National Oil Companies and the Stewardship Paradox

The engagement frameworks investors have built to hold the energy industry accountable are aimed, almost without exception, at the wrong companies.

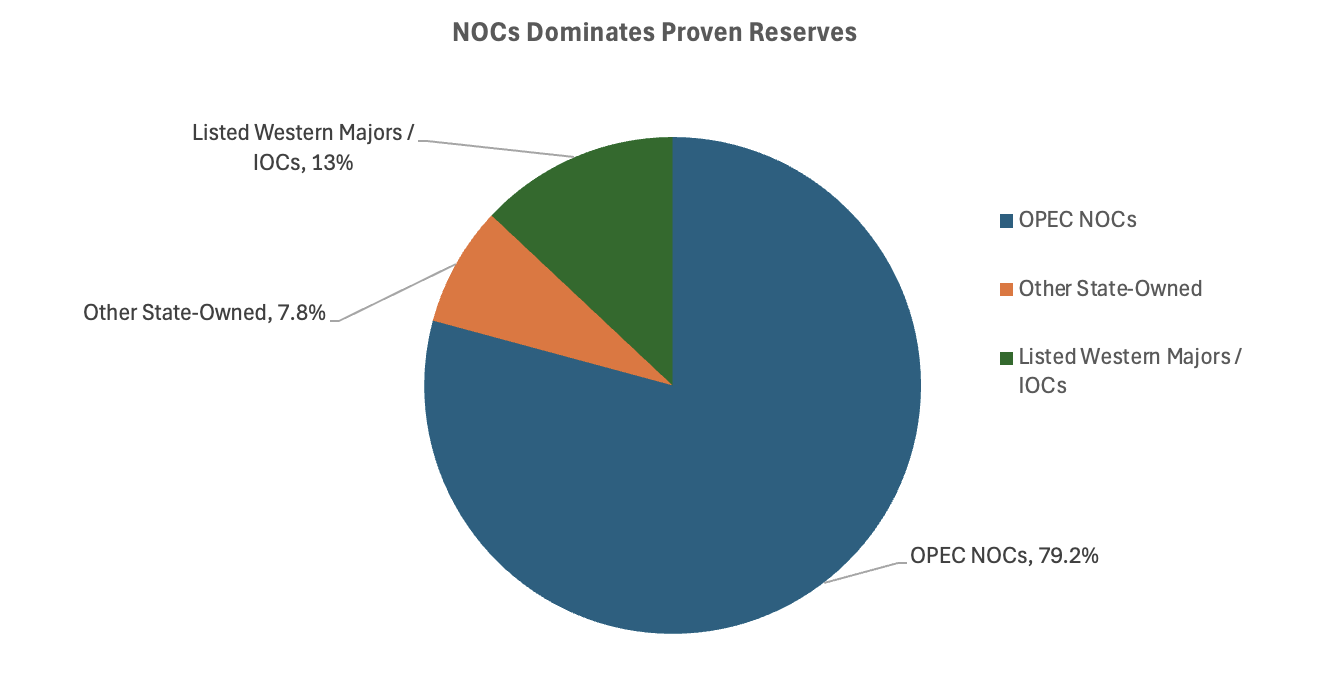

State-owned energy producers control the vast majority of the world's hydrocarbon reserves, yet they sit almost entirely outside the perimeter of institutional stewardship. Environmental, social and governance (ESG) frameworks, engagement coalitions, and net-zero alliances have been constructed around listed Western majors: Shell, BP, TotalEnergies, ExxonMobil. These companies collectively command perhaps 13% of global proven crude oil reserves. The remaining 87% sits with national oil companies (NOCs), most of which are unlisted, most of which operate under sovereign mandates that investors cannot easily penetrate, and most of which are now navigating a structural transition that will have material consequences for energy security, sovereign credit, and emerging-market capital allocation for the next two decades.

Why This Matters

Reserve concentration: OPEC member-country NOCs alone hold approximately 1,241 billion barrels, representing nearly 80% of global proven crude oil reserves at end-2024. The listed universe where stewardship effort is concentrated holds a fraction of that.

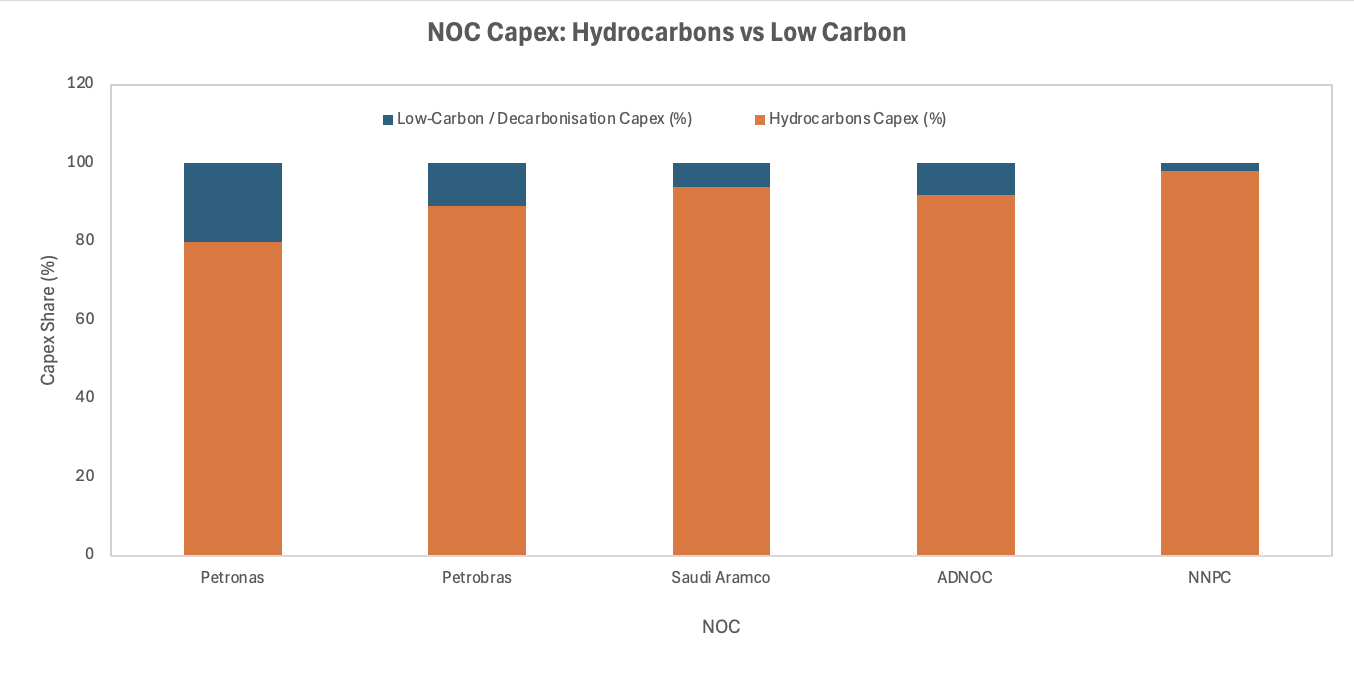

Dual-mandate drift: Petronas has committed 20% of its total capital expenditure over five years to low-carbon and decarbonisation initiatives, while managing a 34% drop in annual profit as oil prices fell. Petrobras has pledged carbon neutrality by 2050 on scopes 1, 2 and 3. The strategic direction is real; the accountability infrastructure is not.

Governance gap: NOCs average 71% more staff for 18% less output than comparable private-sector firms, and the political economy that drives those inefficiencies is precisely what investors need to assess when pricing sovereign or quasi-sovereign exposure in emerging markets.

The Core Shift

The transfer of reserve control from international oil companies (IOCs) to NOCs was not an event: it was a multi-decade structural shift that culminated quietly, without a closing bell. Today, the architecture of the global energy system is predominantly sovereign. Venezuela, Saudi Arabia, Iran, Iraq, Kuwait, and the United Arab Emirates collectively account for the lion's share of OPEC's 1,241 billion barrels. Brazil's Petrobras, Malaysia's Petroliam Nasional Berhad (Petronas), and Nigeria's Nigerian National Petroleum Corporation (NNPC) anchor the energy sectors of three of the world's most consequential emerging economies.

Source: OPEC Annual Statistical Bulletin 2024

What has changed more recently is the strategic pressure applied to these entities from both ends simultaneously. Falling oil prices compress the fiscal surpluses that governments extract from NOCs as quasi-taxation. The energy transition threatens the terminal value of their core asset base. And a cohort of more commercially aware NOC leadership teams, in Kuala Lumpur, Rio de Janeiro, and Abu Dhabi, has concluded that standing still is not an option. Petronas' three-part strategy, reducing emissions from operations, investing in renewables and low-carbon businesses, and deploying carbon management technologies, reflects a genuine attempt to reconcile the hydrocarbon mandate with transition reality. The question investors have not adequately answered is: how do you measure credibility when there is no listed equity to price?

The Non-Obvious Mechanism

The standard criticism of NOCs is the dual mandate: they must maximise commercial returns whilst fulfilling social and political objectives, from subsidised fuel pricing to national employment quotas. That tension is well-understood. The less examined mechanism is what the dual mandate does to governance quality as the energy transition sharpens the trade-off.

As decarbonisation capex rises, NOC management teams face a new version of the classic principal-agent problem. The principal, typically a finance ministry or a sovereign wealth fund structure, wants hydrocarbon revenue to underwrite national budgets. The agent, the NOC itself, knows that long-term asset value requires transition investment. Petronas' decision to allocate 20% of capex to low-carbon projects, taken against a backdrop of declining profits, suggests that at least some NOC boards are resolved to run this gauntlet. Petrobras, under chief executive Magda Chambriard, has extended its geographic reach back into Africa while simultaneously maintaining a carbon neutrality pledge, threading a needle that most sell-side analysts have not followed to its logical balance-sheet conclusion.

Sources: Company disclosures, 2025 plans

The second-order effect follows directly: divergence in transition commitment across NOCs will widen the spread between their implied cost of capital, even though most of that capital is raised through sovereign bonds or government-intermediated debt rather than through equity markets. NNPC allocating virtually nothing to low-carbon capex while Petronas commits 20% is not merely a difference in ambition. It is a leading indicator of which sovereign energy systems will face refinancing pressure, stranded-asset write-downs, and fiscal instability as the energy transition progresses. Investors in Nigerian sovereign paper are, functionally, long NNPC's ability to sustain hydrocarbon cash flows indefinitely, but few frame their position that way.

Investor and Stakeholder Implications

Investors seeking exposure to emerging-market energy cannot engage with NOCs the way they engage with Shell or BP. There is no annual general meeting. There is no shareholder resolution mechanism. There is no obligation to respond to Climate Action 100+ letters. The engagement infrastructure built for listed companies does not translate.

What does translate is sovereign and quasi-sovereign bond engagement, and this is where the stewardship conversation needs to relocate. Sovereign bond investors who apply net-zero alignment methodologies to country-level emissions are, in effect, conducting a proxy form of NOC governance assessment, since in most resource-dependent economies the NOC's production trajectory, investment programme, and fiscal transfers are the dominant variable in any credible decarbonisation plan. Investors who separate these two analytical tracks, treating sovereign fixed income and NOC energy exposure as distinct silos, are likely mispricing both.

The practical implication is that meaningful engagement with NOC governance requires three things: direct government-level dialogue on the fiscal incentive structure embedded in NOC transfer pricing, assessment of whether transition capex commitments are ring-fenced from budget pressure, and scrutiny of disclosure quality as a proxy for institutional maturity. Brookings' research on NOC transparency identifies consistent public reporting, benchmarking against well-defined objectives, and enhanced corporate governance as the critical variables; these are exactly the dimensions on which NOC bond covenants and sovereign lending conditions remain weakest.

Near-Term Catalysts and Policy Outlook

The asymmetry over the next twelve months favours further divergence between NOCs that are credibly positioning for the transition and those that are not, with the principal catalyst being the fiscal stress test applied by oil prices remaining range-bound below the budget break-even levels of several OPEC producers.

0-3 month window: The immediate driver is oil price trajectory. Several Gulf NOCs and NNPC operate with budget break-even oil prices well above current spot levels, creating pressure on transition capex commitments made when revenues were higher. Petronas' reported 34% profit decline in 2024 is the template; NOCs with weaker balance-sheet buffers will face harder choices between dividend transfers to the sovereign and discretionary low-carbon investment in the near term.

3-12 month window: The medium-term story is Petrobras and the Brazilian regulatory cycle. Petrobras' acquisition of Petronas' 50% stake in the Tartaruga Verde and Espadarte Module III fields in the Campos Basin for $450 million signals a deliberate strategy of consolidating hydrocarbon assets while maintaining the decarbonisation pledge. How the Brazilian government handles the tension between short-cycle oil production growth and longer-cycle transition investment will set a precedent for other resource-dependent emerging markets navigating the same structural constraint.

The scenario framing for the next twelve months is as follows. The divergence in NOC transition credibility either widens or narrows depending on three variables: oil price resilience, the pace of multilateral financing for energy transition in emerging markets, and whether sovereigns adopt fiscal frameworks that ring-fence NOC transition capex from general budget demands.

Base case: Oil prices remain volatile but broadly range-bound; transition capex commitments at Petronas and Petrobras hold but do not expand materially; NNPC and lower-income NOCs defer low-carbon investment further; the stewardship gap narrows only at the margins.

Upside: Multilateral Development Bank (MDB) financing for NOC transition programmes scales meaningfully, providing an alternative capital source that reduces the fiscal trade-off; Petronas and Petrobras use this to accelerate decarbonisation capex; sovereign bond spreads begin to price NOC transition credibility more explicitly.

Downside: A sustained oil price decline below $65 per barrel forces NOCs, including Petronas, to cut discretionary capex; transition commitments are deferred rather than abandoned, but the market reads them as structurally subordinate to fiscal needs; the implied cost of capital for NOC-linked sovereign debt widens, particularly in West Africa and Southeast Asia.

Conclusion

The stewardship conversation has been conducted in the wrong boardrooms for more than a decade. The listed Western majors, for all their disclosure obligations and engagement receptivity, are not where the structural energy story is written. It is written in Kuala Lumpur, Abuja, Rio de Janeiro, and Riyadh, in the budget negotiations between finance ministers and NOC boards, and in the quiet decisions about whether transition capex survives the next oil price down-cycle.

The structural read-across is clear: as the energy transition extends its timeline under the weight of energy security concerns and geopolitical realignment, NOCs will remain central to global supply. The investors who price that reality accurately are those who have learned to engage at the sovereign level, to read transition capex commitments not as marketing signals but as institutional stress tests, and to treat NOC governance quality as a first-order input into their emerging-market fixed income and energy allocation. The geopolitical overlay is not subtle: resource nationalism is rising, sovereign control over energy assets is tightening, and the window for influence through engagement, rather than through price alone, is narrower than it appears. The more likely read is that the NOCs who have begun the transition in earnest are doing so not because of external pressure, but because their own leadership has concluded the alternative is fiscal ruin. That is a more durable basis for change than any stewardship letter ever written to a listed company.

References

OPEC Secretariat – Annual Statistical Bulletin 2024: Global Proven Crude Oil Reserves – 2024

IISD / 2035 Initiative – National Oil Companies and Climate Change: Insights for Advocates – 2021

Brookings Institution – New Data on Governance of National Oil Companies – March 2022

World Economic Forum – National Oil Companies and the Challenge of ESG Reporting – August 2022

Petronas / Forbes – Taking the Lead in Asia's Energy Transition – October 2025

LinkedIn / Petronas – Petronas to Channel 20% of Capex to Decarbonisation Projects Over Next Five Years – June 2025

Reccessary – Petronas Cuts Jobs, Bets on Low-Carbon Transition as Profits Decline – February 2025

Reclaim Finance – Assessment of Petrobras' Climate Strategy (PDF) – 2024

LinkedIn – Brazilian NOC's 7 Strategic Shifts Under New CEO Magda Chambriard – June 2025

Offshore Technology / Yahoo Finance – Petrobras to Buy Petronas' 50% Campos Basin Stakes for $450m – March 2026

Rystad Energy – National Oil Companies Hold the Key to Global Energy Stability – May 2025

Deep Dive Global – The Paradox of National Oil Companies: Power, Politics, and Profit (YouTube) – October 2025

T. Rowe Price – Establishing Industry Best Practice: A Net Zero Methodology for Sovereign Investors – October 2025

IIGCC – Sovereign Bonds Net Zero Framework – June 2024

Disclaimer: This article is for information and discussion only and does not constitute investment advice or a recommendation.