Discount to Dislocation: The Mis-priced Alpha Hidden Inside SEA's Conglomerate Breakups

The Southeast Asian conglomerate discount is not being corrected through governance reform. It is being resolved through forced liquidation — and the assets being released are systematically under-priced.

Southeast Asia's family-controlled conglomerates have long sustained a control premium in domestic capital markets that international investors never fully accepted. That premium is reversing, driven not by governance improvement but by three structural forces converging simultaneously: generational succession, deepening domestic capital markets, and the operational complexity introduced by US-China decoupling. The result is a divestiture pipeline of material size: assets priced inside intrinsic value and misclassified by consensus as governance noise, rather than what they are — a structural source of entry-level mis-priced alpha.

Why This Matters

Discount depth: From 2022 to 2025, SEA conglomerates traded at an average 32% discount to sum-of-the-parts (SOTP) valuations, with individual structures showing gaps as wide as 75%. The discount is not mean-reverting through re-rating; it is crystallising into forced asset sales.

Pipeline supply: Private equity (PE)-backed carve-outs accounted for 20% of all Asia-Pacific buyouts exceeding US$100 million in 2024, with general partners (GPs) at the AVCJ Private Equity Forum 2025 identifying carve-outs as the dominant pipeline source.

Succession as trigger: Second and third-generation family heirs are less willing to manage diversified complexity inherited from the economic liberalisation era. Succession timelines, not governance reform, are the structural catalyst.

The Core Shift

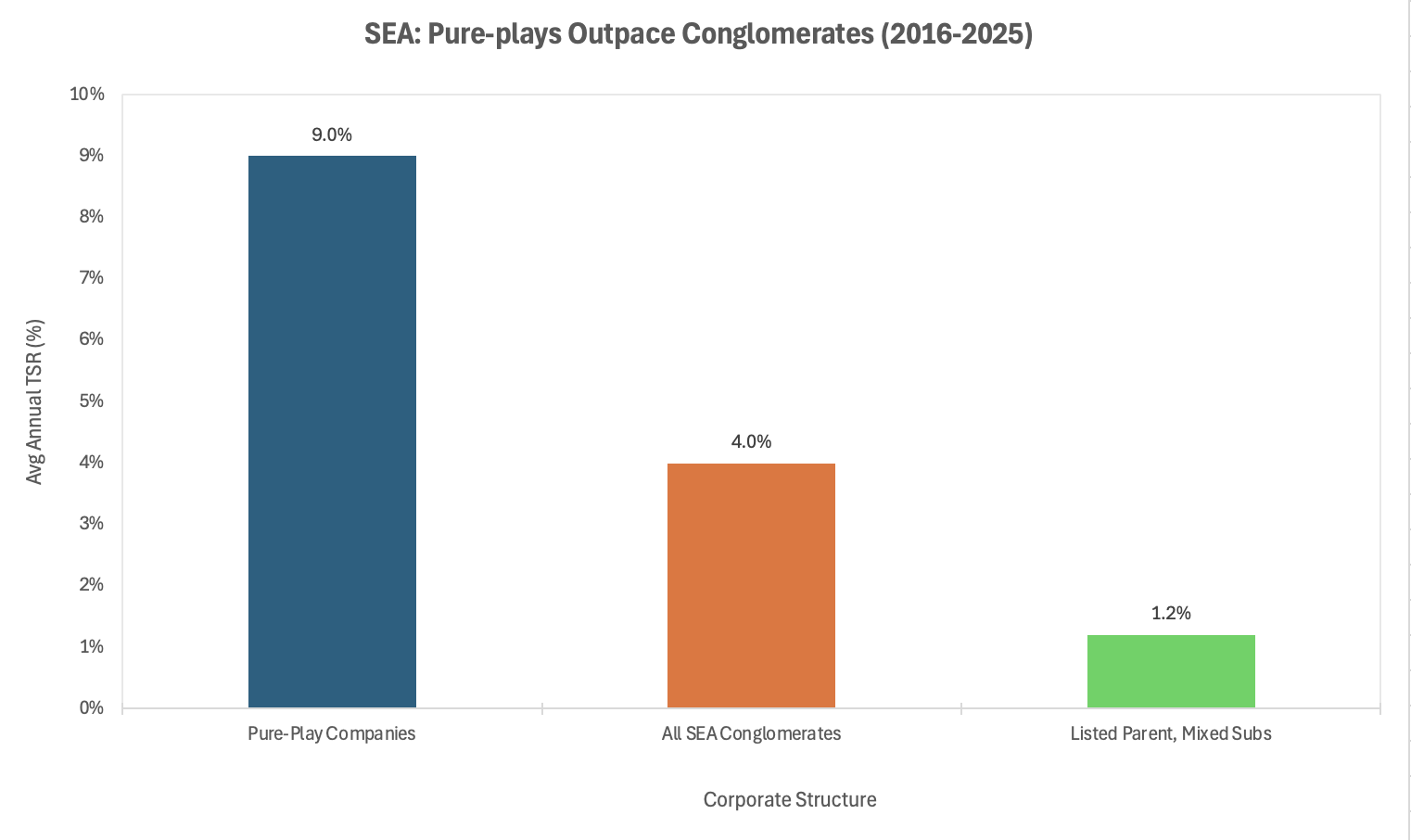

The performance gap is unambiguous. Between 2016 and 2025, SEA conglomerates delivered average annualised total shareholder returns (TSR) of 4%, trailing pure-play companies by five percentage points, according to Bain & Company's March 2026 analysis of the region's listed conglomerates. The worst-performing cohort, structures with a listed parent holding a mix of listed and unlisted subsidiaries, delivered just 1.2% annualised TSR over the same period. The discount to SOTP averaged 32% from 2022 to 2025, with individual gaps ranging from 10% to 75%.

Source: Bain & Company, March 2026

What is shifting is not the discount itself but the mechanism of its resolution. For two decades, controlling families absorbed the conglomerate discount as the cost of maintaining political connectivity, regulatory access, and capital allocation power across diversified asset bases. That calculus is now changing. Domestic capital markets across Indonesia, Malaysia, the Philippines, and Thailand have deepened sufficiently that subsidiaries can raise growth capital independently, removing the parent's role as financial intermediary. Pure-play valuations in digital infrastructure, logistics, and financial services are now high enough that separations are accretive to NAV rather than dilutive.

The Non-Obvious Mechanism

Consensus frames this as a corporate governance story: boards are improving, minority investor protections are strengthening, and regional regulators are pressing for transparency. That is a second-order effect. The first-order driver is succession.

Across the region's largest family groups, generational transitions are compressing the timeline for portfolio simplification. Founders who built diversified structures as a hedge against political risk and capital scarcity are being succeeded by heirs who are frequently more comfortable managing focused businesses. Unlike their predecessors, second and third-generation principals are less inclined to absorb operating complexity across sectors where professional management already exists. The result is not voluntary portfolio pruning driven by shareholder activism, which remains nascent in SEA, but involuntary simplification driven by the practical limits of next-generation management bandwidth.

The geopolitical overlay compounds this. Family conglomerates with material exposure to both Chinese capital sources and US-dollar-denominated revenue streams face increasing regulatory and reputational friction in a deglobalising environment. The tariff escalation of 2025 has made cross-border conglomerate structures operationally cumbersome. Apollo's Asia PE head made this explicit at AVCJ 2025: carve-outs are partly attractive because they reduce tariff risk, with counterparties being business-to-business (B2B) operators incentivised to preserve value chains — and pre-deal engagement processes now routinely run six to twelve months to ensure proprietary deal flow. This is the mechanism consensus is missing: the discount is not being corrected through re-rating. It is being resolved through asset liquidation at prices that remain inside intrinsic value.

Investor and Capital Implications

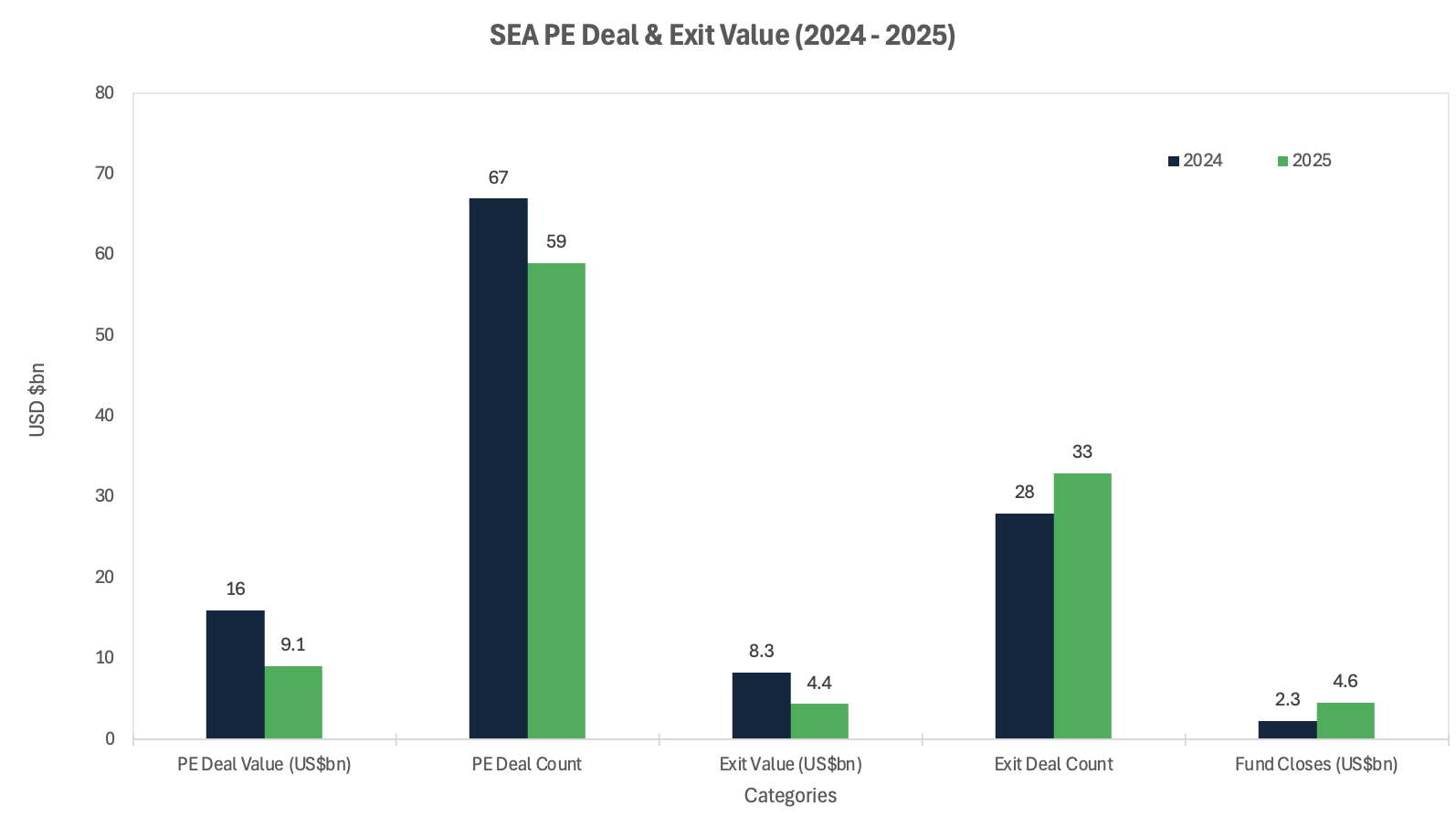

The investable implication is structurally attractive but requires early positioning. SEA PE deal value fell 43% in 2025 to US$9.1 billion across 59 deals, down from US$16 billion across 67 deals in 2024. Exit values declined 47% to US$4.4 billion across 33 transactions, even as deal volume rose 18%. The divergence between rising deal count and falling aggregate exit value signals a shift towards smaller, proprietary transactions: precisely the profile of conglomerate carve-outs reaching the market below marketed valuations.

Source: EY Southeast Asia Private Equity Pulse, February 2026

The cost of capital dynamic for separated entities is critical. A subsidiary carved out from a diversified parent and listed as a pure play typically benefits from multiple expansion relative to sector-comparable peers, and a lower equity risk premium as investors can price concentrated exposure accurately. The divesting parent absorbs restructuring costs, regulatory friction, and the loss of internal cross-subsidy in the near term: this depresses the parent's share price and creates a secondary re-entry opportunity for allocators who understand the separation mechanics. Who ultimately captures value is the decisive question. Regional sovereign wealth funds (SWFs) with patient capital — Khazanah in Malaysia, GIC and Temasek in Singapore, and Indonesia's newly established Danantara — are structurally positioned as anchor buyers in privatisations and de-listings. For international PE, the competitive dynamic is intensifying: domestic SWFs are accelerating direct deal capabilities with no return hurdles and permanent holding periods. Allocators who wait for marketed processes will be bidding against sovereign capital that can justify sub-commercial entry pricing. The alpha in this trade is proprietary, not public.

Catalysts and Policy Outlook

Several near-term triggers are identifiable. In Indonesia, Telkom signed a conditional spin-off agreement in October 2025 for its fibre infrastructure subsidiary Telkom Infrastruktur Indonesia (TIF), branded as Infranexia, at a valuation of IDR 35.79 trillion (US$2.2 billion), with the first phase of asset transfer beginning in late 2025 and completion targeted for 2026, creating a dedicated infrastructure entity with an estimated total asset value of IDR 150 trillion (US$9 billion). Danantara's establishment as Indonesia's sovereign wealth fund and the consequent restructuring of the regulatory framework for state-owned enterprises (SOEs) will generate further asset supply through 2026 and 2027.

In Malaysia, merger speculation between Sime Darby Property and SP Setia has resurfaced following Sunway's RM11 billion takeover bid for IJM Corporation, signalling that the construction and property conglomerate layer is entering a consolidation phase. In the Philippines, Capital A completed the AirAsia airline spin-off and rebranding to AirAsia Group by December 2025, consolidating airline operating certificates across Malaysia, Thailand, Indonesia, the Philippines, and Cambodia under a single listed vehicle. These transactions represent the leading edge of a region-wide simplification wave, not isolated corporate events.

Three scenarios are plausible across a twelve-to-thirty-six-month horizon.

Base: The most probable, is a moderate acceleration of divestiture activity through the second half of 2026, as Indonesian and Malaysian policy frameworks clarify and PE exit markets recover.

Upside: US Federal Reserve rate cuts reduce the cost of re-listing pure plays, accelerating separations and supporting premium exit valuations.

Downside: A prolonged geopolitical freeze in which cross-border buyers withdraw, concentrating pricing power with domestic acquirers and compressing realised valuations below intrinsic value.

Conclusion

The non-consensus assertion is this: the SEA conglomerate divestiture cycle is not a governance improvement trade. It is a structural liquidation of legacy complexity, generating a pipeline of assets carrying two layers of mis-pricing simultaneously: the SOTP discount embedded in the parent holding company, and the cyclical discount applied at the point of sale when sellers are motivated by necessity rather than optionality.

The risk that consensus has not followed to its logical conclusion is domestic SWF competition. Danantara, Khazanah, and their equivalents are not passive observers; they are accelerating direct deal infrastructure for precisely this pipeline, carrying structural advantages — permanent capital, sovereign relationships, and no return hurdles — that international allocators cannot replicate. The implication for cross-border capital is that proprietary access, established before assets reach broad distribution, is not merely preferable. It is the precondition for alpha.

Geopolitically, the unbundling of SEA's cross-border conglomerate structures is not incidental to US-China decoupling; it is a direct consequence of it. That structural force is not reversing. The divestiture pipeline will lengthen. Entry valuations will tighten as domestic capital deepens. The window for dislocation-level pricing is open now, not in three years.

References

Bain & Company – Southeast Asia Conglomerates: It's Time for Reinvention – March 2026

EY – Southeast Asia Private Equity Pulse 2025 – February 2026

Business Times Singapore – South-east Asia PE Deal Value Down 43% in 2025 – February 2026

Bain & Company – Asia-Pacific Private Equity Report 2025 – March 2025

Ion Analytics / Mergermarket – PE Must Evolve to Exploit Asia's Growing Large-Cap Buyout Market – November 2025

Marketing Interactive / Telkom Indonesia – Telkom Sets US$2.2b Spin-Off of Infranexia – March 2026

LinkedIn / Capital A – AirAsia to Spin Off Airline Business, Rebrand as AirAsia Group – October 2025

PwC Indonesia – General Legal Implications and Practical Approaches in Spin-Offs – March 2025

Business Times / Facebook – Merger Speculation Between Sime Darby Property and SP Setia – 2026

The Star Malaysia – South-East Asian Firms Fall Behind – March 2026

Disclaimer: This article is for information and discussion only and does not constitute investment advice or a recommendation.