The Brand Layer Nobody Built: Why Chinese OEM Dominance in Southeast Asia Is the Contrarian Capital Entry Point

Chinese original equipment manufacturers have taken the product; the brand sitting above it is, across most of Southeast Asia, still for sale.

Chinese manufacturers have executed one of the fastest market penetration campaigns in modern consumer history across the Association of Southeast Asian Nations (ASEAN). From white goods to electric vehicles (EVs), they now control product economics in category after category. Yet the brand premium layer — the trust infrastructure that converts commodity supply into durable consumer loyalty — remains thin, fragmented, and in most markets, privately held at distressed-to-fair valuations. That gap is not a failure of ambition. It is a structural consequence of how Chinese original equipment manufacturer (OEM) expansion works, and it will not close without capital.

Why This Matters

The real scarcity in ASEAN is not manufacturing. It is regionally credible brand equity sitting above commoditised supply chains — a scarcity that Chinese OEM penetration is actively widening, not narrowing.

United States tariff escalation, reaching a weighted average of 47.5% on Chinese goods by November 2025, is accelerating Chinese OEM production relocation into Southeast Asia, intensifying supply-side compression on local brands whilst simultaneously creating demand for regionally trusted alternatives.

Southeast Asian private capital penetration stands at just 0.5% of regional gross domestic product (GDP), against a backdrop of mid-market deal sizes averaging $267 million in 2025; the brand acquisition window is open, but not indefinitely.

The Core Shift

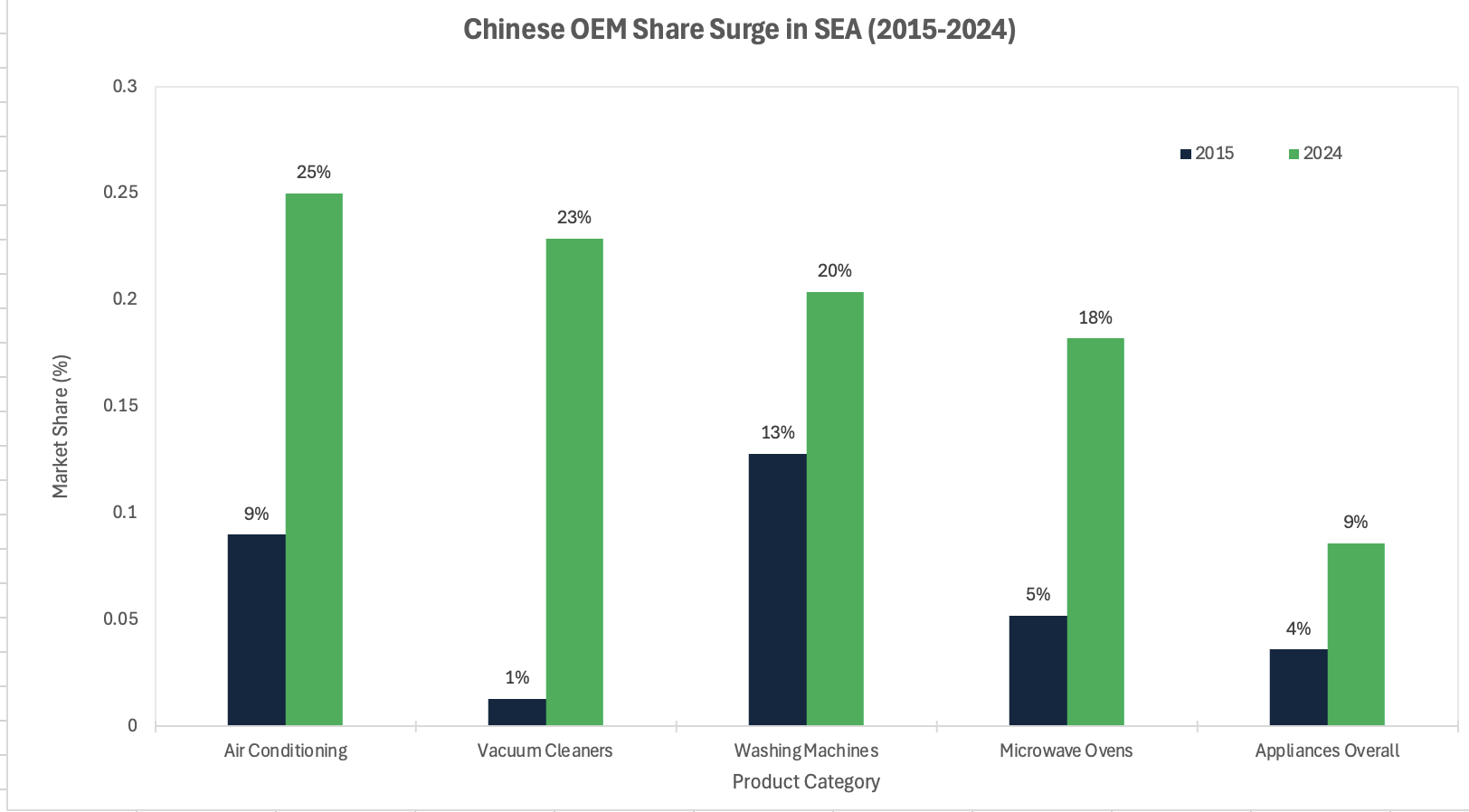

The numbers are not subtle. Chinese exports to Southeast Asia reached $587 billion in 2024, a 12% increase year on year. Across consumer appliances, Chinese brands' share of the ASEAN market grew from 3.6% in 2015 to 8.6% in 2024, according to Euromonitor International. Within specific categories the movement is more dramatic: from 1.3% to 22.9% in vacuum cleaners; from 9% to 25% in air conditioning, where Japanese manufacturers surrendered seven percentage points of share over the same period. In electric vehicles, Chinese-origin OEMs held 63% of Southeast Asian market share by the second quarter of 2025. BYD surpassed Toyota as Singapore's bestselling car brand in the first half of 2025 and captured more than half of Indonesia's EV market in the same period.

Chart 1: Chinese OEM share gains across five Southeast Asian consumer categories, 2015 vs 2024. The vacuum cleaner and air conditioning categories illustrate the speed of displacement of Japanese and South Korean incumbents

Source: Euromonitor International.

The mechanism driving this penetration is not simply price. Chinese OEMs have combined manufacturing scale, supply chain vertical integration, and aggressive e-commerce distribution to compress product costs below levels that regional manufacturers can absorb without structural change. Once a Chinese OEM achieves sufficient volume to anchor a retail channel relationship, the switching costs for distributors rise sharply. The displacement is structural, not cyclical.

The Non-Obvious Mechanism

Here is what consensus analysis consistently underweights. Chinese OEM dominance at the product and component level does not automatically translate into brand equity. It accelerates the scarcity of brand equity, because consumers navigating a commoditised product landscape increasingly allocate their trust budget to the few credible signals remaining. The scarce factor of production in ASEAN consumer markets is no longer the product itself; it is the regional identity layer above it.

This dynamic has a structural analogue. When electronics manufacturing consolidated into Taiwanese and South Korean contract manufacturers in the 1990s, it did not diminish brand value — it amplified it. Apple's margins are not a function of its factories. Brand, in a high-OEM-penetration environment, becomes the only durable source of pricing power. ASEAN is entering precisely this phase: product commoditisation is advancing faster than brand infrastructure is being built.

There is a second-order effect that capital markets are not yet pricing. Chinese OEMs relocating production into Southeast Asia — driven by US tariffs averaging 47.5% on Chinese goods as of November 2025 — are inserting themselves into regional supply chains but are not, in most cases, building ASEAN-native brand equity. They are bringing Chinese-origin brand identity into markets where origin increasingly matters, particularly among the digital-native cohorts in Thailand, Indonesia, Vietnam, and Malaysia who are active on TikTok Shop and Shopee. The brand gap above Chinese OEM supply is widening even as the supply itself scales.

Investor and Capital Implications

The entry thesis rests on three structural legs. First, the acquisition of under-capitalised regional brand platforms in personal care, apparel, consumer electronics accessories, and mobility-adjacent categories, where Chinese OEM penetration has compressed valuations without destroying consumer attachment. Second, licensing arbitrage: acquiring the distribution rights or brand licences for dormant Western and Japanese brands that retain residual equity in ASEAN markets but whose parent companies have retreated. Third, building digital-first brand infrastructure on top of existing Chinese OEM supply through private label strategies anchored by regional identity, influencer ecosystems, and direct-to-consumer (D2C) fulfilment.

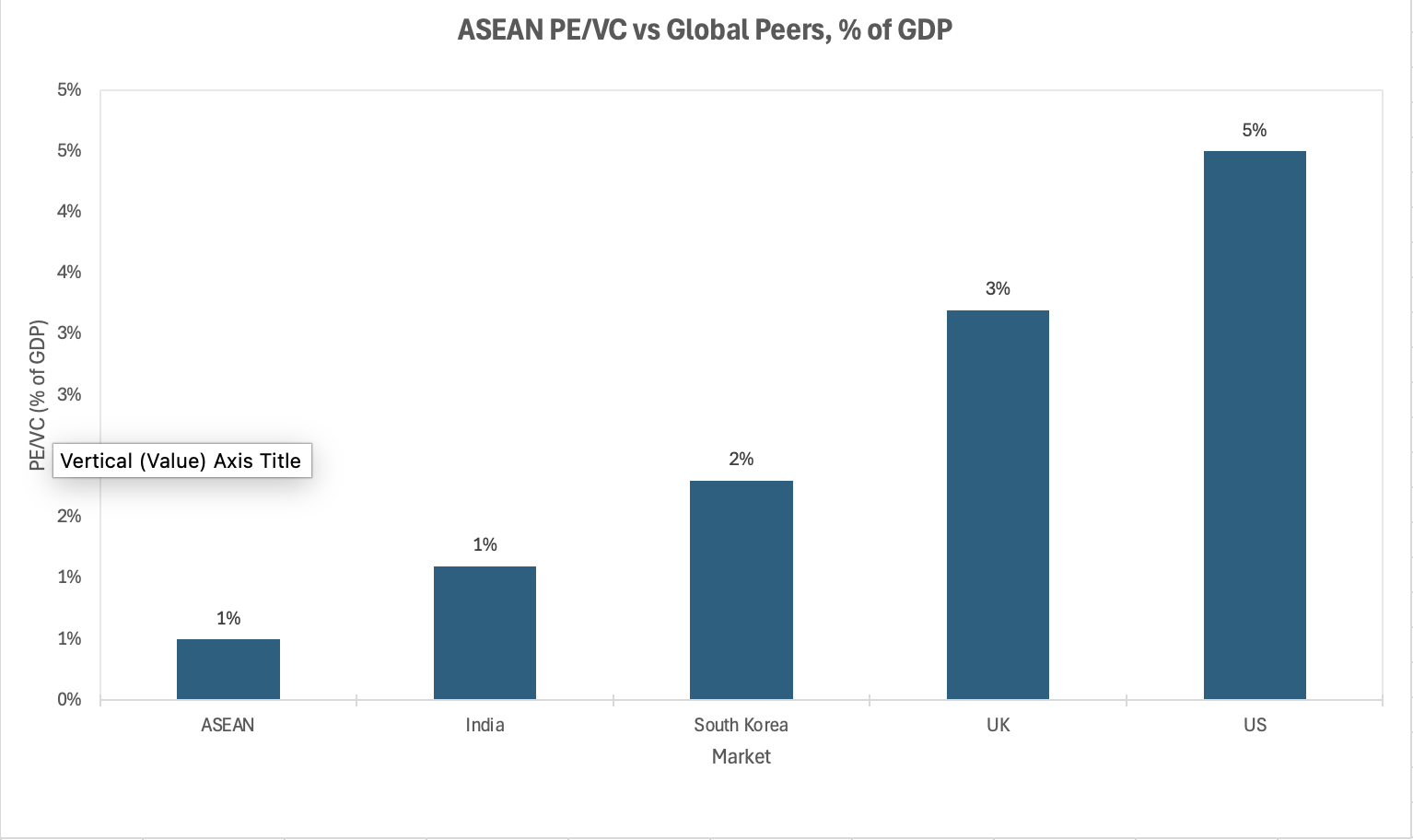

ASEAN private equity and venture capital deployment as a percentage of GDP compared to global peers (2023). The structural under-penetration is the entry context; consumer-facing brand platforms represent one of the highest-conviction deployment opportunities within that gap. Source: ASEAN Business Advisory Council.

Valuations support entry. Southeast Asia's mid-market PE deal size averaged $267 million in 2025, down from $356 million the previous year, reflecting the retreat of financial investors from the region. PE and venture capital deployments in ASEAN total only $19 billion, representing 0.5% of regional GDP. Exit routes are credible: multinational consumer goods companies seeking ASEAN-native brand exposure without building from scratch represent natural acquirers; regional sovereign wealth funds, including Khazanah Nasional Berhad and Temasek Holdings, have signalled appetite for consumer sector co-investments; and an improving initial public offering (IPO) environment in Indonesia and Malaysia provides an additional pathway for scaled brand platforms.

Near-Term Catalysts and Policy Outlook

Three catalysts are converging on a 12 to 36-month horizon.

Tariff-driven OEM relocation: US tariffs on Chinese goods, fixed at a weighted average of 47.5% by late 2025 ahead of a potential Trump-Xi meeting in April 2026, have already reduced Chinese export volume to the US by 20% and redirected capital and production capacity into Vietnam, Thailand, Malaysia, and Indonesia. This intensifies supply-side commoditisation at exactly the moment when ASEAN consumer incomes are rising: a structural wedge that only regionally trusted brands can monetise.

ASEAN industrial policy: Thailand's 30% EV production target by 2030, Malaysia's national semiconductor and advanced manufacturing strategy, and Indonesia's nickel-to-EV supply chain ambitions are all drawing in foreign capital and accelerating the formation of an industrial consumer middle class that will anchor demand for differentiated products.

Social commerce as brand-building infrastructure: TikTok Shop's penetration across Thailand, Vietnam, Indonesia, and Malaysia has lowered consumer acquisition costs dramatically relative to traditional retail. A brand built digitally on Chinese OEM supply can achieve regional scale in 18 to 24 months at a fraction of the capital previously required.

Three plausible scenarios:

Base: Brand consolidation accelerates through 2026 to 2027, driven by mid-market private equity and family office capital. Exit multiples for scaled platforms reach 8 to 12 times earnings before interest, taxes, depreciation and amortisation (EBITDA), supported by strategic acquirer interest.

Upside: A Trump-Xi tariff détente in 2026 triggers renewed Western corporate interest in ASEAN brand platforms as a vehicle for China-diversified regional exposure, expanding acquisition multiples.

Downside: Chinese OEMs elect to build their own regional brands aggressively, using deep capital subsidies to short-circuit the brand gap. Haier's acquisition of GE Appliances and Aqua, and BYD's expanding regional brand investment, illustrate the capability; the question is appetite and speed.

Conclusion

The consensus ASEAN investment thesis has focused on manufacturing relocation, logistics infrastructure, and technology platforms. These are real opportunities, but they are increasingly competed, well-capitalised, and priced. The mis-priced risk sits one layer above: the brand and distribution infrastructure that converts Chinese OEM supply into regionally trusted consumer propositions.

This is not a cyclical opportunity contingent on macroeconomic normalisation. It is a structural window created by the interaction of Chinese manufacturing dominance, rising ASEAN consumer incomes, and the digital-native cohort's demand for identity-led consumption. The geopolitical overlay reinforces the case. In an environment of sustained US-China trade friction, ASEAN-native brands serve a dual function: commercially credible in Southeast Asian markets and politically palatable in Western markets in ways that Chinese-origin brands, regardless of product quality, are structurally not. That is a premium that balance sheets have not yet been asked to price. They will be.

References

Euromonitor International — The Rise of Chinese Brands in Southeast Asia — 2025

KR Asia / Nikkei Asia — Chinese consumer brands surge in Southeast Asia, challenge legacy names — January 2026

Business Wire / Euromonitor — Southeast Asia Is the Biggest Export Destination for Chinese Products — July 2025

Counterpoint Research — Southeast Asia EV Sales Double in Q2 2025 — August 2025

China Global South Project — BYD Tops Southeast Asia EV Sales — July 2025

EY — Southeast Asia Private Equity Pulse 2025: Year in Review — February 2026

Deloitte — 2025 Asia Pacific Private Equity Almanac — February 2025

ASEAN Business Advisory Council — ASEAN's Private Markets: Coming Together for Growth — 2025

Value Chain Asia — China Plus One in Southeast Asia: Chinese Companies Expand Manufacturing — November 2025

Al Jazeera — US trade with Southeast Asia and Taiwan surging despite Trump tariffs — January 2026

RSIS International — Impact of Trump's 2025 "Liberation Day" Tariffs on Southeast Asia — June 2025

Peterson Institute for International Economics — The Trump-China Trade Wars: Five Takeaways from US Imports in 2025 — March 2026

This article is for information and discussion only and does not constitute investment advice or a recommendation.