Managed Trade Is Not a Deal — It Is a Structural Tax on Capital Allocation

The agreements being signed are not liberalisation. They are discretionary controls dressed in the language of diplomacy. Institutional capital needs to price this correctly.

Why This Matters

Every bilateral "deal" since 2025 replaces a rules-based market signal with a government instruction, and government instructions can be revoked, renegotiated, or weaponised.

The cost of capital for cross-border investment has structurally risen. Most valuation models have not yet reflected this.

The reversion trade, the bet that managed trade is a phase and that multilateral rules will return, is the most dangerous consensus position in allocation today.

This Is Not Liberalisation. Stop Calling It That.

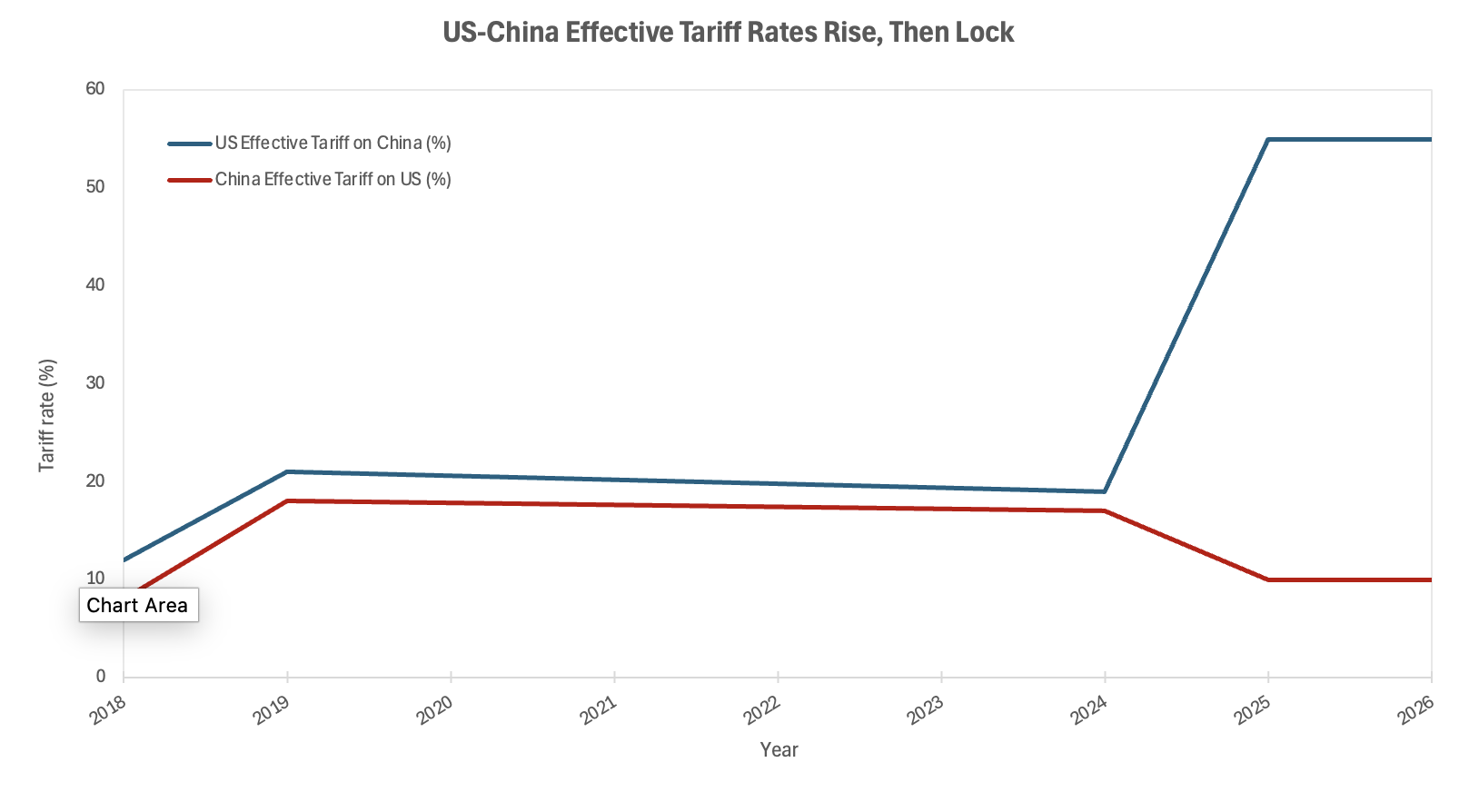

The world is in the middle of a significant repricing event, and the framing is wrong. What governments and financial media are calling "trade deals" are, in structural terms, bilateral administered arrangements: managed purchase quotas, sector-specific carve-outs, and discretionary access windows, all enforced by political will rather than treaty law. The October 2025 US-China framework is the clearest example. China committed to purchasing at least 25 million metric tonnes of US soybeans annually through 2028, to suspending retaliatory tariffs, and to halting investigations targeting US semiconductor companies. These are not tariff reductions arrived at through multilateral negotiation. They are government-to-government purchase mandates, contingent on the political relationship remaining intact.

The 2026 USTR Trade Policy Agenda makes the architecture explicit. "Managing bilateral trade with arrangements negotiated among each country's political leaders" is listed as a formal priority. The language is candid in a way that markets have not absorbed: the operating principle of the global trade system has shifted from rules to relationships. The rules-based order through the World Trade Organization (WTO) enforced predictable, legally contestable frameworks. Managed trade enforces nothing independently. Compliance is a political act, not a legal obligation.

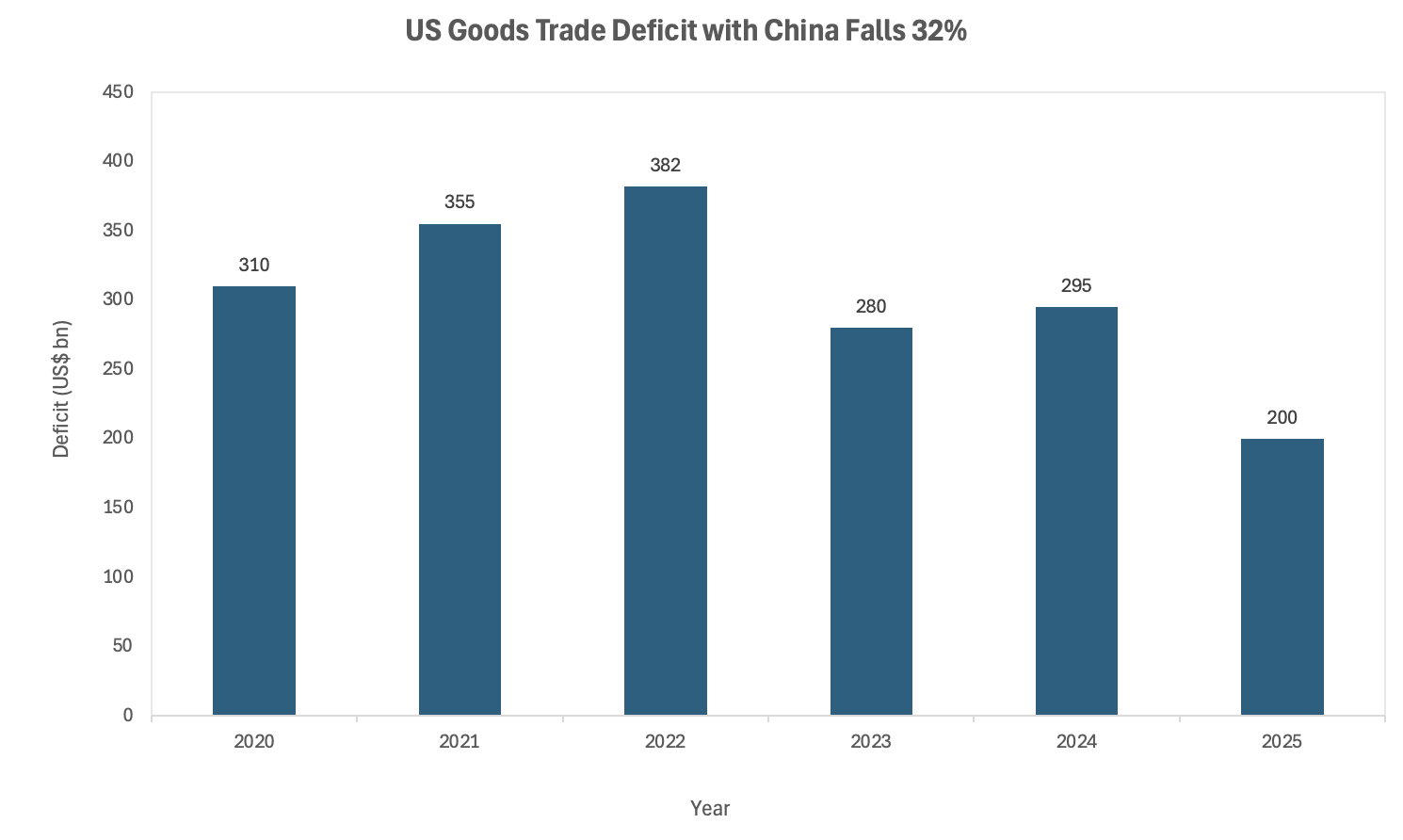

The US goods trade deficit with China fell 32% year-on-year in 2025, and for the first time since 2000 China is no longer the US's largest bilateral deficit partner. That statistic is being read as success. The more rigorous read is that it is evidence of administered adjustment, not market correction. Deficits do not fall 32% in twelve months through price signals. They fall through managed flows.

Sources: USTR; White House Fact Sheet, October 2025

Uncertainty Has Not Been Removed — It Has Been Promoted

This is the mechanism consensus has not followed to its conclusion. Free trade agreements, even imperfect ones, reduce a specific class of risk: policy discretion. Once tariff schedules are bound and dispute mechanisms are in place, companies can invest across borders against a stable regulatory baseline. Managed trade does the opposite. It makes the terms of market access a live political variable, permanently.

Consider what happened within hours of the June 2025 US-China framework announcement. China placed a six-month cap on rare earth export licences to US manufacturers. The deal was not yet signed. The leverage was already being deployed. This is not an aberration; it is the logic of the system. When access is discretionary, every party with leverage will use it. The result is that investment decisions that once required modelling tariff schedules now require modelling political relationships, leadership tenures, and summit calendars. That is a categorically different and higher-order risk.

The Trump administration's 2026 Trade Policy Agenda formalises a further layer of discretionary exposure: the Agreement on Reciprocal Trade programme, under which the US retains tariff leverage as a permanent negotiating tool even after bilateral arrangements are reached. Tariffs are not being removed; they are being held in reserve. The investment implication is that any cross-border position is now exposed, at any point, to tariff re-escalation as a political signalling tool. This is a structural change in the risk profile of globalised supply chains, not a temporary trade dispute.

The Repricing Nobody Has Invoiced

Cash flows, cost of capital, and sector valuations are all affected, and not uniformly. The primary transmission mechanism is the effective widening of the political risk premium on cross-border capital deployment, particularly in sectors where supply chains cross managed trade boundaries: semiconductors, agriculture, pharmaceuticals, critical minerals, and advanced manufacturing.

For institutional investors, three specific distortions are not yet reflected in most portfolio models. First, duration mismatch: managed trade agreements expire or are renegotiated on political cycles, typically three to four years, far shorter than the capital cycles of the infrastructure, manufacturing, and energy transition assets that depend on stable cross-border flows. Second, counterparty risk has changed in character. The counterparty in a managed trade environment is, ultimately, a government rather than a market. Government counterparties do not mark to market. Third, the US-Taiwan investment arrangements, which commit Taiwan-based firms to at least $250 billion in US semiconductor and AI production, create significant balance sheet concentrations in a geography that carries its own structural geopolitical risk.

The balance sheets absorbing the greatest friction are those of multinational manufacturers with deep China exposure and limited supply chain optionality: companies that built their cost structures on the assumption that globalisation was a one-way ratchet. That assumption is now a liability.

Sources: USTR; Bureau of Economic Analysis (BEA)

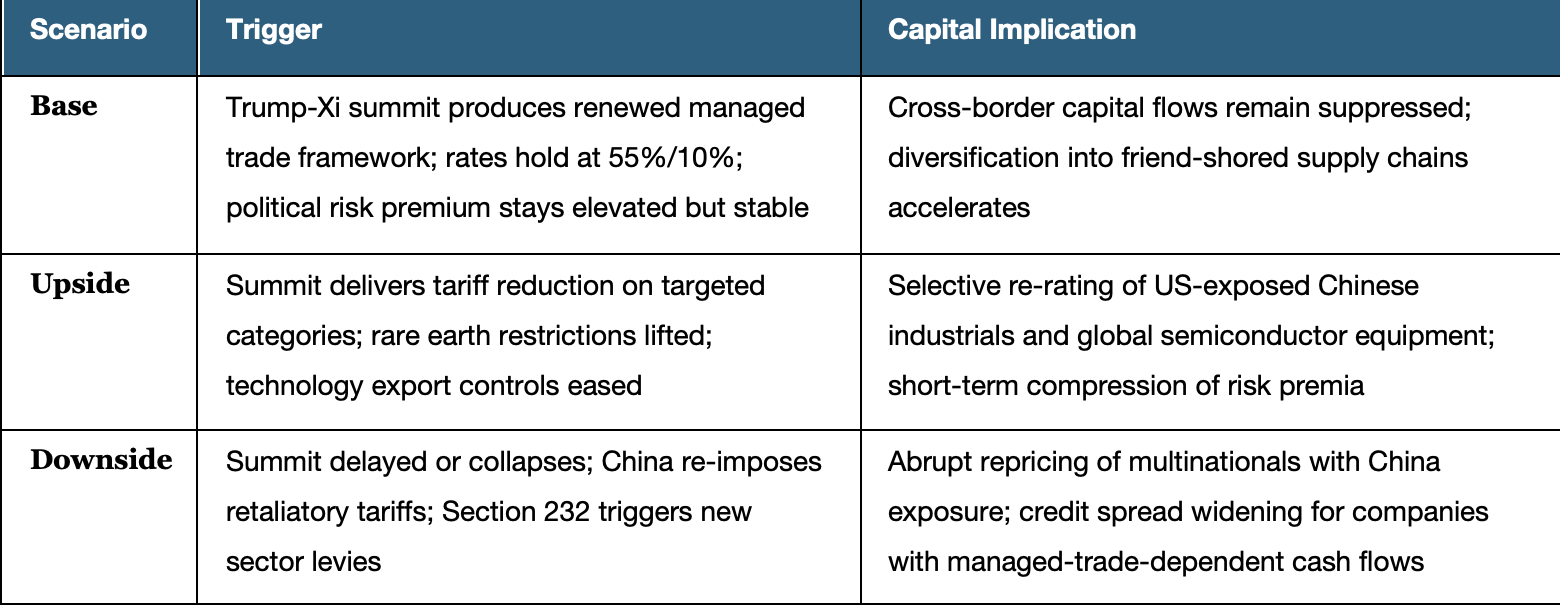

Twelve Months, Three Scenarios, One Asymmetry

The asymmetry is clear: the upside from managed trade arrangements is bounded by government discretion; the downside is not. The next twelve months will determine whether this structural repricing is gradual or abrupt.

0–3 months: The Trump-Xi summit, signalled for mid-2026, is the immediate catalyst. The market is pricing a constructive outcome. The structural case is more cautious: the Paris discussions in March 2026 produced a proposal for a formal US-China Trade Council, a mechanism that would institutionalise managed trade rather than resolve it. An institutionalised council is not a step towards liberalisation. It is a permanent administrative apparatus for discretionary control. The USMCA joint review, due July 2026, adds a second front; any renegotiation signal will widen political risk premia across North American supply chains.

3–12 months: Section 232 investigations into critical industries remain pending and could trigger new sector tariffs without warning. The rare earth export licence cap imposed by China in June 2025 runs on a six-month renewal cycle, meaning the leverage instrument is refreshed regularly. Any deterioration in the US-China political relationship, driven by Taiwan, technology export controls, or the US midterm political cycle, can convert a managed arrangement into an administered disruption within weeks.

Scenario analysis under managed trade is not the same exercise as under rules-based trade: the variables are political dispositions and summit outcomes, not supply-demand fundamentals. With that constraint acknowledged, three scenarios define where capital allocation decisions are most exposed.

Conclusion

Managed trade is not a phase in a normalisation cycle. It is the new operating system. The shift from rules to relationships as the governing principle of global trade has permanently altered the risk structure of cross-border capital allocation. The question for institutional investors is not whether multilateral rules will return: they will not, on any investment horizon that matters. The question is whether portfolios have been repriced to reflect the cost of operating in a world where market access is a political instrument.

The structural read-across is straightforward: assets with long capital cycles, cross-border supply chain dependencies, and exposure to sectors targeted by managed trade frameworks, semiconductors, agriculture, critical minerals, advanced manufacturing, carry a risk premium that most current valuations do not reflect. The geopolitical overlay sharpens this. A US administration that has made managed trade a formal policy priority, and a Chinese government that has demonstrated its willingness to use economic instruments tactically, are not moving towards convergence. They are settling into an adversarial equilibrium. Capital that has not priced this is not diversified. It is exposed.

References

White House – Fact Sheet: President Donald J. Trump Strikes Deal on Economic and Trade Relations with China – October 2025

USTR – 2026 Trade Policy Agenda and 2025 Annual Report – February 2026

South China Morning Post – Trump's 2026 Trade Agenda Sharpens Push for 'Managed' US-China Ties – March 2026

New York Times – Trump Officials Look to More Managed Approach to Trade With China – March 2026

Alston & Bird – US and China Reach a "Framework" Trade Agreement – June 2025

Morgan Lewis – US International Trade and Investment: Key Shifts in 2025 – January 2026

White House – Rebuilding America's International Trade Policy, Economic Report of the President – April 2026

New York Life Investments / Epoch – The US-China Trade War: What to Expect in 2026 – 2026

This article is for information and discussion only and does not constitute investment advice or a recommendation