The Compounding Trap: Why Junior Professionals Who Ignore AI Will Fall Behind Faster Than Anyone Expects

The junior workforce is not mainly being displaced by artificial intelligence. It is being re-sorted by who learns to use it as leverage early, and who does not. The market still talks about junior professionals as if automation is the central risk. The more important shift is that artificial intelligence compresses the apprenticeship period that once forced graduates to spend years on low-value repetition before they could develop judgement. That changes who compounds fastest.

Why This Matters

Labour market: Entry-level roles in the United States are under pressure, with the World Economic Forum reporting that entry-level roles are down 35 per cent, while jobs mentioning artificial intelligence have risen sharply even as broader hiring remains weak.

Employer expectations: Gallup found that half of employed American adults now use artificial intelligence in their role at least a few times a year, with frequent use also rising, which means 2026 graduate cohorts are entering workplaces where these tools are already becoming normalised.

Career divergence: The advantage will accrue not to those who merely have access to artificial intelligence, but to those who can structure prompts, test outputs, and apply domain judgement faster than peers who still work in a pre-artificial intelligence way.

The Core Shift

The graduate entering the market in 2026 faces a different bargain from the one that existed even five years ago. Employers are hiring more selectively, overall postings remain subdued, and the share of job postings that mention artificial intelligence continues to rise across knowledge work roles. Indeed reported that jobs mentioning artificial intelligence were 134 per cent above February 2020 levels by the end of 2025, even though wider hiring conditions remained soft.

That matters because the traditional junior pathway relied on time-intensive work to build pattern recognition. First drafts, document summaries, comparables, routine reporting, and parts of scenario analysis once forced juniors through repetition. Those tasks are now increasingly compressed by co-pilot tools that can generate, summarise, and structure output at speed. In software development, researchers highlighted by MIT Sloan found that developers with access to GitHub Copilot increased time spent on core coding by 12.4 per cent and reduced project management activity by 24.9 per cent.

The structural case is not that the junior workforce disappears. It is that the learning model changes. If repetitive work is no longer the main gate through which capability is built, then the junior who learns to use artificial intelligence well can reach higher-value judgement work faster than the previous generation did.

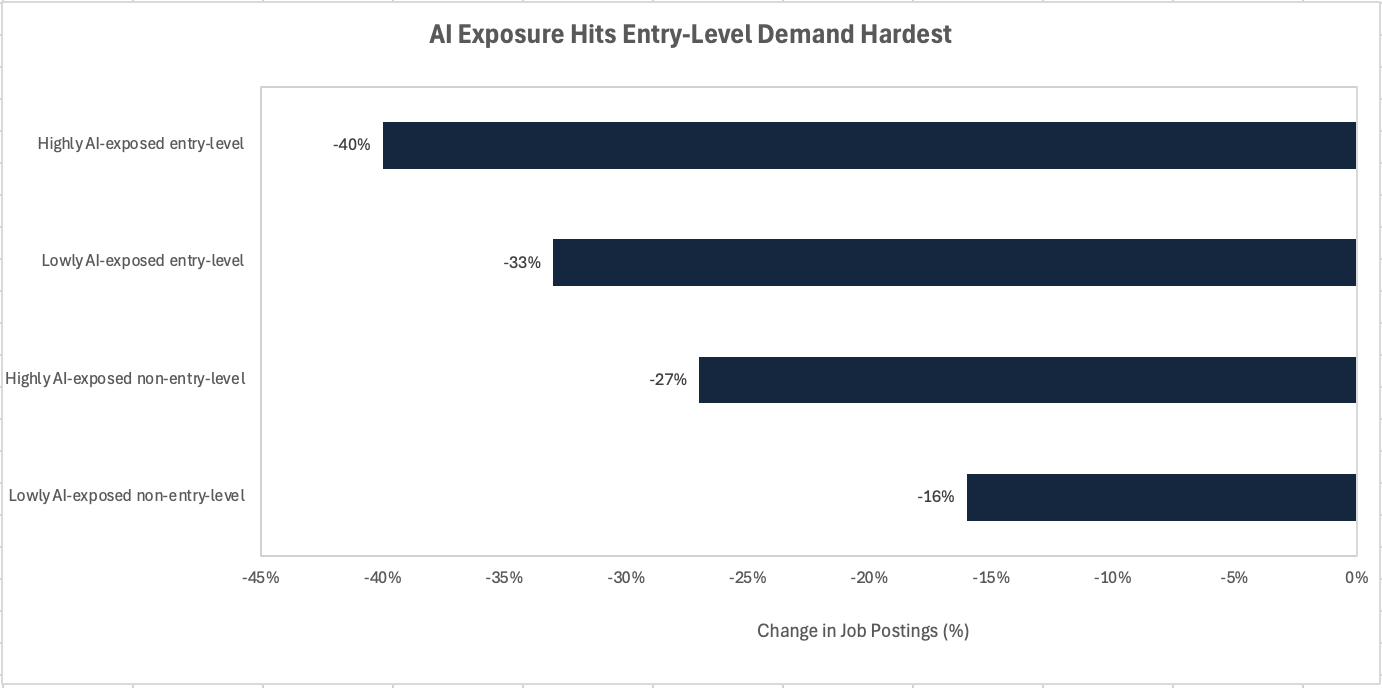

Source: Revelio Labs, August 2025. Job postings indexed to January 2023 baseline.

The Non-Obvious Mechanism

The overlooked mechanism is compounding. Artificial intelligence does not simply save time. It changes what that saved time can be reinvested into, and how quickly feedback loops tighten. A junior professional who uses these tools well can test more hypotheses, review more materials, compare more outputs, and spot errors earlier in the cycle. That is not incremental productivity. It is accelerated learning.

This is where the narrative around victimhood misses the point. A decade ago, a first-year analyst or consultant often learned through volume. Hours of grinding were a tax paid to gain exposure. Now part of that exposure can be compressed. The junior who treats artificial intelligence as a thinking partner for first drafts, structuring, synthesis, and challenge can move more quickly from execution to interpretation. The junior who refuses to engage may still graduate with the right credentials, but without the compounding edge created by tighter iteration and broader exposure.

That edge will not come from blind dependence. MIT Sloan also pointed to a potential retreat from teamwork, with developers using Copilot reducing peer collaboration substantially, which is a reminder that artificial intelligence can create brittle capability if it weakens judgement formation or social learning. The more likely read is that artificial intelligence fluency becomes a capital asset only when paired with scepticism, context, and the ability to know when the machine is wrong.

Investor and Stakeholder Implications

Employers are already re-pricing junior talent, even if many have not yet stated it plainly. If artificial intelligence raises the baseline productivity of a capable first- or second-year employee, then firms will expect more output per junior seat and may hire fewer people to do the same body of work. That changes the cash flow profile of labour-intensive professional services businesses. It can support margins for firms that redesign workflows quickly, but it can also create training gaps if they cut too deep into the cohort that would have become the next generation of mid-level operators.

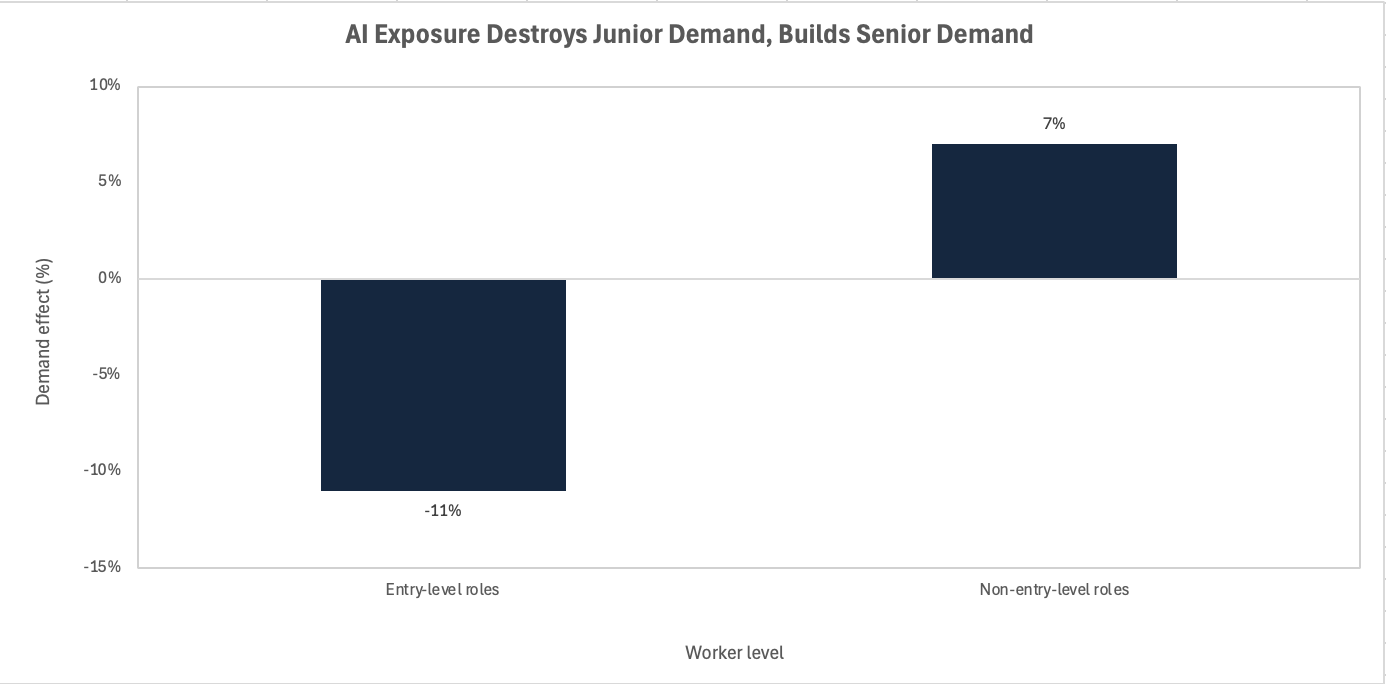

For investors, this is not a narrow human capital story. It affects revenue per employee, operating leverage, quality control risk, and ultimately the resilience of the talent pipeline. PwC’s 2025 Artificial Intelligence Jobs Barometer argued that artificial intelligence can make people more valuable even in highly automatable jobs, which supports the case for augmentation rather than simple substitution. But the Stanford Digital Economy Lab paper found substantial relative employment declines for workers aged 22 to 25 in the most artificial intelligence-exposed occupations, while older workers remained more stable. That tension matters: the firms that benefit most may be those that augment junior labour without destroying the developmental rung entirely.

Source: Revelio Labs, August 2025. Elasticity estimated from job postings data; figures represent the demand change associated with a 10 percentage point increase in the AI exposure score of a given role.

The risk not yet reflected in many narratives is balance-sheet and organisational. Large firms with strong training cultures, proprietary workflows, and brand attraction can absorb the transition. Smaller firms may gain speed from artificial intelligence but struggle to train judgement if they over-automate the bottom of the pyramid. In other words, artificial intelligence may widen performance gaps not just between workers, but between institutions.

Near-Term Catalysts and Policy Outlook

The next twelve months will widen the gap faster than consensus expects, because the downside risk sits with passive adoption while the upside sits with deliberate workflow redesign.

In the next 0–3 months, the signal to watch is hiring language. Employers are already concentrating scarce hiring on roles and skills tied to artificial intelligence, and that is likely to keep filtering into graduate recruitment criteria, assessment processes, and early-role productivity expectations. Gallup’s data on rising workplace use suggests that many teams have already crossed from experimentation into routine use.

In the 3–12 month window, the key development will be workflow normalisation inside finance, consulting, technology, and adjacent knowledge sectors. As co-pilots move from optional tools to embedded habits, the benchmark for what a junior can produce in a day will shift upward. That will increase the premium on verification, judgement, and communication, because firms will care less about who can produce a first draft and more about who can improve it, challenge it, and stand behind it.

The scenario range matters because this is not a one-directional story.

Base: Entry-level hiring remains selective, but firms increasingly prefer juniors who demonstrate artificial intelligence fluency alongside core analytical discipline. The labour market remains uneven, yet capable juniors gain more responsibility sooner.

Upside: Employers redesign apprenticeship models intelligently, using artificial intelligence to strip out low-value drudgery while preserving coaching, review, and judgement formation. In that outcome, juniors become more productive without hollowing out the pipeline.

Downside: Firms use artificial intelligence mainly to reduce headcount and raise near-term output expectations, while universities and training programmes lag. That would produce a cohort with formal qualifications but weaker real-world judgement, and a narrower path into high-quality professional careers.

Conclusion

The junior workforce is not being set up to fail by artificial intelligence alone. It is being set up to fail by a stale mental model of what early-career labour is for. The structural read-across is clear: in a world where machines compress execution, the scarce asset is not effort at the bottom of the pyramid but judgement built faster through intelligent use of tools. That is why artificial intelligence fluency should be treated as a capital asset rather than a software skill, and why the winners will be the juniors, employers, and investors who understand that the true divergence lies in compounding, not replacement.

References

World Economic Forum – How AI is changing the nature of entry level work – 2026-03-25

Gallup – Rising AI Adoption Spurs Workforce Changes – 2026-04-12

IMF – Bridging Skill Gaps for the Future: New Jobs Creation in the AI Age – 2026-01-14

PwC – AI Jobs Barometer – 2025-06-01

MIT Sloan – Generative AI changes how employees spend their time – 2026-03-09

Indeed Hiring Lab – January 2026 US Labor Market Update: Jobs Mentioning AI Are Growing Amid Broader Hiring Weakness – 2026-01-21

Ohio State University summary citing McKinsey Global Institute demand trend – 2026-01-19

Stanford Digital Economy Lab – Canaries in the Coal Mine? Six Facts about the Recent Employment Effects of AI on Young Workers – 2025-11-12

CFTE – The Age of AI Fluency: Why Professionals in Finance Can't Afford to Be Left Behind – 2025-07-07

iXperience – AI & Your Career: What Every GenZ Student Needs to Know Before Recruiting Season – 2026-04-01

This article is for information and discussion only and does not constitute investment advice or a recommendation.