The Hedge Fund Horizon Problem — Why Stewardship in Real Assets Cannot Be Activist

The most consequential governance decisions in defence supply chains, mining and energy infrastructure are not made at shareholder AGMs. They are made at financial close.

Activist hedge funds have built a credible record in consumer-facing, short-cycle sectors. The mechanics are well understood: acquire a meaningful stake, identify operational slack, apply pressure through the boardroom or the proxy process, and exit once the repricing occurs. The logic is internally consistent because the capital cycles in those sectors — two to four years for a consumer brand, three years for a media property — are broadly compatible with the fund's own return horizon.

That logic collapses entirely when the same playbook is applied to real assets.

Why This Matters

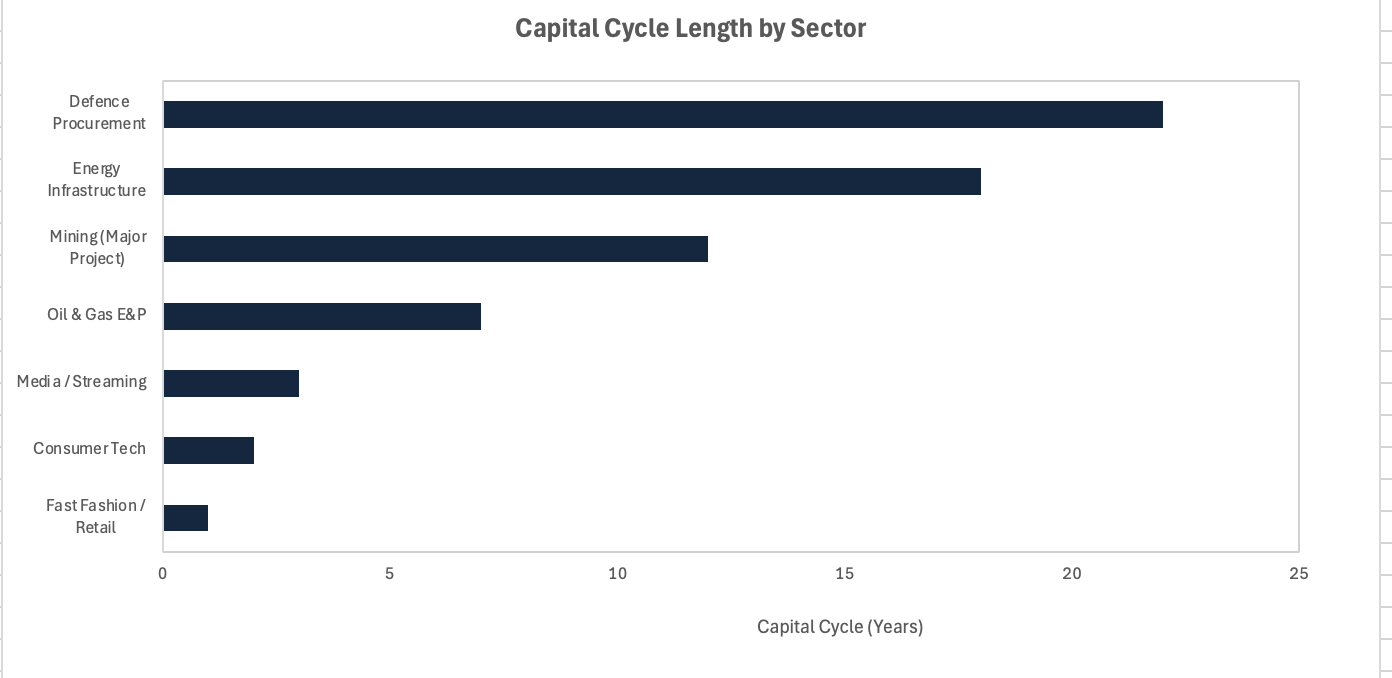

Structural mismatch: Capital cycles in defence, mining and energy infrastructure run 15 to 25 years; activist hedge fund holding periods average 18 to 24 months. The two cannot coexist productively.

Governance is migrating: In Southeast Asia and the Middle East, blended finance structures and sovereign wealth fund (SWF) co-investment are redefining stewardship in long-cycle assets, bypassing the public equity market entirely.

The practical implication for allocators: Governance premium in real assets is captured through patient capital structures, not through engagement letters. The fund manager who understands this distinction will construct a materially different portfolio from one who does not.

The Core Shift

Real assets are not slow consumer businesses. They are a categorically different class of capital commitment, defined by the irreversibility of the investment decision and the length of time before any meaningful cash flow is generated.

A greenfield lithium mine in Indonesia or the Philippines requires six to ten years of permitting, pre-development and construction before first production. A naval frigate programme under contract to a regional defence ministry will draw on supply chain financing arrangements that span two decades. An LNG terminal anchoring a national energy transition strategy may not reach a commercial payback threshold for eighteen years. The governance decisions that actually determine value in these assets, the choice of project finance structure, the construction risk allocation, the offtake covenant, the debt-to-equity ratio at financial close, are all made long before the asset ever appears on a public market screen.

An engagement letter delivered three years into a twenty-year asset life change nothing of consequence. The bet has already been placed.

Source: McKinsey, IEA, Industry estimates

The Non-Obvious Mechanism

The standard critique of activist hedge funds in long-cycle sectors focuses on time horizon misalignment. That is correct but incomplete. The deeper problem is where in the capital structure the value is created and where the governance lever actually sits.

In a retailer or a media company, the publicly traded equity represents a meaningful share of total enterprise value, and shareholder votes carry real weight. In a large mining or defence project, the publicly traded equity is often a thin residual claim sitting above a capital structure dominated by project finance debt, export credit agency (ECA) guarantees, development finance institution (DFI) tranches and sovereign off-take obligations. The decisions that shape that capital structure, the covenants, the intercreditor agreements, the blended finance architecture, are negotiated between development banks, governments, project sponsors and institutional lenders. A hedge fund holding three percent of the listed equity has no seat at that table and no mechanism to influence the outcome.

The activism that matters in these sectors happens at origination. The fund that participates in the project finance syndicate, or co-invests at financial close alongside a DFI, is the one with genuine governance influence. The fund that buys the equity three years later and sends a letter to the board is a price-taker dressing itself as a steward.

This is not a theoretical observation. Elliott Investment Management's campaign against BP, in which the fund acquired close to five percent of the company and pressed for an accelerated divestment programme, illustrates the structural limits precisely. The assets Elliott wanted to reshape, long-cycle upstream positions and infrastructure commitments, are governed by capital structures and contractual obligations that equity activism cannot unwind without destroying value. The more likely read of that campaign is that it functioned as a pricing catalyst for the equity, not as a genuine governance intervention in the underlying asset base.

Investor Implications

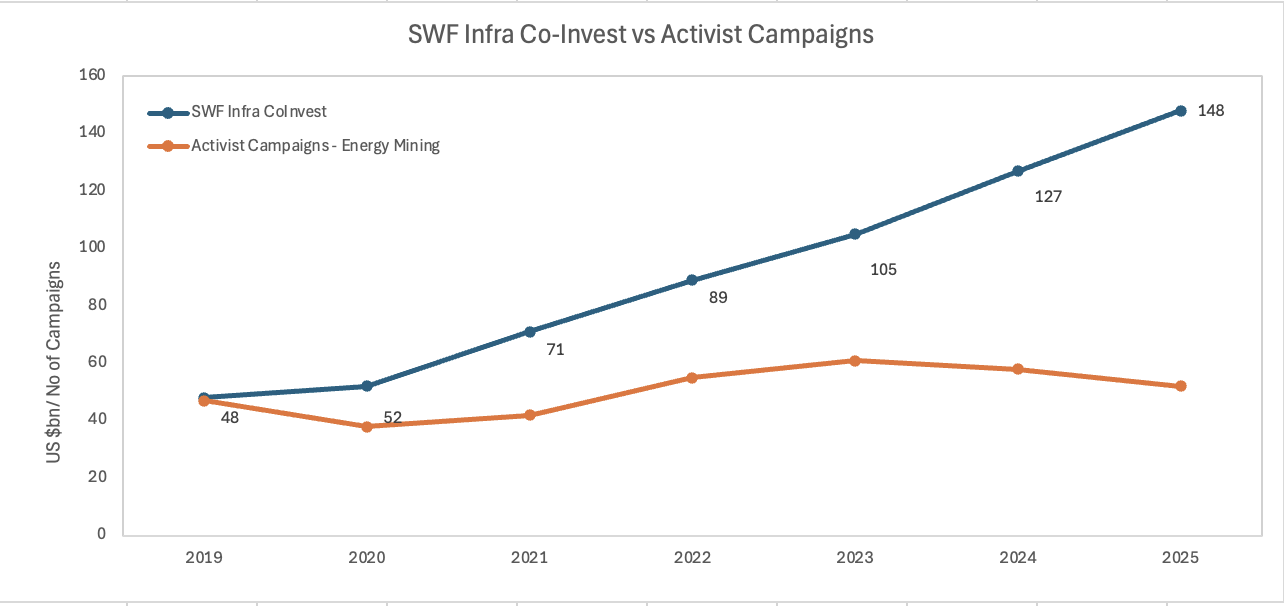

The structural case for patient capital in real assets is now being validated empirically rather than argued theoretically. SWF assets crossed USD 13 trillion globally in 2025, driven in part by Gulf funds, with Mubadala and Saudi Arabia's Public Investment Fund (PIF) expanding their direct co-investment activity in infrastructure, energy and materials at scale. Mubadala Capital raised USD 554 million for its inaugural co-investment fund in January 2026, surpassing its initial target. GIC and Temasek together deployed USD 31 billion in 2025, maintaining direct deal teams across all three channels: fund commitments, co-investments and direct sourcing.

The pattern across Southeast Asia and the Middle East is consistent. The capital that is shaping governance in long-cycle real assets is not arriving through the secondary equity market. It is arriving through co-investment alongside private equity sponsors, through blended finance structures where concessional capital from DFIs de-risks the first-loss tranche for commercial investors, and through direct bilateral arrangements between SWFs and host governments.

For capital allocators, this has a direct portfolio construction implication. Exposure to governance premium in real assets requires access to primary structures: project finance, infrastructure debt, co-investment, or direct equity at financial close. Secondary equity activism in these sectors does not produce the same outcome, and in several documented cases produces the opposite, by forcing short-cycle decisions onto long-cycle asset bases.

The hedge fund community's genuine contribution in these sectors is different and valuable: liquidity provision in listed infrastructure equities, disciplined pricing in secondary debt markets, and relative value positioning across the capital structure. These are legitimate roles. They are not stewardship roles.

Source: Global SWF – 2026 Annual Report: Sovereign Investor Activity 2025 – December 2025; Reuters – Mubadala Overtakes PIF as World's Top Wealth Fund Spender – December 2024; Khaleej Times – Mubadala Invests Dh120 Billion in 40 Transactions in 2025 – December 2025.

Near-Term Catalysts and Policy Outlook

The next twelve months represent an asymmetric period for this thesis: the structural case for patient capital in real assets is strengthening faster than the allocation infrastructure to support it is being built, which creates both opportunity and risk.

0–3 month window: Defence budget cycles across NATO-adjacent and Indo-Pacific states are in active appropriation phases. India's Ministry of Defence has been allocated a record Rs 7.85 lakh crore for 2026–27, a 15 percent increase year-on-year, with capital expenditure for acquisition up 24 percent. Procurement decisions at this scale generate multi-decade supply chain financing requirements. Allocators with access to defence-adjacent project finance and ECA-backed structures are being positioned now.

3–12 month window: Blended finance frameworks are being codified at the policy level. The Organisation for Economic Cooperation and Development (OECD) published updated Blended Finance Guidance in September 2025, clarifying how development finance institutions (DFIs) can mobilise private capital across emerging markets. In parallel, Gulf SWFs are scaling their Asia allocations: Mubadala's stated target is 25 percent of its portfolio in Asia, up from current levels, with infrastructure and energy as primary channels. This creates a structural co-investment corridor between the Middle East and Southeast Asia that bypasses Western public equity markets almost entirely.

The scenario range from here is wide. Introducing the scenario block: the degree to which patient capital structures scale beyond the current SWF and DFI anchors, and into broader institutional allocation, will determine how quickly governance premium migrates away from public equity activism.

Base case: Blended finance and SWF co-investment continue growing at 15 to 20 percent annually in real asset sectors; listed equity activism in energy and mining plateaus as governance influence demonstrably resides elsewhere; allocators incrementally shift from secondary to primary structures over a three to five year period.

Upside case: A major activist campaign in a long-cycle infrastructure asset visibly destroys value, accelerating institutional recognition of the structural flaw; blended finance frameworks gain regulatory clarity in key jurisdictions; patient capital structures attract a wider LP base including mid-tier pension funds.

Downside case: Geopolitical fragmentation reduces cross-border co-investment capacity; SWF domestic allocation mandates constrain external deployment; blended finance frameworks become politically contested in the context of US trade policy under President Trump's administration, slowing multilateral DFI activity.

Conclusion

The governance debate in real assets has been framed, incorrectly, as a contest between activist engagement and passive indifference. The more precise framing is between capital that sits inside the structure and capital that observes it from the outside.

Patient capital structures, blended finance co-investment, project finance participation and SWF direct investment, do not merely provide longer holding periods. They provide governance access at the point in the asset's life where governance actually matters. The structural shift being observed across Southeast Asia and the Middle East is not a cultural preference for relationship-based investing. It is a rational response to where value in long-cycle assets is actually created and protected.

The practical read-across for allocators is structural rather than cyclical: this is not a rotation trade. Capital allocators who build primary market access in defence supply chain finance, minerals project finance and blended energy infrastructure will capture the governance premium. Those who rely on secondary equity activism in the same sectors will find themselves, at best, providing liquidity to those who got there first.

The geopolitical overlay reinforces the point. In a world where defence capability, critical minerals and energy security are being treated as strategic national interests by governments from Jakarta to Riyadh to New Delhi, the capital that earns a seat at the governance table is sovereign-adjacent, patient and structured. The capital that writes engagement letters to boards of publicly listed contractors is a peripheral participant in a game being decided elsewhere.

References

IFC – The Role of Blended Finance in an Evolving Global Context – 2025

OECD – DAC Blended Finance Guidance 2025 – September 2025

Global SWF – SWF Assets Cross USD 13 Trillion; GIC AuM Rises to USD 936bn – July 2025

Praxis Rock – 34 Sovereign Wealth Funds: SWF Directory – March 2026

Reuters – Hedge Fund Elliott Commands Attention in C-Suites as Relentless Activist – February 2025

Harvard Law School Forum on Corporate Governance – The 2025 Activist Watchlist – March 2026

Mitsui Global Strategic Studies Institute – Torrent of Middle Eastern Money Flooding Into Asia – May 2025

Mubadala Capital – Inaugural Co-Investment Fund, USD 554 Million Raise – January 2026

Communications Workers of America – Report on Elliott Management's Long-Term Impact – September 2021

Institute for New Economic Thinking – How Shareholder Activism Became Toxic – January 2025

Ministry of Defence, India – Defence Budget Allocation FY 2026–27 – May 2026

DealStreet Asia – Beyond the Buyout: Mubadala and PIF on Capital Deployment at Scale – April 2026

J.P. Morgan – Working Capital Solutions for Defence Sector Supply Chains – February 2026

This article is for information and discussion only and does not constitute investment advice or a recommendation.