Shadow Climate Finance: How Transition Risk Is Migrating Off‑Balance‑Sheet in the Age of Controlled Disorder

Author: Justin Kew

Shadow climate finance is quietly moving the most acute transition risks from regulated balance sheets into opaque structures where they are harder to price, supervise and hedge. This shift is accelerating in a world of “controlled disorder”: policymakers signalling tighter climate policy over time while avoiding abrupt shocks, encouraging risk warehousing in the shadows rather than genuine balance‑sheet adaptation.

Why this matters

Transition risk is not falling; it is being reassigned from banks and insurers to securitisations, funds, structured credit and offshore vehicles.

Reported financed emissions and regulatory capital ratios are improving just as systemic climate risk becomes more fragmented and less observable.

In a disorderly transition, losses will crystallise where data are poorest and liquidity least reliable – in the shadow system, not in the stress‑tested banking core.

What is changing

The formal banking and insurance sectors are under sustained pressure to quantify, price and hold capital against climate transition risk, while most shadow entities face looser or no dedicated requirements. Supervisors and central banks have focused scenario analysis, disclosure and prospective capital tools on regulated balance sheets, implicitly creating incentives to migrate problematic exposures elsewhere.

Three structural shifts stand out:

From loans to capital markets: Banks increasingly intermediate fossil‑heavy and high‑transition‑risk exposures via underwriting, securitisation and distribution rather than long‑term on‑balance‑sheet lending, particularly through bond markets and structured credit.

From core to shadow banking: Empirical work now links higher climate vulnerability to a relative expansion of shadow banking versus traditional bank assets, pointing to a substitution of intermediation channels as climate risks intensify.

From direct to synthetic exposures: Derivatives and insurance structures transfer emissions‑linked and transition risks without corresponding transparency in who ultimately owns the tail risk, especially across investment funds, hedge funds and bespoke vehicles.

For senior investors, the headline picture of “de‑risked” bank balance sheets increasingly masks a transfer – not a reduction – of transition risk across the financial network.

The non‑obvious mechanism

The core mechanism is regulatory and reputational arbitrage around climate metrics and capital requirements, not simply yield‑seeking in carbon‑intensive assets. As climate capital rules tighten and financed‑emissions disclosures harden, banks and insurers face mounting incentives to transform climate exposures into fee‑earning, off‑balance‑sheet business or to shift them to entities without equivalent scrutiny.

Key channels:

Loan securitisation and “carbon offloading”

Fossil‑linked and high‑emitting corporate loans are securitised and placed with less‑regulated investors, reducing reported financed emissions and risk‑weighted assets for originating banks.

This frees capital and improves climate metrics while leaving aggregate transition risk unchanged or higher if securitisation concentrates risk in thin‑capitalised vehicles.

Emissions risk transfers and shadow insurance

Bespoke guarantees, insurance‑linked structures and derivatives transfer climate‑related credit and market risk to non‑bank, often offshore entities that are outside standard prudential or climate disclosure regimes.

Insurers themselves are experiencing rising climate risk on both sides of the balance sheet, but can respond by repricing, tightening coverage or using reinsurance and capital‑markets solutions that again push tail risk outward.

Bond financing and underwriting pipelines

Banks arrange and underwrite bonds for carbon‑intensive corporates, generating fee income while limiting long‑term on‑book exposure; the duration and transition risk are ultimately held by asset managers, insurers and pension funds.

Where these instruments are packaged into funds or structured credit products, the underlying climate risk becomes harder to trace across holders, especially in cross‑border portfolios.

The second‑order effect is that network topology of climate risk is changing faster than aggregate exposures: the same transition shock now hits a more complex, less supervised graph of counterparties, amplifying contagion potential.

What investors are missing

Market attention still gravitates to headline financed‑emissions and direct fossil lending exposure at large banks, even as system‑wide climate risk migrates towards entities that combine leverage, liquidity mismatch and thin governance. Three blind spots are notable:

Misreading improving bank metric

Falling reported financed emissions, “green” lending ratios and reassuring climate stress test outputs are increasingly shaped by portfolio structure and risk transfers rather than real‑economy decarbonisation.

Supervisory reluctance to hard‑wire climate capital charges – precisely because of model uncertainty and pro‑cyclicality – encourages more complex off‑balance‑sheet risk‑sharing instead of transparent repricing or withdrawal of credit.

Underweighting shadow‑system fragility

Shadow banking has grown faster in more climate‑vulnerable economies, indicating that transition and physical risks are being warehoused in less regulated credit channels.

Fire‑sale dynamics and margin spirals around climate‑sensitive assets are more likely in funds and leveraged vehicles with daily liquidity and mark‑to‑market constraints than in regulated bank books.

Ignoring cross‑sector interdependencies

Agent‑based modelling for climate transition shocks shows material indirect effects propagating via cross‑holdings and common exposures among banks, insurers, pension funds and investment funds.

Insurance balance sheets are particularly exposed through both liabilities (claims) and assets (portfolios), yet their de‑risking moves can amplify pressures on credit markets and funding costs for high‑emitting sectors.

The mispricing is not simply at the sector level; it sits in the capital structure and risk packaging of climate‑sensitive assets, from mezzanine tranches of securitisations to derivative books referencing transition‑exposed indices.

Why this matters now

The next 12–18 months are likely to deliver a step‑change in how supervisors treat climate risk – still framed as “controlled disorder”, but with sharper edges. Policy is coalescing around three levers:

Enhanced disclosures and templates (0–12 months)

The European Banking Authority is consulting on more granular disclosure templates for climate transition risk, including exposures to “top 20” carbon‑intensive corporates and to shadow entities, with explicit breakdowns of on‑ and off‑balance‑sheet exposures.

Global standard‑setting bodies and central banks are deepening climate scenario analysis, with updated guidance emphasising forward‑looking risk assessments across the entire financial system, not just core bank books.

Climate‑sensitive capital regimes (12–36 months)

Technical work shows that climate‑related credit exposures can pose solvency threats to European banks under more stringent policy scenarios, strengthening the case for macroprudential capital tools such as “brown penalising factors” and “green supporting factors”.

Policymakers recognise that without such tools, banks could amplify systemic risk during an aggressive decarbonisation, reinforcing the need to buffer transition shocks in advance.

New conditionality and sovereign‑system linkages (ongoing)

Facilities such as the IMF’s Resilience and Sustainability Facility explicitly tie sovereign support to building climate risk analysis and stress testing capabilities in domestic financial systems, including disclosure and risk‑assessment reforms for banks.

This embeds climate risk into the broader architecture of sovereign surveillance and conditionality, raising the stakes for jurisdictions with large shadow systems and limited supervisory reach.

In this context, transition risk that has migrated off regulated balance sheets is poised to be “rediscovered” as authorities extend scrutiny across funds, insurers and cross‑border structures.

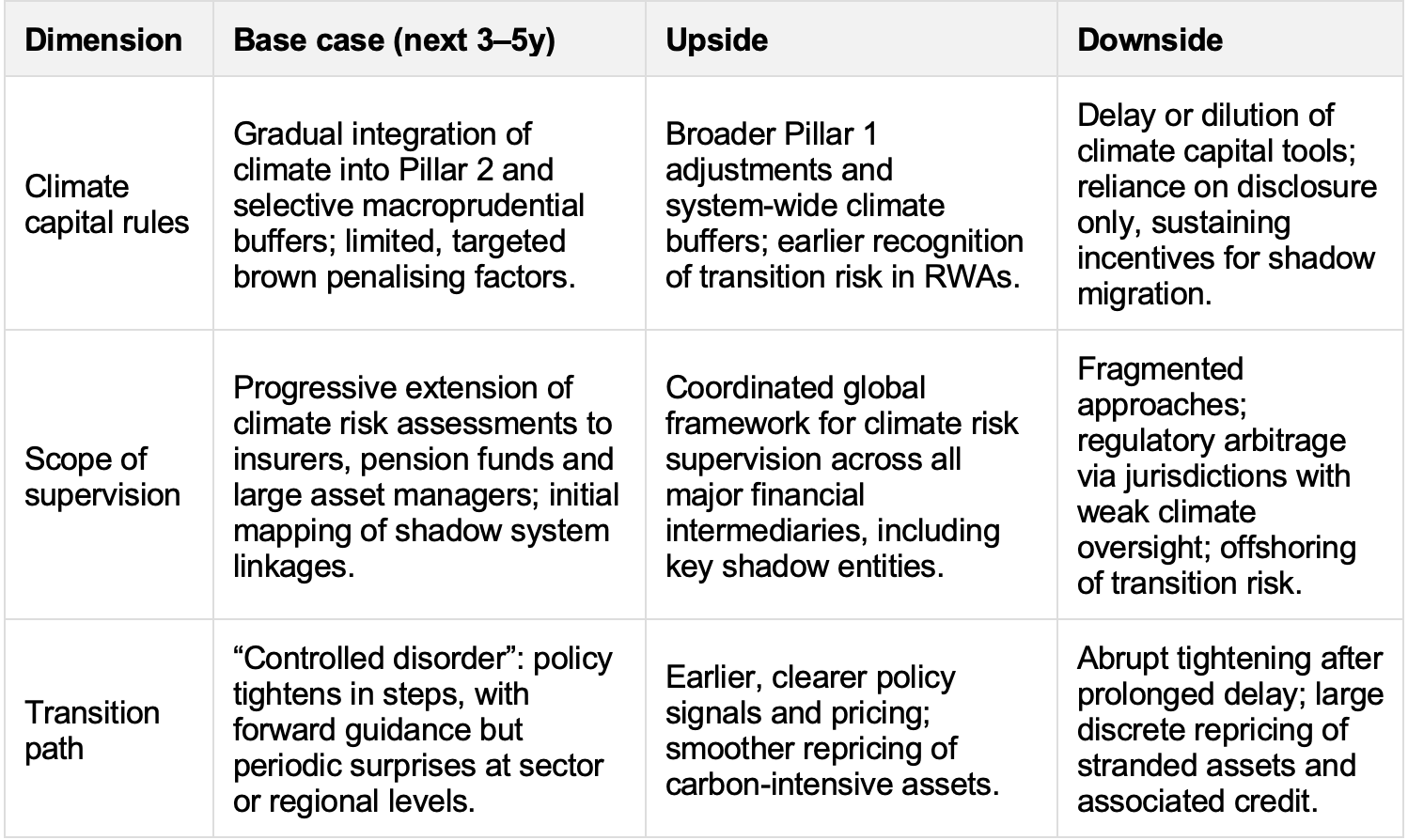

Policy outlook and scenarios

Climate financial policy is converging on a regime where climate risk is treated as a core prudential and macro‑financial concern, but the path is uneven and politically constrained. A practical scenario grid:

The non‑consensus element is that even in the base case, policy evolution increases the probability that off‑balance‑sheet climate risk will be forced back into view – either through capital add‑ons, disclosure of look‑through exposures, or stress‑induced failures in shadow entities.

Sector, supply‑chain and asset implications

The migration of transition risk off balance sheet changes who ultimately absorbs climate losses, with implications for cash flows, funding costs and market structure across sectors.

Banks

Cash flows shift from net interest income on carbon‑intensive lending towards fee income from underwriting, securitisation and risk transfer, but contingent reputational and legal risks remain if transactions are seen as “greenwashing by structuring”.

Cost of capital may fall in the short term due to cleaner climate metrics and supportive disclosures, yet rise later if supervisors impose climate buffers that treat risk transfers as imperfect and demand group‑wide consolidation of exposures.

Insurers and reinsurers

Liability cash flows become more volatile due to climate‑related claims and repricing, while asset portfolios remain exposed to transition shocks; use of reinsurance and insurance‑linked securities can disperse risk but also obscures final loss‑bearers.

Regulatory moves to integrate climate into solvency frameworks would raise capital charges for concentrated exposures and potentially incentivise further use of capital‑markets solutions, again pushing risk into less regulated structures.

Asset managers, pension funds, sovereign investors

These entities become the primary holders of securitised and bond‑based transition risk, often in vehicles marketed as diversified or “sustainable”, creating a disconnect between labels and embedded climate beta.

Liquidity and redemption terms will determine whether they act as buffers or amplifiers in a transition shock; open‑ended funds with climate‑sensitive holdings are particularly vulnerable to runs and forced selling.

Real‑economy sectors

High‑emitting corporates may perceive continued access to market‑based funding as evidence that transition risk is manageable, even as their investor base shifts towards actors with shorter horizons or higher leverage.

Supply‑chain and regional climate vulnerabilities will increasingly matter for credit spreads and equity premia, with climate‑sensitive sovereigns facing compounded risks through both public and private balance‑sheet channels.

From an investor’s lens, the key is where in the capital structure climate risk is crystallising and which balance sheets are designed – or not – to absorb it without forced deleveraging.

Non‑consensus takeaway

Transition risk is evolving from a “single‑institution solvency” problem into a network plumbing problem: the core question is less which banks have lent to whom, and more which shadow structures sit between climate‑sensitive assets and ultimate capital providers. This makes climate risk resemble pre‑GFC credit more than a slow‑burn ESG externality, with complexity and opacity doing more work than absolute exposure size in determining systemic outcomes.

The shift is structural: as long as climate policy remains in a regime of controlled disorder – ratcheting up over time but avoiding explicit, predictable carbon prices – financial institutions will continue to arbitrage climate rules by redesigning instruments and intermediation chains, not just by reallocating capital. For senior allocators, the defensible but under‑owned position is to treat shadow climate finance as a distinct risk factor, mapped and priced at the level of structures and counterparties rather than sectors alone.

References

Out of the Light, Into the Dark: How Shadow Carbon Financing Hampers the Green Transition, Schairer et al., 2025.

SuFi Network paper on loan securitisation and shadow carbon financing.

Climate change and the rise of shadow banking: A global analysis, 2025.

Climate risks and banks’ capital requirements, technical report on macroprudential tools.

NGFS Guide to climate scenario analysis for central banks and supervisors.

IMF Global Financial Stability Report, October 2023.

The interdependencies of Canadian financial institutions: Climate transition shock application.

Climate change and European insurance balance sheets, 2025 assessment.

Climate Change Risk Assessment for the Insurance Industry, Geneva Association.

Addressing Climate‑Related Financial Risk Through Bank Capital Requirements, Center for American Progress.

IMF Technical Assistance Report on Climate Risk Analysis, Bangladesh RSF.

EBA Consultation Paper on ESG risk disclosures and transition risk templates.

Climate Strategy and Modelling for Insurance, IFRS 17 report.

Climate risks building in banks’ balance sheets, Sarasin & Partners.