What Investors Can Really Do About Climate Change

The gap between commitment and consequence has never been wider. It is time for a more honest conversation.

The investment industry has made extraordinary promises about climate change. In 2021, the Glasgow Financial Alliance for Net Zero (GFANZ) launched with over $130 trillion in committed private capital, claiming it could "deliver the estimated $100 trillion of finance needed for net zero over the next three decades." Four years on, as Professor Tom Gosling, Dr Hans-Christoph Hirt, and Dr Fernanda Gimenes document in their May 2026 LSE report "What Can Investors Do About Climate Change?", those commitments have run into fundamental limits. The theory of change underpinning the last decade of investor climate action has proved flawed. It is not that investors are irrelevant. It is that the theory of change needs to be rebuilt.

This is the starting point for a more honest, precise, and regionally differentiated conversation about what different types of investors can actually accomplish, and where the systemic gaps remain most dangerous.

Why This Matters

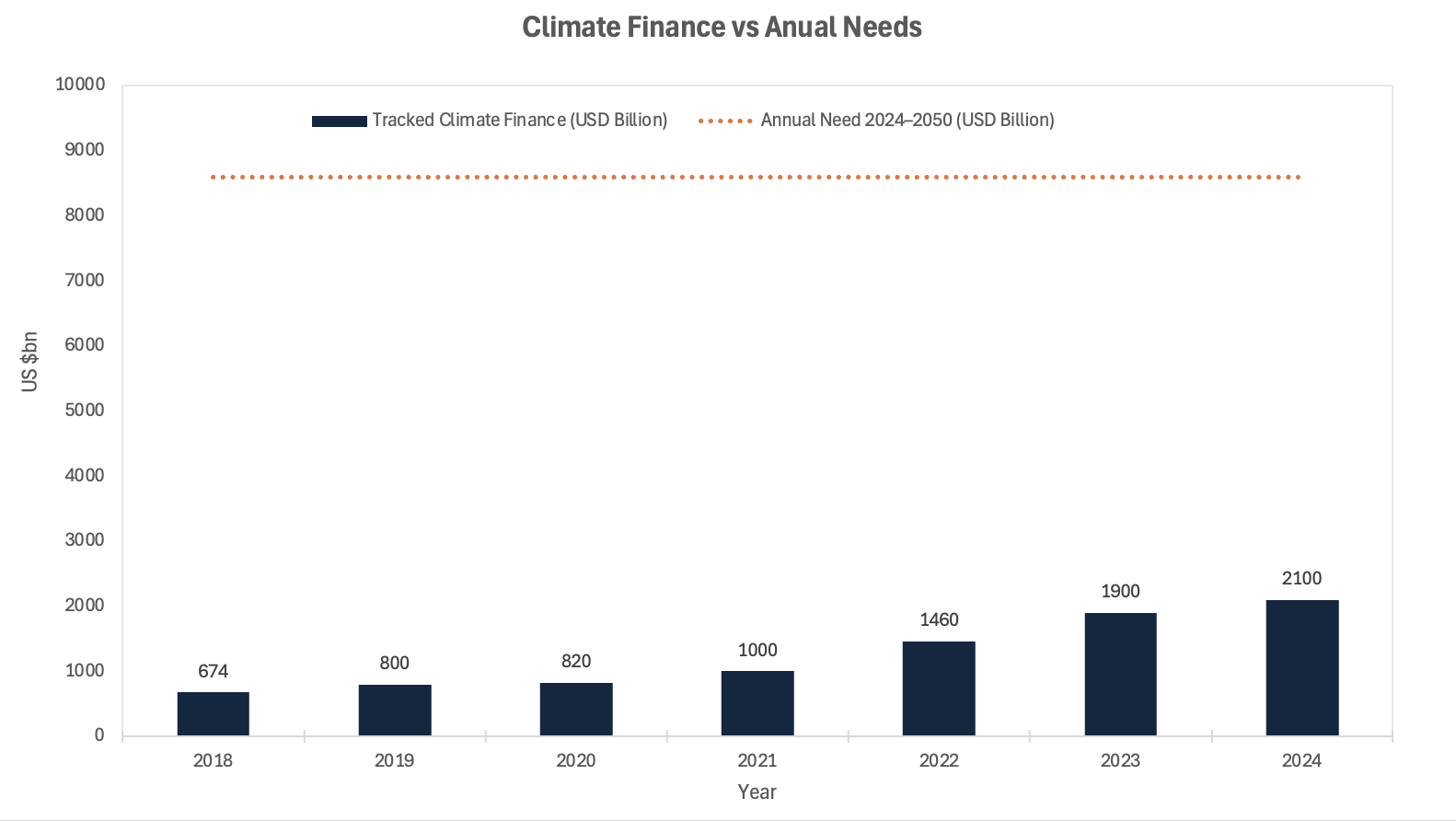

Global climate finance hit approximately $2 trillion in 2024, yet the average annual need through 2050 is $8.6 trillion: a gap that will not be closed by disclosure frameworks and net-zero pledges alone.

The LSE report, drawing on five workshops with over 60 senior representatives of asset owners and managers with USD 40–50 trillion in combined assets, concludes that "decarbonisation cannot be delivered one company at a time through investor pressure, when economic incentives point the other way."

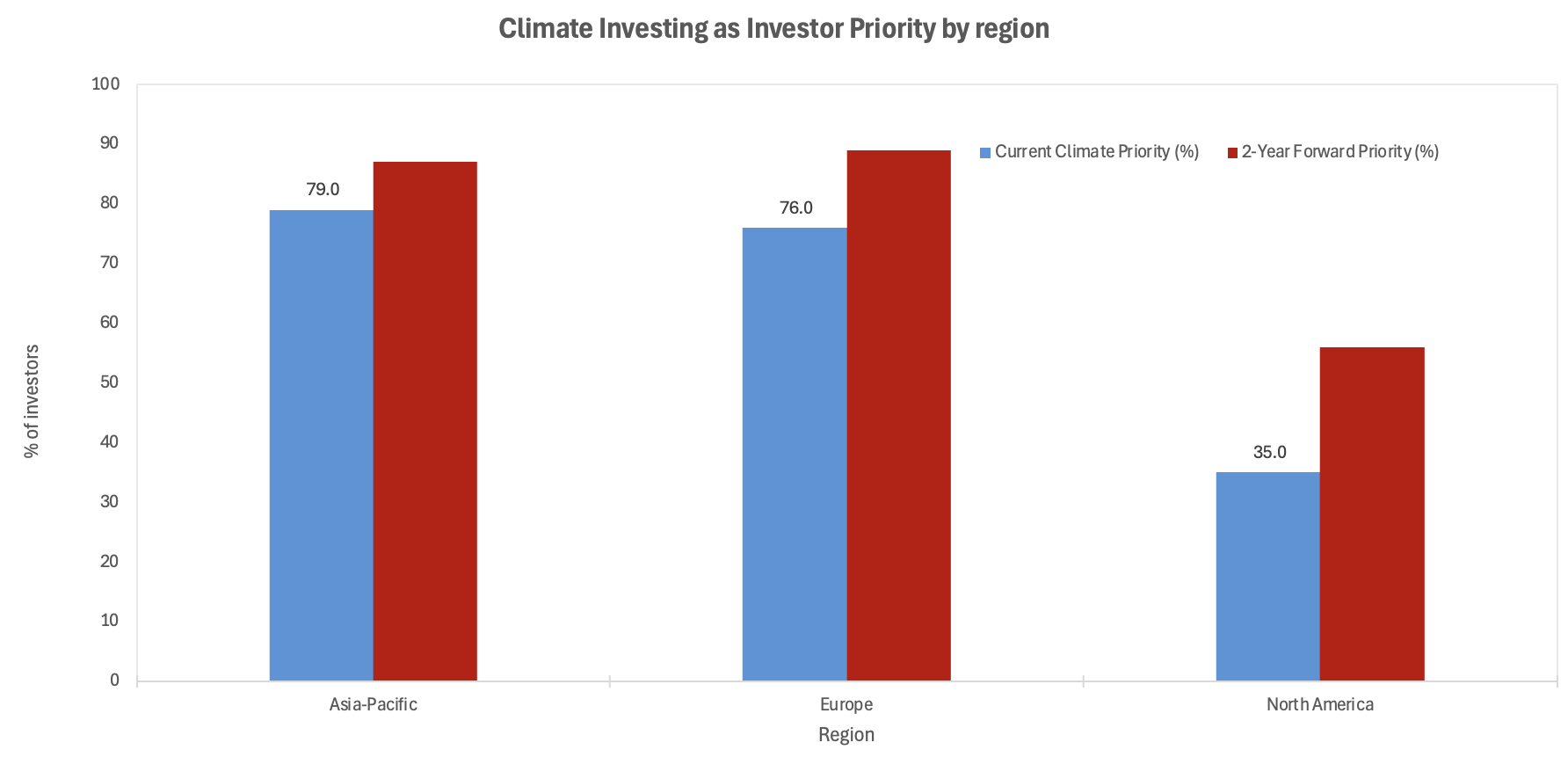

Regional divergence is accelerating. APAC investor climate commitment reached 79% in 2024, overtaking Europe for the first time, while North American commitment fell to 35%, reshaped by legal, political, and reputational risk under the Trump administration.

The Core Shift

The standard framing of investor climate action over the past decade rests on what the LSE report calls a "market-led narrative": investors, acting collectively and guided by sector pathways, could play a defining role in driving real-world emissions reduction through disclosure, corporate net-zero targets, solutions investments, and forceful stewardship including voting and divestment. This narrative has materially shaped a theory of change based on disclosure, targets, and investor-driven accountability. That theory has now run into fundamental limits.

The diagnosis offered by Gosling, Hirt, and Gimenes is carefully calibrated but uncomfortable for much of the industry. It rests on two linked observations: first, investor climate action over the past five years has been shaped by a largely top-down, market-led narrative that has overstated investor agency; second, the next phase of investor action requires a more focused and bottom-up approach, grounded in realism about where specific investors can most credibly and effectively contribute to what the authors call a "policy-led and technology-enabled transition."

Under the market-led narrative, investors were positioned as the primary driver of corporate decarbonisation. Under the policy-led narrative they propose, the role changes fundamentally: rather than trying to dictate corporate change regardless of economic incentives, investors support and enable the policy environment that is needed. Government policy and technology development are the primary determinant of decarbonisation pathways. Where policy does not align incentives with climate goals, investors cannot, on a sustained basis, force companies to act against economic reality. As Lord Nicholas Stern — whose 2025 book is cited by the report — put it: "Governments need to establish strategic and institutional frameworks that indicate clear and credible directions for the economy if investment is to flourish."

The financial arithmetic confirms the urgency of the structural problem. Global climate finance reached approximately $1.9 trillion in 2023 and crossed an estimated $2 trillion in 2024, with private sector contributions exceeding public investment for the first time. These are genuine achievements. But they represent barely one-quarter of the $8.6 trillion average annual investment the Climate Policy Initiative estimates will be required through 2050. The gap is not a rounding error.

Source: Climate Policy Initiative, Global Landscape of Climate Finance 2025. 2024 is preliminary estimate.

The Non-Obvious Mechanism

The LSE report's central argument is that the market-led narrative has not only underperformed but has actively distorted the allocation of investor attention and resource. By framing investors as the primary drivers of decarbonisation, it has led to two damaging outcomes simultaneously: greenwashing, through the adoption of metrics such as portfolio decarbonisation that create the appearance of alignment without driving real-world change; and political overreach, by pushing companies towards targets that lack credible commercial pathways.

Portfolio decarbonisation achieves the appearance of climate alignment far more easily than actual impact. An investor who rotates out of fossil fuel producers into renewable energy companies reduces their financed emissions; the oil company has simply found a new shareholder, often in less regulated, less scrutinised markets. The LSE report is direct on the displacement problem: "displacement of polluting activities from one form of ownership to another, less scrutinised form is a real concern." The counter-argument, that restricting access to public capital raises the cost of capital for high-emitters, has some empirical support, but the magnitude is small relative to what would be needed to alter investment decisions.

Stewardship and engagement is the tool workshop participants most consistently described as the "most dependable and legitimate lever available to investors." But the report introduces a concept that is crucial to understanding its limits: "limitations-aware engagement." Stewardship is most effective within the boundary of what is economically viable for a company, or when it encourages firms to expand that boundary through credible commercial framing. Attempts to force boards into uneconomic actions do not accelerate sector transitions; instead they generate competitive loss, backlash, and ultimately an over-reaction to attempted decarbonisation. As the report notes, investors can encourage boards to act within their "zone of discretion," but "forcing boards to act against their view of the company's commercial interests is not realistic."

The academic evidence on divestment reinforces this framing. A Harvard Law School governance review found that green public investors do reduce portfolio company emissions, but through engagement rather than divestment: "Engagement is better than divestment for investors that want companies to reduce carbon emissions." The Institute for Energy Economics and Financial Analysis (IEEFA) takes a more nuanced position, arguing that divestment and engagement are not a binary choice and that credible engagement requires the threat of exit to carry weight. Both positions contain truth: engagement without divestment is toothless; divestment without engagement is displacement.

The true first-order lever is policy. The LSE report is unambiguous: "of 127 investors who at the end of 2024 had published targets under the Net Zero Asset Owner Alliance (NZAOA) target-setting framework and the IIGCC Net Zero Investment Framework (NZIF), only five made any reference to public policy engagement." This is the most striking single statistic in the piece. The channel from investor voice to government decision to corporate action to real-world emissions is the one that actually works, and it receives almost no systematic resource allocation within the current net-zero frameworks.

The second-order effect that consensus has not fully traced is the interaction between corporate lobbying and investor engagement. A pension fund may engage its portfolio company on net-zero targets while that same company spends tens of millions lobbying governments to weaken the carbon pricing mechanisms that would make those targets commercially necessary. The report identifies this as a priority: investors need to examine whether companies' climate policy advocacy is aligned with their stated climate strategy, and to promote transparency on lobbying and industry association membership.

Investor and Stakeholder Implications

The LSE report's second major structural conclusion is that "asset managers will not lead the charge. Clear leadership from asset owners is needed." This reflects a persistent and structural misalignment: asset owners often frame climate change as a long-term, system-level risk to portfolio returns across decades; asset managers focus primarily on asset-level risks and opportunities over timeframes of a few years, reflecting mandate constraints, culture, and in the United States, perceived legal and political risk. Asset managers say that asset owner preferences on climate are "not well reflected in mandates," creating a persistent gap between stated expectations and day-to-day incentives.[^2]

Source: Robeco Global Climate Investing Survey 2024. APAC overtook Europe as highest priority for the first time

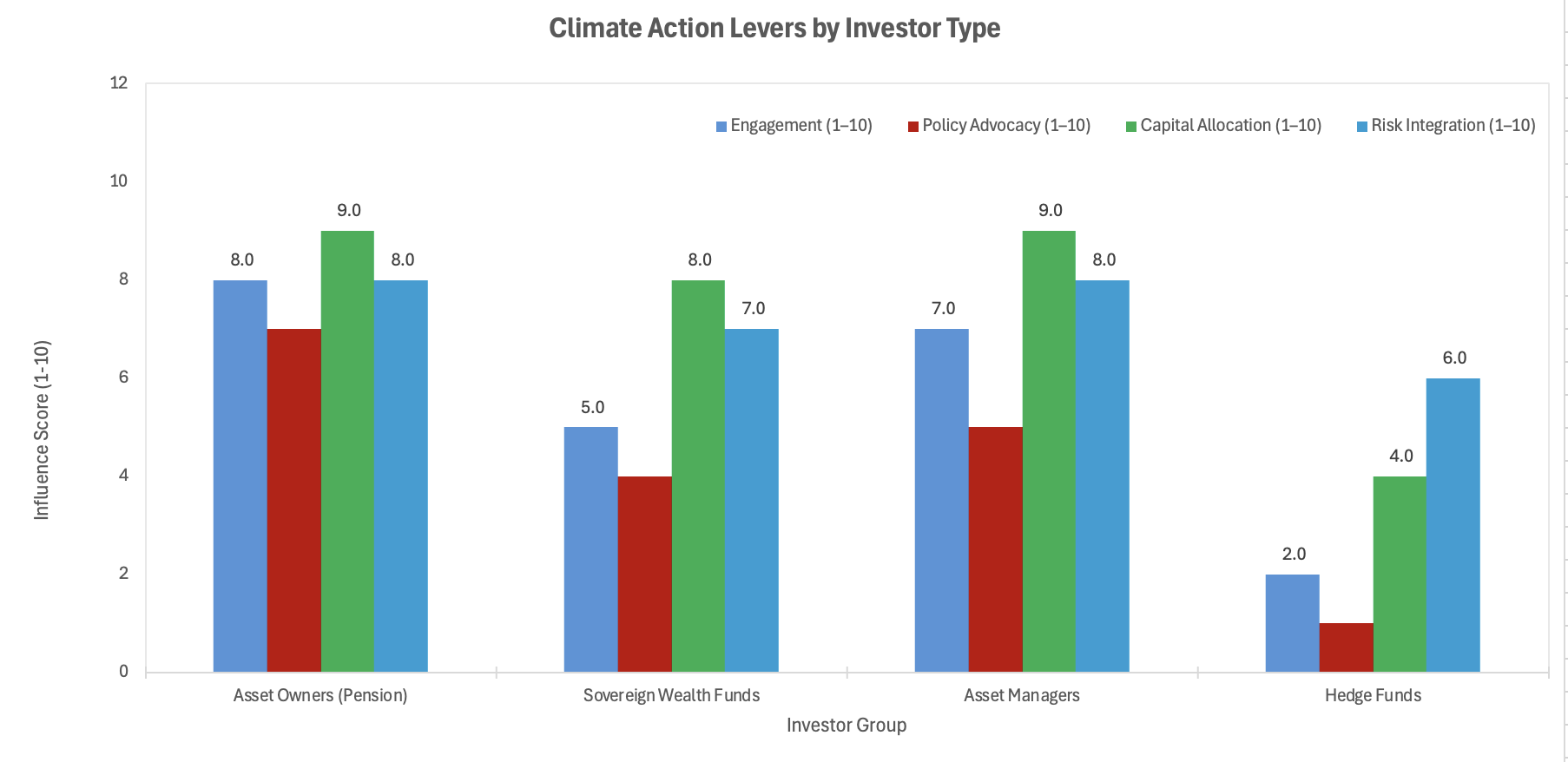

Source: Author synthesis based on LSE/ISF report, CPI, and IFSWF data. Hedge funds are systematically absent across all dimensions except risk integration.

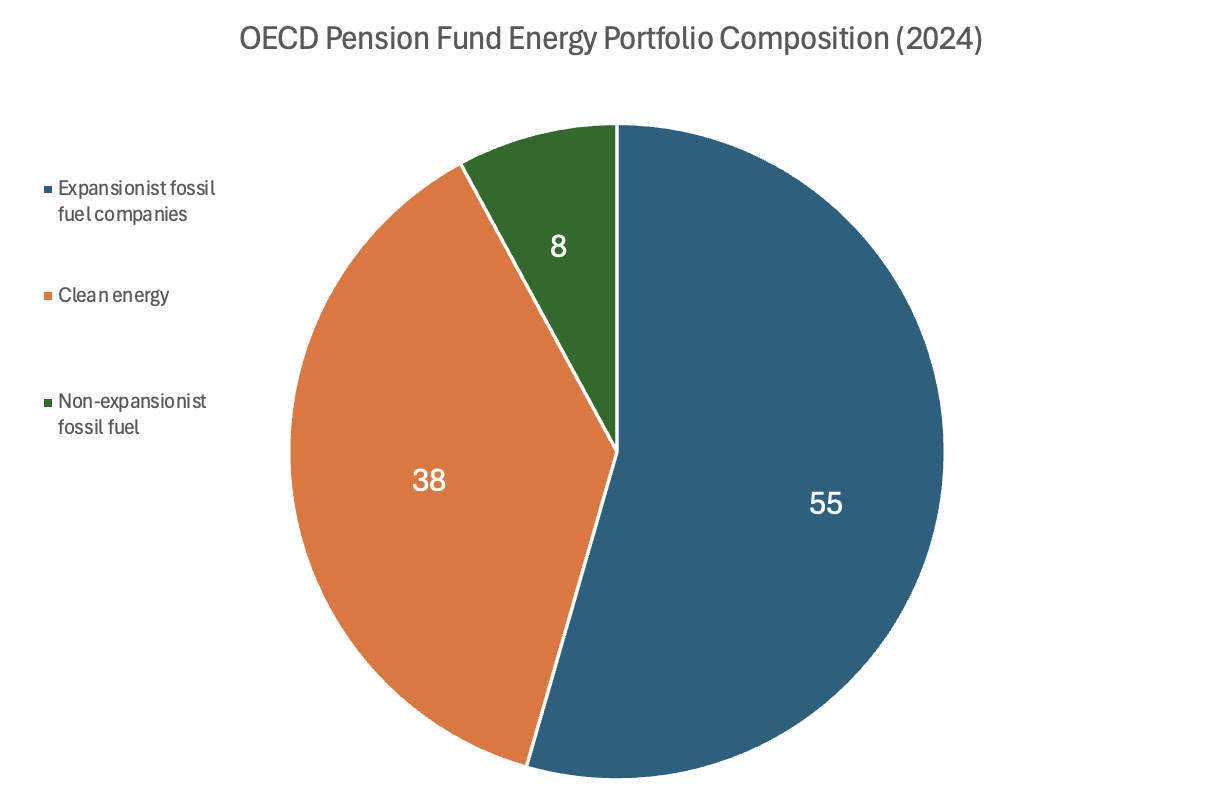

Asset owners, pension funds, and insurance companies have the clearest fiduciary mandate to act on climate and the longest time horizons. The Climate Policy Initiative's tracking of 594 OECD-based pension funds found they hold $22.5 trillion in assets and have made measurable progress on climate targets, yet remain materially exposed: across 96 funds analysed, 55% of energy portfolio holdings are in companies actively expanding fossil fuel operations.

Source: CPI Net Zero Finance Tracker, 96 pension funds, $310 billion in energy holdings. 55% sits in companies still planning to expand fossil fuel production

The pension fund-to-asset manager relationship is itself a climate lever that remains under-used. The LSE report is specific: asset owners need to embed climate expectations directly into mandates and make alignment an explicit selection criterion. In December 2025, BlackRock lost a EUR 5 billion Dutch equity mandate over climate misalignment, a single event that carries more weight than any number of coalition letters. Asset owners who are serious about climate action must begin making manager selection and mandate governance the primary vehicle through which their stated commitments are operationalised

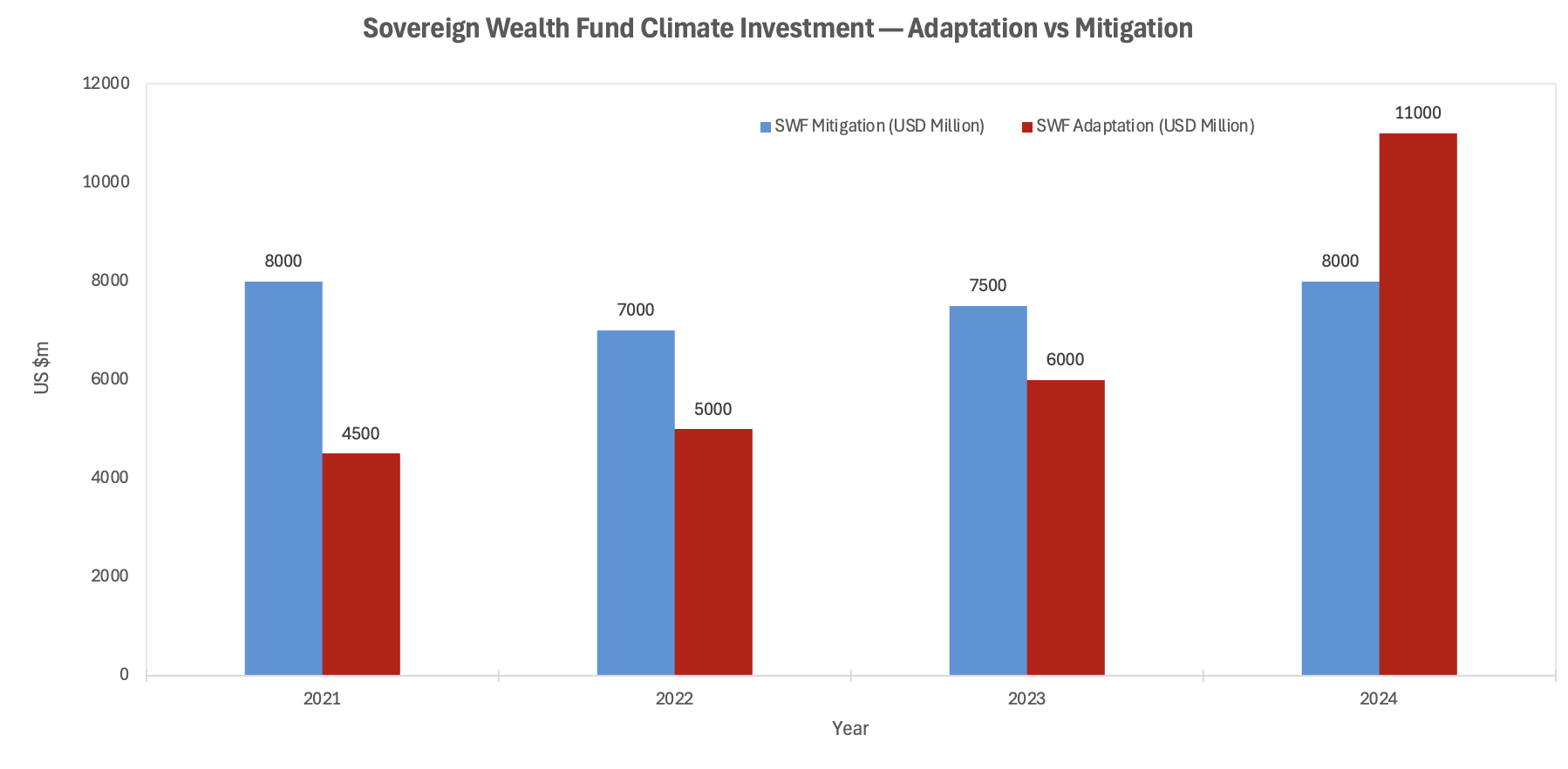

Sovereign wealth funds (SWFs) collectively manage over $12 trillion in assets and occupy a unique structural position: permanent capital with sovereign mandates, able to tolerate time horizons that conventional institutional investors cannot. In 2024, SWFs invested a record $11 billion across 79 climate-related deals, with adaptation investment ($11 billion across 24 deals) overtaking mitigation for the first time. Approximately 75% of SWFs are now integrating climate into investment decisions.

Source: IFSWF Climate Resilience Report 2025. Adaptation investment exceeded mitigation for the first time in 2024 across 79 deals.

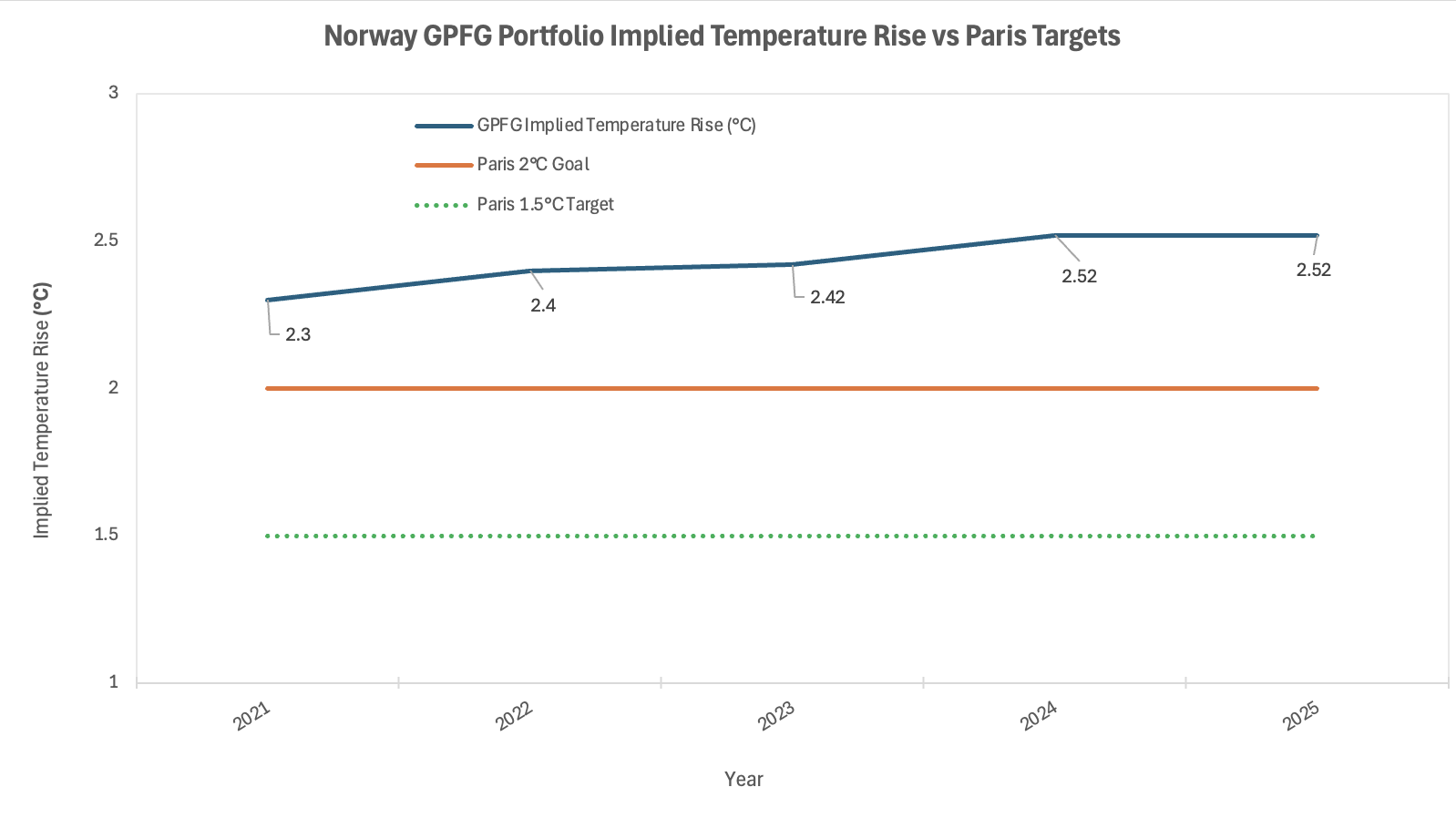

But the structural contradiction at the heart of the SWF universe remains unaddressed. Norway's Government Pension Fund Global (GPFG), with $2.2 trillion in assets and roughly 1.5% of all listed equities globally, published an ambitious 2030 Climate Action Plan and has advocated for the Science-Based Targets Initiative to allow target setting based on 2°C rather than 1.5°C alignment, explicitly referenced as a model in the LSE report. Yet environmental groups reported in May 2025 that of 23 priority climate votes, NBIM signalled disapproval of management in only three instances, and the fund's implied portfolio temperature rise stands at 2.52°C, having risen from 2.3°C in 2021.

Source: NBIM Climate Disclosures 2025. The world's largest sovereign fund is drifting further from Paris alignment, not closer.

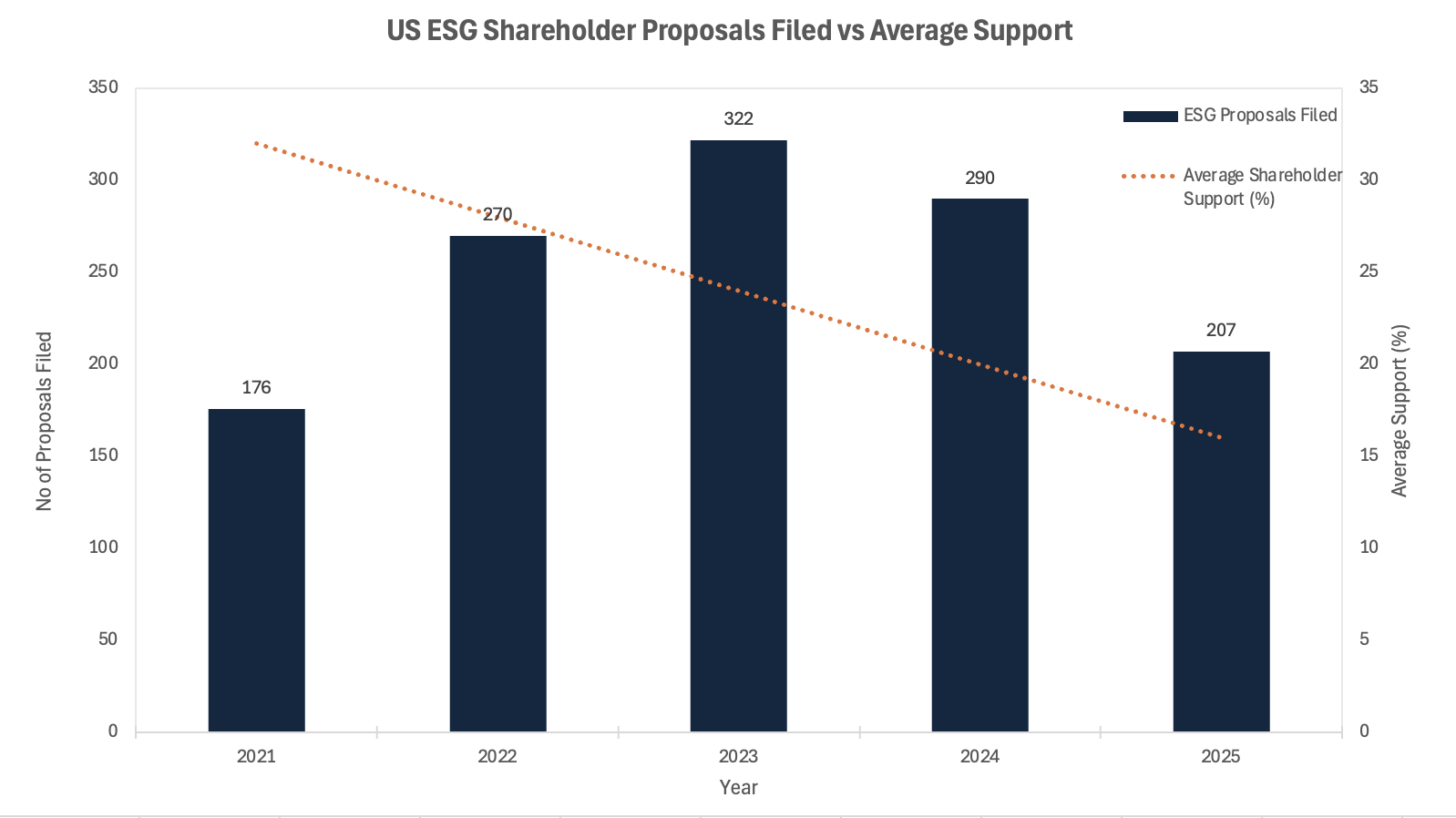

Asset managers occupy the most conflicted position in the climate architecture. The LSE report is frank: "Where their clients have diametrically opposed climate beliefs, it is not realistic for them to have firm-wide climate goals." BlackRock, with roughly $10 trillion in AUM, supported just 20 of 493 climate shareholder proposals in 2024, less than 4%, down from nearly 50% at its 2021 peak. Vanguard reviewed over 400 environmental proposals and supported none. The US Securities and Exchange Commission's February 2025 guidance reclassifying engagement at certain thresholds caused BlackRock and Vanguard to reduce company meetings by 28% and 44% respectively year-on-year.

Source: Root Intelligence and Morningstar, 2026. Anti-ESG political pressure drove average support from 32% to 16% in four years.

Hedge funds are the missing chapter. Every major review of investor climate action, including the LSE report itself, focuses on asset owners, asset managers, pension funds, and sovereign wealth funds. Hedge funds are almost entirely absent from the conversation.

The three leading multi-strategy and systematic hedge funds, Citadel (approximately $63 billion in AUM), Millennium Management, and Marshall Wace (approximately $75 billion, after returning $3.1 billion to investors in early 2025), do not operate with Environmental, Social, and Governance (ESG) mandates. Citadel's European entity explicitly states that it "does not seek to promote one or more ESG characteristics" and that "the portfolios managed do not aim at sustainable investment or reducing carbon emissions." Millennium's investor-facing materials focus exclusively on return generation and risk-adjusted performance.

This is entirely within their mandates. But the consequence is significant. Hedge funds are the most intensive users of market price signals, and their short-selling activities can accelerate or delay the market pricing of climate risk. A hedge fund that systematically shorts clean energy on the back of political headwinds, as many did profitably during the 2025 US policy reversal, creates a price signal that makes renewable capital more expensive at precisely the wrong moment. Conversely, Marshall Wace has demonstrated that a systematic ESG approach can work the other way: its Environmental Focus TOPS fund maintains a long-short strategy incorporating ESG factors, investing in stocks with strong ratings while shorting weaker-rated shares.

The more interesting question is not whether hedge funds will adopt ESG mandates, because the answer is that most will not. It is whether pension funds and other asset owners, as major allocators to alternative managers, will begin to attach climate conditions to those allocations. The LSE report notes that asset owners selecting managers aligned with their climate beliefs may be "a necessary step for investors prioritising policy influence." That logic extends to alternative allocations. To date, it has not been applied at scale.

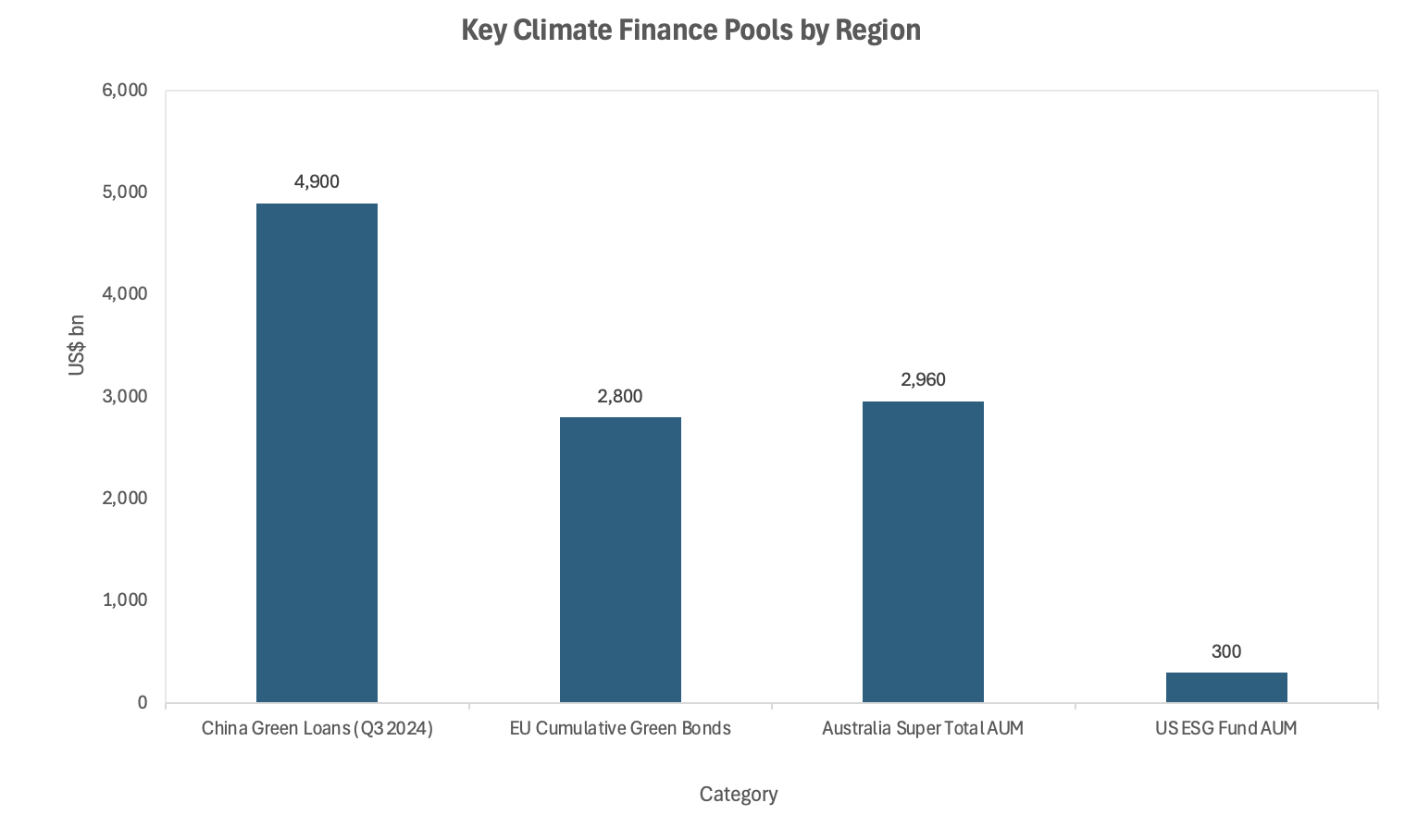

Source: PBOC/UNEPFI, Climate Bonds Initiative, ASFA, Morningstar. China's green loan book alone dwarfs the entire US ESG fund universe.

Near-Term Catalysts and Policy Outlook

The asymmetry of risks over the next twelve months is clear: political headwinds in the United States are entrenched and beginning to export to other jurisdictions, while structural demand for climate investment in APAC and Europe is accelerating on different tracks. Investors who conflate the policy cycle with the transition cycle will make the most expensive errors.

The LSE report concludes that "global to local, general to specific" is the right direction for policy advocacy: geographically local, focused on specific events such as elections, NDC revisions, and specific legislative developments; and focused in scope, around issues such as methane or deforestation, where investors have clear expertise and legitimacy.

0–3 months: COP 30 in Belém, Brazil is the critical policy moment for nationally determined contribution (NDC) revisions and the new Collective Quantified Goal on climate finance for emerging markets. Multilateral development banks (MDBs) reached a record $137 billion in climate finance in 2024, mobilising an additional $134 billion in private capital, a 33% increase year-on-year. The LSE report specifically calls on asset owners to build expertise in blended finance and emerging market and developing economy (EMDE) climate investments, noting that private capital flows to EMDEs are "at least an order of magnitude below where they need to be," despite EMDEs outside China being responsible for more than half of projected future emissions.

3–12 months: The European Union's Sustainable Finance Disclosure Regulation (SFDR) overhaul, published in November 2025, introduces a new product category architecture including an explicit "transition" category. The UK government's June 2025 announcement of its ambition to become the world's sustainable finance capital, coupled with the Transition Finance Council's sector transition planning framework, creates a near-term window for pension fund mandate reform in one of the world's largest defined-benefit markets.

The following scenarios shape the outlook. The divergence between US retreat and APAC and European advance creates a three-scenario structure that will determine capital allocation trajectories more than any single corporate engagement.

Base case: APAC maintains momentum, driven by China's 15th Five-Year Plan clean energy targets and continued green loan growth; European institutional capital flows accelerate post-SFDR reform; US engagement effectively pauses but does not reverse the underlying energy transition economics. Climate finance approaches $2.5 trillion in 2025, still well below annual need but sustaining a 20–25% compound annual growth rate.

Upside case: COP 30 delivers credible NDC revisions from key emitters, including China's commitment to wind and solar capacity at six times 2020 levels. The policy signal unlocks re-engagement by US pension funds operating under state-level sustainability mandates, offsetting the federal-level pullback. Blended finance structures supported by MDB guarantees bring private institutional capital into emerging market adaptation at scale. Climate finance reaches $3 trillion in 2025.

Downside case: US anti-ESG legislation continues to export; more pension funds in other jurisdictions face political pressure to retreat from climate commitments; the European simplification agenda weakens SFDR in ways that reduce disclosure standards without strengthening product substance; MDB commitments are not matched by private sector co-investment. Climate finance growth stalls below $2.2 trillion, and the annual gap to the $8.6 trillion need widens materially.

The most important variable in all three scenarios is not investor appetite, which surveys confirm remains broadly strong outside North America. It is policy certainty. As the LSE report observes, investors can be "a force multiplier" for effective policy, "but they cannot compensate for its absence."

Conclusion

The structural case for investor climate action is not in doubt. What is in doubt is the precision with which that action is designed, targeted, and held to account.

The LSE report by Gosling, Hirt, and Gimenes offers the clearest compass yet for climate-concerned investors who want to move from aspiration to impact. Its five practical priority areas, grounded in workshops across New York, Amsterdam, London, and Singapore with institutions managing up to $50 trillion in assets, provide a framework that is neither dismissive of investor agency nor inflated by it. The five areas are: stepping up on policy advocacy, treating it as the most influential climate tool available rather than a peripheral activity; integrating climate expectations into mandates and asset manager selection; developing genuine expertise in EMDE climate investments where capital need is greatest; building climate into the core investment process, particularly pricing physical risk and adaptation; and refocusing coalitions around specific purposes with realistic agency, rather than sprawling global accountability frameworks.

The regional picture is as divergent as any in modern finance. China's green loan book stands at $4.9 trillion, with clean energy technologies exceeding 10% of gross domestic product (GDP) for the first time in 2024. Japan's five largest institutional investors hold $40.6 billion in companies with the largest global fossil fuel expansion plans, with a clean-to-fossil ratio of 1.07:1 against the 4:1 required by 2030 under Paris. Australia's $4 trillion superannuation sector allocates less than 1% to targeted climate investment activities. In Europe, the mood from the LSE workshops reflects a recognition that "the days of unquestioning societal support for climate action are probably over, at least for now," even as the regulatory framework remains the most ambitious globally. In Asia, and particularly Singapore, participants described a "quite different" environment: "climate mitigation and adaptation are considered uncontroversial requirements for sustainable economic growth, with investors, companies, governments, and regulators seeking to work together to find pragmatic solutions."

The missing variable in the entire debate remains the hedge fund industry. Multi-strategy platforms, systematic quantitative funds, and long-short equity managers set prices, absorb information, and transmit signals through markets at a speed and scale no pension fund or sovereign wealth fund can match. Their absence from the climate accountability conversation reflects a commercial and structural reality. Progress will come not from voluntary hedge fund engagement with ESG, but from the asset owners who allocate capital to them: when a pension fund begins conditioning its alternative investment allocations on the climate risk management practices of the underlying manager, the conversation will change. The LSE report's emphasis on mandate integration as a priority lever points directly at this gap.

The four qualities Gosling, Hirt, and Gimenes identify as essential to investor climate leadership in 2026 are, in their own words, "courage, honesty, curiosity, and commitment." Of these, honesty is the most structurally important: the honest acknowledgement that investors cannot substitute for governments, that portfolio metrics are not the same as real-world emissions reductions, and that the transition is real but requires a fundamentally different theory of change from the one the industry has been operating with for the past five years.

The transition is real. The capital is increasingly available. The gap is not funding in the narrow sense. It is the policy framework that makes deployment commercially rational, the governance architecture that holds capital to account, and the intellectual honesty to distinguish between investors who are managing climate risk and investors who are managing climate optics.

References

Gosling, T., Hirt, H-C., and Gimenes, F. – What Can Investors Do About Climate Change? Workshop Feedback and Suggested Ways Forward – LSE Financial Markets Group / Initiative in Sustainable Finance – May 2026

Gosling, T. – Universal Owners and Climate Change – Journal of Financial Regulation, Vol. 11, No. 1, pp. 1–40 – 2025

Gosling, T. – A New Focus for Investor Climate Commitments – CFA Institute Research and Policy Centre – 2024

Climate Policy Initiative – Global Landscape of Climate Finance 2025 – May 2026

Climate Policy Initiative – How Big is the Net Zero Finance Gap? – November 2025

Climate Policy Initiative – State of OECD Pension Funds' Climate Transition: Insights and Recommendations – May 2026

Robeco – Global Climate Investing Survey 2025 – May 2026

IFSWF – Climate Resilience: Prioritising Adaptation in a Shifting Landscape – 2025

Norges Bank Investment Management – 2030 Climate Action Plan – October 2025

Norges Bank Investment Management – Climate and Nature Disclosures – 2025

UNEP Finance Initiative / Green Finance Development Centre – China Green Finance Status and Trends 2024–2025 – March 2025

Market Forces – Exposed: Japan's Five Largest Investors Delay Clean Energy Transition – June 2025

Root Intelligence – Five Years of US Shareholder ESG Proposals 2021–2025 – February 2026

IIGCC – EU SFDR Review – November 2025

Reuters – US Investors Back Away from Climate and Social Reforms – July 2025

Harvard Law School Forum on Corporate Governance – Divestment and Engagement: The Effect of Green Investors on Corporate Carbon Emissions – November 2023

IEEFA – Engagement and Divestment: Shareholders Transcend a False Binary – September 2024

UK Government – UK Net Zero Transition: Investor Prospectus – October 2025

Multilateral Development Banks – Joint MDB Climate Finance Report 2024 – September 2025

Asia Investor Group on Climate Change (AIGCC) – State of Net-Zero Investment in Asia – 2024

Citadel Advisors Europe Limited – TCFD Report 2024

Lord Nicholas Stern – The Growth Story of the 21st Century: The Economics and Opportunity of Climate Action – LSE Press – 2025

This article is for information and discussion only and does not constitute investment advice or a recommendation.