Pricing What Actually Matters: A Market Materiality Framework for the New Resource Cycle

Financial materiality, as currently practised, does not capture the risks that are actually moving prices in real-asset markets. This article proposes a working framework built on three empirically grounded signals: scarcity concentration risk, policy acceleration events, and social licence volatility. Together, they offer allocators a more honest map of where value is being created and destroyed in the new resource cycle.

Why This Matters

Mispriced risk: Standard ESG disclosure frameworks systematically lag the risks now driving project failure and commodity repricing, leaving allocators exposed to losses they cannot model with existing tools.

Supply chain fragility: China controls refining for over 80% of the rare earths on NATO's defence-critical raw materials list; a single policy decision in Beijing can reprice entire sectors within weeks, as April 2025 demonstrated.

African project risk: Social licence failure has become the primary driver of cost overrun and schedule slippage in African and Southeast Asian mining, yet it carries no line item on most due diligence templates.

The Framework's Starting Point

The standard financial materiality test asks whether a given piece of information would influence the decision of a reasonable investor. In practice, for real assets tied to the energy transition and defence supply chains, that test has been applied so narrowly that it systematically excludes the risks that are actually moving prices.

Three datasets illustrate the problem. First, research published in late 2025 by the University of Cambridge and the University of Bristol provides empirical evidence that biodiversity-related transition risk is priced in global commodity markets: commodities with higher biodiversity footprints earn a risk premium of between 20 and 60 basis points per month, a signal that post-dates any disclosure standard currently in force. Second, the European Commission's Joint Research Centre projects lithium consumption in the EU alone rising nine to twelve times by 2030, a demand trajectory that no supply chain has been constructed to meet. Third, McKinsey analysis finds that 83% of major mining and metals projects suffer cost overruns of more than 40% and schedule delays of 20 to 30%, with megaprojects averaging cost overruns of 79% above initial estimates. These are not tail-risk scenarios; they are base-case outcomes that standard investment models treat as exceptional.

The framework proposed here does not replace financial modelling. It sits upstream of it, identifying the three categories of signal that should be feeding into discount rates, scenario assumptions, and position sizing before a model is built.

Signal One: Scarcity Concentration Risk

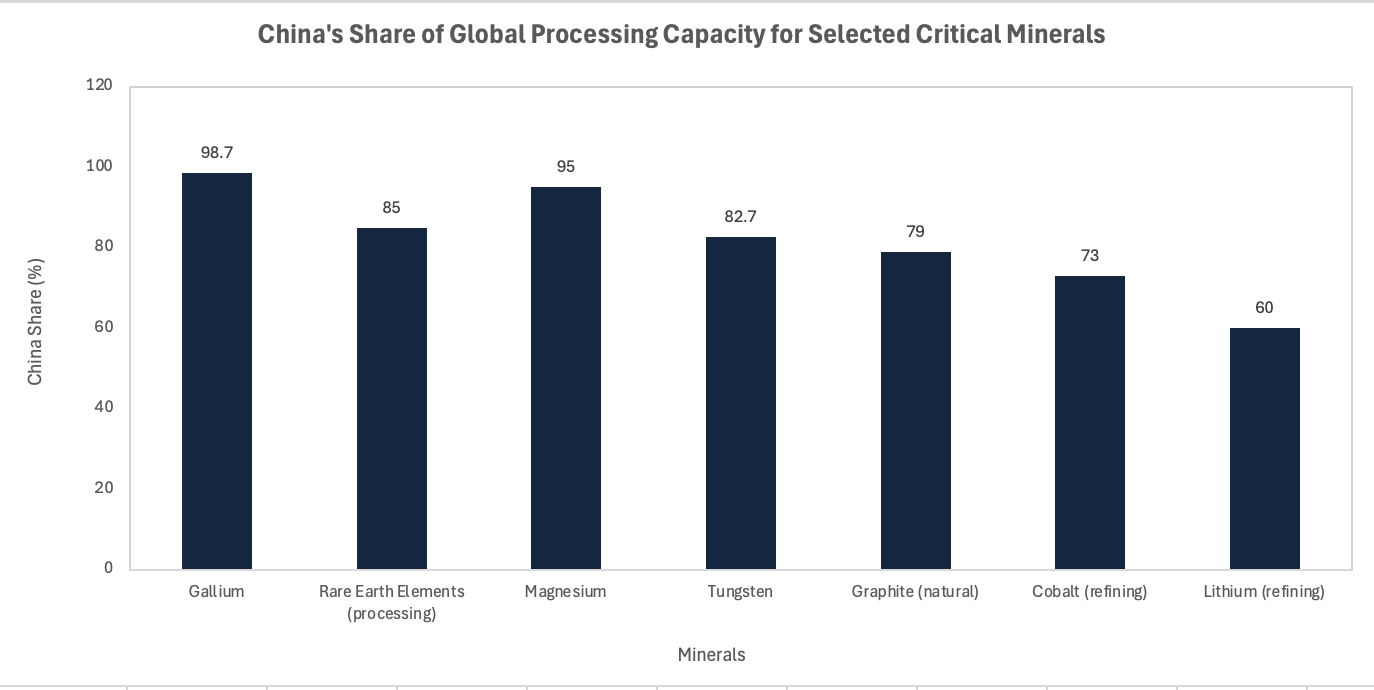

Scarcity concentration risk measures the probability that a single adversarial state can interrupt supply of a material for which no credible substitute or alternative processing route yet exists. China currently dominates production of at least 15 critical mineral groups, including gallium at 98.7% of global supply, magnesium at 95%, and tungsten at 82.7%. More importantly, it dominates the processing infrastructure through which materials from third-country mines must pass before reaching manufacturers.

The sequence of events in 2025 illustrates how quickly this theoretical risk translates into price disruption. In April, Beijing imposed export controls on seven heavy rare earth elements: dysprosium, gadolinium, lutetium, samarium, scandium, terbium, and yttrium. By October, the regime had expanded to cover five additional rare earths critical to magnets and defence applications, along with downstream and foreign-produced items incorporating Chinese-origin rare earths. The policy reached beyond Chinese borders. NATO's December 2024 publication of 12 defence-critical raw materials, covering aluminium, beryllium, cobalt, gallium, germanium, graphite, lithium, manganese, platinum, rare earth elements, titanium, and tungsten, formalised the strategic exposure that markets had been pricing informally for two years.

For allocators, scarcity concentration risk is not simply a geopolitical background variable. It is a direct input into the cost of capital for any project or company dependent on these supply chains. The relevant question is not whether disruption will occur, but which single-point-of-failure sits upstream of the investment and how long it would take to route around it. The honest answer, for most rare earth and heavy mineral supply chains today, is measured in years rather than months.

China's processing dominance across defence-critical minerals means export controls impose immediate supply shocks regardless of where raw materials are extracted. Sources: USNI; CFR; NATO (2024); SIPRI (2024).

Signal Two: Policy Acceleration Events

Policy acceleration events are discrete regulatory or legislative decisions that permanently reprice a commodity, a supply chain, or a project's risk profile. They are distinct from background policy trends because they carry hard timelines that compress the adjustment period available to investors. Three categories matter most in the current cycle.

Export controls are the most legible. China's April and October 2025 interventions demonstrated that a government can reshape global rare earth pricing through a single administrative act, with downstream effects on defence contractors, EV manufacturers, and wind turbine producers simultaneously. The EU's Critical Raw Materials Act, which sets binding benchmarks of at least 10% domestic extraction, 40% processing, and 25% recycling of annual EU consumption by 2030, with no more than 65% of any strategic material sourced from a single third country, creates a procurement mandate that will redirect capital flows regardless of whether commercial logic would have done so unaided. The structural case is that the 65% concentration ceiling alone will force source diversification at scale across the EU supply chain within four years.

Carbon Border Adjustment Mechanism (CBAM) adjustments represent the second category. As CBAM moves from its transitional phase into full implementation, the embedded carbon cost of imports is transferred explicitly to the balance sheets of European importers and their upstream suppliers. For mining projects in high-carbon jurisdictions, this is a repricing event in slow motion, but one with a known schedule. The third category is NATO procurement mandates. The June 2025 Hague Summit decision to allocate 1.5% of member GDP to critical infrastructure and the defence industrial base, with explicit attention to critical mineral supply chain security, creates a demand floor that did not exist two years ago. Canada formalised the domestic implication in December 2025, mandating the use of Canadian steel, aluminium, and critical minerals in federal defence procurements valued at $25 million or more.

The investor implication is that policy acceleration events do not merely adjust the probability distribution of outcomes; they shift the entire distribution. Projects and companies that were marginal under pre-event assumptions can become strategic under post-event assumptions, and vice versa. Allocators who treat policy signals as qualitative overlays rather than quantitative inputs will consistently misprice the adjustment.

Signal Three: Social Licence Volatility

Social licence volatility describes the risk that community opposition, environmental litigation, or governmental renegotiation of operating terms interrupts project delivery after capital has been committed. It is the least modelled of the three signals and, in African and Southeast Asian mining, the most consequential driver of project failure.

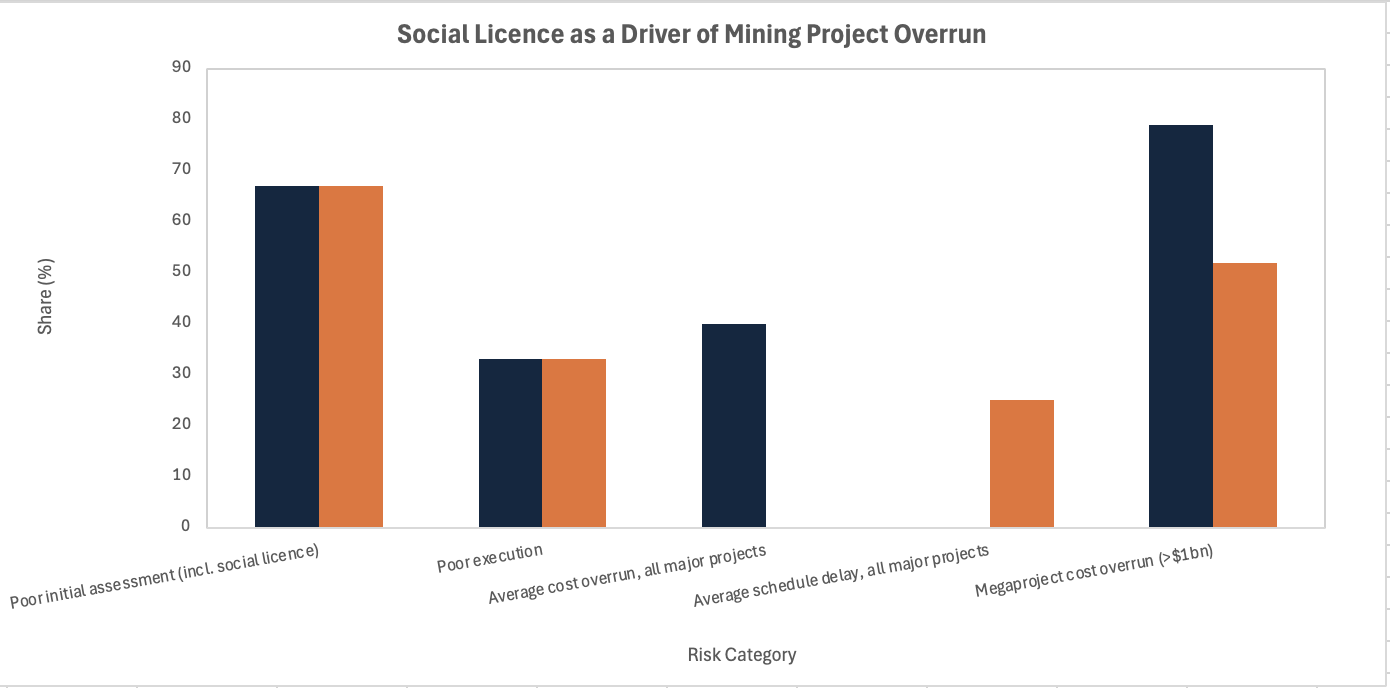

McKinsey's 2024 analysis of major mining projects found that approximately two-thirds of cost overruns and schedule delays originate in poor initial assessments rather than poor execution. The more precise read is that "poor initial assessment" largely means failing to account for the conditions under which community consent is sustainable over a multi-year project lifecycle. In Africa, the structural conditions for social licence failure have intensified: political transitions have multiplied, with new governments renegotiating mining codes and fiscal terms as a first act of sovereignty; community expectations around revenue sharing have risen with the commodity price cycle; and mobile technology has compressed the time between local grievance and international NGO mobilisation from months to days.

The World Economic Forum's 2026 analysis of critical minerals bankability identified permitting delays and policy volatility as primary drivers of cost overruns and schedule slippage at project level, with ad hoc government intervention representing the highest-impact single risk for projects in emerging market jurisdictions. The structural case is that social licence risk is now a pricing variable, not a disclosure checkbox. Allocators in private equity and project finance who underwrite African or Southeast Asian mining assets without a granular social licence assessment are not taking on unquantified risk; they are taking on quantified risk they have chosen not to measure.

Social licence failure and poor community assessment account for the dominant share of project underperformance. Source: McKinsey & Company, "The CapEx Crystal Ball", November 2024.

Catalysts and the Near-Term Policy Window

The asymmetry of risks in the 12 months from mid-2026 is heavily skewed toward further tightening: supply chains face more downside from policy escalation than upside from demand moderation.

0–3 month window: The immediate pressure points are China's export control regime, which has expanded twice in seven months and carries no structural incentive to reverse; CBAM's transitional phase, where compliance costs for non-EU producers are still being absorbed rather than fully priced; and project-level social licence disputes in West and Central Africa, where several large-scale mining renegotiations initiated by post-transition governments remain unresolved. Any further escalation of the US-China trade dispute, particularly if Beijing extends controls to downstream magnet products, would constitute a discrete pricing event across the defence and EV supply chains simultaneously.

3–12 month window: The EU's Critical Raw Materials Act strategic project pipeline enters its first significant review cycle, with procurement decisions that will set precedent for how European capital treats non-EU source diversification. NATO's Hague commitment begins translating into member-state procurement budgets, creating explicit demand signals for approved-source critical minerals. African sovereign wealth funds, which increased climate and infrastructure allocations materially in 2025, are expected to intensify engagement with mining royalty structures and value-addition requirements. The more likely read is that local beneficiation requirements will become non-negotiable conditions for new project approvals across several jurisdictions, raising both capital intensity and project timelines for external investors who did not model them.

The appropriate bridging observation before scenario analysis is that the direction of travel is clear and the uncertainty is around pace, not destination.

Base case: China's export control regime remains broadly stable at current scope; CBAM compliance costs are absorbed with modest price pass-through; social licence negotiations in Africa result in revised but workable terms for the majority of projects under review. Critical mineral prices remain elevated and volatile within a broadly supported range.

Upside case: US-China trade framework produces a structured easing of rare earth export restrictions in exchange for technology concessions; EU strategic project approvals accelerate capital deployment into non-Chinese sources; social licence frameworks mature in two or three key African jurisdictions, reducing the political risk premium for project finance. Capital flows into the sector broaden beyond the current cohort of specialist investors.

Downside case: China extends export controls to processed rare earth products and magnet assemblies, triggering supply disruption across multiple defence and clean energy supply chains simultaneously; one or more high-profile African project failures politicises the sector and triggers a capital withdrawal; CBAM adjustments provoke retaliatory trade measures that reduce the competitiveness of EU-sourced materials. The cumulative effect is a period of structural underinvestment precisely when physical demand is accelerating.

Conclusion

The repricing of biodiversity-linked commodities after the Kunming Declaration, the measurable risk premium now embedded in high-biodiversity-footprint assets, and the expansion of China's export control regime across twelve rare earth elements in seven months are not isolated events. They are evidence of a structural transition in how resource-cycle risks are being valued by markets, and that transition is running ahead of the analytical frameworks most allocators are using to underwrite it.

The three signals proposed here, scarcity concentration risk, policy acceleration events, and social licence volatility, are not novel in concept. What is new is that all three are now empirically observable in price data, and all three are accelerating simultaneously. For hedge fund managers, the implication is position-sizing: single-point-of-failure supply chains can gap significantly on a single policy announcement, requiring liquidity buffers that standard commodity volatility models do not accommodate. For private equity allocators underwriting African or Southeast Asian mining assets, the implication is diligence methodology: social licence assessment must precede financial modelling, not follow it. For sovereign capital, the structural implication is that the window for securing off-take agreements and strategic partnerships in non-Chinese critical mineral jurisdictions is narrowing as competing sovereign mandates from the EU, NATO members, and the United States intensify simultaneously.

The wider read-across is geopolitical. The mineralisation of strategic competition, the process by which supply chain control has become a tool of statecraft, has created a new category of investable risk that does not map cleanly onto either traditional commodity analysis or ESG disclosure. Allocators who recognise this first, and build analytical frameworks to price it rather than disclose around it, will not merely avoid the obvious errors. They will find the overlooked opportunities that the current frameworks are structurally incapable of seeing.

References

University of Cambridge / University of Bristol — "The Pricing of Biodiversity Risk in Commodity Markets" — November 2025

European Commission Joint Research Centre — EU Critical Raw Materials Act and High Demand Scenario projections — 2023/2024

McKinsey & Company — "The CapEx Crystal Ball: Beating the Odds in Mining Project Delivery" — November 2024

NATO — "NATO Releases List of 12 Defence-Critical Raw Materials" — December 2024

Council on Foreign Relations — "Leapfrogging China's Critical Minerals Dominance" — February 2026

World Economic Forum — "Making Critical Minerals Bankable: Policy Tools to Unlock Investment" — 2026

SIPRI — "Critical Minerals and Great Power Competition" — October 2024

Atlantic Council — "Critical Minerals in Crisis: Stress Testing US Supply Chains" — October 2025

Torys LLP — "Securing Canada's Critical Minerals Supply Chain" — March 2026

EIES / Secure Energy Europe — "NATO's 1.5% Must Include Critical Material Supply Chains" — July 2025

This article is for information and discussion only and does not constitute investment advice or a recommendation.