Silent Compression: How AI Adoption Gaps Become Margin Events by 2027

The boards deferring AI transformation are not making a technology decision. They are quietly building a liability.

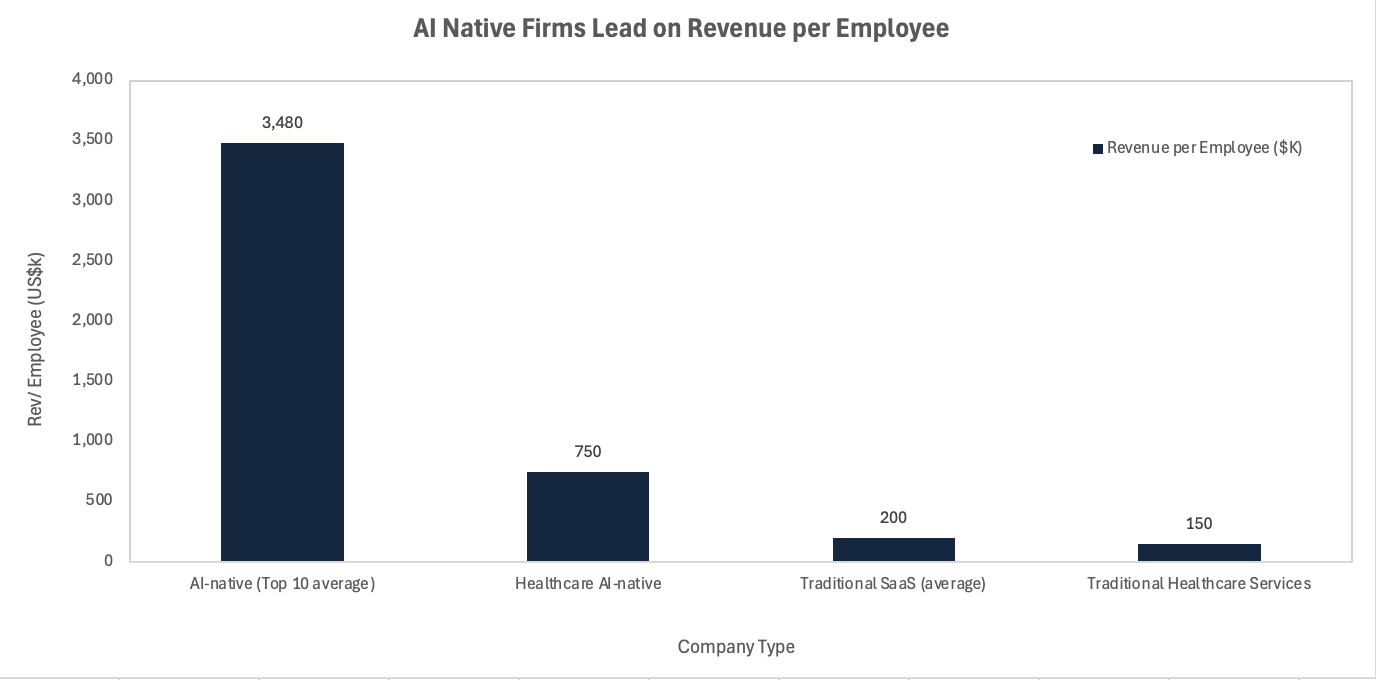

The pattern is already visible in the data. AI-native firms are operating at structurally different unit economics: the top ten AI companies average $3.48 million in revenue per employee, against a traditional SaaS average of $200,000 — a 17-fold gap that did not exist five years ago. In healthcare, AI-native companies are generating $500,000 to over $1 million in ARR per full-time employee, compared to $100,000 to $200,000 for traditional services firms. These are not productivity improvements at the margin. They are a different cost architecture entirely, and the gap is compounding.

Why This Matters

The productivity debt is silent until it is not: Companies deferring AI adoption are not standing still; they are falling behind at an accelerating rate as early movers deepen their structural cost advantages across every workflow.

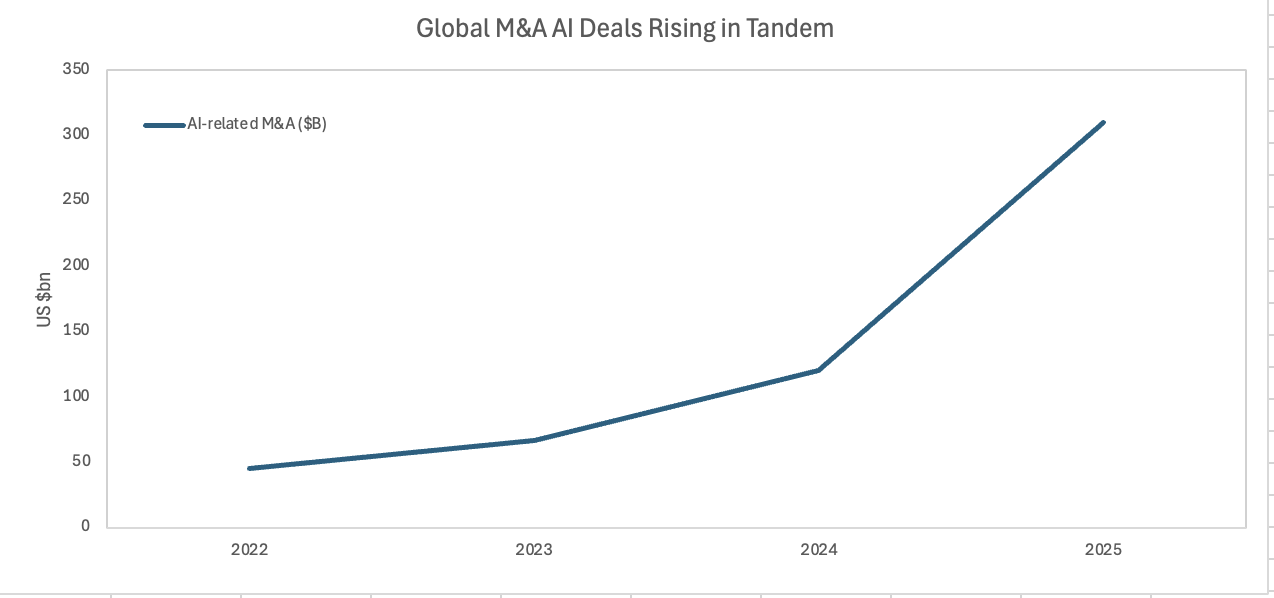

The M&A signal is already live: AI-related deal activity rose from $45 billion in 2022 to $310 billion in 2025 — a six-fold increase in three years — and the acquirers are those who moved early, buying the capability gaps they cannot close organically.

Boards are misclassifying the risk: Treating AI as an IT budget line, rather than a structural operating model decision, is the same error mill owners made with electrification in the 1890s. The outcome will be the same.

The Core Shift

The structural transformation now under way is not about chatbots or copilots. It is about the fundamental ratio of human labour to revenue output. Controlled field experiments and randomised trials document 15% to over 50% reductions in task-completion time across writing, customer support, software development, accounting, law, and translation. A Fortune 500 customer-support deployment showed a 15% average productivity increase measured in issues resolved per hour, with a 36% increase for workers in the bottom skill quintile. These gains do not materialise uniformly: they accrue disproportionately to firms that redesign workflows around AI capability, not those that bolt tools onto legacy processes.

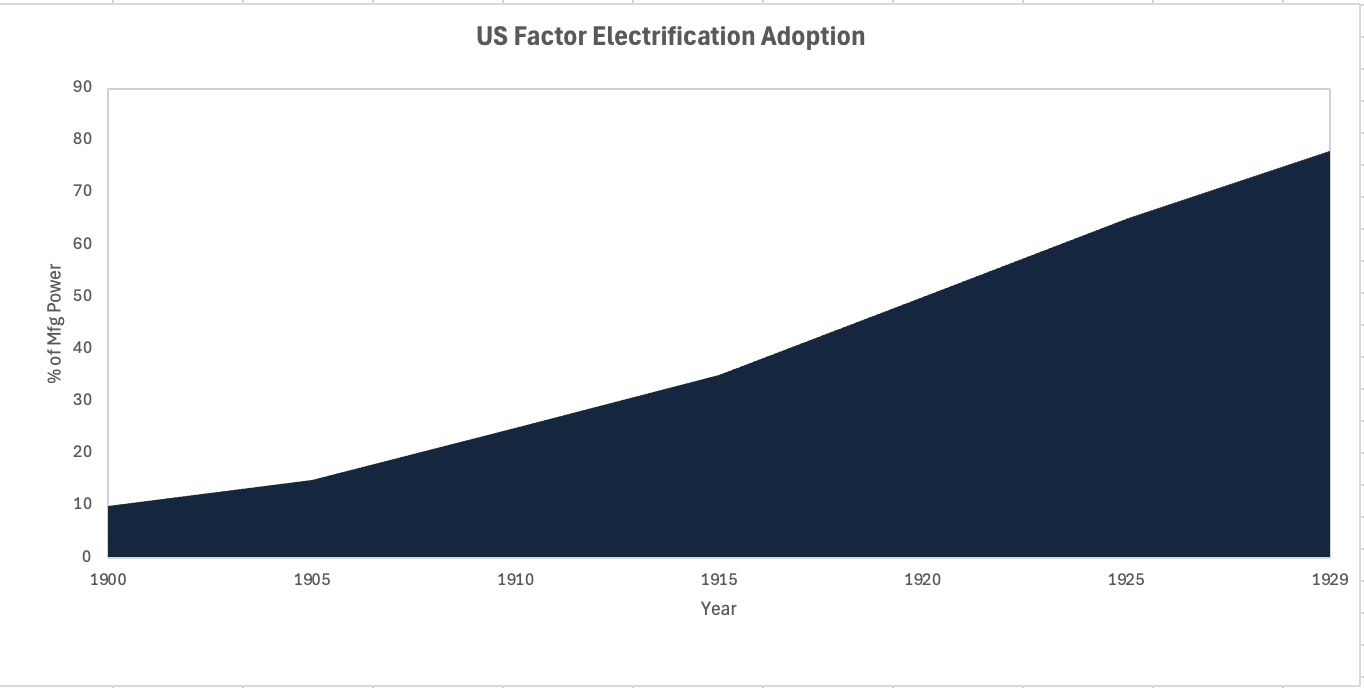

The electrification analogy is more precise than it first appears. Between 1900 and 1929, electricity's share of US manufacturing power rose from 10% to 78%. The transition was not linear; it required a complete redesign of factory layout, power distribution, and machine organisation. Manufacturers who electrified increased productivity and output relative to those who did not. Those who delayed long enough did not survive to close the gap. The structural dynamic today is equivalent: AI adoption requires process redesign, not just tool procurement, and the firms that understand this distinction are pulling ahead at a rate their competitors have not yet measured.

US manufacturing electrification, 1900–1929. Electricity's share of manufacturing power rose from 10% to 78% in under three decades. Mill owners who delayed reorganising their factory architecture did not rebound — they were acquired or collapsed. The AI transition is structurally identical: the compounding begins in the workflow redesign, not in the tool itself. Source: NBER, OSTI.

The Non-Obvious Mechanism

The consensus view treats AI as a productivity tool: invest, automate some tasks, reduce some costs. The more consequential mechanism runs one level deeper. What AI actually does, when integrated at the process level, is compress the relationship between revenue and the human capital required to generate it. The consequence is not just lower costs — it is a structurally lower cost-to-revenue ratio that becomes visible in margin comparisons and, eventually, in valuation differentials.

Enterprise AI spending reached $37 billion in 2025, up from $11.5 billion in 2024 — a 3.2-fold increase in a single year. Goldman Sachs Research projects that generative AI could raise labour productivity by approximately 15% when fully integrated across developed markets. McKinsey's April 2026 analysis goes further, arguing that using AI to boost productivity alone is unlikely to create a sustainable advantage: the real value lies in reshaping offerings and business models. That distinction is precisely what most boards are missing.

The firms accumulating a "productivity debt" are not those ignoring AI entirely — most have pilots running somewhere. The firms at risk are those treating AI adoption as a departmental initiative rather than an operating model decision. They are acquiring the vocabulary of transformation without redesigning the processes that determine their cost base. The productivity paradox documented in manufacturing is real: MIT Sloan research confirms that AI adoption tends to reduce productivity in the short term before delivering stronger output. Firms without the organisational commitment to absorb that short-term disruption will stall at the pilot stage indefinitely.

Revenue per employee: AI-native firms vs traditional counterparts, 2025. The gap is not incremental — it reflects a fundamentally different operating architecture. Source: Menlo Ventures, Bessemer Venture Partners.

Investor and Stakeholder Implications

For M&A practitioners and corporate advisers, the investment thesis is straightforward once you accept the underlying mechanism. Companies with legacy process architecture, high middle-management headcount, no AI integration roadmap, and low revenue-per-employee ratios are trading at discounts they do not yet understand. They believe they are valued at a cyclical low. The more likely read is that they are priced for what they are: a structurally higher-cost business in a market that is repricing cost efficiency.

Global M&A value reached an estimated $4.8 to $4.9 trillion in 2025 — the second-highest year on record, up 40% from 2024. AI-related deal activity accelerated within that surge, rising from $45 billion in 2022 to $310 billion in 2025. Crucially, the character of AI M&A in 2025 shifted: deals became less about acquiring revenue and more about securing capability, talent, and process infrastructure. That is a signal of where the scarcity is. The acquirers understand that the time to buy a transformation mandate is before the target's board does.

AI-related M&A deal activity, 2022–2025. From $45B to $310B in three years: the acquirers are those who transformed early; the targets are those who did not. Source: Bain & Company, Morrison Foerster.

The distressed value and transformation mandate pipeline is forming now, not in 2028. The identifiable profile of a target is specific: sector-leading revenue in a process-heavy industry (financial services operations, professional services, mid-market manufacturing, insurance), combined with headcount ratios that have not shifted in three years, no disclosed AI integration programme, and margins that are flat or softening. These businesses are not distressed in the traditional sense — they are structurally expensive, and the market has not finished repricing that.

Near-Term Catalysts and Policy Outlook

The asymmetry of risk here is unusual: the downside for laggards is structural and permanent; the downside for early movers is a short-term productivity dip followed by durable margin improvement. The next two to three quarters will be the first earnings cycles where that asymmetry becomes visible in reported numbers.

0–3 month window (May–August 2026): Q2 earnings reports will begin showing divergence in cost-to-revenue ratios between AI-integrated firms and those still at pilot stage. Analysts covering enterprise software, professional services, and financial technology will start asking the question boards have been avoiding: where is your AI integration reflected in unit economics? Any company unable to answer will face multiple compression.

3–12 month window (September 2026–May 2027): The first wave of transformation-motivated M&A mandates will emerge in earnest. Private equity, which has been building AI operating capability in portfolio companies, will begin targeting asset-heavy businesses with high labour-to-revenue ratios and no credible transformation roadmap. Strategic acquirers in technology and financial services will use the window before targets begin to understand the discount at which they are trading.

The policy environment adds a further dimension. Clifford Chance's 2026 global M&A analysis notes that regulators are taking a more proactive stance on technology deals, with particular attention to transactions that might entrench dominance or eliminate future competitors. For cross-border deals involving AI-capable acquirers and operationally legacy targets, regulatory scrutiny will extend timelines and increase deal complexity. This creates a further advantage for well-positioned acquirers who engage early: the longer a target waits to understand its own situation, the more compressed the deal window becomes.

The scenario range for the next twelve months narrows considerably once you price the policy variable correctly:

Base case: Earnings divergence becomes visible by Q3 2026; transformation mandates accelerate through 2027; AI-laggard businesses in process-heavy industries trade at 15–25% discounts to AI-integrated peers within 18 months.

Upside: Rapid regulatory clarity on AI liability in the EU and US accelerates corporate investment in AI integration; the divergence compresses faster than base case; M&A window shortens.

Downside: A major AI reliability failure or regulatory intervention causes enterprise adoption to stall; the productivity gap widens more slowly, but the structural dynamic does not reverse — it merely delays.

Conclusion

The electrification parallel is not rhetorical. It is structurally precise: both transitions require a redesign of the operating architecture, not just the tools; both produce a compounding advantage for early movers; and both create acquisition targets from firms that waited too long to make a capital commitment. The difference is that the current transition is faster. Electricity took three decades to move from 10% to 78% of manufacturing power. AI integration is moving on a five-year cycle, not thirty.

The structural case for action is not that AI is transformative in the abstract. It is that cost-to-revenue ratios are diverging now, that M&A activity is already accelerating around the capability gap, and that the window in which a board can make this decision on its own terms — rather than a prospective acquirer's — is closing. The companies that will define the next decade of their industries are not those that recognised AI's potential earliest. They are those that redesigned their operating models before the margin compression forced the decision for them.

References

Menlo Ventures – 2025: The State of Generative AI in the Enterprise – December 2025

Web Strategist – AI Startups are Dominating Traditional Software in One Key Metric – May 2025

Bessemer Venture Partners – State of Health AI 2026 – January 2026

MIT Sloan Management Review – The Productivity Paradox of AI Adoption in Manufacturing Firms – July 2025

Law & Economics Centre – AI, Productivity, and Labor Markets: A Review of the Empirical Evidence – February 2026

Bain & Company – Looking Back at M&A in 2025: Behind the Great Rebound – December 2025

Morrison Foerster – M&A in 2025 and Trends for 2026 – January 2026

Goldman Sachs Asset Management – Market Know-How 2Q 2026 – April 2026

McKinsey & Company – Where AI Will Create Value — and Where It Won't – April 2026

Clifford Chance – Global M&A in 2026: Our Top 10 Predictions – 2026

NBER Working Paper – Electrification and Productivity in US Manufacturing – 2002

OSTI / US DOE – Historical Perspective of the Value of Electricity in American Manufacturing – archived

Grand View Research – Artificial Intelligence Market Size Report – 2025

Goldman Sachs – Why AI Companies May Invest More Than $500 Billion in 2026 – December 2025

This article is for information and discussion only and does not constitute investment advice or a recommendation