AI's Power Mirage: When Infinite Compute Hits a 175 GW Wall

Author: Justin Kew

Executive Summary

The AI investment narrative is undergoing a fundamental revaluation. Consensus continues to model artificial intelligence as a demand story for semiconductors and hyperscale cloud infrastructure while systematically under-pricing the hard physical constraints that will determine who captures value over the next 24 to 36 months. Grid congestion, multi-year interconnection queues stretching beyond five years in major markets, and escalating power capacity costs are quietly reallocating economics away from GPUs and toward utilities, power producers, transmission infrastructure, and on-site generation—assets that control access to the scarcest input in AI's production function: firm, dispatchable electrons.

This transition will manifest over the next three months as three catalysts converge. First, regional grid operators including PJM Interconnection will implement new tariff structures and interconnection reforms mandated by December 2025 Federal Energy Regulatory Commission (FERC) orders, fundamentally repricing how data centres pay for grid access and behind-the-meter generation.

Second, utilities will update load forecasts and capital expenditure guidance in Q4 2025 and Q1 2026 earnings, revealing which service territories can deliver incremental gigawatts and at what cost to ratepayers.

Third, hyperscale’s will report Q1 2026 results with capital expenditure composition that—if disclosed with sufficient granularity—will show spending shifting from accelerators into substations, land acquisition, backup generation, and power purchase agreements (PPAs), even as headline capex continues to grow.

Differentiation now hinges on identifying which operators have secured—or can credibly secure—scarce power, interconnection rights, and regulatory approval in timeframes compatible with deployment schedules. Those that cannot, will face schedule slippage, rising cost of capital, and margin compression as they compete for a finite pool of sites for energy. The scarcity rent is migrating from silicon to substations, and capital markets have not yet repriced this shift.

The Demand Surge: AI Rewrites Load Forecasts Across Grid Operators

Quantifying the Power Wall

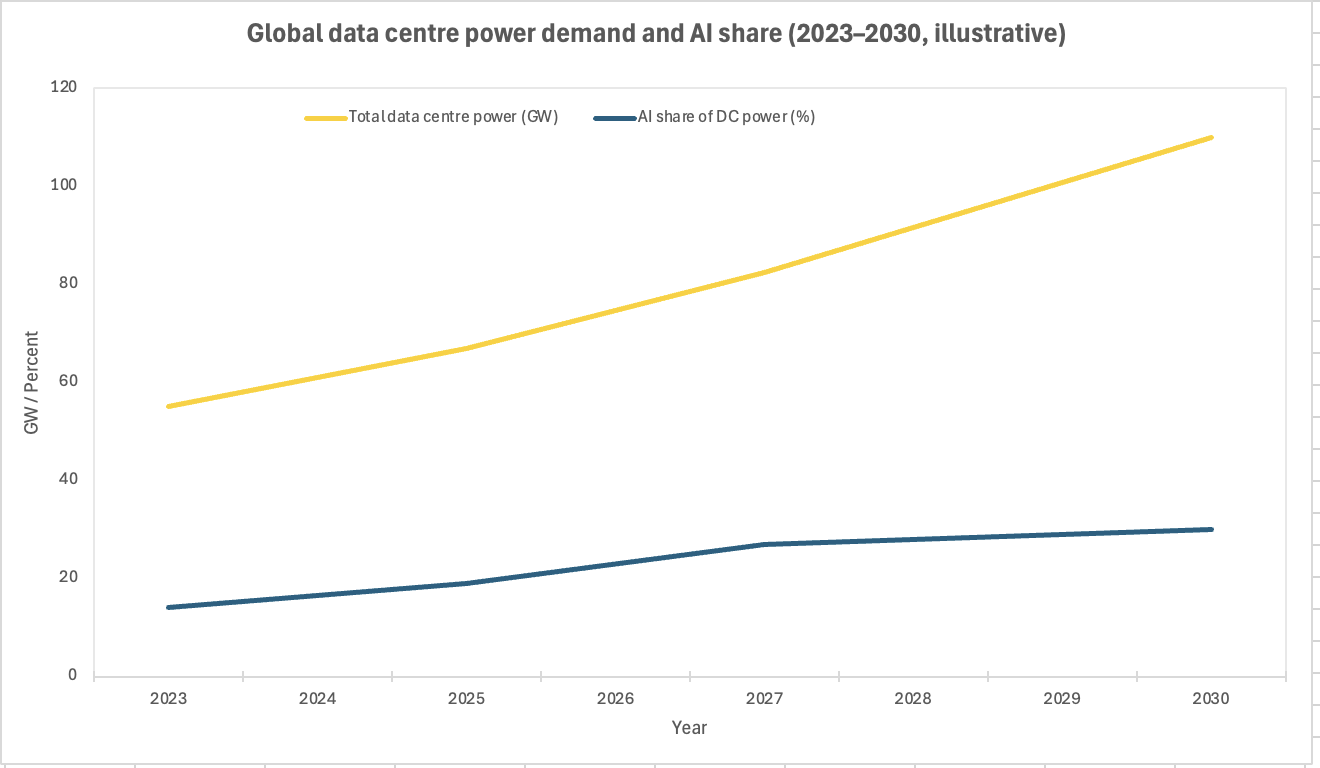

Global data centre power demand stood at approximately 55 gigawatts (GW) in 2023. Goldman Sachs Research forecasts this will rise 50% to roughly 82.5 GW by 2027, with artificial intelligence's share of that load climbing from 14% to 27% over the same period. Within the United States, projections are even more dramatic: Bloomberg Intelligence estimates that domestic data centre electricity consumption could quadruple by 2032, driving data centres to account for 7% to 20% of total U.S. electricity demand depending on adoption scenarios, up from approximately 2% today. S&P Global's 451 Research expects utility-supplied power to data centres to increase by roughly 11 GW in 2025 alone, reaching 62 GW, and forecasts demand will nearly triple to approximately 183 GW by 2030.

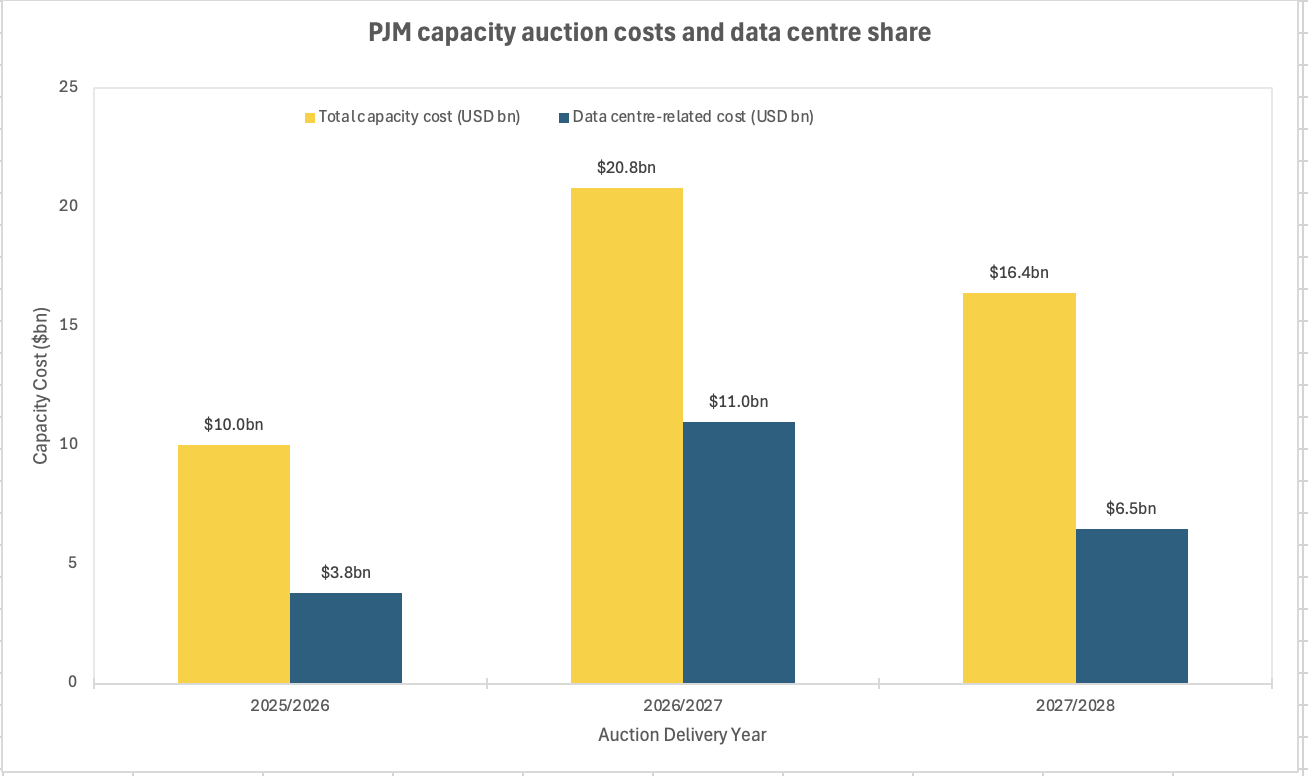

These are not abstract projections. They are already reshaping capacity markets and transmission planning. In December 2025, PJM Interconnection—the largest U.S. grid operator, serving 67 million people across the Mid-Atlantic and Midwest—held its base residual capacity auction for the 2027/2028 delivery year. Data centre load accounted for $6.5 billion, or 40%, of the $16.4 billion in total auction costs, with approximately $6.2 billion tied to facilities that have not yet been constructed but could come online by June 2027. Across PJM's last three capacity auctions, data centre forecasts above existing load totalled $21.3 billion, representing 45% of the $47.2 billion in cleared capacity costs. PJM's forecast for the 2027/2028 delivery year is approximately 5,250 MW higher than the prior auction, with nearly 5,100 MW of that increase directly attributable to data centre demand.

Yet the auction cleared 6,516.6 MW short of PJM's reliability target, and PJM's independent market monitor flagged "extreme uncertainty in the load forecasts based on uncertainty about the addition of large data centre loads," noting that this uncertainty is "unique and unprecedented." The monitor's concern is well-founded: many of these capacity commitments are based on load projections for facilities that may never materialize, or that will materialize years later than forecast, creating a structural mismatch between paid-for capacity and actual consumption—a gap that other ratepayers will ultimately finance.

The National Backdrop: Record Load Growth Meets an Aging Grid

Data centres are not expanding into spare capacity; they are adding to record national electricity demand. The U.S. Energy Information Administration projects total domestic electricity consumption will reach approximately 4,179 terawatt-hours (TWh) in 2025 and 4,239 TWh in 2026, both figures exceeding the 2024 record. This growth is driven not solely by AI and cloud computing but also by electrification of transportation, industrial reshoring, and residential heat pump adoption, meaning data centres are competing for electrons in a system already operating near peak load in several regions.

Utility capital expenditure is responding, but on timescales incompatible with GPU refresh cycles. S&P Global estimates that major U.S. utilities will spend approximately $84.9 billion on transmission and distribution (T&D) in 2025, with a five-year pipeline through 2029 totalling roughly $436 billion—an increase of nearly 46% compared to projections made in 2023. Individual utilities are revising capital plans upward at extraordinary rates: Duke Energy raised its five-year capital plan from $87 billion to $100 billion; American Electric Power (AEP) increased its plan from $54 billion to $72 billion, a 33% jump; and Dominion Energy, Southern Company, Entergy, and Xcel Energy have all announced multi-billion-dollar expansions explicitly tied to data centre load growth.

These investments reflect a fundamental truth: the binding constraint on AI infrastructure is not chip supply, but the ability to deliver firm, reliable power to facilities consuming 100 MW or more—equivalent to the electricity demand of roughly 80,000 homes. Hyperscale AI campuses planned by Meta, Google, and Microsoft are targeting 1 GW to 5 GW of load per site, a scale that dwarfs the capacity of most existing substations and requires multi-year transmission upgrades, new generation interconnections, or dedicated on-site power.

The Interconnection Crisis: A 2,600 GW Queue Versus a 1,280 GW Fleet

The Bottleneck in Numbers

The interconnection queue—the regulatory process by which new generation or large loads request connection to the grid—has become the single largest impediment to data centre deployment in power-constrained regions. As of 2023, the aggregate installed capacity of the entire U.S. power plant fleet was approximately 1,280 GW. Yet the capacity requested and awaiting interconnection study across all U.S. independent system operators (ISOs) reached 2,600 GW—more than double the current grid. Projects that reached commercial operation in 2023 took an average of nearly five years from initial interconnection request to energization, up from fewer than two years in 2008. In California ISO (CAISO), project timelines now average close to eight years.

The overwhelming majority of these requests—approximately 1,570 GW of generator capacity and 1,030 GW of storage—are for renewable and storage projects. However, data centres represent a new category of "high-impact large load" that has compounded queue congestion. In Texas, the Electric Reliability Council of Texas (ERCOT) reported more than 2,000 interconnection requests in its queue as of May 2025, many tied to data centre and industrial electrification projects. PJM's interconnection queue similarly shows explosive growth, with 190 GW of active projects awaiting study in AEP's service territory alone as of late 2025.

Crucially, only 20% of projects that requested interconnection between 2000 and 2018 reached commercial operation by the end of 2023. Over 70% of requests are ultimately withdrawn, often after developers discover that required network upgrades make projects uneconomic or that timelines extend well beyond financing windows. This high attrition rate reflects the structural mismatch between speculative project requests and the grid operator's capacity to study and approve them, creating a "queue within a queue" where even projects with firm commitments face multi-year delays.

Regulatory Response: FERC's December 2025 Intervention

Recognizing that existing interconnection frameworks cannot accommodate the scale and speed of AI-driven load growth, FERC issued a unanimous order on December 18, 2025, directing PJM to establish clear rules for co-locating data centres with generation assets. The order mandates three new transmission service options—Firm Contract Demand Service, Non-Firm Contract Demand Service, and Interim Network Integration Transmission Service—each designed to allow data centres to contract for specific grid capacity while drawing primary power from co-located generators.

Critically, the order requires that behind-the-meter generation (BTMG) arrangements above a specified megawatt threshold must now undergo full interconnection studies to assess grid reliability impacts, and that the interconnection customer—not other ratepayers—must pay the full cost of any required modifications or network upgrades before the generator can withdraw capacity to serve a co-located load. This represents a sharp break from prior practice, where some co-located, arrangements effectively netted out load from the grid without paying for the transmission infrastructure required to maintain system reliability.

A parallel reform occurred in January 2026, when FERC accepted Southwest Power Pool's new "High Impact Large Load Generation Interconnection Agreement" (HILLGA) process, explicitly acknowledging that data centres require bespoke interconnection treatment distinct from traditional industrial customers. The White House and a coalition of state governors issued joint principles in mid-January 2026 calling for accelerated interconnection timelines, but these principles come with no binding deadlines and face multi-year implementation lags.

For investors, the implication is clear: the era of implicit grid subsidies for co-located data centres is ending, and the cost of interconnection—both in dollars and time—is being repriced upward. Projects that assumed a 24-to-36-month path to energization must now plan for five to eight years in most regions or accept the full cost of building dedicated transmission infrastructure on their own balance sheets.

The Hyperscaler Response: $602 Billion in 2026 Capex and the Pivot to Power

The Capital Intensity Shock

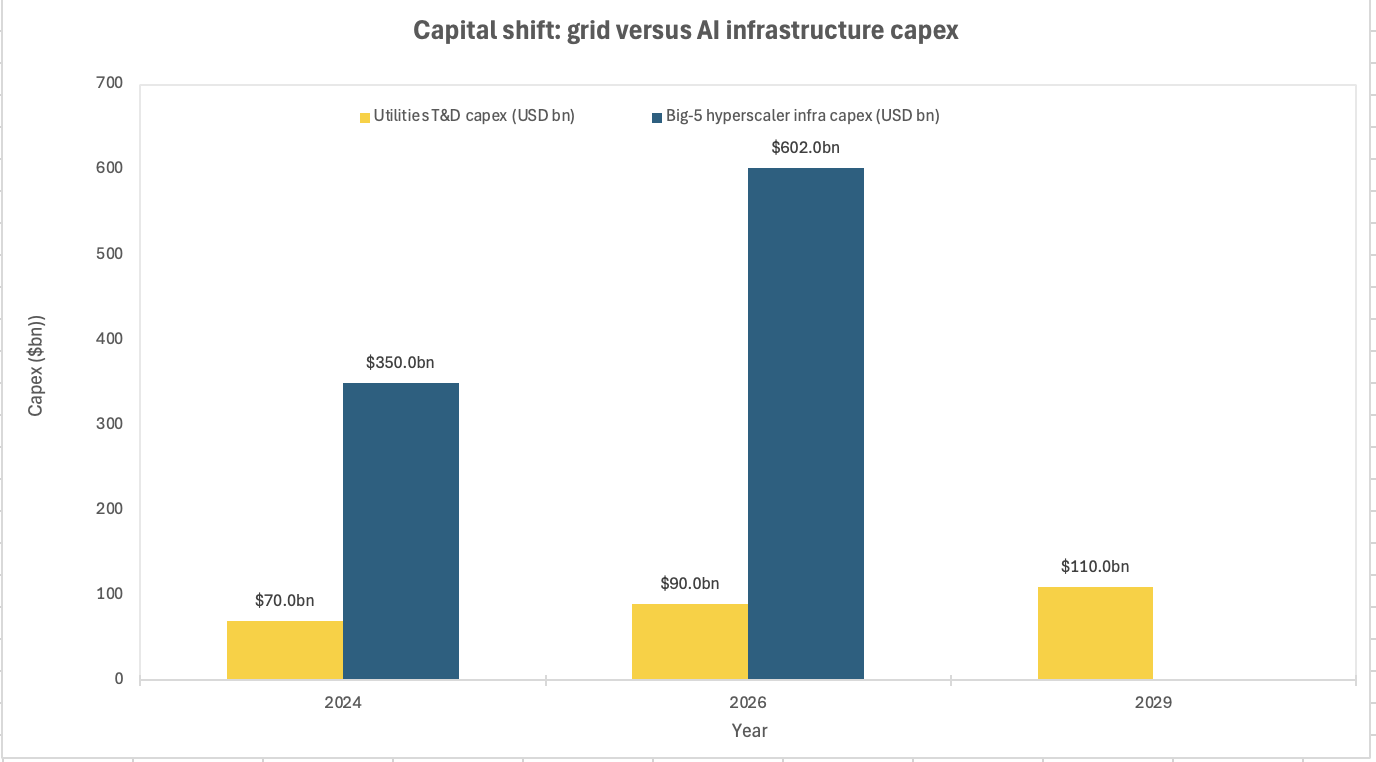

The five largest hyperscalers—Amazon, Microsoft, Alphabet (Google), Meta, and Oracle—are projected to spend approximately $602 billion on infrastructure in 2026, a 36% increase year-over-year. Roughly 75% of this total, or $450 billion, is earmarked for AI-specific infrastructure including GPUs, data centre construction, networking equipment, and—increasingly—power supply and generation assets. To finance this buildout, these companies raised $108 billion in debt during 2025 alone, more than three times the historical annual average, and analysts project that the technology sector may need to issue $1.5 trillion in new debt over the coming years to sustain AI infrastructure expansion.

This represents a historic shift in capital intensity. Amazon's capital expenditures now constitute approximately 57% of revenue; Meta's reach 52%; Microsoft's 48%; and Google's 45%—ratios that exceed the 15% to 25% range typical for technology companies and approach levels seen in utilities and heavy industry. For context, the aggregate 2026 capex of these five companies exceeds the entire annual capital spending of the U.S. oil and gas sector in 2023.

Yet the composition of this spending is shifting in ways that most equity research has yet to fully capture. Goldman Sachs estimates that of the $450 billion directed toward AI infrastructure, approximately $180 billion will go to GPUs and accelerators (purchasing roughly 6 million units at an average price of $30,000), $120 billion to data centre construction, $50 billion to networking, and the remainder to power systems, cooling, land acquisition, and transmission infrastructure. This $120 billion in construction spending translates to approximately 15 to 20 GW of new data centre capacity—but only if power can be secured and interconnected on schedule.

Increasingly, it cannot.

Vertical Integration: Hyperscalers Become Power Developers

Faced with interconnection queues that stretch beyond their planning horizons, hyperscalers are vertically integrating into power generation and transmission at a pace unseen in the technology sector. In December 2025, Alphabet announced the acquisition of Intersect Power, a developer of co-located data centre and energy infrastructure, for $4.75 billion in cash plus assumption of debt. The deal includes 3.6 GW of solar and wind capacity under development, 3.1 GWh of battery storage, and a development team with a track record of delivering $15 billion in infrastructure projects. Google's total pipeline of co-located renewable and clean backup projects now exceeds $20 billion, with locked-in access to over 10 GW of generation capacity through 2028.

Microsoft committed $10 billion to a renewable energy partnership with Brookfield Asset Management, deploying 10.5 GW of capacity between 2026 and 2030. In a more dramatic pivot, Microsoft signed a $16 billion, 20-year power purchase agreement with Constellation Energy to restart Unit 1 of the Three Mile Island nuclear plant in Pennsylvania, delivering 835 MW of carbon-free baseload power starting in 2028. This marks the first time a major technology company has financed the restart of a retired nuclear reactor specifically to power data centres.

Amazon's strategy has been similarly aggressive. The company invested over $20 billion to convert the Susquehanna nuclear site in Pennsylvania into a dedicated AI data centre campus, and in June 2025 signed a PPA with Talen Energy to purchase 1.9 GW through 2042. Amazon is also backing small modular reactor (SMR) development through investments in X-energy and partnerships with Energy Northwest, committing to purchase power from up to 12 Xe-100 reactors (delivering 320 to 960 MW) at the Cascade Advanced Energy Facility in Washington state, with commercial operation targeted for the early 2030s.

Meta has issued a request for proposals targeting 1 to 4 GW of new nuclear generation and announced agreements with Vistar, TerraPower, and Oklo to power its Prometheus supercluster in New Albany, Ohio—a facility requiring over 1 GW of power when construction completes in 2026, making it the world's first single data centre campus exceeding that threshold. Meta's planned 5 GW Hyperion facility in Louisiana, scheduled for 2028, will include three on-site natural gas plants costing $3 billion.

These are not pilot projects; they are multi-billion-dollar commitments to secure generation capacity that would otherwise require five to eight years of interconnection study, permitting, and construction—timelines incompatible with AI deployment schedules. By owning or directly contracting for generation, hyperscalers bypass grid interconnection queues, lock out competitors from accessing scarce resources, and capture the full economic rent of firm power in constrained markets.

The Utility and Independent Power Producer Playbook: Who Wins the Power Race

Regulated Utilities: Redefining the Customer Relationship

Vertically integrated utilities with generation, transmission, distribution, and customer load in data-centre-intensive regions are emerging as the primary beneficiaries of AI-driven electricity demand growth. These companies possess structural advantages that independent data centre developers cannot replicate long-term planning mandates, investment-grade credit ratings enabling low-cost debt financing, cost-of-service regulatory models that allow capital expenditure recovery through rate base, and decades of operational expertise in managing gigawatt-scale generation and transmission assets.

Duke Energy has signed agreements to connect 2 GW of new data centre capacity across its service territories in the Carolinas, Florida, Ohio, Kentucky, and Indiana, with additional load expected to materialize in 2027 and 2028. The company raised its five-year capital plan to $100 billion, up from $87 billion, and will add 13 GW of new generation over five years to support this growth. Duke's chief financial officer emphasized that data centre operators are particularly attracted to the company's carbon-free nuclear generation, positioning Duke favourably for customers with sustainability mandates.

Dominion Energy, the bellwether for the data centre market given its dominance in Northern Virginia—the world's largest data centre hub—reported 47.1 GW of data centre contracted capacity as of Q3 2025, with 9.8 GW already in binding take-or-pay electric service agreements and another 9 GW in construction letters of authorization that require customers to reimburse Dominion for all spent costs if they withdraw. Dominion's contracted load has more than doubled since mid-2024, when it stood at approximately 21 GW, underscoring the acceleration in hyperscale commitments.

American Electric Power brought 2 GW of data centre load online in Q3 2025 and has signed contracts for 28 GW of large load by 2030, of which 22 GW is for data centres. AEP's interconnection queue contains 190 GW of active projects, and the company's forecasted system peak is projected to reach 65 GW by 2030—nearly double its current 37 GW peak. To support this growth, AEP raised its five-year capital plan from $54 billion to $72 billion, a 33% increase driven almost entirely by transmission expansion and generation additions tied to data centre load.

Southern Company is benefiting from a combination of data centre and manufacturing reshoring, reporting 8 GW of large load contracts and a pipeline exceeding 50 GW, supporting an 8% annual sales growth forecast through 2029. Seven gigawatts representing 23 projects have already broken ground across Southern's territories, and Georgia Power recently filed an updated load forecast requesting 10 GW of new capacity resources, including five natural gas combined-cycle units and 11 battery energy storage facilities.

These utilities are not merely responding to demand; they are actively shaping the market through regulatory innovation. Duke, Dominion, and AEP have introduced or are piloting "data centre tariffs" with take-or-pay provisions, minimum demand charges (typically 85% of contracted capacity), and cost-allocation mechanisms that assign network upgrade costs directly to the data centre customer rather than socializing them across the broader ratepayer base. This ensures that the marginal cost of serving hyperscale load does not drive residential and commercial electricity prices upward—a critical political and regulatory constraint in states where data centre growth has sparked public backlash over rising bills.

Independent Power Producers: Capturing the Nuclear and Gas Premium

Independent power producers (IPPs) with existing generation fleets are extracting significant premiums by offering what data centres need most: firm, carbon-free or low-carbon power available within 24 to 36 months, rather than the five-to-eight-year timelines typical for new-build interconnection.

Vistar, the largest competitive generator in the United States, has become the most aggressive acquirer of dispatchable generation to serve data centre demand. In January 2026, Vistar agreed to purchase 10 natural gas-fired power plants with a combined capacity of 5.5 GW in the U.S. Northeast and Texas for approximately $4 billion, or $730 per kilowatt—roughly one-third the cost of building new gas capacity, which now exceeds $2,200 per kilowatt due to supply chain constraints and extended turbine lead times. This follows Vistra's May 2025 acquisition of a natural gas fleet from Infrastructure Partners for $2 billion, adding capacity in PJM, New England, New York, and California.

Vistra's CEO emphasized that "natural gas-fired generation will play an increasingly vital role in ensuring the reliability, affordability, and flexibility of U.S. power grids as energy demand rises," and the company is in active discussions with multiple hyperscalers regarding long-term contracts at its Comanche Peak nuclear facility in Texas, which is licensed to operate until 2053. Vistra executives indicated they have already signed contracts with Amazon and Microsoft totalling over $700 million in capital commitments for 2025 generation and capacity expansion.

Constellation Energy, the largest owner of U.S. nuclear generation, signed a 20-year PPA with Meta to support relicensing and ongoing operations of the Clinton nuclear facility in Illinois starting in June 2027. Constellation's restart agreement with Microsoft for the 835 MW Crane Clean Energy Centre (Three Mile Island Unit 1) is valued at $16 billion over the contract life and represents the first commercial reactivation of a retired nuclear reactor in U.S. history.

NextEra Energy announced a 25-year PPA with Google to restart the 615 MW Duane Arnold nuclear plant in Iowa by early 2029, with additional exploration of advanced nuclear generation deployment across the U.S. NextEra added 3 GW of new renewables and storage to its backlog in Q3 2025, bringing total contracted capacity to 29.6 GW, much of it tied to corporate PPAs with hyperscalers seeking to match data centre load with carbon-free generation.

NRG Energy, following its 2025 acquisition of LS Power's generation fleet, now operates approximately 25 GW of capacity heavily weighted toward flexible, quick-start natural gas plants critical for stabilizing grids with high renewable penetration. NRG has secured $562 million from the Texas Energy Fund—a state-backed program providing low-interest loans for new dispatchable generation—to build the Cedar Bayou facility, and the company is aggressively pursuing co-location agreements where it provides dedicated power directly to AI data centres at premium rates.

The valuation impact has been dramatic. Vistra's stock rose over 40% in 2025, driven primarily by surging data centre demand and successful financing of new gas-fired generation in Texas. Constellation Energy shares hit all-time highs in Q4 2024 and continued gains into 2025 on the strength of its Microsoft and Meta deals. NRG posted a five-year total return exceeding 315%, vastly outperforming the S&P 500 and the utilities sector, as the company successfully transitioned from a volatile, debt-laden independent power producer to a growth-oriented "energy-tech" company commanding higher multiples.

The Economics of Scarcity: How Power Constraints Are Repricing the Stack

From $/kW to Controlled Disorder

The shift from abundant, cheap grid power to scarce, expensive, and time-constrained capacity is fundamentally repricing data centre economics. Global data centre colocation pricing rose 3.3% year-over-year in Q1 2025 to an average of $217.30 per kilowatt (kW) per month on a weighted inventory basis—a relatively modest increase compared to prior years, but one that masks dramatic regional divergence driven by power availability.

Northern Virginia, the world's largest data centre market, saw asking rents increase 17.6% year-over-year, while Chicago rose 17.2% and Amsterdam climbed 18%. These markets share a common characteristic: they are power-constrained, with years-long waiting lists for new interconnections and limited availability of substations capable of supporting multi-megawatt loads. Phoenix, by contrast, saw stable pricing year-over-year at $190 per kW per month following rapid gains in prior periods, reflecting the completion of several large-scale wholesale facilities that temporarily increased supply.

Wholesale colocation lease rates in Tier-1 U.S. markets now range from $120 to $150 per kW per month for large deployments (hundreds of kilowatts to multi-megawatt suites), while retail colocation—where customers lease individual cabinets or cages—commands $150 to $250 per kW per month depending on redundancy levels and interconnection density. However, these headline figures obscure the growing premium for "powered" versus "unpowered" space. Operators with firm, multi-year power commitments in constrained markets are commanding premiums of 20% to 40% above comparable facilities that lack guaranteed power or that face imminent interconnection delays.

Investment underwriting has shifted accordingly. Where data centre valuations historically centred on square footage, construction quality, and tenant diversification, investors now underwrite megawatts first and real estate second. Pricing is increasingly normalized on a dollars-per-kilowatt-per-month basis, and the primary value driver is not the building itself but the power purchase agreement, interconnection service agreement, or utility tariff that guarantees electrons will flow.

This repricing is visible in M&A valuations. In October 2025, a consortium comprising the AI Infrastructure Partnership (whose members include Microsoft, Nvidia, and BlackRock), MGX, and Global Infrastructure Partners acquired Aligned Data Centres for $40 billion—more than double the previous record of $16.1 billion paid for AirTrunk the year prior. Aligned's valuation was driven not by its existing facilities, but by its 5 GW pipeline of active and planned capacity with secured interconnection agreements across Illinois, Texas, Utah, Arizona, Northern Virginia, Maryland, and Ohio. CoreWeave, a GPU-cloud provider that owns both compute hardware and data centre infrastructure, went public in January 2026 at a $23 billion valuation, down from a summer 2025 peak around $70 billion, as investors re-evaluated the company's ability to bring contracted capacity online given power supply and interconnection delays.

The Ratepayer Dilemma: Who Pays for AI's Grid?

A politically sensitive dimension of AI's power demand is the question of cost allocation: to what extent will residential and small commercial customers subsidize the transmission and distribution upgrades required to serve hyperscale data centres? Several mechanisms allow data centre costs to "creep" into broader rate bases, even when utilities and regulators publicly commit to preventing cross-subsidization.

First, when a data centre triggers the need for a new substation, transmission line upgrade, or generator interconnection, the costs are often allocated across all customers in a regional transmission organization through FERC-regulated cost-sharing formulas. In PJM, for example, half the cost of new transmission lines is allocated regionally across all member utilities, meaning that a substation built to serve a data centre in Virginia can result in rate increases for customers in Ohio or Pennsylvania. Utilities can mitigate this by requiring the data centre to pay for upgrades upfront or through a dedicated tariff, but regulatory approval for such mechanisms varies widely by state and can take years to implement.

Second, capacity market prices—which ensure that sufficient generation is available to meet peak demand—have risen sharply in regions with high data centre concentration. PJM's capacity market price increased from approximately $30 per megawatt-day in 2023 to $270 per megawatt-day in the 2025/2026 auction and currently sits at roughly $330 per megawatt-day for the 2027/2028 delivery year. These costs are passed through to all customers, and analysts estimate that data centre load growth contributed approximately $9.3 billion to PJM's 2025–2026 capacity price increase—equivalent to roughly $16 to $18 per month in higher bills for residential customers in Ohio and western Maryland.

Third, if a data centre receives favourable contract terms—such as discounted energy rates, exemptions from certain transmission charges, or tax incentives—other customers must absorb a greater share of grid cost recovery. Harvard Law School's Environmental and Energy Law Program analysed several utility filings and found instances where special contracts allowed data centres to reduce their bills at the expense of ratepayers, particularly when the data centre was granted a rate structure that did not fully capture the marginal cost to serve its load.

To address these concerns, several utilities and state regulators have introduced "clean transition tariffs" or "data centre tariffs" that require large customers to pay for dedicated infrastructure, sign long-term take-or-pay contracts (often 10 to 15 years), and maintain minimum demand levels (typically 85% of contracted capacity) to ensure they cannot withdraw after the utility has made sunk investments. These tariffs shift the risk of stranded costs onto the data centre operator, but they also increase the upfront capital and contractual commitment required to secure a site—a barrier that favours hyperscalers with strong balance sheets over smaller developers or enterprises.

The Portfolio Construction Implication: Differentiating Compute Stories

The Winners: Power-Secured and Vertically Integrated Operators

The investment thesis for AI infrastructure must now explicitly incorporate power supply and interconnection status as primary valuation drivers. Companies and assets that own, control, or have long-term contractual access to scarce power and grid capacity will capture expanding margins and command valuation premiums as competitors bid up the cost of remaining supply. The following categories warrant overweight positioning:

Vertically integrated utilities with generation and T&D in data-centre-intensive regions. Duke Energy, Dominion Energy, American Electric Power, and Southern Company possess regulated monopolies over transmission, own baseload nuclear and gas generation, and can recover capital expenditures through rate base mechanisms. These utilities are experiencing 5% to 8% annual load growth—the highest in decades—and are expanding capital programs by 30% to 50% to meet demand. They face limited competitive threats, offer stable dividend yields, and provide a hedge against both AI infrastructure growth and energy inflation.

Independent power producers with existing dispatchable generation fleets. Vistra, Constellation Energy, NRG Energy, and NextEra Energy are securing multi-decade PPAs at premium pricing by offering immediate or near-term power from existing nuclear and gas plants, bypassing interconnection queues entirely. These companies are trading at energy-multiples rather than utility-multiples, reflecting their ability to capture scarcity rents in tight capacity markets. Vistra's aggressive acquisition strategy—buying existing gas capacity at 30% to 40% of replacement cost—provides a structural cost advantage that will compound as new-build economics deteriorate further due to equipment lead times and financing costs.

Data centre operators and REITs with multi-year power commitments in supply-constrained markets. Aligned Data Centers (now private), Equinix, and Digital Realty have differentiated themselves by securing power years in advance of facility construction, locking in capacity that competitors cannot access. Equinix, with revenues rising from $4.59 billion in 2020 to an estimated $6.52 billion in 2024, benefits from its highly interconnected platform and customer base exceeding 10,000 enterprises, allowing it to command retail colocation premiums. Digital Realty's PlatformDIGITAL ecosystem and focus on hyperscale-ready wholesale capacity position it to capture the shift toward megawatt-scale leases. However, the sector is bifurcating: operators without secured power in Tier-1 markets face occupancy risk and margin compression as tenants prioritize energizable sites over location alone.

Transmission, substation, and power distribution equipment suppliers. The $436 billion five-year U.S. utility T&D pipeline and similar investments globally create sustained demand for transformers, circuit breakers, high-voltage cables, and substation automation systems. This category has received less attention than semiconductors or data centre REITs but represents critical infrastructure with multi-year lead times and limited manufacturing capacity. Companies exposed to this segment—such as Eaton, Siemens, ABB, and Schneider Electric—face favourable supply-demand dynamics and pricing power as utilities compete to secure equipment for grid expansion projects.

Midstream natural gas infrastructure with exposure to data-centre-intensive regions. Natural gas is emerging as the dominant bridge fuel for data centres that cannot wait for renewable or nuclear capacity. East Daley Analytics projects that AI-driven data centre demand could add 4 to 6 billion cubic feet per day (Bcf/d) of incremental U.S. gas demand by 2030, with behind-the-meter projects requiring dedicated gas pipelines and on-site generation adding an additional 2.1 Bcf/d. Energy Transfer, Williams Companies, and Kinder Morgan operate extensive pipeline networks in Texas, the Mid-Atlantic, and the Southeast—regions where the majority of hyperscale data centre development is concentrated—and are investing heavily in laterals, storage, and compression capacity to serve this load. These midstream operators offer 6% to 8% distribution yields backed by fee-based, take-or-pay contracts, providing both income and exposure to structural gas demand growth.

The Losers: Implicit Cheap-Power Assumptions

Conversely, several categories face material downside risk as the power constraint binds and reprices expectations:

Pure-play GPU and semiconductor stories that assume infinite grid capacity. NVIDIA maintains approximately 90% market share in AI accelerators and posted extraordinary revenue growth through 2024 and 2025, but the company's forward multiples embed an assumption that every GPU sold can be deployed and energized. As data centres report having chips "sitting in inventory awaiting facilities" due to the "warm shell" shortage—operational data centres with available power connections—GPU utilization rates will decline, extending payback periods and reducing the economic justification for incremental chip orders. AMD, which saw its stock rise 77% in 2025 versus NVIDIA's 39% on the strength of its MI300 and MI350 accelerator wins, faces the same constraint: even cost-effective, energy-efficient chips cannot generate revenue if they cannot be plugged in.

Data centre developers without secured power or interconnection agreements in Tier-1 markets. Generic colocation providers entering saturated markets like Northern Virginia, Silicon Valley, or Frankfurt without multi-year power commitments will face extended lease-up periods, lower occupancy, and compressed yields as tenants prioritize powered sites. The bifurcation between "haves" (operators with firm power) and "have-nots" (operators in interconnection queues) will widen, with the latter forced to discount rents or accept unfavourable tenant terms to compete.

Hyperscalers slow to verticalize power supply or overly reliant on utility interconnection in congested regions. Companies that have not secured dedicated generation, signed long-term PPAs, or established co-location partnerships will face schedule delays, rising interconnection costs, and reputational risk if they cannot deliver promised AI compute capacity on the timelines communicated to investors and customers. The market has not yet penalized hyperscalers for power-driven delays—Q1 2026 earnings will be the first major test of whether capex is translating into energized, revenue-generating capacity or accumulating as work-in-progress inventory awaiting grid connections.

Late-mover data centre developers entering markets with multi-year interconnection queues. In CAISO, PJM, and parts of MISO and ERCOT, new entrants without existing queue positions or utility relationships face five-to-eight-year timelines even for greenfield sites, by which time technology cycles will have rendered initial design assumptions obsolete and financing costs will have compounded. This creates a first-mover advantage for incumbent operators and utilities that is nearly impossible for new entrants to overcome without paying for dedicated transmission infrastructure—a capital outlay that destroys returns for all but the largest hyperscalers.

The Three-Month Catalyst Window: What to Watch

Q1 2026 Hyperscaler Earnings: Reading the Capex Tea Leaves

The most critical near-term catalyst is the composition disclosure in Q1 2026 hyperscaler earnings, expected between late April and mid-May 2026. Investors should scrutinize management commentary and supplemental disclosures for signals that capital expenditure is shifting from GPUs and servers into "technical infrastructure," land acquisition, power supply agreements, and grid interconnection costs. Key questions include:

What percentage of 2026 capex is allocated to compute hardware (GPUs, networking) versus infrastructure (power, cooling, substations)?

How many gigawatts of new capacity are "under construction" versus "energized and operational"?

What is the average timeline from capex commitment to revenue-generating capacity, and has this timeline extended?

Are any facilities experiencing delays due to power supply or interconnection issues?

Microsoft, Amazon, and Google have historically provided the most granular capex breakdowns, but even these disclosures often aggregate "technical infrastructure" in ways that obscure the power-versus-compute split. Analyst questions on earnings calls will be critical for eliciting useful detail, and any acknowledgment of "power-driven schedule adjustments" or "longer-than-expected interconnection timelines" will trigger material re-ratings of both hyperscaler equities and their downstream suppliers.

PJM and Regional ISO Compliance Filings

FERC's December 2025 order directed PJM to file revised interconnection procedures by January 20, 2026, and to implement three new transmission service options by February 17, 2026. PJM must also submit a detailed informational report on its Critical Issue Fast Path (CIFP) stakeholder process for large load additions, including the status of proposed expedited interconnection processes and enhanced load forecasting.

These filings will reveal the specific rates, terms, and conditions that data centres must meet to co-locate with generation, the cost-allocation mechanisms for reliability upgrades, and the queue priority rules that will determine which projects advance and which remain stuck in study. Utilities, data centre developers, and generation owners will submit comments and protests, providing a real-time view of commercial positioning and lobbying strategies. A stringent tariff that assigns full upgrade costs to the data centre will increase the effective cost of co-location and Favor vertically integrated utilities that can internalize these costs through rate base recovery. A lenient tariff that socializes costs will trigger political backlash and potential state-level intervention, creating regulatory uncertainty that delays projects.

Utility Q4 2025 and Q1 2026 Earnings Guidance

Between January and March 2026, major utilities will report Q4 2025 results and provide updated 2026 guidance, including revisions to long-term load forecasts, capital expenditure plans, and data centre interconnection pipelines. Duke, Dominion, AEP, Southern, Entergy, NextEra, and Xcel have all flagged material upward revisions to data centre load in recent quarters, and Q1 2026 will reveal whether these forecasts continue to accelerate or begin to plateau as power constraints bind.

Key metrics to track include:

Contracted data centre capacity (in megawatts and revenue)

The number and total capacity of projects in the "late-stage negotiation" or "construction letter of authorization" phase

The timeline from contract signing to energization (which will reveal whether interconnection delays are worsening)

The percentage of capital expenditure allocated to transmission and distribution versus generation

Regulatory approvals received or pending for data centre tariffs and cost-allocation mechanisms

Utilities that report accelerating contracted load but lengthening timelines to energization will signal that power supply—not customer demand—is the binding constraint, validating the thesis that scarcity rents are accruing to power owners rather than compute operators.

Federal and State Interconnection Reform Announcements

Beyond PJM, several other ISOs and state regulators are considering interconnection reforms in response to data centre load growth. MISO, CAISO, and ERCOT have all initiated stakeholder processes to streamline large-load interconnection, but none have yet implemented binding reforms comparable to FERC's PJM order. Any announcements of expedited review processes, dedicated large-load queues, or cost-allocation rule changes will materially impact regional site selection decisions and data centre valuations.

At the state level, governors and public utility commissions in Virginia, Texas, Georgia, Ohio, and North Carolina—the five states with the highest data centre concentration—are under political pressure to prevent residential rate increases driven by data centre demand. State actions could range from requiring data centres to fully fund transmission upgrades (favourable for ratepayers, negative for data centre economics) to offering tax incentives and streamlined permitting (favourable for developers, potentially negative for utilities if cost recovery is constrained). The divergence in state policies will create "regulatory arbitrage" opportunities, with data centre developers gravitating toward states that offer the most favourable combination of power availability, interconnection speed, and cost allocation.

Conclusion: The End of the Free-Electron Era

The AI infrastructure buildout is colliding with the physical reality of a power grid designed for steady, predictable load growth, not the exponential, geographically concentrated demand of gigawatt-scale data centres. Interconnection queues that stretch beyond five years, capacity auctions where data centres account for 40% of costs, and utilities raising capital expenditure plans by 30% to 50% are not transient bottlenecks—they are the new equilibrium.

For investors, this transition marks the end of an era where AI could be modelled as a pure software and silicon story. The marginal dollar of value creation is shifting from chip designers and cloud platforms to the entities that control access to scarce, firm electrons: vertically integrated utilities with nuclear and gas generation, independent power producers with existing fleets, and data centre operators that secured power years before competitors recognized the constraint.

The next three months will reveal which hyperscalers have successfully internalized this reality and which remain implicitly dependent on interconnection timelines and utility cooperation that cannot be secured at any price in saturated markets. CIOs should abandon blanket AI overweight and reconstruct portfolios around a binary question: does this asset own, control, or have long-term contractual access to gigawatt-scale power that can be energized within 36 months? Those that answer yes will compound; those that answer no will face schedule risk, rising costs, and margin compression as they compete for the last electrons available.

The 175 GW wall is not a metaphor. It is the sum of transmission constraints, regulatory friction, and the physical inertia of a grid that cannot scale at GPU speed. Capital markets have not yet priced this constraint. They will.

References

Goldman Sachs Research – “AI to drive 165% increase in data center power demand by 2030” (2025).

S&P Global Commodity Insights / 451 Research – “Data center grid-power demand to rise 22% in 2025, nearly triple by 2030” (2025).

JLL – “2026 Global Data Center Outlook” (2026).

U.S. EIA – “Record US data center power use amid AI and crypto boom” (2025).

Deloitte – “Can US infrastructure keep up with the AI economy?” (2025).

PJM Interconnection – “PJM Auction Procures 134,479 MW of Generation Resources” and associated news releases on 2027/2028 auction (2025–2026).

Utility Dive – “Data centers were 40% of PJM capacity costs in last auction” (2026).

University of Chicago / Energy Policy Institute – “How the Interconnection Queue Backlog Is Slowing Energy Growth” (2025).

Enverus – “2025 Interconnection Queue Outlook” (2025).

FERC – Orders on PJM tariff reforms and co-location (Dec 2025–Jan 2026).

K&L Gates – “FERC Orders PJM to Reform Tariff for Co-Located Generation and Load” (2026).

SPP / FERC – “High Impact Large Load Generation Interconnection Agreement (HILLGA)” filings and commentary (2026).

Latham & Watkins – “US Data Center Demand: White House and Governors Issue Principles while PJM Issues Decisional Letters” (2026).

Introl – “FERC’s Data Center Colocation Ruling: Complete Guide” (2026).

CBRE – “Global Data Center Trends 2025” (2025).

Cushman & Wakefield – “Data Center Spotlight: Power and Lease Pricing Outlook” (2025).

Harvard Environmental & Energy Law Program – “Extracting Profits from the Public: How Utility Ratepayers Fund Investor-Owned Utility Profits” (2025).

E3 / Lawrence Berkeley National Laboratory – “Electricity Rate Designs for Large Loads: Evolving Practices” (2025).

S&P Global Ratings – “Data Centers: Are The Winning Odds Less Certain in 2026?” (2025).

Bloomberg / Investopedia – coverage of Vistra, Constellation and NRG equity performance and AI-linked deals (2024–2026).

East Daley Analytics – “Data Centers Could Add 6 Bcf/d to Gas Demand” (2025).

Woodway Energy – “Natural Gas and the Rise of Data Center Power Demand” (2025).

Introl – “Nuclear power for AI: inside the data center energy deals” and “SMR Nuclear for Data Centers Accelerates” (2025–2026).

BNEF – “AI and the Power Grid: Where the Rubber Meets the Road” (2025).

Morgan Stanley – “AI Might Not Fry The Grid” (2025).