Same Model, Same Voice, Same Brand: The Hidden Cost of Delegating Strategy to AI

Brand equity is not destroyed by a single bad campaign. It erodes gradually, in the gap between what a brand says it stands for and what its output actually communicates — and right now, that gap is widening for reasons most marketing teams have not yet named.

Why This Matters

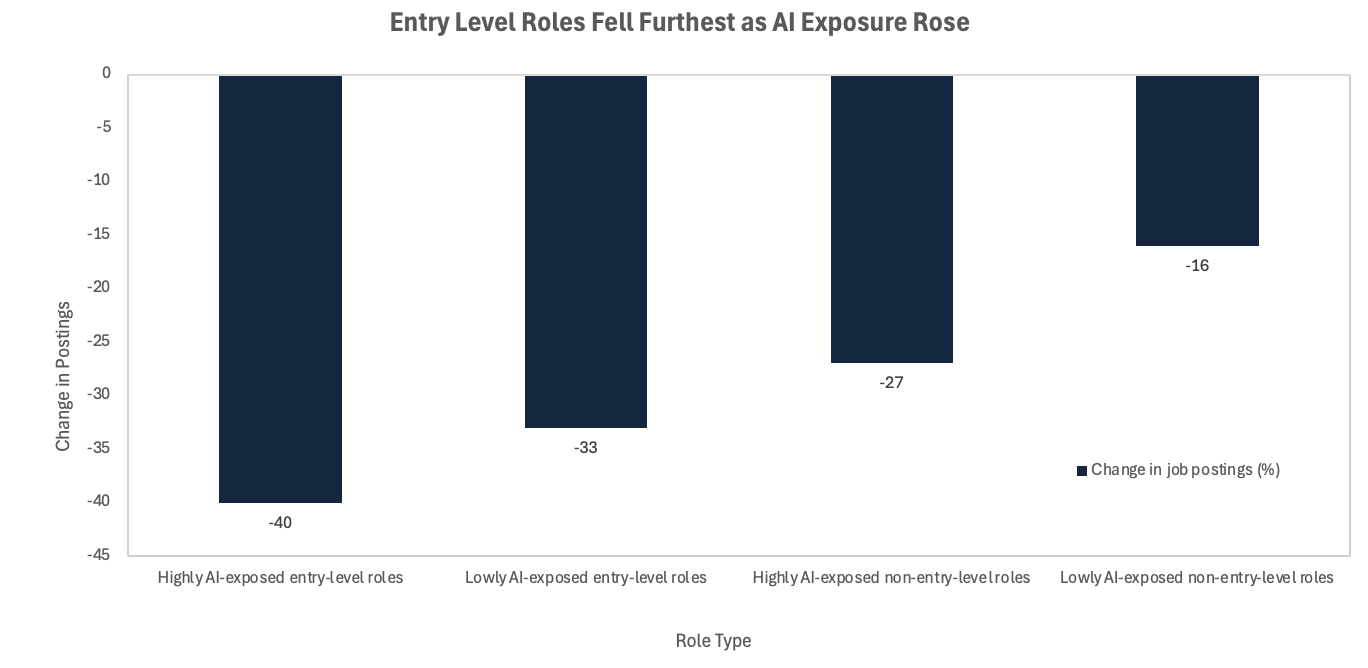

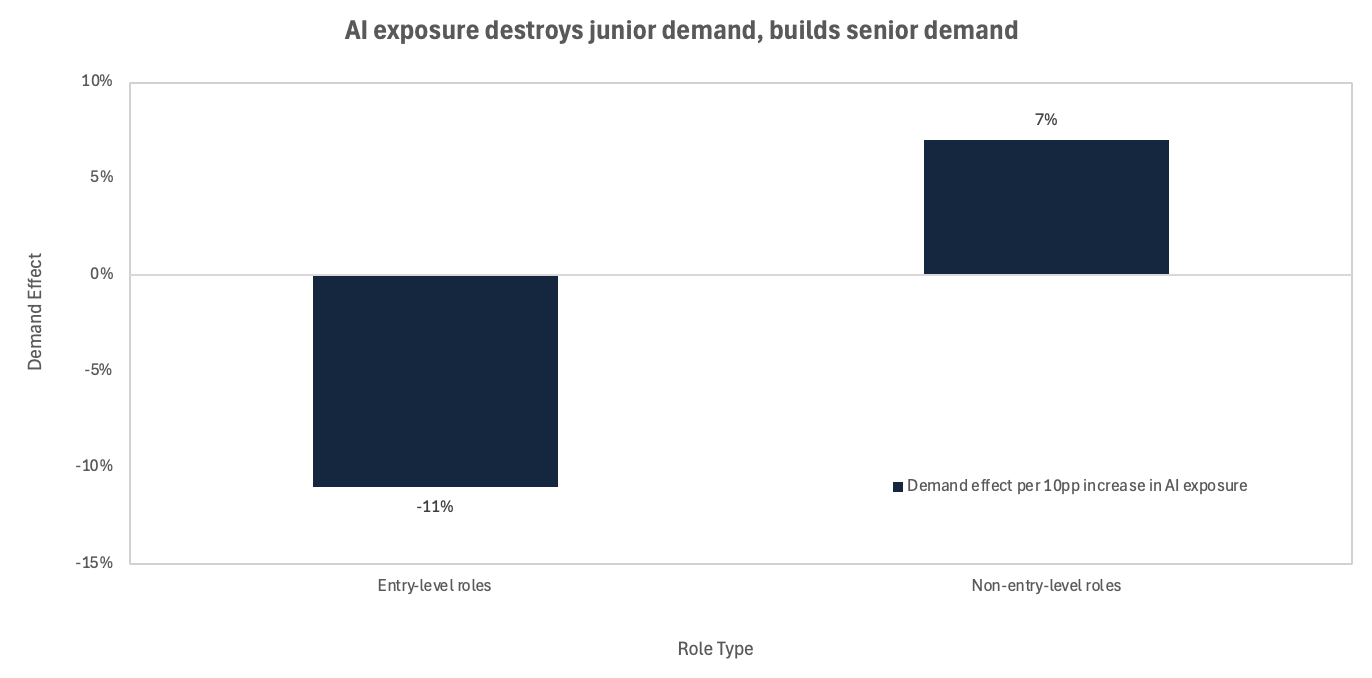

Labour market: Entry-level roles in the United States are under pressure, with the World Economic Forum reporting that entry-level roles are down 35 per cent, while jobs mentioning artificial intelligence have risen sharply even as broader hiring remains weak.

Employer expectations: Gallup found that half of employed American adults now use artificial intelligence in their role at least a few times a year, with frequent use also rising, which means 2026 graduate cohorts are entering workplaces where these tools are already becoming normalised.

Career divergence: The advantage will accrue not to those who merely have access to artificial intelligence, but to those who can structure prompts, test outputs, and apply domain judgement faster than peers who still work in a pre-artificial intelligence way.

The Core Shift

Non-AI blog creation has collapsed from 65% of marketing output to approximately 5% in three years. By 2026, an estimated half of all marketing content is AI-generated, with another 42% AI-assisted. The speed and scale advantages are real: AI-generated social captions have demonstrated engagement improvements while cutting manual effort by around 70%, and AI personalisation tools now adapt messaging in real time across behavioural, contextual, and historical signals in ways no human team could match at volume.

Source: Revelio Labs, "Is AI Responsible for the Rise in Entry-Level Unemployment?", 3 August 2025. Based on job postings data indexed to January 2023 baseline.

The adoption curve, however, has outpaced the strategic thinking about where AI belongs in the production hierarchy. The question most marketing teams have not asked is not "can AI produce this?" but "should AI be the origin of this?" Those are entirely different questions, and conflating them is where the damage begins.

The Non-Obvious Mechanism

The homogenisation problem is structural, not correctable by better prompts. Generative models are trained on content that already exists — which means they are learning from marketing material that has already been optimised, refined, and narrowed by years of A/B testing and best-practice convergence. They are, in effect, learning the patterns of patterns. When millions of marketing teams then apply similar prompts to those same models, the outputs naturally cluster around the statistical centre. The edges are smoothed away. Distinctive voices disappear.

A 2026 study published in a peer-reviewed journal confirmed this formally: generative AI models are inherently prone to regression toward the mean, producing outputs that trend toward the broadly acceptable rather than the genuinely differentiated. A related SSRN paper on digital marketing noted that homogenisation from AI adoption "may dampen consumer engagement and dilute brand uniqueness over time". The more consequential finding from the Nuremberg Institute for Market Decisions is that consumers penalise AI-generated content even when the content is objectively identical to human-made equivalents — labelling an ad as AI-produced made participants view it as less natural, less useful, and they were less inclined to engage or purchase as a result. This is a trust penalty built into perception, not quality.

The implication is uncomfortable for budget-driven CMOs: the efficiency gains from AI content production may be partially offset by a structural discount that accrues to the brand over time. It does not appear on a quarterly dashboard. It shows up 18 months later in brand tracking scores, share-of-voice metrics, and the cost of re-earning attention that was quietly lost.

Source: Revelio Labs, August 2025

Investor and Stakeholder Implications

Brand equity is a balance-sheet adjacent asset that most finance teams undervalue until it deteriorates. For consumer-facing businesses, the cash-flow implications of eroding brand distinctiveness are material: pricing power weakens as brands become interchangeable; customer acquisition costs rise as organic reach declines; and retention becomes increasingly dependent on promotional spend rather than genuine loyalty. Organic reach across major social platforms dropped by an estimated 40–60% in 2025, and brands competing primarily on AI-generated content volume have fewer tools to arrest that decline. The brands with authentic, differentiated voices are the ones Hootsuite's 2026 Social Trends report identifies as winning through human-made authenticity — not because authenticity is fashionable, but because it is algorithmically and emotionally harder to replicate.

For investors evaluating consumer or media businesses, the audit question is whether the marketing function has a clear delineation between where AI executes and where humans originate. Companies that cannot answer that question cleanly are carrying a brand risk that is not yet visible in their numbers.

Near-Term Catalysts and Policy Outlook

The next 12 months represent an asymmetric window: the brands that restore human upstream judgment now will compound that advantage as AI-generated content volumes continue to rise across all competitors.

0–3 month window: The practical pressure point is the EU's AI labelling requirement, currently in consultation, which would require disclosure of AI-generated advertising content. Research by the Nuremberg Institute shows this disclosure materially reduces consumer engagement and purchase intent. Brands relying heavily on AI-generated creative will face a near-term choice between compliance costs and reputational exposure.

3–12 month window: Kantar's 2026 Marketing Trends report identifies AI purchasing agents as the next structural shift — consumers will brief autonomous agents to make purchase decisions on their behalf. In that environment, a brand's measurable attributes across third-party sources (reviews, editorial coverage, forum sentiment) will carry more weight than owned messaging. Brands that have delegated their narrative to AI will have thinner third-party signal to draw on, because they have produced less genuine opinion, less cultural commentary, and less content that earns citation.

The scenario distribution for the next 12 months is as follows.

Base case: AI content volumes continue rising, organic engagement continues declining at a moderate rate, and the performance gap between distinctive and commoditised brands widens slowly enough to remain deniable in quarterly reporting.

Upside: Regulatory pressure on AI labelling accelerates the revaluation of authentic brand voice; early movers who have rebuilt human creative ownership gain outsized earned media and pricing power relative to peers.

Downside: AI agents become the dominant purchase-decision mediator faster than expected; brands without strong third-party sentiment and consistent attribute signals are systematically de-recommended by those agents, compressing both volume and margin simultaneously.

Conclusion

The structural read here is not anti-AI — it is a capital allocation argument. AI is genuinely superior at execution: personalisation at scale, real-time media optimisation, A/B testing at volume, and data synthesis across customer touchpoints. It consistently underperforms on the tasks that build durable brand equity: original narrative, cultural relevance, emotional resonance, and any position that requires a brand to say something that a statistically averaged model would not publish. The distinction between execution and origination is the one that marketing leadership needs to institutionalise — not as a philosophical preference for human creativity, but as a risk management decision about brand equity depreciation. The brands that treat AI as a force multiplier for human strategic judgment will compound their differentiation. Those that use it as a substitute for that judgment are running down an asset they have not yet valued correctly.

References

Typeface — Content Marketing Statistics to Watch, 2026 — March 2026

HubSpot — State of Marketing Report 2026 — 2026

AIJourn — The Homogenization Problem: Why AI-Generated Marketing All Sounds the Same — October 2025

Journals of SAGE Publications — When Artificial Intelligence Makes Everything Similar — March 2026

SSRN — Generative AI and Content Homogenization: The Case of Digital Marketing — July 2025

Nuremberg Institute for Market Decisions (NIM) — Consumer Attitudes Toward AI-Generated Marketing Content — 2025

Hootsuite — Social Media Trends 2026 — January 2026

Kantar — Marketing Trends 2026 — March 2026

Market Science — AI is Breaking Brand Visibility and Marketing Measurement — May 2026

CXL — How Mindless Use of AI Content Undermines Your Brand Voice — September 2025

This article is for information and discussion only and does not constitute investment advice or a recommendation.