Dressed for Distress: The Hidden Capital Reallocation Reshaping the Fashion Industry

Fashion is not in a normal downturn. It is in a capital reallocation cycle, and the structural opportunity sits below the brand layer.

The industry has entered 2026 with several pressures that look cyclical in isolation but structural in combination: luxury has stalled after a decade of price-led growth, the mid-market is moving from margin squeeze to insolvency, de minimis reform has attacked the economics of ultra-fast fashion, and the European Union's product rules are shifting compliance from marketing language to hard operating infrastructure. The important point for investors is that the opportunity does not primarily sit in buying battered labels. It sits in the financing, data, logistics, manufacturing and inventory-control layers that brands now need in order to keep selling into major markets.

Why This Matters

Capital repricing: Fashion's cost of capital is rising at the same time as revenue visibility is deteriorating, which means weak operators are being forced into restructurings faster than public equity valuations fully reflect.

Supply-chain control: The investable opportunity is shifting away from pure brand exposure and towards the infrastructure that manages traceability, sourcing flexibility, working capital and end-of-life product flows.

Policy as catalyst: European product regulation is no longer a soft constraint. It is becoming an operating requirement that will reward scale, clean data architecture and supplier discipline.

The Core Shift

Fashion's old model depended on three forms of cheapness: cheap money, cheap global fulfilment and cheap ignorance about what sat inside the supply chain. All three are being withdrawn. Bain's 2025 luxury update showed the personal luxury goods market moving from €369 billion in 2023 to €364 billion in 2024, with 2025 expected to be flat to slightly down at constant currency after years of aggressive price increases that alienated customers. McKinsey's luxury work made the same point differently: the sector is no longer riding a broad-based demand wave and has become much more dependent on operational precision and customer retention.

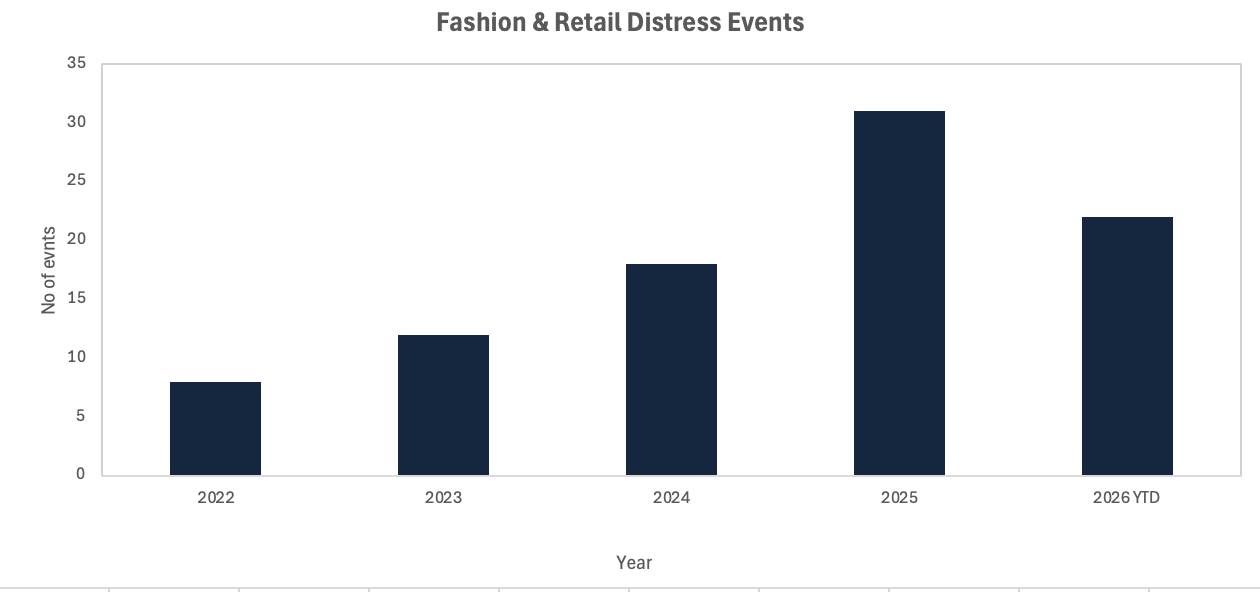

The middle of the market is under more pressure than the top. The running bankruptcy and closure trackers now show repeated stress in mall-based apparel, denim, footwear and private-equity-backed retail, where debt, lease liabilities and weaker footfall have converged. The mechanism matters. Bankruptcy in fashion is no longer simply an endpoint. It has become a tool for lease rejection, balance-sheet reset, debtor-in-possession financing and intellectual property transfer.

The count of notable distress events rose sharply into 2025, showing that this is not a single-brand problem but a broader balance-sheet event across the sector.

Source: The Fashion Law, Glossy, Business

The Non-Obvious Mechanism

Most commentary still treats fashion's stress as a consumer demand story. That is incomplete. The more useful read is that the industry's financial plumbing is being rebuilt under duress.The withdrawal of the United States de minimis exemption for low-value imports from China and Hong Kong hit the economics that helped platforms such as Shein and Temu scale in the United States, with shipments under $800 becoming subject to duties that materially change pricing and fulfilment decisions. Reuters reported that the change has already pushed bulk-shipping and warehouse restocking behaviour, which means inventory, logistics and working capital are moving back onto balance sheets instead of floating outside them.

That is where the capital reallocation sits. When tariffs become a strategic variable rather than a fixed tax, brands need more supplier redundancy, more regional manufacturing options and more cash tied up in inventory positioning. Vogue Business reported that tariffs in 2025 drove diversification into markets perceived as lower risk and turned sourcing strategy into a central board issue for 2026, which is costly. Mid-market brands with weak balance sheets cannot fund supplier diversification, compliance systems and inventory buffers at the same time. Stronger operators, specialist lenders, supply-chain technology providers and near-shore manufacturers can.

The second underappreciated mechanism is regulatory. The Digital Product Passport under the Ecodesign for Sustainable Products Regulation will make product-level traceability a practical requirement for textiles sold into the European Union, with detailed requirements expected around late 2026 or early 2027 and an 18-month compliance period thereafter. That changes the economics of the market in two ways. First, it creates an immediate spend requirement on data, certification, supplier mapping and systems integration. Second, it raises entry barriers for smaller or financially stretched brands that cannot produce compliant product information at scale.

Investor Implications

For investment professionals, the temptation will be to treat fashion distress as a classic buy-the-brand exercise. That is only selectively true. The better opportunities sit where cash-flow visibility improves as the industry becomes more complex. Three areas stand out.

Traceability and compliance infrastructure: Providers of product data management, supplier verification, testing and passport-enablement tools now face demand that is being driven by regulation rather than by discretionary brand budgets.

Near-shore and diversified manufacturing: As brands shift production to reduce tariff and logistics risk, manufacturers in countries such as Turkey, Morocco and Vietnam gain strategic relevance, especially those that can offer shorter lead times, audited processes and stronger data integration.

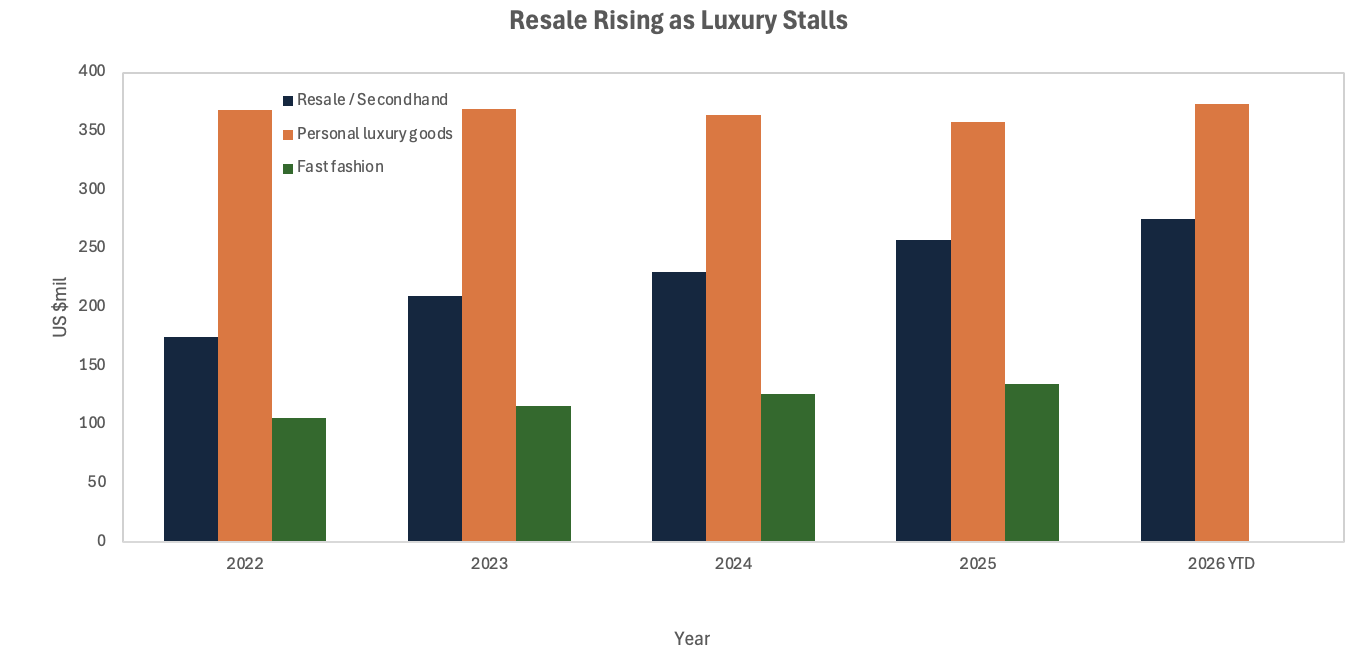

Recommerce and inventory monetisation: The global secondhand market is projected to reach $393 billion by 2030, while the United States market is expected to reach $78.8 billion by 2030, according to ThredUp's 2026 Resale Report with GlobalData. That is not a niche adjunct. It is a structural demand shift that also gives brands and intermediaries a better outlet for excess inventory and product-life extension.

Resale is growing faster than the overall apparel market while personal luxury goods have stalled. This matters because capital usually chases the brand narrative, even when the revenue momentum is shifting to secondary channels and service layers. Sources: Bain/Altagamma, ThredUp/GlobalData.

The more provocative conclusion, and one cautious sell-side analyst is less likely to state plainly, is that many quoted and sponsor-backed fashion names are no longer the natural holders of their own economics. Margin, working capital control and compliance capability are migrating away from the brand owner and towards whoever owns the systems, warehousing, financing lines and supplier relationships around it. In that sense, fashion increasingly resembles an asset-light intellectual property industry resting on a much more capital-intensive operating substrate. The hidden opportunity is to own the substrate.

Near-Term Catalysts & Policy Outlook

The next 12 months are asymmetric because policy timing is hardening just as balance sheets are weakening.

0–3 month window: The near-term focus is continued fallout from tariff and de minimis changes, plus the operating response from brands that need to rebalance sourcing and warehouse strategies quickly. The practical implication is more pressure on gross margins and higher working capital needs for businesses that previously relied on direct-to-consumer low-value parcel economics.

3–12 month window: The key watchpoints are the refinement of Digital Product Passport requirements for textiles, supplier mapping build-outs, and further distress in the mid-market as refinancing capacity narrows. The strategic divide will widen between groups that have already built compliance data architecture and those still treating regulation as a disclosure exercise.

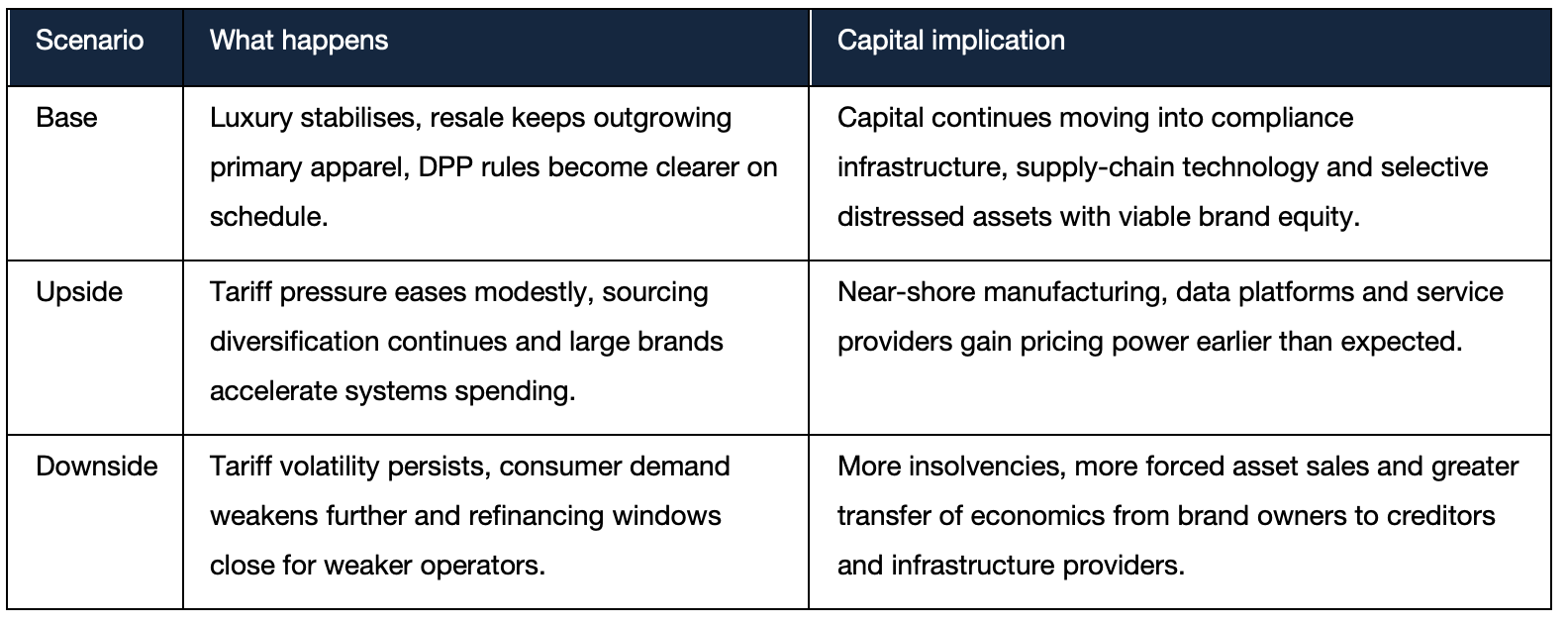

A scenario framework helps separate cyclical noise from structural direction.

Conclusion

The fashion transition trade is being mislabelled. This is not mainly a sustainability theme, nor merely a weak-consumer trade. It is a structural reallocation of capital away from undifferentiated brand owners and towards the operating infrastructure required to keep product flowing, compliant and financeable across fractured trade and regulatory regimes. The real opportunity sits where cash flows become more essential as the industry becomes less simple: traceability systems, specialist financing, near-shore manufacturing capacity, logistics control and recommerce channels.

References

Bain & Company / Altagamma – Luxury Is Ready for a New Era After Stabilizing in 2025 – 19 Nov 2025

Bain & Company / Altagamma – Spring Luxury Update reported by Fortune – 18 Jun 2025

McKinsey & Company – The State of Luxury Goods in 2025 – 12 Jan 2025

The Fashion Law – A Tracker of Retail Bankruptcies & Brand Closures – 16 Mar 2026

Vogue – The Forces That Will Shape Fashion's Supply Chains in 2026 – 5 Jan 2026

The Independent – Trump closes China tariff loophole used by fast-fashion retailers like Shein and Temu – 3 Apr 2025

Reuters – US-China trade reprieve buys Shein and Temu time to restock US warehouses – 12 May 2025

Trimco Group – What you need to know about the Digital Product Passport – accessed 2026

cyrcID – DPP for Textiles: Complete ESPR Compliance Guide 2027 – 29 Mar 2026

Retail Dive / ThredUp / GlobalData – US resale market expected to surpass $78B by 2030 – 2 Apr 2026

Harper's Bazaar – Secondhand clothing market set to be twice the size of fast fashion by 2030 – 22 Jun 2021

LinkedIn post cited for Morocco sourcing context – 16 Jul 2025

This article is for information and discussion only and does not constitute investment advice or a recommendation.