From Transition Risk to Value Chain Stress — The Physical Climate Signal That Portfolio Construction Is Not Designed to Receive

Physical climate risk is not a future scenario. It is repricing assets, severing supply chains, and withdrawing insurance cover today, and most institutional portfolios are architecturally unequipped to see it.

Why This Matters

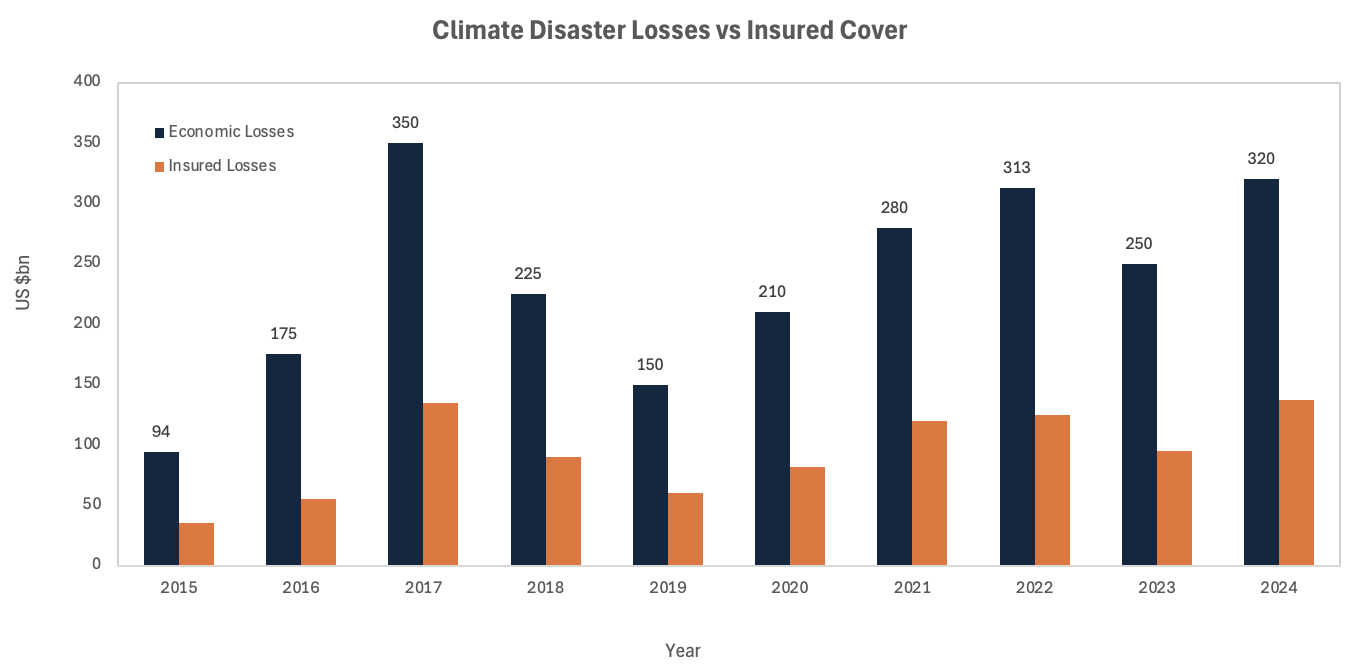

Global economic losses from climate disasters reached $320 billion in 2024, yet less than half were insured, transferring unpriced risk directly onto corporate balance sheets and, by extension, onto institutional holders

Most portfolios are built to capture transition risk through carbon metrics, leaving the slower, more structural damage from physical hazards largely unmeasured and unpriced

Physical risk travels upstream and downstream through value chains, meaning an investor's direct asset exposure materially understates total portfolio vulnerability

The Core Shift

The investment community spent a decade building frameworks for transition risk: carbon footprints, net-zero alignment scores, stranded-asset scenarios. That work was necessary. It is also, increasingly, the wrong half of the problem.

Physical climate risk, encompassing both acute shocks (floods, wildfires, hurricanes) and chronic stresses (heat, water scarcity, sea-level rise), has crossed the threshold from long-dated tail risk to near-term financial materiality. Global economic losses from natural disasters averaged roughly $200 billion annually over the prior decade; in 2024, that figure reached $320 billion, above the inflation-adjusted 10-year and 30-year averages. Aon's 2025 Climate and Catastrophe Insight places total 2024 losses at a minimum of $368 billion. The trajectory is not noise; it is a structural step-change in the frequency and severity of hazard events. The more uncomfortable read is this: even these numbers understate the problem, because the majority of physical losses sit outside the insurance perimeter, and it is those uninsured losses that flow directly into corporate earnings, credit quality, and asset valuations.

Chart: Global economic losses from climate disasters versus insured losses, 2015–2024. The persistent gap between the two bars represents risk absorbed by corporate balance sheets and, ultimately, by institutional holders. Sources: Swiss Re, Aon, S&P Global.

The Non-Obvious Mechanism

The structural problem is not that investors lack awareness of physical risk. It is that portfolio construction methodology was never designed to receive the signal.

Standard equity and fixed income frameworks aggregate exposure at the entity level: revenues, margins, leverage, and cost of capital. Physical climate hazards do not respect entity boundaries. A manufacturing company's direct operations may sit in a low-risk geography, yet its tier-two suppliers may be concentrated in flood-prone river deltas in South Asia or water-stressed regions in southern Europe. When those nodes fail, the disruption propagates through the value chain and surfaces in the holding company's earnings, not in the physical risk score of the direct asset. Supply chain disruptions cost organisations an estimated $184 billion annually, and that figure predates the acceleration in extreme weather frequency observed through 2024 and 2025. Most Fortune 500 companies are, by their own assessments, reasonably protected at the asset level; the three points of genuine exposure, confirmed by senior corporate risk officers, are supply chains, distribution channels, and the productivity costs of dangerous heat.

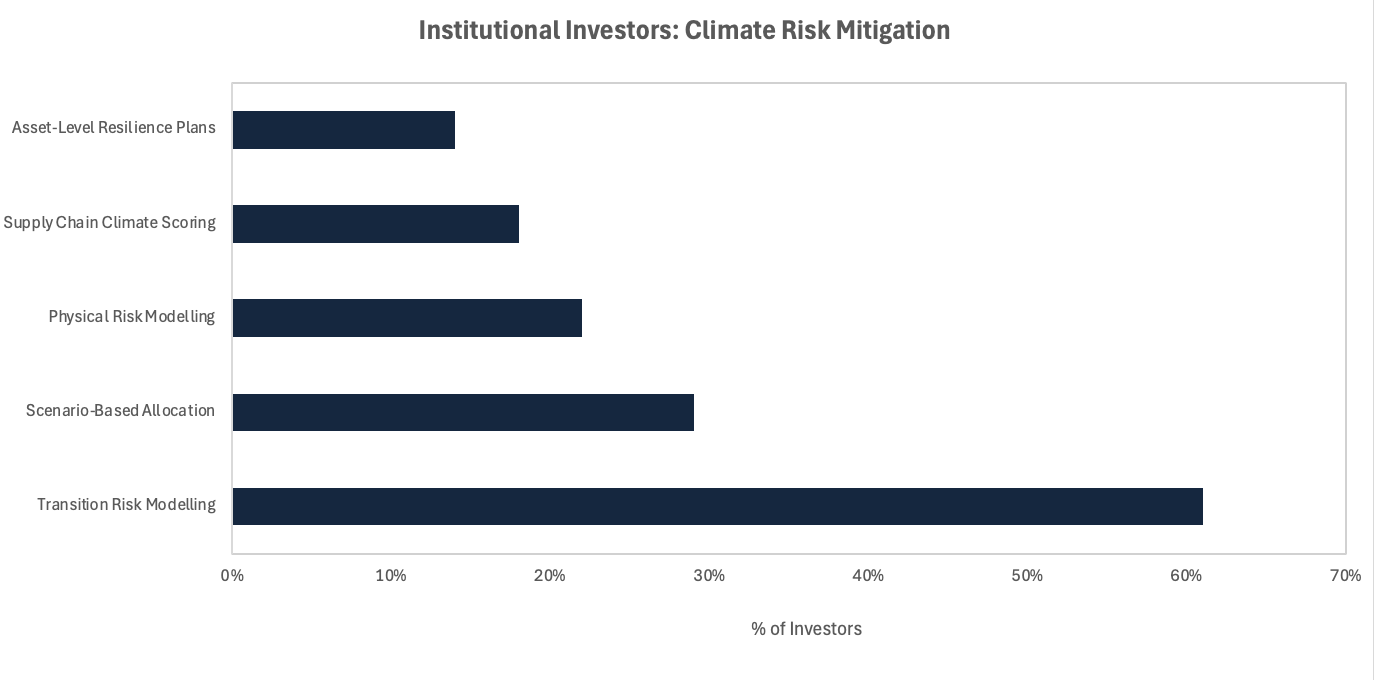

This creates a specific and underappreciated mispricing dynamic. Carbon-based metrics, the primary lens for climate risk in most institutional mandates, are designed to capture transition exposure. They say almost nothing about a company's physical vulnerability, the resilience of its supplier network, or the probability of operational disruption from a climate event. A survey of nearly 2,000 CFA professionals confirms that current valuations across asset classes do not sufficiently reflect physical climate risk. The gap is not marginal; it is structural, because the data architecture most portfolios rely on was built around emissions, not exposure.

Chart: Share of institutional investors with meaningful integration of climate risk by category. Physical risk modelling, supply chain climate scoring, and asset-level resilience planning lag transition risk integration by a wide margin. Sources: MSCI Institute, CFA Institute, IIGCC.

Investor Implications

The repricing pathway for physical climate risk is already operating through one channel: insurance. Where coverage for specific climate-related perils in high-risk regions is being withdrawn or priced at prohibitive levels, risk transfers back to asset owners and operators. This is not a theoretical future state; it is happening now in coastal real estate, agricultural land, and infrastructure assets in wildfire-exposed geographies. The insurance market, in effect, is running a continuous physical risk assessment that the equity market is not yet consistently pricing in.

For institutional investors, the implications cut across several dimensions simultaneously. First, the cost of capital for physically exposed assets will rise as insurers reprice or exit, increasing discount rates and compressing valuations for assets where coverage gaps are material. Second, operating cash flows will become more volatile: extreme weather events introduce episodic disruption to revenues and supply continuity that standard cash flow models, which rely on stable operating assumptions, will consistently underestimate. Third, credit risk in fixed income portfolios concentrated in climate-exposed geographies, including sovereign debt from climate-vulnerable emerging markets, carries physical risk loadings that credit rating methodologies are only beginning to incorporate. The balance sheets that will absorb this risk are those of the asset owners and the companies they hold, not the intermediaries.

Institutional investors overseeing more than $1.5 trillion are now explicitly signalling that meaningful climate risk integration is an expectation, with direct implications for mandate allocation and manager evaluation. This creates a governance imperative: boards and investment committees that have approved net-zero transition plans without a parallel physical risk framework have addressed the more tractable half of the problem and left the more immediate half unmanaged.

Near-Term Catalysts and Policy Outlook

The next twelve months carry an asymmetric risk profile: the downside from physical shocks arriving faster than portfolio frameworks can adapt is larger than the upside from any near-term policy tailwind.

0–3 month window: Regulatory pressure on physical risk disclosure is intensifying. The International Sustainability Standards Board (ISBS) framework, adopted in a growing number of jurisdictions, requires companies to disclose material physical risks at the asset level. As reporting cycles progress through 2026, institutional investors will receive the first cohort of standardised physical risk disclosures, creating an early basis for cross-portfolio comparison. The practical utility will vary significantly by quality of underlying data, but the direction is unambiguous.

3–12 month window: Insurance market behaviour in the United States, Australia, and parts of Southern Europe will serve as a leading indicator of where physical risk is being recognised at price. As renewals in 2026 reflect updated hazard models, gaps in coverage will become visible in corporate filings, triggering the first wave of equity repricing in directly exposed sectors. Infrastructure, real estate investment trusts (REITs), and agriculture are the highest-conviction exposure points. The more structural question is whether those repricing signals will be isolated to directly held assets or will begin propagating through supply chain exposure into sectors that currently carry no physical risk premium in their valuations.

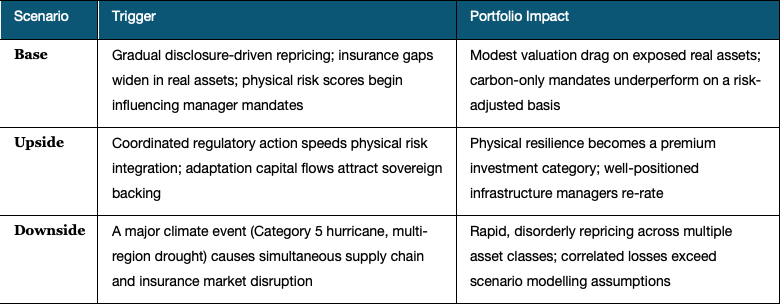

The following scenarios frame the range of outcomes over the next 12 months:

Conclusion

The structural case for rebalancing institutional climate risk frameworks away from an emissions-first model and towards a dual-lens approach, capturing both transition and physical exposure, is now beyond debate. The more important question is sequencing: which physical risks are already material to current holdings, and which are not yet priced? The honest answer is that most portfolios do not know, because the analytical infrastructure does not exist within them.

The geopolitical overlay adds a further complication. Physical climate stress concentrates in the Global South, where institutional capital has meaningful emerging market exposure through sovereign and corporate bonds. The interaction between physical vulnerability, fiscal capacity to adapt, and political stability creates a risk cluster that standard country-risk frameworks do not adequately capture. The investors who will navigate this most effectively are those who treat physical risk not as an ESG overlay but as a fundamental input to cash flow, cost of capital, and balance sheet resilience analysis, applied with the same rigour as any other structural shift in the investment environment.

References

Aon – 2025 Climate and Catastrophe Insight – 2025

S&P Global Ratings – Physical Climate Risks: What Can We Expect – December 2025

Swiss Re Institute – Natural Catastrophe Losses – 2024/2025

MSCI Institute – Are Companies and Investors Ready for Climate Shocks? – December 2025

IIGCC – Adaptation and Resilience: Corporate Engagement Priorities 2026 – January 2026

Mercer – Understanding Physical Climate Risks in Portfolios – December 2025

Aberdeen Investments – Why Physical Climate Risk Demands Investor Attention – December 2025

WBCSD – Physical Risk and Resilience in Value Chains – September 2025

Mitiga Solutions – Physical Climate Risk Assessment: Key Considerations for Asset Managers – March 2026

Ortec Finance – Beware How Financial Markets Are Pricing in Climate Risk – May 2026

J.S. Held – Global Supply Chain Disruptions and Risks: 2025 Global Risk Report – February 2025

CFA Institute – Survey on Climate Risk and Valuations – 2025

IGCC – Physical Climate Risk Assessments of Infrastructure Assets – June 2025

This article is for information and discussion only and does not constitute investment advice or a recommendation.