You Can't Electrify a Pyramid From the Top

The professional services business model has not been disrupted. It has been repriced. The firms that have not noticed will discover the difference in the next two earnings cycles.

Why This Matters

The high-margin, high-volume work that funds professional services pyramids — drafting, reviewing, researching, modelling — is precisely what generative AI delivers fastest and cheapest, not the work at the top.

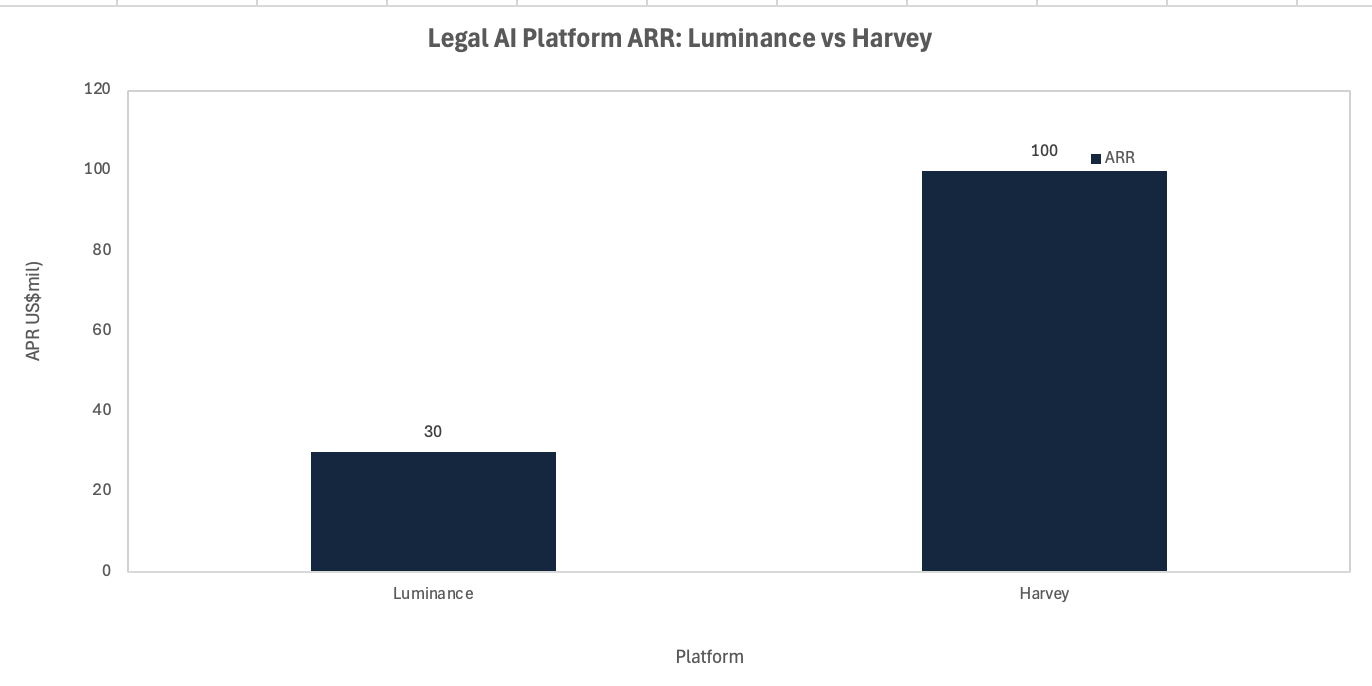

Legal AI platforms are already embedded directly inside Fortune 500 in-house teams, bypassing panel firms at scale; Luminance reached $30M ARR in 2024, up 150% year-on-year, and Harvey is estimated at ~$100M ARR in 2025.

The coming M&A wave in professional services will not be driven by organic consolidation; the acquirers will be tech-augmented operators, and the targets will be firms still billing for hours a model now completes in minutes.

The Core Shift

The billable hour is not being challenged by a pricing trend. It is being structurally dismantled by a cost curve. Generative artificial intelligence (AI) performs the tasks that represent the largest share of revenue in professional services — contract drafting, due diligence, audit sampling, tax compliance, benchmarking research, and financial modelling — at a fraction of the time and cost required by a team of associates or junior analysts. What clients are beginning to realise, and what managing partners are slow to admit, is that the hours being billed are the hours most easily eliminated.

The professional services industry in the United States generates over $405 billion in legal revenues alone, with the Am Law 100 collectively producing $178.95 billion in gross revenue and an average revenue per lawyer of $1.39 million in 2025. Those figures look healthy. They do not yet reflect the structural erosion already underway in the layer below the partner level, where the volume work sits. An ex-PwC senior figure has stated publicly that most structured, data-heavy tasks in audit, tax, and strategic advisory will be automated within three to five years, potentially eliminating approximately 50% of roles in those areas, with AI solutions already capable of performing 90% of the audit process. That is not a long-range forecast. It is a description of what is already deployable.

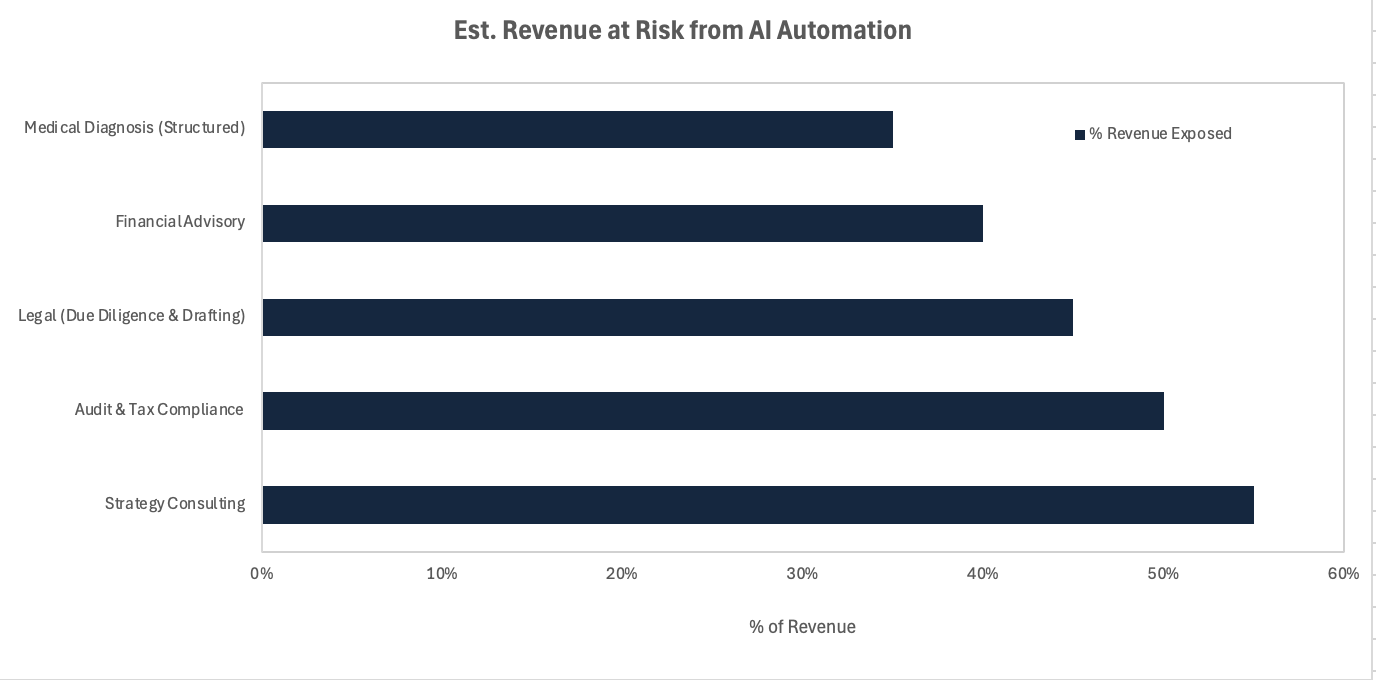

Estimated share of high-volume task revenue exposed to AI automation by 2030, across professional services segments. Sources: ex-PwC analysis, BPM Outlook 2026, Cherry Bekaert 2026. The methodology isolates structured, repeatable task revenue rather than total sector revenue.

The Non-Obvious Mechanism

The conventional read is that AI will eliminate junior roles and compress margins on commodity work, while senior expertise remains safe. That is partially correct and almost entirely beside the point. The mechanism that consensus has not followed to its conclusion is a pyramid funding problem: senior partners are expensive because they were made profitable by the leverage underneath them. A Magic Circle equity partner generating £3–5 million in profit per equity partner (PEP) is only economically rational when six associates billing 200 hours each on due diligence are funding the model. Remove the associates; the economics of the senior layer become far harder to justify to clients who can now see what the work actually cost to produce.

This is the Kodak parallel in precise form. Kodak did not fail because it could not make a digital camera; it failed because digital photography destroyed the film and processing revenues that cross-subsidised everything else. Professional services firms face the same problem: the AI does not need to replace the senior partner's judgment to destroy the business model. It only needs to replace the volume work that makes the model viable. Value-based and subscription pricing models are already gaining momentum as clients demand measurable outcomes rather than hours worked, and firms restructuring along these lines are expected to hold a significant competitive advantage in 2026 and beyond. The firms holding the old model are not being cautious; they are being slow.

Investor and Stakeholder Implications

For capital allocators, the divergence between firms that have restructured delivery and those that have not is a sourcing signal as much as a risk flag. Firms that rebuild around AI-leveraged senior judgment — where one experienced professional delivers the output previously requiring a team — will compress costs, expand margins, and scale without headcount. The Big Four are already moving in this direction: KPMG's increased partner pay is a direct result of scaling without proportional headcount growth, as technology replaces the need for large junior staff teams. That is not altruism; it is the model proving itself in real-time.

For clients and corporate boards, the implication is a shift in negotiating leverage that has not yet been fully priced into panel arrangements. CFOs are already pushing General Counsels to cut external legal spend, and AI-augmented boutiques are pitching at a fraction of Magic Circle rates for work that is structurally identical. The risk for large incumbent firms is not sudden collapse; it is a slow attrition of mid-market mandates that eventually makes the fixed cost base — prime office, graduate recruitment, global infrastructure — unsustainable relative to revenue. Mid-tier strategy consultancies whose differentiation rests on slide production and benchmarking synthesis are particularly exposed, as those are precisely the tasks where generative AI delivers fastest and at lowest marginal cost.

Annual recurring revenue for leading legal AI platforms. Luminance: $30M ARR in 2024, up 150% year-on-year. Harvey estimated at ~$100M ARR in 2025. Both platforms are embedded directly inside corporate in-house legal teams, bypassing traditional panel firms. Sources: Sacra (May 2025); industry estimates.

Near-Term Catalysts and Policy Outlook

The window for managing this transition rather than reacting to it is measured in quarters, not years. The asymmetry of risk is clear: firms that move early restructure on their own terms; firms that delay will restructure under client pressure or at valuation compression.

0–3 month window. The next earnings and fee cycles will begin surfacing margin divergence between firms that have rebuilt delivery and those that have not. Expect further enterprise contract announcements between legal and advisory AI platforms and Fortune 500 in-house teams: Harvey launched Contract Intelligence specifically for in-house counsel in May 2026, with general availability targeted for Q3. Each announcement narrows the addressable market for panel firms on the work type in question.

3–12 month window. M&A in professional services will accelerate, with private equity increasing its focus on scalable, high-margin firms demonstrating AI adoption, workflow automation, and client data platform integration. Firms that demonstrate AI-leveraged delivery will command premium valuations; those still charging for automated hours will find themselves acquisition targets at distressed multiples rather than platform anchors. The pattern visible in the broader M&A market — approximately one-third of the 100 largest transactions in 2025 cited AI as part of the strategic rationale — will migrate firmly into professional services deal flow in 2026.

The more likely scenario over the next 12 months is as follows:

Base case: Continued margin bifurcation. AI-augmented boutiques and in-house platforms take incremental share on volume work. Incumbent firms hold revenue headline numbers through rate increases on retained senior work, masking the underlying volume erosion. No systemic collapse, but a structural ratchet that does not reverse.

Upside case: A wave of proactive restructuring among mid-tier firms — deliberately shrinking the associate pyramid, redeploying capital into proprietary AI tooling, and repositioning on outcome-based pricing — creates a new cohort of high-margin, scalable operators. Deal flow and capital follow the restructured model; the incumbents who move fast set the new valuation benchmark.

Downside case: A large incumbent firm faces a public pricing dispute with a major corporate client who presents AI-generated work product as evidence that billed hours were not required. Regulatory scrutiny of billing practices follows. The reputational cascade accelerates client attrition beyond what the model can absorb through rate increases alone.

Conclusion

The structural read is straightforward: professional services is not experiencing a technology upgrade cycle; it is undergoing a cost structure reset that will separate firms capable of delivering senior judgment at scale from those dependent on volume billing to remain profitable. The historical parallel with electrification is not rhetorical. The firms that delayed rewiring in the 1890s did not survive as premium boutiques; they became footnotes. The geopolitical overlay adds urgency: as corporates retrench spending under macro uncertainty and CFOs prioritise cost discipline, the internal pressure to replace external panel spend with AI-augmented in-house capability will compound. The firms treating this as an optional strategic question are, in effect, defending a pyramid from the top. The base is already being removed.

References

BPM — Professional Services Industry Outlook 2026 — November 2025

Cherry Bekaert — 2026 Professional Services Industry Trends & Outlook — February 2025

Sacra — Luminance at $30M ARR — May 2025

Business Insider / ex-PwC (Alan Paton) — AI is Coming for the Big Four — May 2025

IBISWorld — Law Firms in the US Industry Analysis — 2025/2026

BCG Attorney Search — 2026 Am Law 100 Most Profitable Law Firms — 2026

Artificial Lawyer — Harvey Announces Contract Intelligence for Inhouse — May 2026

PwC — Global M&A Industry Trends: 2026 Outlook — January 2026

Supervizor — Big Four in the Age of AI: How Audit Giants Are Transforming — April 2025

newsbywire — Private Equity and Professional Services M&A Trends 2025–2026 — January 2026

This article is for information and discussion only and does not constitute investment advice or a recommendation.