ASEAN's Carbon Infrastructure Sprint: Singapore Is Quietly Cornering the Article 6 Intermediary Layer

Five compliance frameworks are activating simultaneously across Asia. The firms that position at the origination and structuring layer in the next 90 days will set the pipeline terms for the next decade.

Why This Matters

Convergence, not fragmentation: Vietnam's Decree 29/2026, Malaysia's 2026 carbon tax, Japan's mandatory Green Transformation Emissions Trading System (GX-ETS), and Singapore's S$15 million Carbon Market Development Grant are activating simultaneously — creating the region's first genuine compliance demand stack before verified supply in eligible categories has scaled.

The intermediary layer is being locked in now: Singapore has signed Article 6.2 Implementation Agreements (IAs) with Thailand (August 2025) and Vietnam (September 2025), establishing the bilateral transfer architecture for Internationally Transferred Mitigation Outcomes (ITMOs). The firms structuring the first tranche of ITMO-eligible credits under these IAs will set the documentation templates, the preferred registry relationships, and the counterparty networks that become the default for all subsequent transactions.

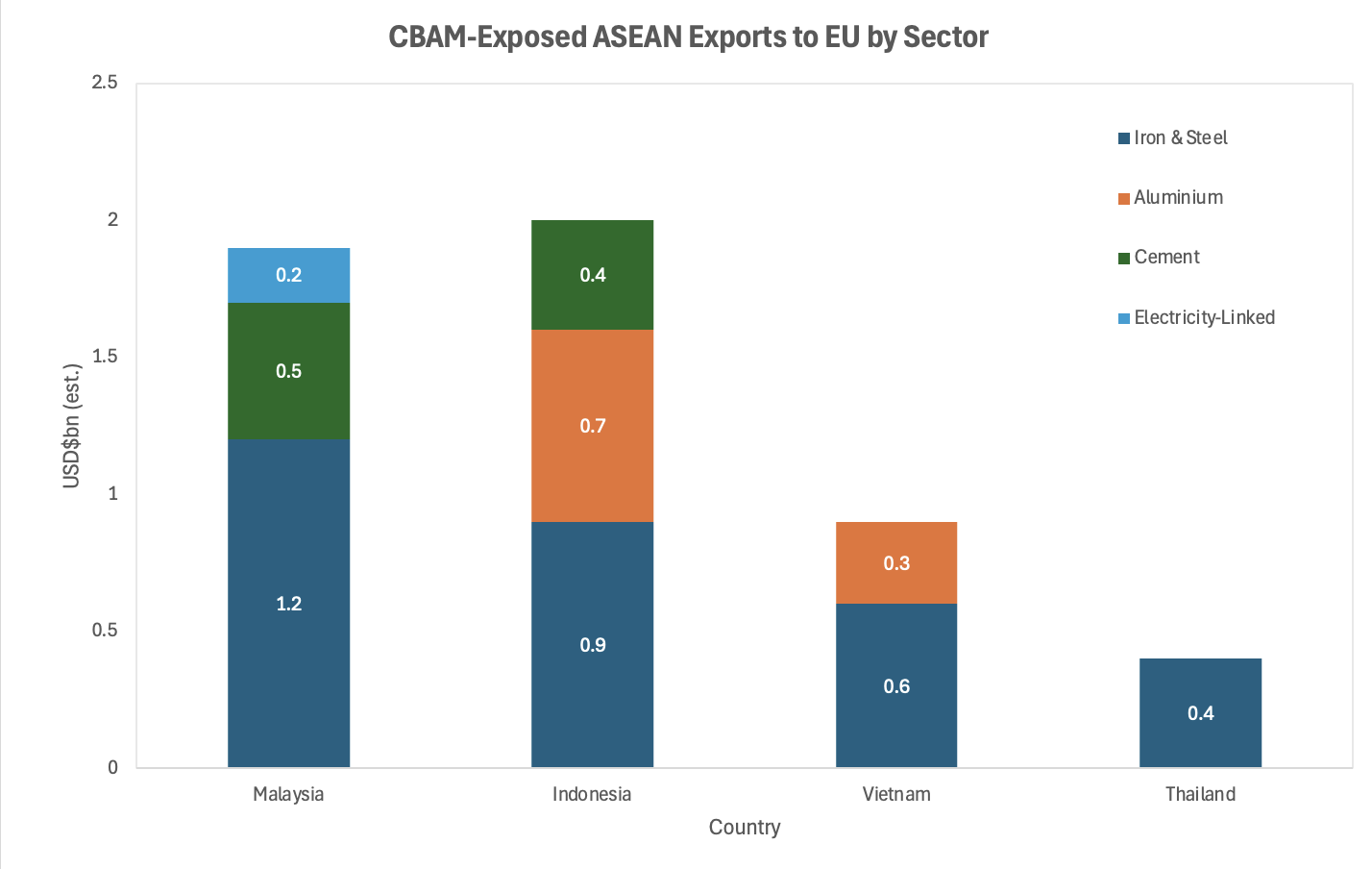

The EU Carbon Border Adjustment Mechanism creates external compulsion: The Carbon Border Adjustment Mechanism (CBAM) entered full force in 2026, pricing embedded carbon in steel, aluminium, cement, fertilisers, and electricity-linked goods. Malaysian, Indonesian, and Vietnamese exporters now face a double squeeze — domestic carbon pricing liability plus an EU border levy — rewarding any firm that controls the verification and structuring layer for their decarbonisation pathway.

The Core Shift

The consensus framing of ASEAN carbon markets as "fragmented and pre-commercial" is anchored to conditions that no longer exist. Three regulatory events in Q1 2026 have moved the regional carbon complex from aspiration to compliance obligation.

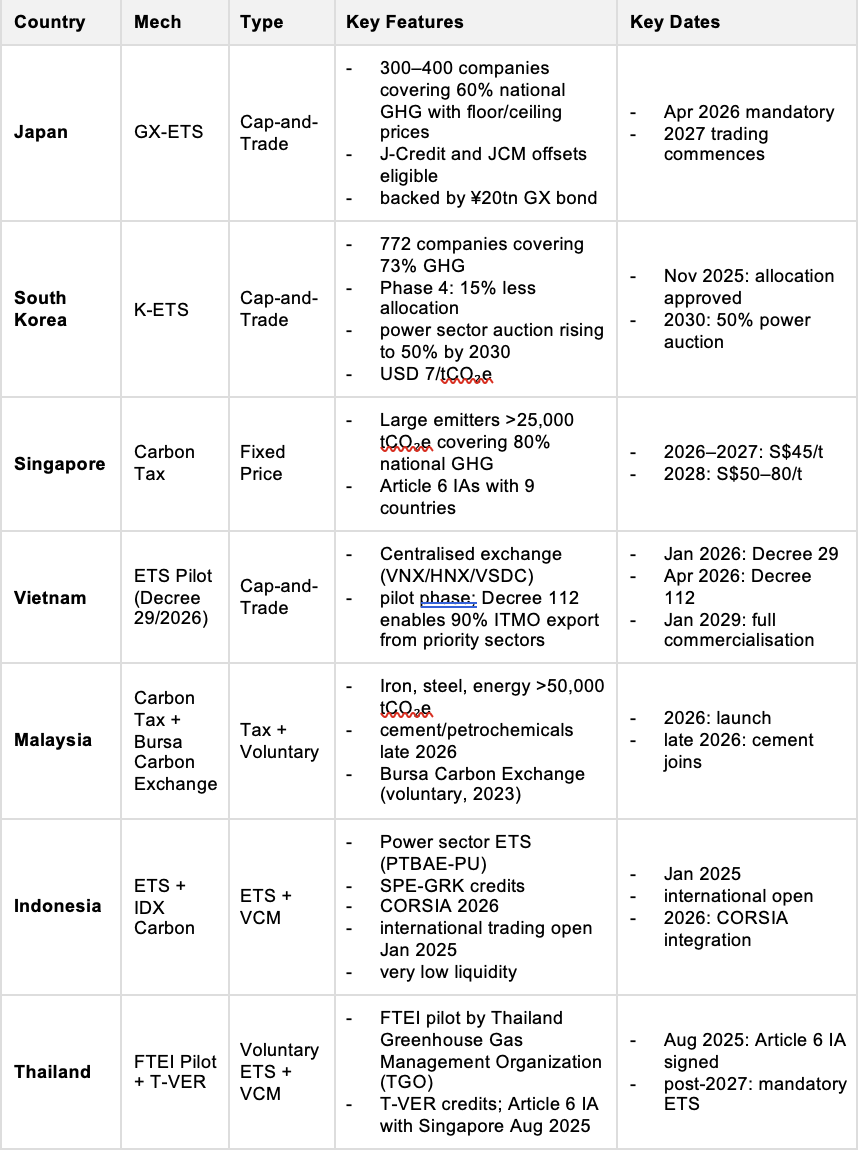

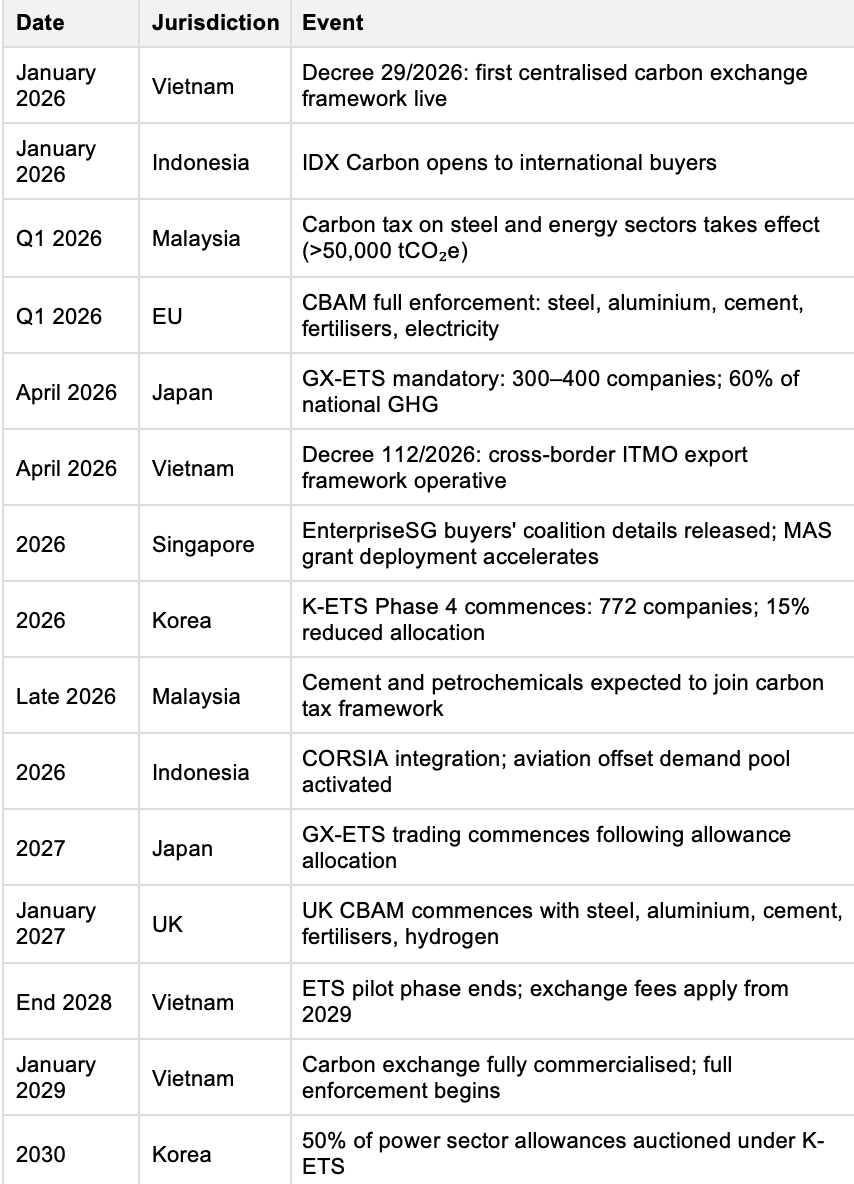

Vietnam's Decree 29/2026/ND-CP (19 January 2026) operationalised the country's first centralised carbon exchange, integrating the Vietnam Exchange (VNX), the Hanoi Stock Exchange (HNX), and the Vietnam Securities Depository and Clearing Corporation (VSDC) into a legal framework covering registration, trading, custody, and settlement of both greenhouse gas (GHG) emission quotas and eligible carbon credits. A second decree, Decree 112/2026/ND-CP (1 April 2026), introduced a cross-border framework allowing offshore wind, carbon capture, and green hydrogen projects to sell up to 90% of their generated credits internationally — an explicit signal that Vietnam intends to function as a net credit exporter under Article 6. The pilot phase runs to end-2028, with full commercialisation from 1 January 2029.

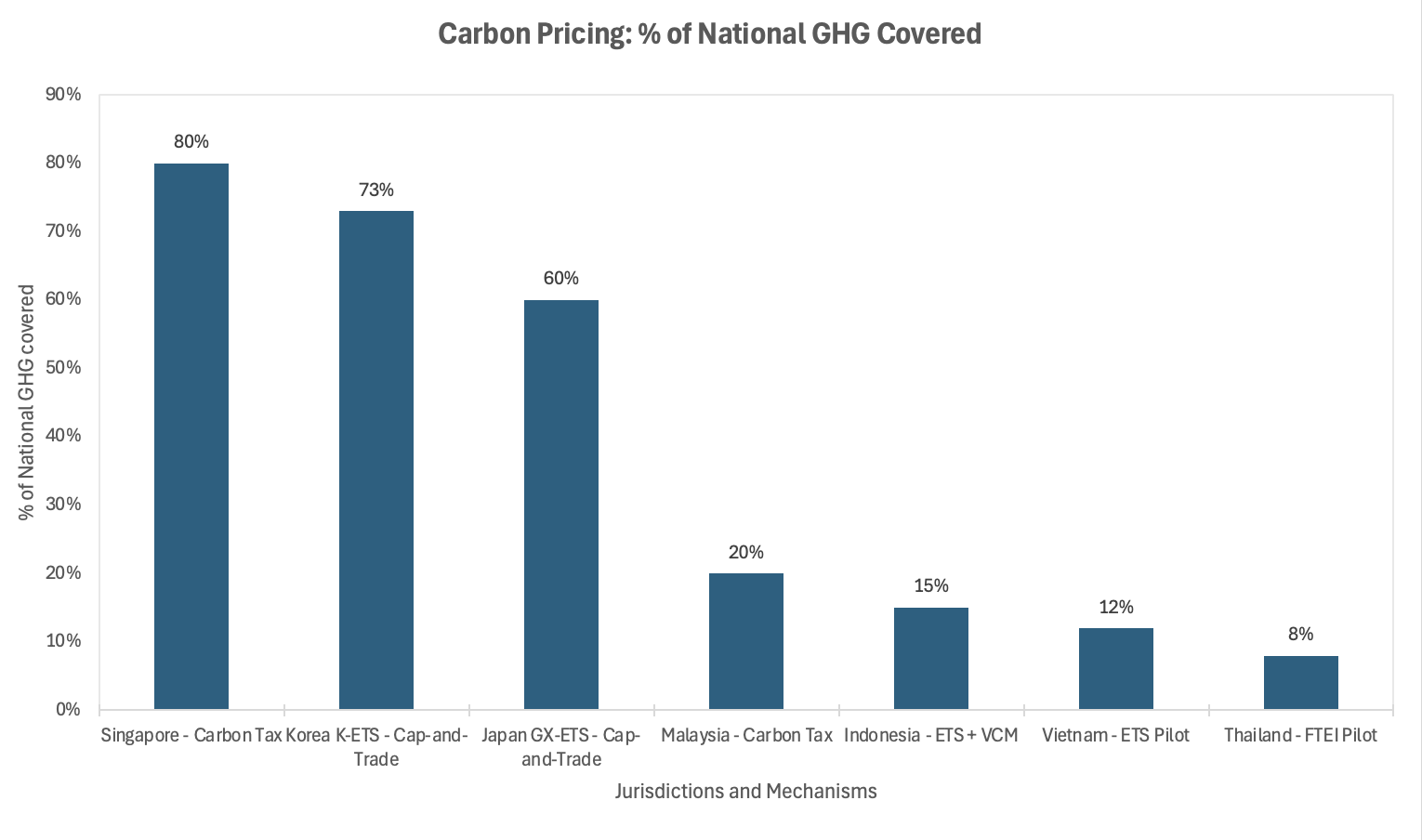

Malaysia has launched its carbon tax on iron, steel, and energy sectors in 2026, capturing any facility emitting more than 50,000 tonnes of CO₂ equivalent (tCO₂e) annually — a threshold that captures every major integrated steel plant and utility-scale power generator in the country from day one. Cement and petrochemicals are expected to be integrated into the framework by late 2026. The tax rate is being finalised by the Ministry of Finance; the structural direction aligns explicitly with EU CBAM compliance strategy.

Japan's GX-ETS became mandatory in April 2026, applying to roughly 300–400 companies that collectively account for approximately 60% of Japan's annual greenhouse gas output. This is Japan's first structured compliance carbon market at scale, mirroring EU ETS architecture with floor and ceiling price mechanisms. Allowance allocation has commenced; trading is scheduled from 2027. The GX-ETS was backed by Japan's GX transition bond programme, which raised ¥20 trillion to fund the broader Green Transformation policy suite.

Source: MAS; ICAP; Korea Exchange; IDX Carbon; JPX.

The Non-Obvious Mechanism

The intermediation hierarchy in Article 6.2 credit transfers is being established now, not in 2028. What most allocators have not followed to its logical conclusion is that bilateral IAs between Singapore and counterparty nations are not diplomatic instruments alone — they define the pipeline architecture: the verification standards, the corresponding adjustment procedures, the eligible project categories, and the accounting rules for ITMO transfers. Singapore has signed its first ASEAN IAs with Thailand (August 2025) and Vietnam (September 2025), having already executed seven earlier agreements with non-ASEAN partners. Negotiations with Indonesia, Cambodia, and the Philippines are at various stages of advancement.

Source: ICAP; NCCS Singapore; national climate regulators.

The firms that structure the first tranches of ITMO-eligible credits under these bilateral frameworks will establish template documentation, preferred registry relationships, and counterparty networks that become the default for subsequent transactions. This is a classic winner-takes-most dynamic in a market where counterparty trust, document precedent, and regulatory familiarity compound as barriers to entry. The strategic play is not carbon advisory per se — it is positioning at the Article 6 origination, verification, and structuring layer before the pipeline terms are locked.

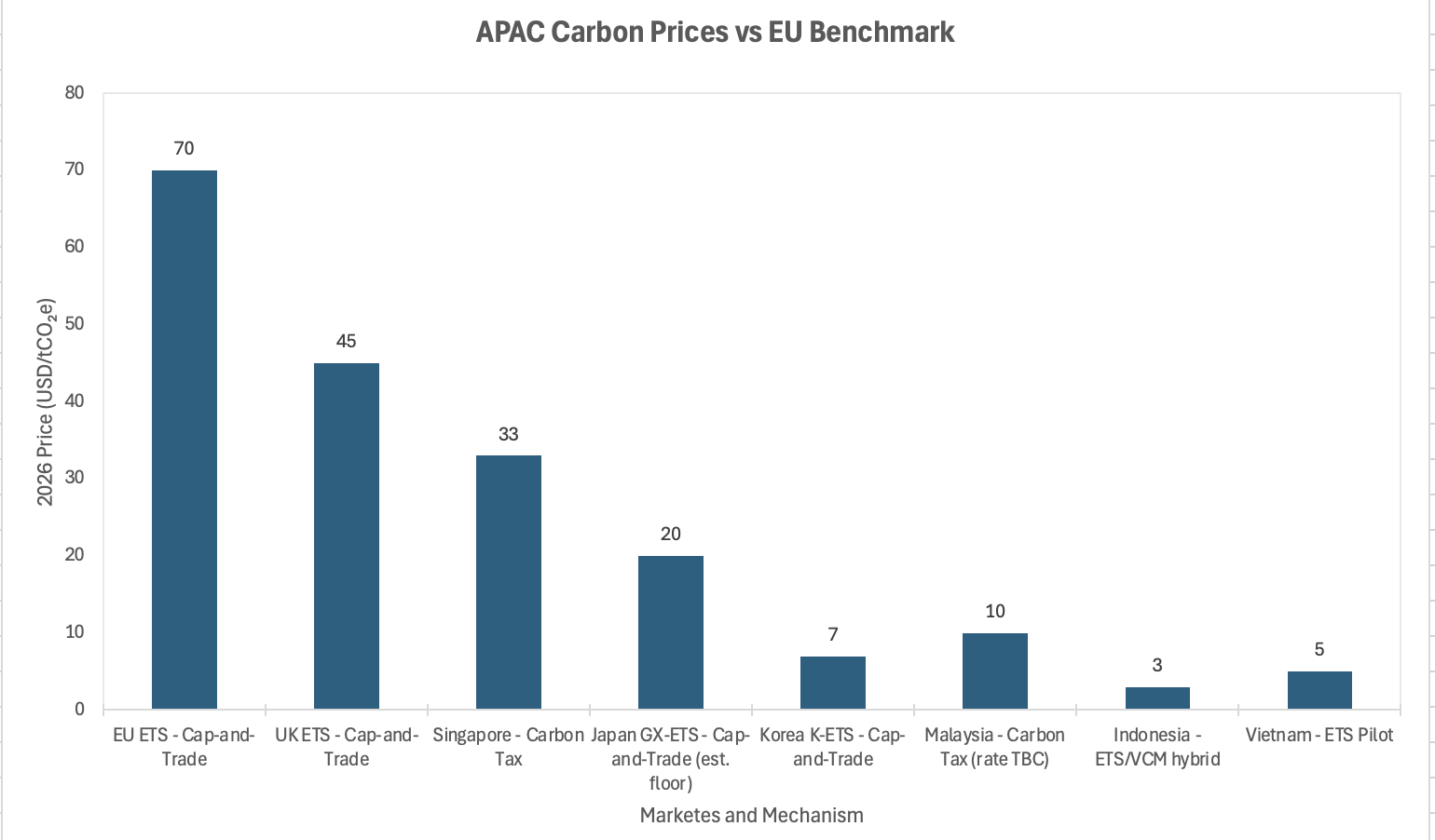

The MAS's S$15 million Financial Sector Carbon Market Development Grant, operational until October 2028, is the institutional vehicle for this positioning. It covers manpower costs for establishing or expanding carbon project financing and trading teams, and defrays upfront transaction structuring costs including due diligence, verification fees, and carbon credit insurance premiums. EnterpriseSG's industry-led buyers' coalition, whose details are expected in 2026, is the demand-side complement: aggregating regional corporate buying interest and channelling it toward high-integrity credits eligible under Singapore's domestic carbon tax framework, where S$45 per tonne applies in 2026–2027 and rises to S$50–80 per tonne by 2028–2030.

The deeper mechanism is verification capacity. The pipeline of projects in Vietnam, Indonesia, and Thailand that will generate ITMO-eligible credits under the bilateral frameworks requires third-party verification against Article 6.4 and domestic standards. Accredited verifiers — SGS, Bureau Veritas, DNV and their technical affiliates — face a structural bottleneck as project pipelines accelerate faster than their capacity to certify. The firm controlling project pipeline introductions with pre-existing verifier relationships controls the credit issuance schedule. A cautious sell-side analyst would not publish this observation; it is nonetheless the correct framing.

Investor and Stakeholder Implications

For corporates with regional operations: Malaysian steel, cement, and energy companies face immediate compliance liability with no voluntary opt-out mechanism, creating forced demand for either capital expenditure in abatement or credit procurement — the latter being structurally faster in the near term. Vietnamese manufacturers operating under GHG emission quotas established by Decree 29 must now integrate carbon account management into treasury and compliance functions, with market price discovery conducted publicly through the VNX/HNX system. Japanese industrials under GX-ETS compliance face a 2026–2027 reporting cycle followed by the commencement of allowance obligations; the Joint Crediting Mechanism (JCM), Japan's bilateral offset framework, now intersects with Article 6.2, creating dual-pathway credit sourcing opportunities from Southeast Asian project developers.

For bankers and M&A advisors: The structuring of ITMO transfer agreements between sovereign parties creates a class of instrument with no established secondary market, no standardised documentation, and significant legal complexity around corresponding adjustments and registry reconciliation. The first five to ten precedent transactions will command substantial advisory fees for firms with experience in climate treaty obligations. Beyond advisory, the project finance implications are significant: offshore wind, REDD+, and methane capture projects in Vietnam, Indonesia, and Thailand now have a new exit pathway — ITMO credit monetisation — that potentially extends the bankable revenue stream beyond power purchase agreements, improving debt-service coverage ratios and supporting leverage.

Second-order effects across the value chain: The least-discussed consequence is the demand surge for measurement, reporting, and verification (MRV) infrastructure. ESG data platforms, registry software providers, satellite-based monitoring firms, and carbon accounting technology companies will face demand that outpaces supply for at least 18–24 months as new compliant installations come online across the region. Verification body capacity is a hard constraint. Insurance underwriters with carbon credit product experience — covering non-delivery risk, permanence risk, and additionality challenges — will find an immediately addressable market. For capital market participants, the actionable second-order position is in the enabling infrastructure, not the credits themselves.

Korea's K-ETS Phase 4 (2026–2030), approved November 2025, reduced total allocation by 15% and is gradually increasing auctioned allowances in the power sector, reaching 50% by 2030. The carbon price at approximately USD 7 per tonne remains structurally underpriced relative to abatement cost — a gap that creates pressure for correction and may accelerate corporate procurement of regional offsets as the cheapest near-term compliance pathway. Indonesia's IDX Carbon opened to international buyers in January 2025 but transaction values collapsed to IDR 1 billion (approximately $72,621) across March–September 2025, exposing a deep liquidity gap that represents both a problem and an opportunity. The firm that can bring institutional-grade liquidity to IDX Carbon's pipeline of 1.78 million tCO₂e from state-owned utility PLN's power plants is not competing against anyone.

Near-Term Catalysts and Policy Outlook

0–3 months: The activation of Singapore's EnterpriseSG buyers' coalition alongside Malaysia's first carbon tax compliance cycle forces corporates across the region to either procure credits or hold internal abatement positions. Demand in compliant credit categories will outpace verified supply. The first bilateral ITMO transfers under the Singapore–Vietnam IA will test the documentary and registry infrastructure; any operational friction will delay the pipeline and compress the window for new entrants to position.

3–12 months: Japan's GX-ETS allowance allocation process produces the first set of compliance-grade demand signals. Japanese trading houses with regional presence — Mitsui, Mitsubishi, Sumitomo — are already positioning in Southeast Asian carbon project origination; their entry compresses the timeframe for independent boutiques to establish counterparty relationships. Vietnam's cross-border framework under Decree 112 enables offshore wind developers to begin locking in ITMO monetisation terms with Singapore-based intermediaries. Indonesia's CORSIA integration confirmed for 2026 creates a new aviation offset demand pool drawing on SPE-GRK certificates.

Three plausible scenarios frame the 2026–2028 horizon:

Base: Singapore consolidates its position as the primary Article 6 clearinghouse for ASEAN, with the MAS grant ecosystem producing five to eight fully operational ITMO-eligible project pipelines by end-2027. Credit prices for compliant ASEAN ITMOs converge toward Singapore's domestic carbon tax rate (S$45–50/tCO₂e), narrowing the pricing spread from both the supply side as project pipelines develop and the demand side as corporate compliance obligations escalate.

Upside: The UK CBAM, entering force January 2027, extends external compliance pressure to a second major export market, accelerating credit procurement by Indonesian and Malaysian exporters and pushing ITMO-eligible credit prices materially above Singapore's domestic carbon tax rate. The EU's review of CBAM sectoral scope — fertilisers, hydrogen, and polymers are under consideration — would further widen the set of obligated buyers.

Downside: Indonesian political resistance to meaningful ETS expansion, combined with delays in the VNX exchange operational launch in Vietnam, extends the supply-demand imbalance but depresses credit price formation. In this scenario, the intermediary layer remains highly valuable but the volume of transactable credits disappoints; fee income from structuring mandates replaces volumetric income from credit flows.

Source: IGES policy brief; Bank Negara Malaysia; European Commission CBAM; estimates based on 2022–2024 trade data.

Regional ETS and Carbon Tax

Key Dates - 2026–2029 for Carbon Infrastructure

Conclusion

The non-consensus position is this: the Article 6 intermediary layer in ASEAN is not a market that will develop — it is a market that is being designed right now, through bilateral government-to-government agreements that will set the terms of credit origination, transfer, and settlement for the remainder of this decade. Singapore is not simply participating in that process; it is structuring the architecture. The MAS grant, the EnterpriseSG buyers' coalition, and the succession of ASEAN Implementation Agreements constitute a deliberate industrial policy to make Singapore the clearinghouse for regional carbon capital flows — analogous to its historical positioning in commodity trade finance, derivatives clearing, and Islamic finance origination.

The structural read-across is significant. Markets where the intermediary layer is cornered early exhibit persistent rent extraction: the early mover benefits from network effects, documentation lock-in, and regulatory familiarity that later entrants cannot replicate at equivalent cost. The CBAM overlay reinforces this dynamic by imposing an external deadline — ASEAN exporters cannot wait for the regional market to mature before they need credible decarbonisation documentation. The combination of internal compliance pressure and external trade pressure is not cyclical. It is a structural repricing of carbon-intensive production across the region, and the firms that control the measurement, verification, and structuring layer will capture a disproportionate share of the value generated in that transition.

The investor conclusion is not a call to buy carbon credits. It is a call to identify and position in the enablers of the compliance stack: origination-layer advisory firms, verification infrastructure, registry technology, carbon insurance underwriters, and project finance structures that unlock ITMO-eligible credit pipelines in Vietnam, Indonesia, and Thailand. The window before bilateral pipeline terms are locked and preferred counterparties established is, in all practical terms, already closing.

References

Baker McKenzie — Vietnam: Operational Framework for Domestic Carbon Exchange Established — January 2026

Vietnam Briefing — Decree 29/2026: Vietnam Operationalizes Its First Carbon Trading Market — March 2026

Vietnam Investment Review — Vietnam Rolls Out First Legal Framework for Cross-Border Carbon Credit Trading — April 2026

MAS / Straits Times — MAS Launches S$15 Million Grant to Spur Financial Institutions to Participate in Carbon Markets — October 2025

ClearBlue Markets — Singapore to Support the Development of High-Integrity Carbon Markets — October 2025

S&P Global Energy — Malaysia Sets 2026 Carbon Tax, Reaffirms Decarbonization Goals — October 2024

Reccessary — Malaysia's Carbon Tax Set for 2026: Experts See Short-Term Pain, Long-Term Gain — October 2025

ACT Group — Japan's GX-ETS to Become Mandatory for Large Emitters in 2026 — October 2025

Japan Times — Japan's Top Polluters Face New Rules as Carbon Market Advances — March 2026

JPX / Japan Exchange Group — GX-ETS Starting in April 2026 — March 2026

ICAP — Korea Approves Phase 4 K-ETS Allocation Plan for 2026–2030 — November 2025

InfluenceMap — South Korea's Emissions Trading Scheme Weakened by Pressure from Industry — February 2026

S&P Global Energy — Indonesia Launches International Carbon Trading on IDX with Five Power Plants — January 2025

IEEFA — Two Years After Launch, Indonesia's Carbon Market Struggles to Find Momentum — October 2025

S&P Global Energy — Singapore, Thailand Sign Article 6 Deal in Boost to ASEAN Carbon Markets — August 2025

NCCS Singapore — Annex A: About the Singapore–Thailand Implementation Agreement — August 2025

Reccessary — Diverging Paths: Asia Pushes Ahead on Article 6 — September 2025

IGES — Implications of the EU's Carbon Border Adjustment Mechanism for ASEAN Member States — Policy Brief

Southeast Asia Public Policy Institute — SEA Global Relations Outlook 2026: European Union — January 2026

This article is for information and discussion only and does not constitute investment advice or a recommendation.