Nuclear Is the Quiet Winner Nobody Is Pricing Into Their Portfolio

The energy transition's defining trade is not solar or storage; it is the asset class that policy banned, analysts ignored, and markets have yet to price correctly.

Nuclear power is undergoing the most significant structural re-rating since the post-Chernobyl era of decommissioning, but in reverse. Policy reversals across three continents, an artificial intelligence (AI)-driven surge in baseload power demand, and a uranium supply chain structurally incapable of meeting 2030 requirements have converged simultaneously. Yet institutional capital remains underweight the entire nuclear complex, and most portfolio models still treat nuclear exposure as a commodity hedge rather than a structural infrastructure position. That mispricing will not persist.

Why This Matters

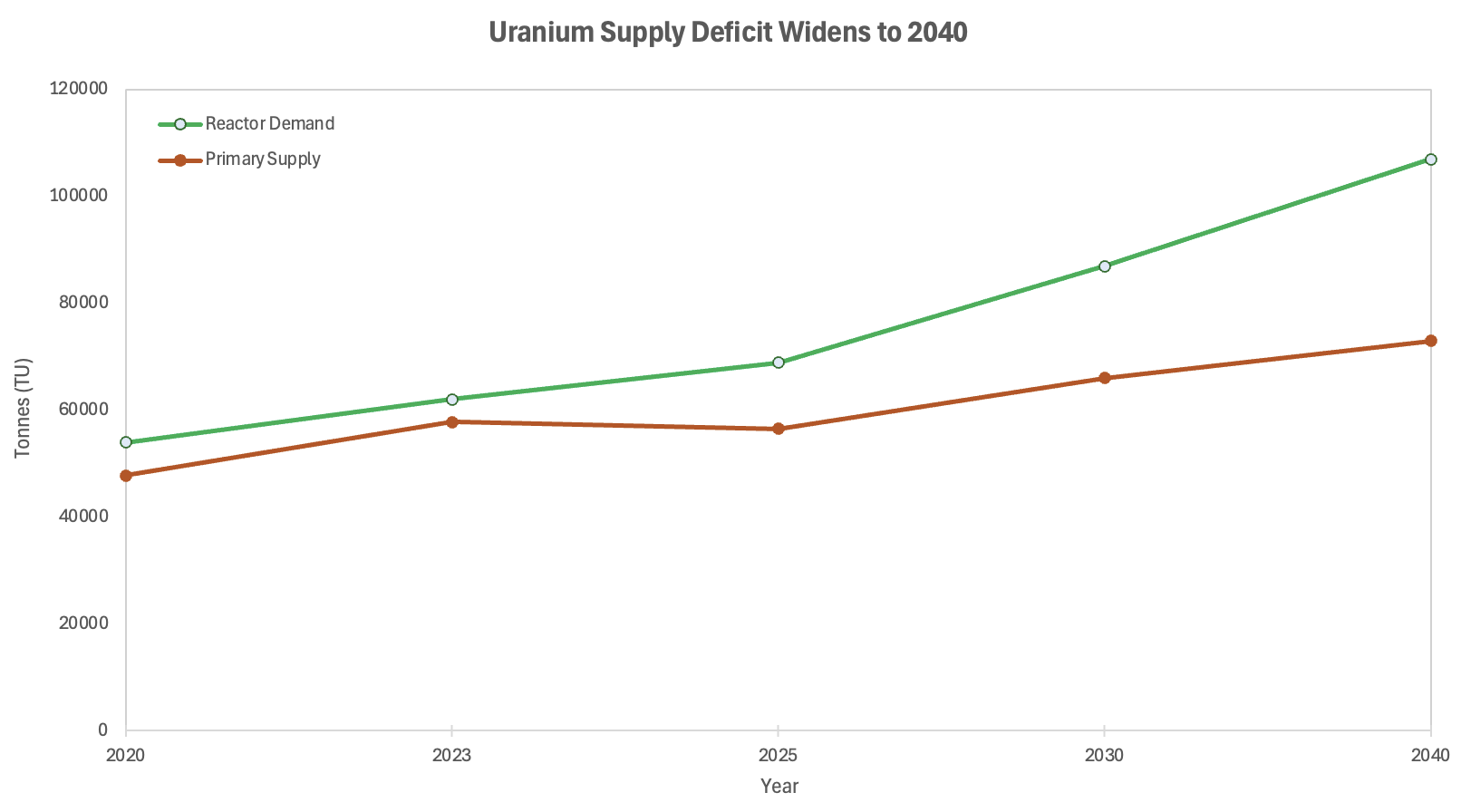

Supply shortfall is structural, not cyclical: demand is projected to reach 107,000 tonnes of uranium by 2040, against primary supply running at roughly 50% of replacement rate today

Equity upside is mis-located: the market is treating nuclear as a utility re-rating, but real value is concentrated in mid-chain scarcity: enrichment capacity, fuel fabrication and specialised engineering, none of which can be scaled in under a decade

Allocation window is compressing: long-term utility offtake contracts are being signed now; once locked in, spot and contract markets decouple, and late entrants pay a structurally higher cost of entry

The Core Shift

The global nuclear consensus broke in one direction for thirty years after Chernobyl and, more sharply, after Fukushima in 2011. Germany accelerated its exit; Belgium, Spain and Switzerland legislated phase-outs; capital dried up and the engineering talent base eroded. That consensus has now reversed, and the reversal is structural rather than cyclical.

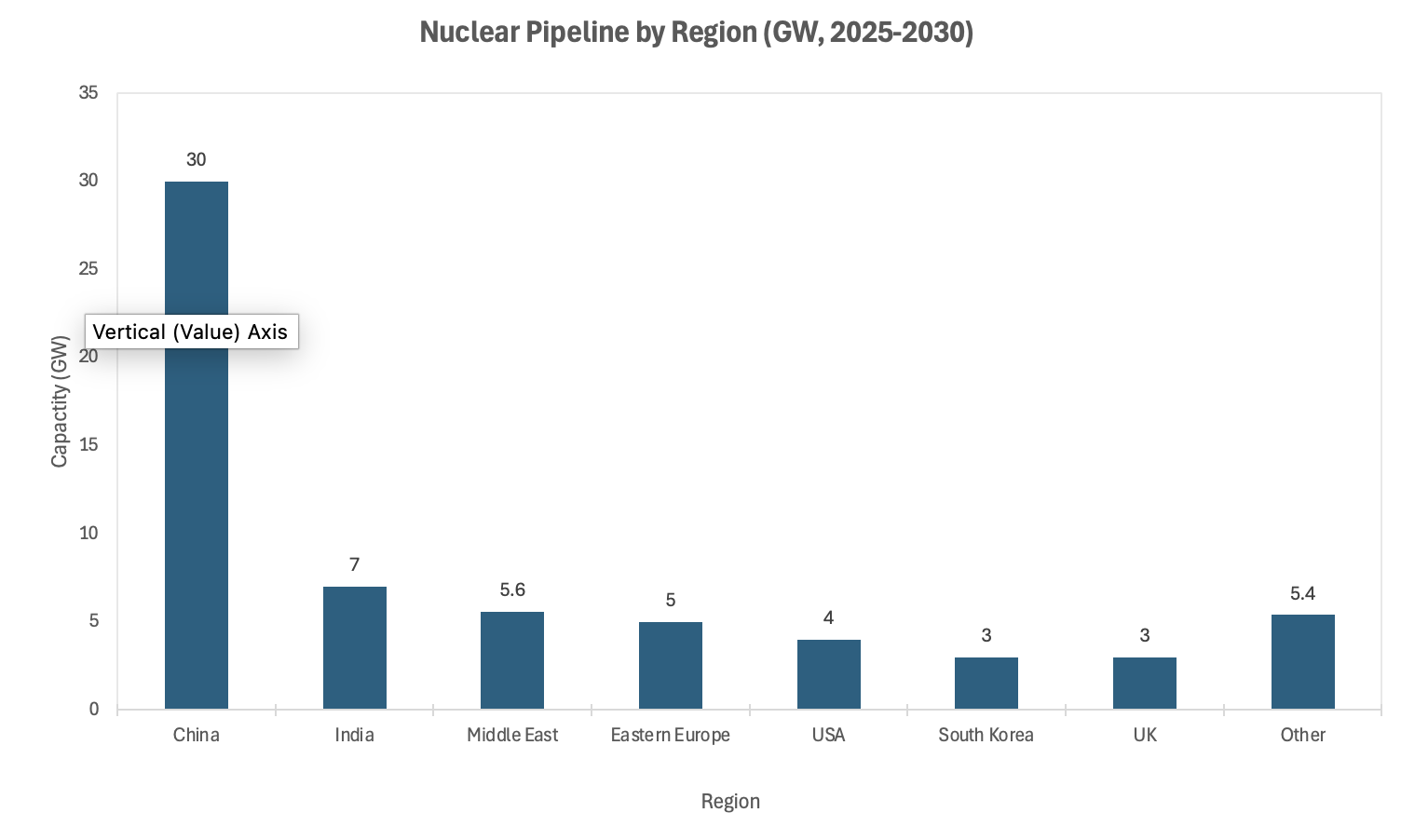

By late 2023, 22 nations signed a pledge at COP28 to triple nuclear capacity by 2050. The United States passed the Accelerating Deployment of Versatile, Advanced Nuclear for Clean Energy (ADVANCE) Act, and executive orders issued in 2025 targeted new test reactors online by mid-2026 as part of a Reactor Pilot Programme. The UK formally approved Sizewell C construction in 2026, committing approximately £26 billion to a project extending baseload capacity into the 2060s. Japan continues restarting capacity idled after Fukushima, and China's construction pipeline remains the largest in the world by volume.

The trigger is not, primarily, decarbonisation rhetoric. It is grid reliability. The AI infrastructure build-out has revealed a hard constraint: hyperscale data centres require uninterruptible, 24-hour baseload power. Wind and solar cannot provide this at scale without storage technologies that do not yet exist commercially. Nuclear is the only proven low-carbon baseload technology available today. That is a demand shift of a different order from any prior nuclear market cycle.

Source: World Nuclear Association, Sprott Asset Management, Crux Investor

The Non-Obvious Mechanism

The consensus nuclear trade is long uranium. That is correct but incomplete: it captures perhaps one layer of a multi-layer repricing. The deeper scarcity lies upstream of the reactor and downstream of the mine, in conversion, enrichment and fuel fabrication.

These are the bottlenecks that no new mine can resolve. Uranium enrichment is a capital-intensive, decade-long infrastructure commitment. Western enrichment capacity was structurally dependent on Russian supply: Rosatom's TENEX unit historically supplied approximately 35% of US enrichment services and over 40% of European utility requirements. Sanctions and supply-chain restructuring following 2022 have removed that option without replacing it. Centrus Energy in the US and Urenco in Europe are expanding, but neither can scale at the speed utilities now require.

The supply-demand arithmetic is unambiguous. The World Nuclear Association estimates 2025 uranium requirements at approximately 68,920 tonnes, rising to 107,000 tonnes by 2040 under reference-case projections. Primary mine production is running at roughly 50% of replacement rate. Kazakhstan, the world's largest producer at approximately 45% of global supply, has effectively nationalised its greenfield uranium exploration, eliminating the most prospective expansion option at precisely the moment demand is accelerating. An estimated 25-30% of 2025 utility requirements remained uncontracted as of mid-year, forcing operators into spot markets or high-priced long-term contracts.

The asset class that benefits most is not the mine. It is the enrichment facility, the fuel fabricator and the engineering house that knows how to build containment structures. None of these are currently priced as scarcity assets.

Investor Implications

For portfolio allocators, the implications cut across four capital pools.

In equities, uranium miners capture spot price upside but carry operational leverage risk and long permitting cycles. The better-positioned equity is in the industrial and engineering complex: companies with proprietary enrichment technology, specialised reactor construction capability or long-term utility service contracts. These carry lower liquidity but stronger pricing power and significantly less commodity price sensitivity in a high-rate environment.

Private credit into nuclear new-build is the most underappreciated entry point currently available. New-build nuclear is a project finance story with no real precedent in modern capital markets at scale. Construction risk, regulatory risk and long payback periods have deterred private lenders. The gap between government-backed debt at sovereign rates and fully private capital is now wide enough to be structurally interesting. Mezzanine tranches on small modular reactor (SMR) projects carry risk-adjusted yields that compare favourably to infrastructure debt in other sectors, without the rate-cycle correlation that burdens conventional infrastructure.

In commodities, uranium spot reached above US$88 per pound in January 2026, and structural constraint supports further appreciation. The more asymmetric position, however, is in enrichment-service contracts: harder to access, but offering less volatile return profiles for mandates that cannot absorb commodity-grade volatility.

The sovereign dimension is underpriced. Nations controlling enrichment capacity, fuel fabrication or large domestic uranium reserves are acquiring strategic leverage not yet reflected in sovereign credit spreads. Canada, Australia and France hold structural positions in the nuclear supply chain that will compound in value as the energy security premium rises. The International Atomic Energy Agency (IAEA) estimates annual nuclear investment must increase from $50-60 billion (the 2017-2023 average) to $125 billion to meet the most ambitious capacity targets. The capital is not yet flowing at that rate.

Source: IAEA, World Nuclear Association, IEA — 2025-2030 pipeline

Catalysts and Scenarios to 2030

Near-term catalysts are sequenced and visible. The US Department of Energy (DoE) committed to three SMRs operational at Idaho National Laboratory by July 2026. NuScale's 77 MWe design received Nuclear Regulatory Commission (NRC) standard design approval in May 2025, the first such approval in years. The EU taxonomy's inclusion of nuclear as a sustainable finance category is progressively lowering the cost of capital for European operators. Multiple US states are legislating to repeal nuclear moratoriums, with fast-track SMR permitting bills requiring regulatory decisions within 150-300 days or deemed approved.

Scenarios:

Base: SMR demonstration projects proceed 12-18 months behind initial targets; enrichment capacity expands incrementally; uranium prices stabilise at $85-100 per pound by 2028; nuclear equities re-rate modestly as regulated-infrastructure assets

Upside:AI power demand continues to outstrip grid capacity forecasts; geopolitical disruption to Kazakhstani or Russian fuel supply forces emergency contracting; uranium breaks above $120 per pound; enrichment-service contracts become sought-after institutional assets; nuclear mid-chain equities re-rate sharply

Downside: A nuclear incident triggers policy reversal in two or more Western jurisdictions; SMR commercialisation timelines slip beyond 2030; utilities slow contracting; the thesis degrades to a longer-horizon, lower-return infrastructure story

Conclusion

The non-consensus view is this: nuclear is not a climate story. It is a geopolitical infrastructure story dressed in green language to satisfy taxonomy committees.

Enrichment, fuel fabrication and specialised engineering now constitute chokepoints in Western energy security as strategically sensitive as semiconductor fabrication or rare-earth refining. Nations and corporations are beginning to price this; most portfolios are not. The trade is not simply to buy uranium because the spot price is rising. It is to position across the nuclear supply chain before the re-rating becomes consensus, at which point the asymmetry has gone.

Most models assume nuclear is a utility re-rating: slow, regulated and priced accordingly. The correct framework treats it as a critical infrastructure scarcity play operating on a ten-to-twenty year capital cycle, with geopolitical optionality that no other energy asset class currently offers. Morgan Stanley has already revised its nuclear value-chain investment estimate from $1.5 trillion to $2.2 trillion through 2050. The revision direction is instructive; the terminal number will be revised again. The window to enter at pre-consensus pricing is measured in quarters, not years.

References

World Nuclear Association – Global Uranium Requirements – 2025

Sprott Asset Management – Uranium Outlook 2026 – December 2025

Crux Investor – Critical Uranium Projects Advance as Supply Deficit Intensifies – February 2026

Morgan Stanley Research – Nuclear Renaissance Gains Momentum – August 2025

IAEA / Aspen Institute – Rethinking the Energy Transition in Europe: Nuclear Power – September 2025

US Department of Energy / MeriTalk – DoE to Launch 3 Small Nuclear Reactors by 2026 – June 2025

National Law Review – 2025 US Nuclear Energy Revival: Policy, Innovation & Investment – August 2025

Morgan Lewis – US States Continue to Generate Nuclear Legislation – August 2025

Carbon Credits – Uranium Prices 2026: Supply Crunch and Rising Demand – February 2026

This article is for information and discussion only and does not constitute investment advice or a recommendation.