After the Land Grab: Why the Next Decade of Southeast Asian Returns Lives Inside the Machine Room

The arbitrage that made Southeast Asia's digital decade has closed. The next one is hidden inside the operations of the companies that won.

For a decade, capital flooded Southeast Asia on a single thesis: gain market entry, ride demographic tailwinds and penetration curves, and exit at scale to a strategic buyer or public market. That thesis produced real returns, and then it produced real crowding.

The region's mid-market incumbents — the distributors, financial intermediaries, manufacturers, and healthcare operators — are now the asset. Their constraint is not market position.

It is the system running the business.

Why This Matters

Legacy systems consume 40% of enterprise IT budgets globally in 2025, silently compressing margins at precisely the moment when operational efficiency determines exit multiples in SEA mid-market portfolios

The ASEAN Digital Economy Framework Agreement (DEFA), expected to be formally signed in 2026, will impose cross-border interoperability standards that legacy-locked, single-jurisdiction systems cannot cost-effectively meet

Family offices and institutional LPs still committing to market-entry vintage fund strategies in SEA are allocating to last decade's thesis at this decade's multiples

The Exhausted Land Grab

Consumer internet alpha in Southeast Asia is structurally spent. Smartphone penetration across the six major economies now exceeds 80%, and the dominant verticals — e-commerce, ride-hailing, digital payments, food delivery — have consolidated around two or three scaled incumbents per market. The incremental user is already acquired. The case for funding another digital lending platform or a fourth last-mile logistics operator is not a market-entry argument; it is a market-share argument, which is a fundamentally different and more expensive proposition.

What remains is a large, undermanaged cohort of mid-market businesses: family-owned distributors, regional manufacturers, multi-country financial services firms, healthcare operators with dozens of sites across Thailand, Vietnam, and Indonesia. These businesses carry real cash flows, genuine market positions, and compressible cost structures. Their shared constraint is not access to capital or customers. It is the operational system running the enterprise: on-premises ERP platforms designed for single-market operation, payroll architectures that cannot integrate with modern HR tools, and financial reporting systems requiring five days and twelve spreadsheets to produce a monthly close.

Private equity (PE) deal value in SEA moderated to US$9.1 billion across 59 transactions in 2025, with the market explicitly transitioning to what EY describes as "value creation-led PE, with sponsors prioritising operational improvement, downside protection and exit readiness". Mid-market deals accounted for 45% of regional values in the first half of 2025, up from 32% in the second half of 2024. The composition of capital is shifting. The question for LPs is whether the managers they back have built the infrastructure to capture it.

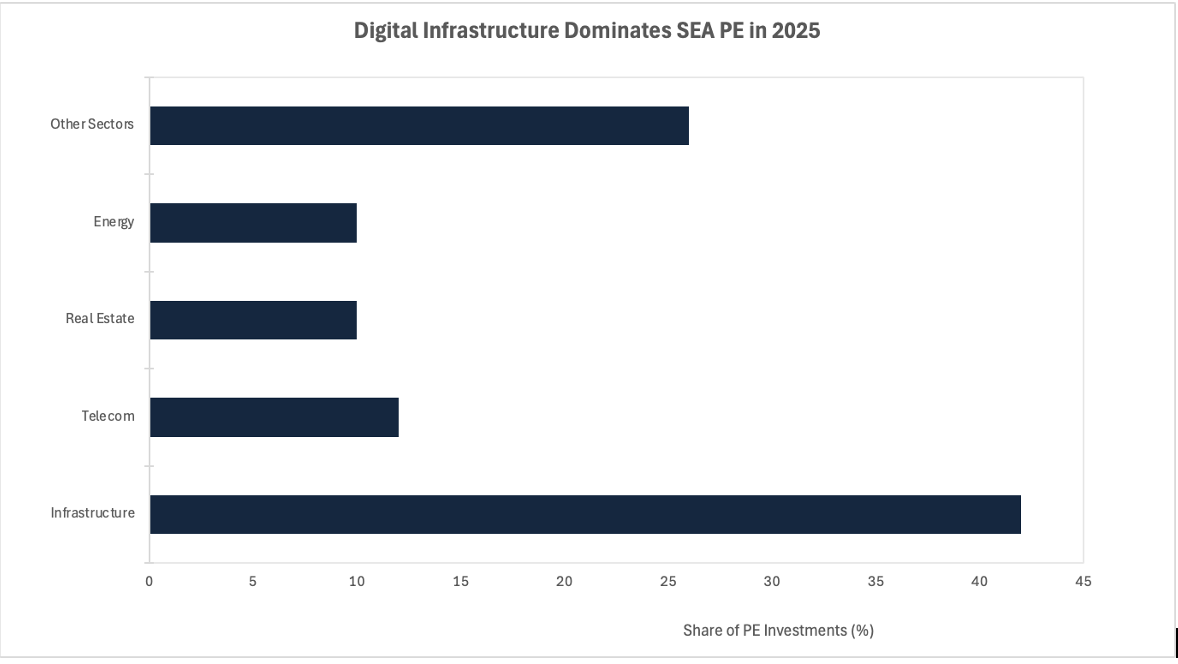

Source: EY SEA PE Pulse 2025. Digital infrastructure accounts for 42% of total PE deployment, signalling a structural reorientation away from consumer internet and towards the operational backbone of the region's economy.

The Hidden Liability

The most important thing to understand about legacy systems in the SEA mid-market is that they are not simply inefficient. They are a structural liability that rarely surfaces in a standard due diligence data room.

McKinsey research cited in 2025 estimates that enterprises globally spend 40% of their IT budgets maintaining legacy systems: not upgrading, not innovating, but keeping existing infrastructure operational. In Asia Pacific, the insurance sector alone carries an estimated US$200 billion in technical and process debt, of which US$134 billion is directly tied to legacy systems. These are sector-specific figures, but the underlying dynamic — operational infrastructure consuming capital that should drive EBITDA improvement — is endemic across mid-market companies throughout the region.

The mechanism through which this suppresses value is threefold.

It caps margin: every dollar spent on legacy maintenance is not spent on AI integration, automated underwriting, or predictive inventory management.

It extends the information cycle: in a multi-country business, systems that cannot consolidate data across jurisdictions slow capital allocation decisions and create asymmetries that disadvantage management in negotiations with suppliers and lenders.

It blocks exit: a mid-market business running on 2009 on-premise infrastructure cannot credibly present to a strategic acquirer in 2026 or 2027 as a scalable platform without a multi-year, high-cost technology programme built into the acquisition price.

Where the LP risk most is mis-located. Most fund-level due diligence assesses portfolio company technology risk as an IT line item, not as an exit impediment. When an acquirer's integration team discounts the target because its system stack is incompatible, the general partner (GP) absorbs the markdown and attributes it to market conditions. It was an underwriting failure.

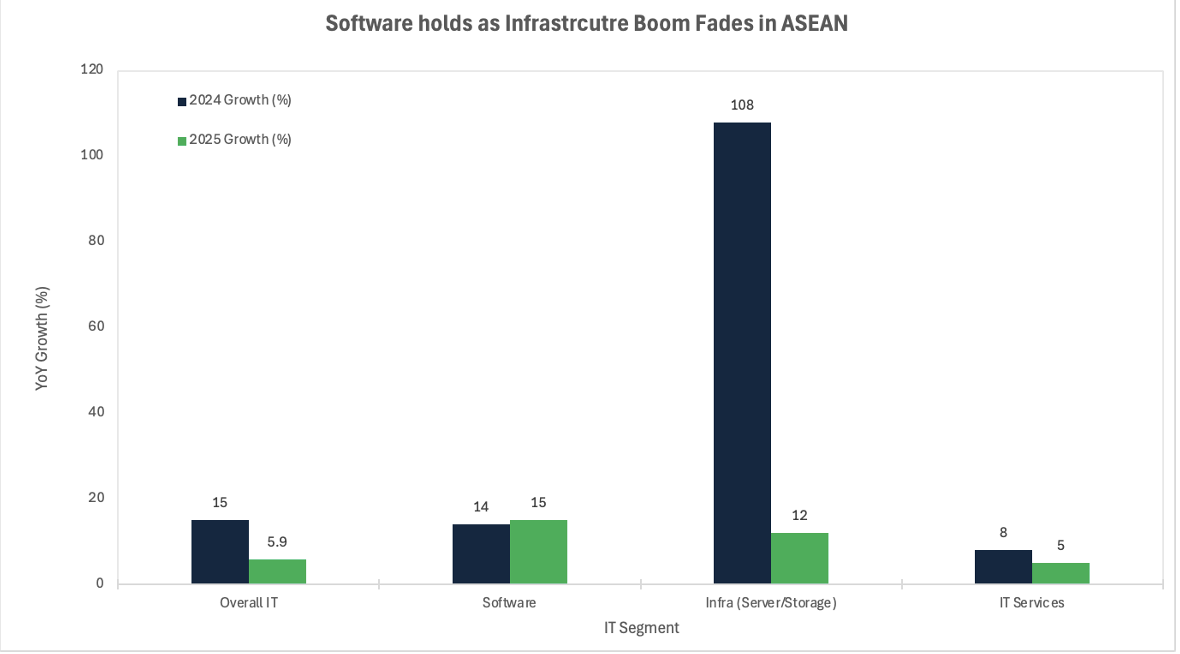

Source: IDC Worldwide Black Book 2025. Software is the only segment sustaining mid-teens growth as the infrastructure surge normalises, reflecting durable demand for cloud migration and AI-enabled modernisation platforms.

What LPs Should Be Asking

For family offices and institutional LPs, the implication is not that legacy-system replacement is a new sector to allocate to. It is that operational transformation capability is a new evaluative dimension to apply to every SEA-focused fund manager they consider.

The GP population in the region splits into three archetypes. The first is the financial-engineering fund: buys at a discount, applies leverage, waits for multiple expansion. This model had a decade-long run and is now under structural pressure as multiples normalise and exit markets remain selective. The second is the sector-specialist fund with genuine operational infrastructure: teams that can deploy technology programme managers into portfolio companies, execute cloud ERP migrations without disrupting revenue, and integrate AI-enabled finance and supply chain tools within a 24-month hold window. The third is the B2B technology growth equity fund, deploying into vertical software-as-a-service (SaaS) platforms, managed-service providers, and ERP vendors that are themselves the solution mid-market incumbents are buying.

LPs should be asking, at the point of commitment: what is the GP's post-close operational playbook for a typical mid-market buyout? How many technology transformation programmes has the team executed, and what is the average cost and timeline overrun? How is the exit case underwritten if the transformation is incomplete at the end of the hold period? Few GP marketing materials answer these questions, because most are still written for the market-entry era.

Catalysts and the Decision Window

Three structural forces are compressing the modernisation timeline from optional to obligatory.

DEFA: ASEAN's Digital Economy Framework Agreement substantially concluded negotiations in late 2025 and is expected to be formally signed in 2026. Once in force, it introduces cross-border data flow standards, digital trade interoperability requirements, and cybersecurity baseline obligations across all ten ASEAN member states. Companies operating on legacy, single-jurisdiction systems face material compliance costs as these standards embed. Those already on cloud-native, Application Programming Interface (API)-first architectures face none.

Generative artificial intelligence (GenAI): By 2026, IDC projects that 60% of Asia Pacific organisations will build applications using open-source AI models. These models require clean, accessible data pipelines. Legacy systems are, in the direct framing of technology analysts, "data prisons": they fragment data across siloed formats that AI tools cannot ingest. The competitive gap between a mid-market business with a modernised data architecture and one without will not take a decade to manifest in EBITDA margins. Based on current adoption trajectories, it will be visible within two to three years.

Private credit: ASEAN software spending is projected to grow at mid-teens in 2025 even as overall IT growth decelerates to 5.9%, reflecting a normalisation of the 2024 infrastructure surge. For LPs with a private credit mandate, the operational transformation of mid-market companies is generating structured financing opportunities: technology deployment facilities, vendor-financed ERP contracts, and hybrid instruments that fund the transformation in return for a share of the resulting margin improvement.

This translates into 3 scenario cases:

Base case: DEFA ratification proceeds through 2026, accelerating compliance-driven modernisation across financial services, logistics and healthcare. Mid-market multiples for tech-enabled businesses expand relative to unreformed peers over a 24 to 36-month horizon.

Upside: GenAI adoption compounds EBITDA improvement faster than consensus expects, pulling forward exit timelines and compressing GP hold periods.

Downside: DEFA implementation is diluted or delayed, removing the regulatory forcing function, and transformation programmes stall at proof-of-concept, extending hold periods and pressuring net internal rates of return (IRR).

Conclusion

The non-consensus read for family offices and institutional LPs is this: the risk in Southeast Asia is not under-allocation to the region. It is mis-allocation into fund strategies calibrated for the market-entry era that have not structurally rebuilt for the operational one. Both strategy types are currently raising capital, both reference the same macroeconomic tailwinds, and both can point to a vintage of returns that no longer reflects the forward opportunity.

The deeper structural point, which most sell-side research on SEA will not commit to, is that the region's next wave of value creation is not a technology story and not a macro story. It is a plumbing story. The mid-market companies that run Southeast Asia's real economy — that move goods, process claims, issue credit, and operate clinics across five currencies and ten regulatory regimes — are sitting on compressible costs and expandable margins. The capital that unlocks that value will not come from another consumer internet bet. It will come from the machine room.

References

EY — Southeast Asia Private Equity Pulse 2025: Year in Review — February 2026

IDC — Worldwide Black Book: Live Edition, ASEAN IT Spending — June 2025

KPMG — Asia Pacific Private Equity Barometer 2026 — March 2026

HFS Research — Asia-Pacific Legacy Tech Burden Report — 2025

McKinsey & Company — Technical Debt and Legacy IT Costs — cited December 2025

Allen & Gledhill — ASEAN DEFA Substantially Concluded — November 2025

World Economic Forum — ASEAN Takes Major Step Toward Digital Economy Pact — October 2025

Tech Collective SEA — Why Legacy Systems Are Stalling Southeast Asia's Global Ambitions — March 2026

Bain & Company — Asia-Pacific Private Equity Report 2026 — March 2026

Deloitte — Asia Pacific Private Equity Almanac 2026 — March 2026

Disclaimer: This article is for information and discussion only and does not constitute investment advice or a recommendation.