The Relational Balance Sheet: What Supply Chain Switching Costs Are Doing to Capital Allocation

The market has spent three years pricing tariffs. It has barely started pricing the cost of leaving.

The structural rewiring of global supply chains is well documented. What is not is the liability it has quietly created on both sides of the supplier relationship: a relational switching premium that sits off balance sheet, is absent from most equity and credit models, and is now beginning to crystallise into real cash flow consequences. This is not a logistics story. It is a capital allocation story.

Why This Matters

Mispriced risk: Switching costs embedded in long-standing supplier relationships are not captured in standard DCF models or credit spreads, creating asymmetric exposure for investors who assume flexibility that no longer exists.

Balance sheet blind spot: Companies that defected from established supplier networks to chase tariff arbitrage are now discovering that re-entry carries a loyalty premium that erodes the margin gain they were chasing.

Policy acceleration: The US-China tariff regime, the EU's Critical Raw Materials Act, and emerging "trusted supplier" frameworks in defence and semiconductors are converting informal loyalty into a formal, priced input — one the market has not yet fully absorbed.

The Core Shift

For most of the post-2008 era, supply chain management was a discipline of cost extraction. Procurement teams benchmarked relentlessly, ran competitive tenders annually, and treated supplier relationships as renewable contracts rather than durable assets. The model worked because geopolitics was broadly permissive and logistics costs were structurally low.

That architecture is now broken. The US-China tariff escalation that began in 2018 and re-accelerated in 2025 under the Trump administration's second term has driven effective tariff rates on Chinese goods above 100% across several categories, including electronics, steel, and key industrial components. The European Union's Critical Raw Materials Act (CRMA), which entered force in 2024, sets binding domestic processing targets for 34 strategic materials, creating a regulatory floor beneath which supply chain geography can no longer freely move. Meanwhile, the CHIPS Act, the Inflation Reduction Act's domestic content rules, and equivalent frameworks in Japan, South Korea, and India have introduced subsidy architectures that reward supply chain geography, not just cost efficiency.

The cumulative effect is that supply chain decisions have stopped being purely commercial. They are now simultaneously a geopolitical signal, a regulatory compliance question, and a balance sheet commitment. The supplier relationship is no longer a contract that renews; it is a position that appreciates or depreciates. Most capital allocation frameworks have not been updated to reflect this.

The Non-Obvious Mechanism

The tariff cost is visible. The loyalty premium is not. This is where the mispricing lives.

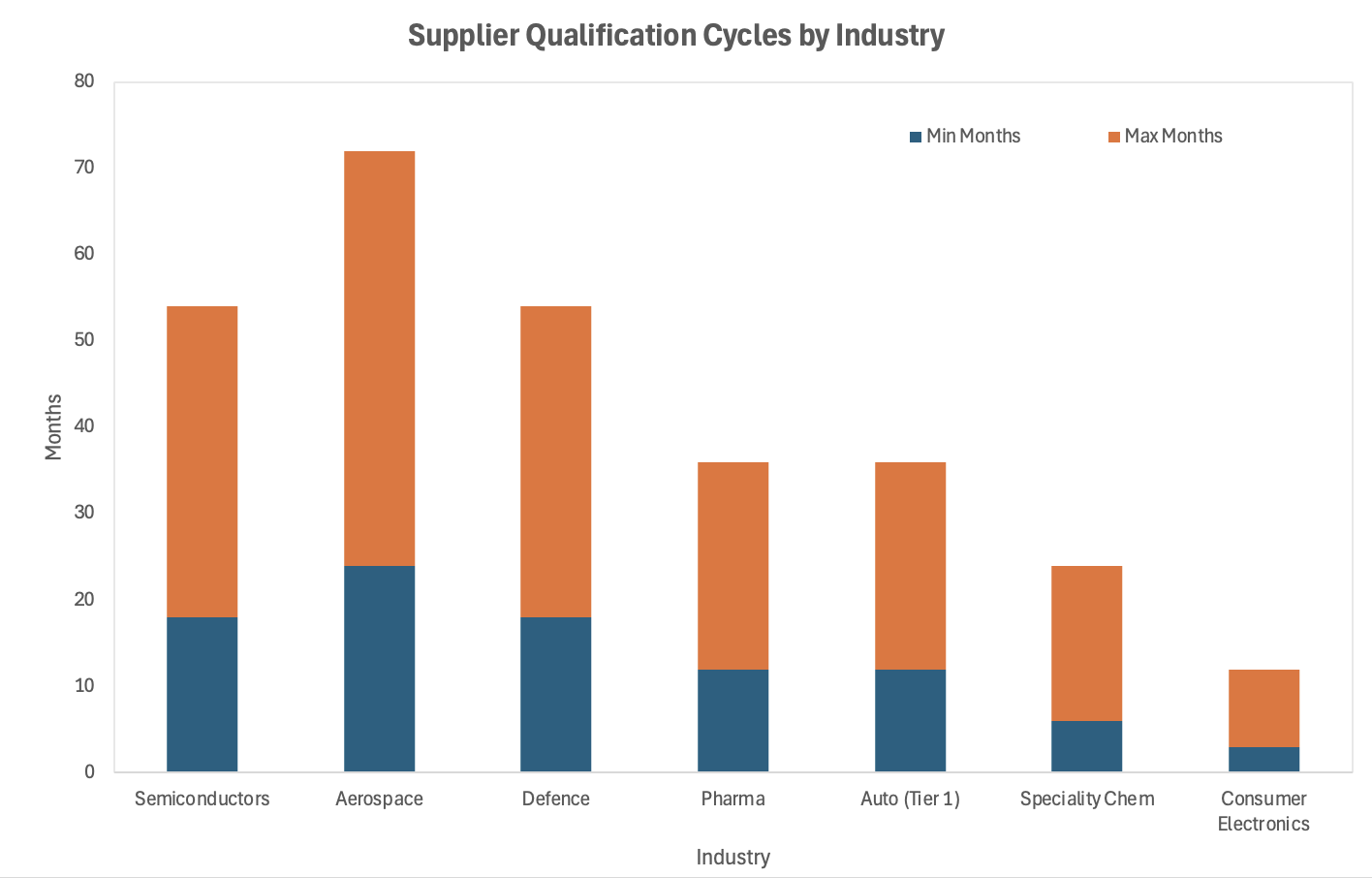

When a buyer defects from a long-standing supplier — whether to chase cheaper alternatives in a new geography, to respond to a government incentive, or to reduce concentration risk — they incur a set of costs that do not appear on any invoice. Qualification cycles for new suppliers in regulated industries (aerospace, defence, semiconductors, pharmaceuticals) routinely run 18 to 36 months. The chart below makes the full range visible: in aerospace, the cycle can extend to 48 months, meaning a defection decision taken today does not resolve until 2029 at the earliest.

Source: Industry estimates, TradeVerifyd, Wolverine LLC

Re-entry costs into established networks, where the original supplier has reallocated capacity to more committed customers, can represent 15 to 25% of the contracted unit value when onboarding, engineering validation, and inventory buffer requirements are aggregated. These costs are real, but they are capitalised inconsistently, often buried in SG&A or operations, and rarely surface cleanly in segment reporting.

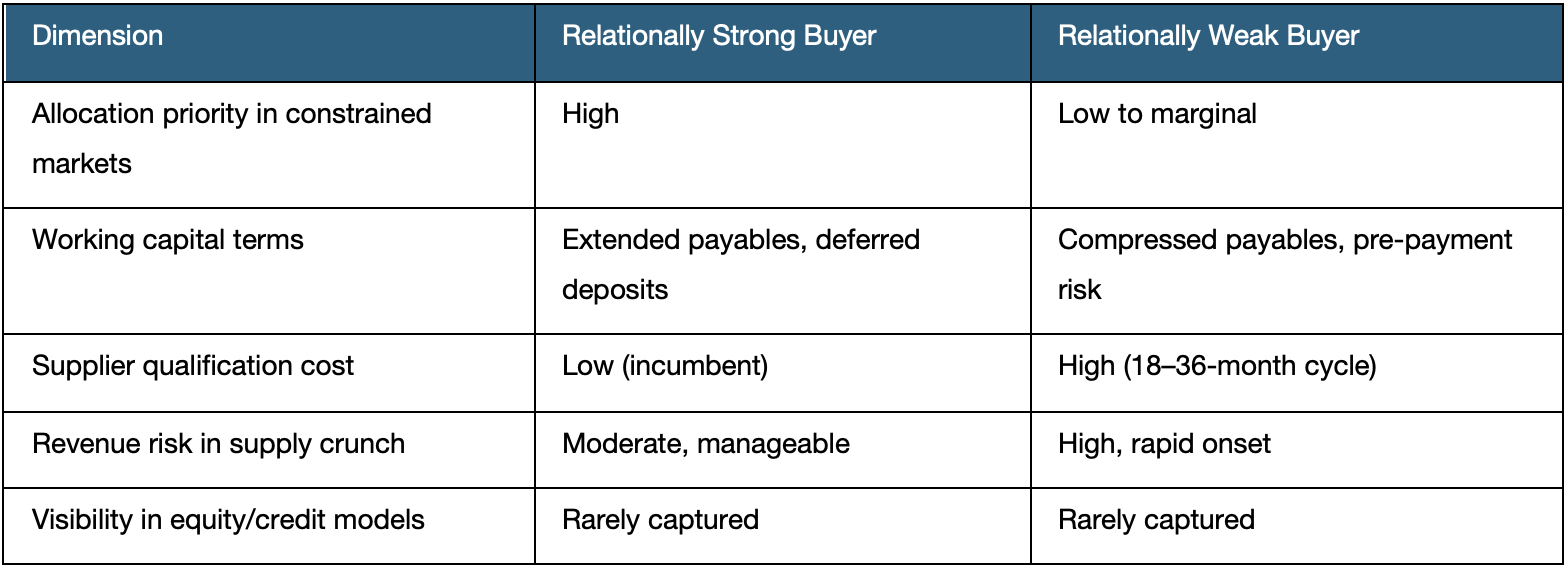

The second-order effect is more consequential. Suppliers operating under capacity constraints — which is now the norm across semiconductor packaging, rare earth processing, and speciality chemicals — are rationing allocation. They are doing so on relational criteria: tenure, payment terms, volume commitment, and what procurement professionals quietly call "loyalty signals." A buyer that switched during the 2020 to 2022 disruption cycle, or that is visibly dual-sourcing as a hedge, is being de-prioritised in allocation queues. This is not sentiment. It is operational. The consequence is that the companies with the most "flexible" supply chain strategies on paper are often carrying the highest execution risk in a constrained market, precisely because their flexibility read as disloyalty.

The third-order effect is the one sell-side models are not following to its conclusion: the loyalty premium is beginning to appear in working capital. Companies with strong supplier relationships are accessing extended payment terms, priority allocation, and collaborative inventory financing that effectively reduces their cash conversion cycle. Companies without those relationships are being asked for longer lead time commitments, higher deposit requirements, and in some cases pre-payment. The divergence in working capital efficiency between relationally strong and relationally weak buyers is widening — and it is not yet visible in most sector-level analyses.

Investor Implications

For equity investors, the implications are most acute in industrials, technology hardware, and consumer durables, where Tier 1 suppliers have genuine pricing power over allocation and where switching costs are highest. The companies most exposed are those that publicly signalled supply chain diversification between 2022 and 2024 without completing the qualification cycle for alternative suppliers. They now carry dual-sourcing costs, reduced priority with original suppliers, and unproven alternatives. The margin compression from this position is not yet fully reflected in forward estimates.[7]

For credit investors, the concern is working capital. A borrower whose cost of goods is rising not because of input prices but because of deteriorating supplier terms is a different credit than the model assumes. Covenants built around EBITDA and leverage ratios do not capture supplier relationship quality. A company that loses priority allocation in a supply crunch faces a revenue shortfall that arrives faster than any early warning system currently flags.

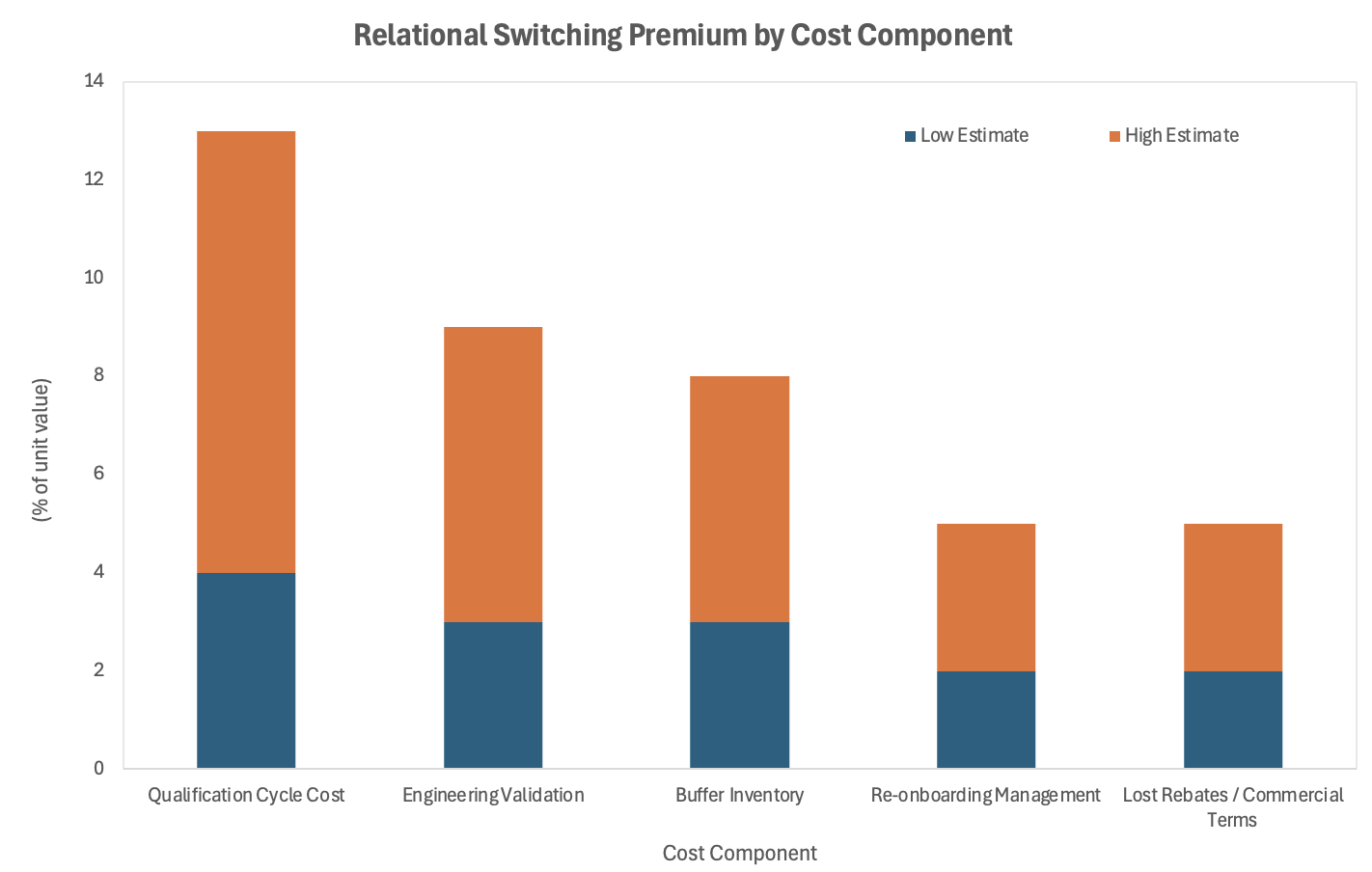

Private equity buyers conducting due diligence on manufacturing or industrial targets should treat supplier relationship quality as a balance sheet item, not a qualitative footnote. A target with three long-standing sole-source relationships and no documented loyalty risk programme is carrying hidden optionality; a target with five recently switched suppliers and a procurement team that benchmarks annually is carrying hidden liability. Neither shows up in the information memorandum. The chart below illustrates the full cost stack: the switching premium aggregates to 15–25% of unit contract value across five components, none of which appears on a single invoice.

Source: LightHouse Advisory estimates, compiled from industry due diligence frameworks (2025–2026)

Near-Term Catalysts and Policy Outlook

The next 12 months represent a period of asymmetric downside: the costs of relational deterioration are nearer than the benefits of new relationship formation, and policy is accelerating rather than pausing the restructuring.

The 0 to 3 month window is shaped by the US-China trade negotiation dynamic. The 90-day tariff pause announced in May 2025 created a brief arbitrage window that many buyers used to accelerate orders from Chinese suppliers, but without re-committing to those relationships. As that inventory cycle normalises through mid-2026, buyers who treated the pause as a one-time opportunity rather than a relational re-engagement will find themselves back outside the allocation priority queue. Separately, the EU's Carbon Border Adjustment Mechanism (CBAM) full implementation is tightening sourcing economics for European manufacturers relying on carbon-intensive upstream supply.[1]

The 3 to 12 month window is dominated by two dynamics. First, the US CHIPS Act domestic content verification cycle intensifies: suppliers that cannot document compliant provenance chains face disqualification from subsidised programmes, and their customers face subsidy clawback risk. Second, the CRMA processing milestones come into review in late 2026, with enforcement signals expected on member state compliance. Both create hard deadlines that convert relational risk into regulatory risk.

The scenarios from here do not distribute evenly. The base case assumes policy stasis; the upside requires political will that is not yet visible; and the downside requires only one escalation that geopolitical trends are already making more probable. Read together, they suggest that the asymmetry of risk over the next 12 months sits firmly to the downside for companies that have not yet secured their relational position — and that the window to act is narrowing faster than most boards appreciate.

Base case: Tariff levels remain elevated but stable through 2026. Companies with intact supplier relationships absorb costs better, widen the working capital gap versus relationally weak peers, and begin to show margin divergence in H2 2026 reporting. Markets reprice the relationship premium partially but with a 2 to 3 quarter lag.

Upside case: A durable US-China trade framework reduces the tariff burden and allows supply chain normalisation. Companies that maintained relationships across the disruption cycle are best placed to capture the cost benefit; those that switched are locked into higher-cost alternatives mid-cycle.

Downside case: A further escalation, triggered by Taiwan Strait tension or a breakdown in trade talks, creates acute allocation rationing across semiconductors and critical materials. Companies without priority supplier relationships face production halts. Credit stress in over-leveraged industrials with weak supplier networks materialises faster than covenant structures flag.

Conclusion

The supply chain debate has been almost entirely about geography: where to source, where to manufacture, which blocs to align with. The more consequential question is relational: who will give you allocation when it matters, and what did you do to earn it?

The structural case is that the era of frictionless switching is over. Policy, geopolitics, and capacity concentration have collectively raised the cost of disloyalty to a level that should appear on every balance sheet and every investment thesis. It does not yet. The companies and investors who close that gap first are not taking a contrarian position; they are simply reading the current structure of the market without the lag that consensus analysis typically requires.

The geopolitical overlay reinforces the direction of travel. In a world of hardening blocs, the supplier relationship is not just a commercial arrangement. It is an alignment signal. Capital flows accordingly.

References

Global Trade Magazine — Tariffs and Geopolitics Are Driving Supply Chain Shifts, but Not All CEOs Are Acting — April 2026

World Economic Forum — Navigating Trade in 2026: 5 Strategic Shifts in Business Decisions — January 2026

Thomson Reuters — The 2026 Supply Chain Challenge: Confronting Complexity and Disruption in Global Trade — February 2026

Xeneta — The Biggest Supply Chain Risks of 2026 — February 2026

Citrin Cooperman — 2026 Economic Outlook for Manufacturers and Distributors — December 2025

S&P Global Market Intelligence — Private Credit in Focus: Cross-Industry Signals From a Shifting Market — April 2026

TradeVerifyd — The Hidden Risks in Your Supply Chain and How to Uncover Them — July 2025

Wolverine LLC — 10 Essential Supply Chain Risk Mitigation Strategies for 2026 — December 2025

IMF Working Paper — The Price of De-Risking: Reshoring, Friend-Shoring, and Quality Ladders — 2024

Harvard Growth Lab — Economic Costs of Friend-Shoring — 2023

This article is for information and discussion only and does not constitute investment advice or a recommendation.