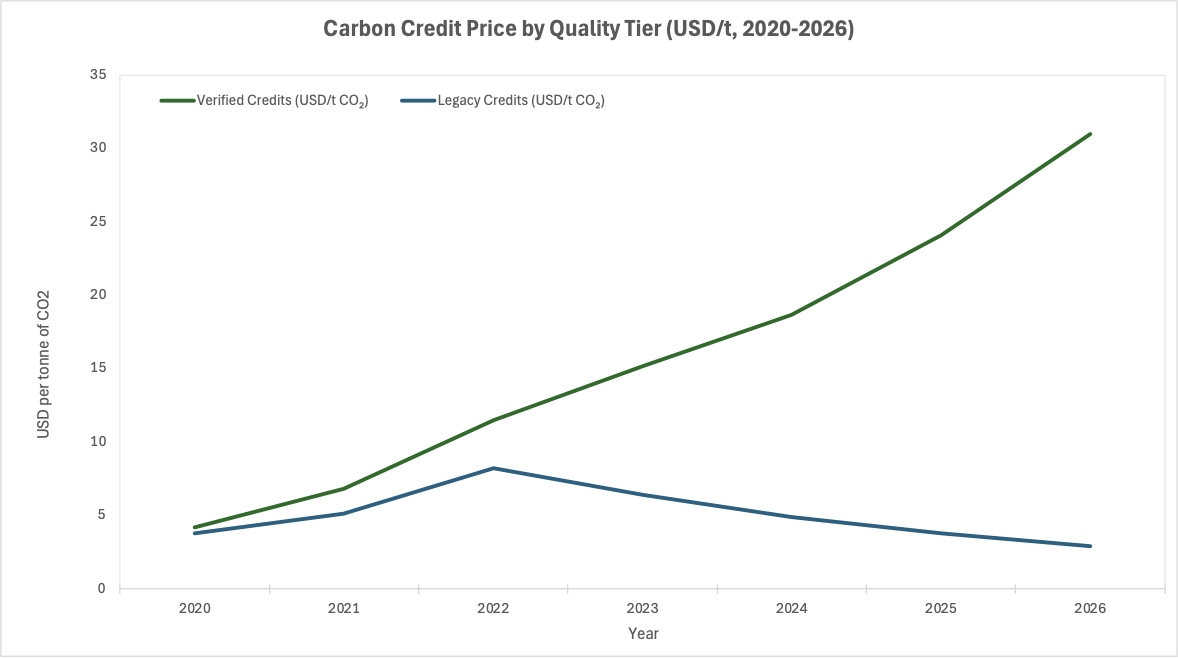

The cost-of-capital implication is significant and asymmetric. Verified, traceable credits are attracting a growing premium as corporates facing EU compliance deadlines seek instruments that will withstand legal scrutiny. Unverifiable credits are simultaneously losing liquidity as counterparties refuse to accept liability transfer. For CIOs constructing or reviewing climate-aligned allocations, this divergence is not a future risk: it is an active repricing already visible in secondary market spreads.

Source: Ecosystem Marketplace; BloombergNEF

Catalysts and Policy Outlook

Three near-term catalysts will determine the pace and severity of repricing.

The operationalisation of Article 6.4 of the Paris Agreement, agreed at COP29, establishes a UN (United Nations)-supervised crediting mechanism with mandatory provenance requirements. The first credits under this framework are expected to enter the market in late 2026. Their arrival will create a direct quality benchmark against which all voluntary credits will be compared, accelerating the bifurcation already underway.

The EU Green Claims Directive, moving through member state transposition with enforcement expected by 2027, will prohibit product-level carbon neutrality claims that rely on offset purchases rather than verified removals. For any family office holding equity in consumer-facing businesses with carbon neutrality marketing, the regulatory exposure is direct and measurable.

The litigation pipeline is the least predictable but potentially most consequential catalyst. Climate litigation recorded more than 2,500 active cases globally by the end of 2025, with a growing proportion targeting the technical specification of specific carbon instruments rather than general climate commitments. Legal advisers at Linklaters flagged in their ESG Legal Outlook 2026 that greenwashing cases are increasingly turning on the provenance and methodology of the underlying credit, not merely the marketing claim built upon it.

Various scenarios building on this:

Base case (2026–2027): Verified credits command a 20–30% premium over unverifiable equivalents; secondary liquidity for non-CCP-compliant credits deteriorates sharply.

Upside case: Article 6.4 adoption accelerates; a major greenwashing ruling in a G7 jurisdiction triggers rapid portfolio reallocation toward verified instruments.

Downside case: Regulatory implementation delays allow continued blurring of standards; litigation uncertainty depresses overall market confidence and delays institutional re-entry.

Conclusion

The structural conclusion is uncomfortable for anyone who has treated carbon credits as a soft allocation rather than a hard instrument. Traceability is not a feature that responsible issuers will eventually add; it is becoming the threshold condition for holding carbon exposure without a contingent liability on the balance sheet.

The non-consensus assertion worth defending is this: the carbon market is not maturing, it is bifurcating. The credible tier, with verified provenance, regulatory acceptance and improving liquidity, will attract institutional capital and tighten further. The legacy tier is becoming structurally un-investable for any institution that cannot afford greenwashing litigation. A cautious sell-side analyst would not say that directly, for obvious reasons. A rigorous independent allocator has no reason not to.

For family offices and CIOs, the geopolitical overlay reinforces the urgency. As the US retreats from multilateral climate commitments under President Trump's second administration, the EU is hardening its own standards to preserve market credibility and competitive advantage. That divergence will not slow the litigation wave; it will redirect it toward European-jurisdiction assets and any non-US entity with EU market exposure. The window to reposition is open, but it is narrowing. The settlement layer is being built; the question is whether portfolios are on the right side of it before the courts make that determination unilaterally.

References

Sabin Center for Climate Change Law / LSE Grantham Research Institute – Global Climate Litigation Report – 2025

The Guardian – Rise in legal challenges over carbon credit schemes – June 2025

Cornell University / blockchain carbon registry platform – New blockchain platform brings credibility to carbon registries – February 2026

Carbon Market Watch – First wave of Article 6 carbon credits misfire spectacularly – April 2025

Linklaters – ESG Legal Outlook 2026 – October 2025

Carbon Direct – Key trends in the 2026 voluntary carbon market – March 2026

European Commission / Carbon Market Watch – EU Green Claims Directive: member state transposition – 2025–2027

UNFCCC – Article 6 of the Paris Agreement: COP29 outcomes – November 2024

Ecosystem Marketplace / BloombergNEF – Voluntary Carbon Market pricing data – 2020–2026

Charles Russell Speechlys – Anti-greenwashing in the UK, EU and the US: the outlook for 2025 and beyond – June 2025

Disclaimer: This article is for information and discussion only and does not constitute investment advice or a recommendation.