Sustainable Finance's Real Problem Is Not Greenwashing. It Is Mis-Location.

Global sustainable funds surrendered $84 billion in net outflows across 2025. The underlying transition risk those funds were meant to price did not leave with them.

The instinct is to read 2025's flow data as a referendum on environmental, social, and governance (ESG) investing as a concept. It is not. It is evidence that the product architecture built around sustainable capital has fractured, while the physical and regulatory exposures embedded in real-economy balance sheets continue to expand. The consequential question for allocators is not whether ESG is dead. It is whether the capital designed to price transition risk can still locate the risk it was meant to discipline.

Why This Matters

The $84 billion in outflows from pooled sustainable funds substantially overstates any institutional retreat from ESG conviction; much of the flow was driven by large UK institutional investors migrating from off-the-shelf commingled vehicles to bespoke segregated mandates, preserving the ESG framework while discarding the product wrapper

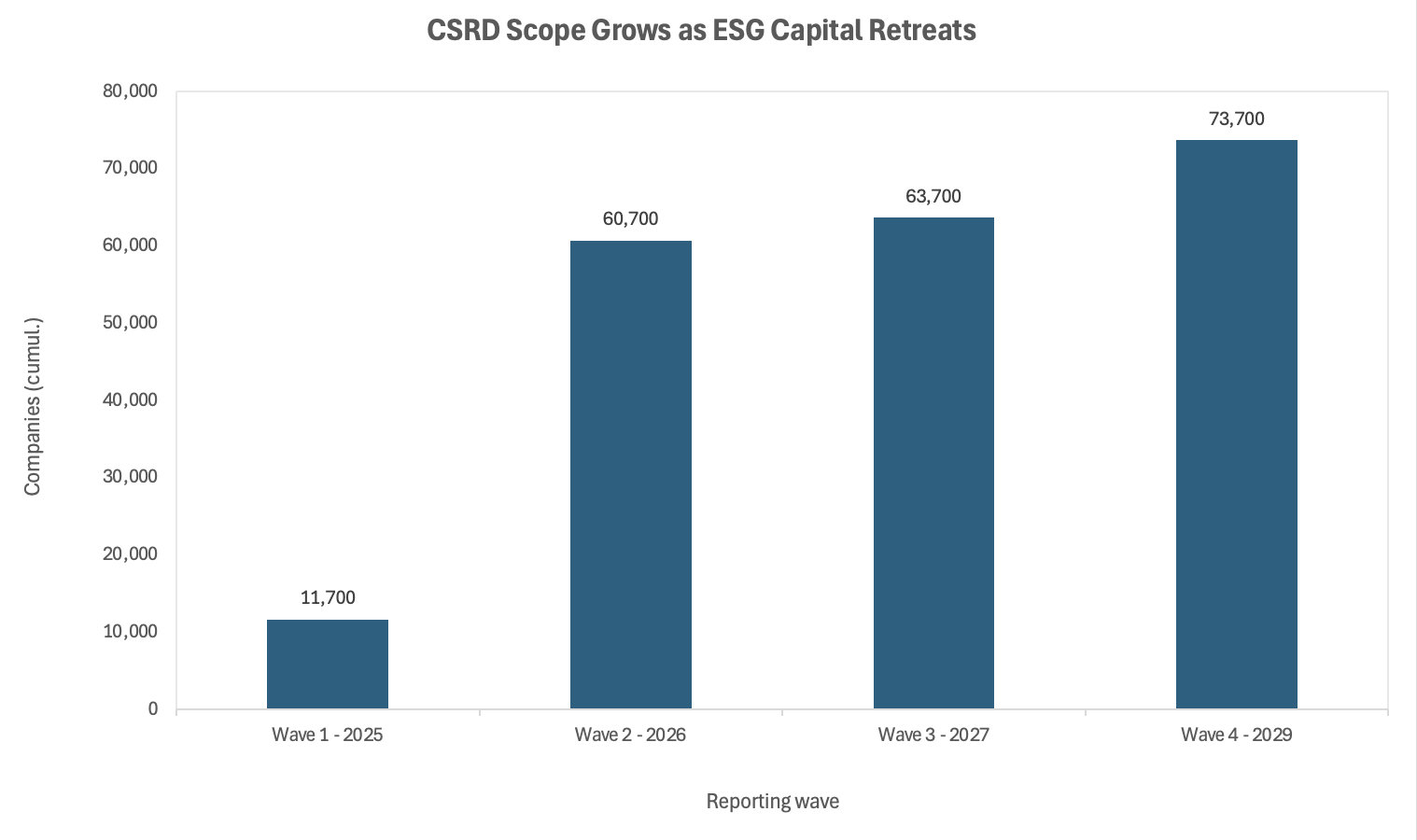

The Corporate Sustainability Reporting Directive (CSRD) Wave 2 brings approximately 49,000 large EU companies into mandatory sustainability disclosure in 2026, expanding the regulatory exposure surface at the exact moment pooled ESG capital is most visibly contracting

The consequential mis-pricing risk is not inside ESG products: it is the temporary cost-of-capital reprieve now accruing to transitional and brown assets as disciplining capital disperses into opaque structures

The Fracture Line

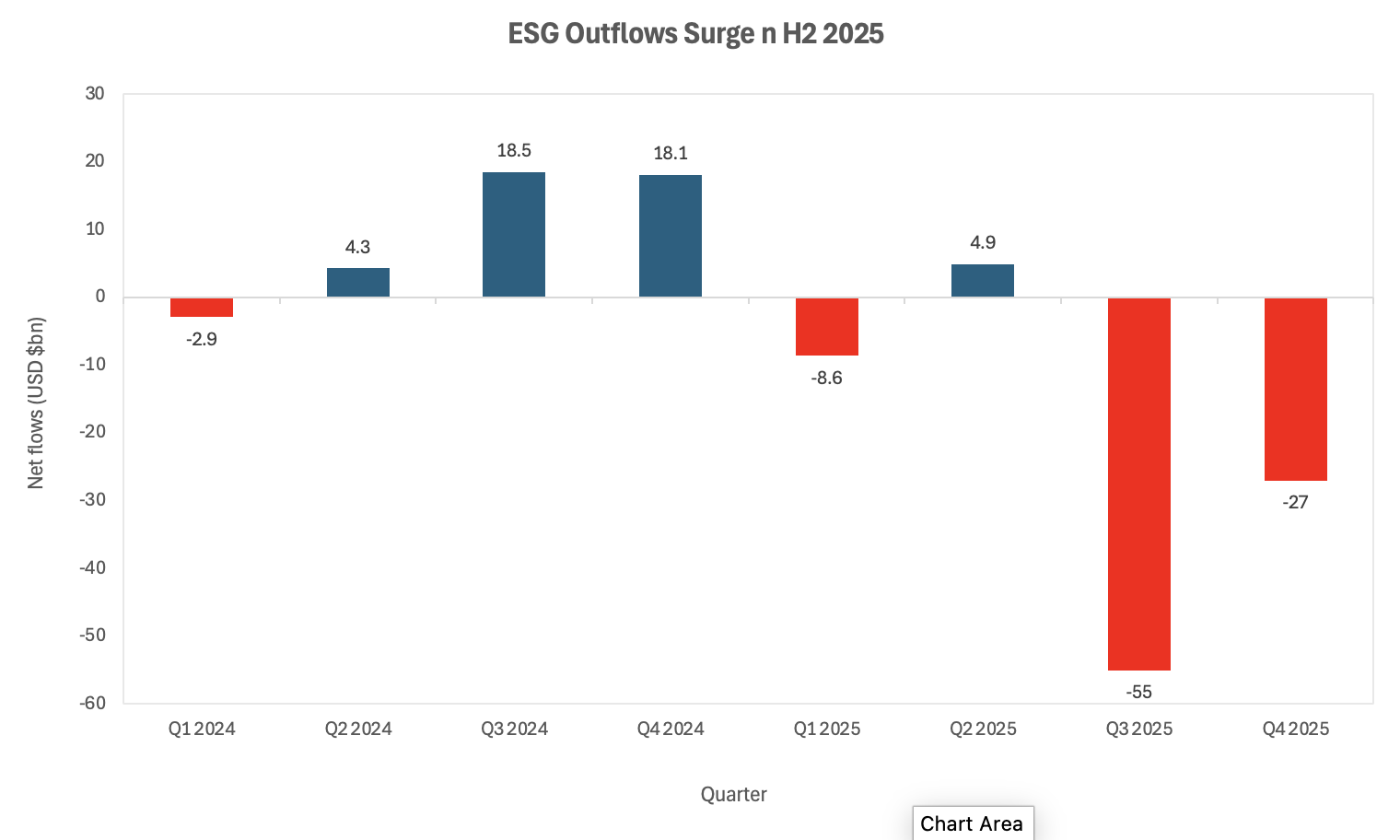

The headline figure from 2025 is unambiguous. Global sustainable open-end and exchange-traded funds registered $84 billion in net outflows for the full year, the first annual redemption since Morningstar began tracking the universe in 2018, reversing $38 billion in net inflows the prior year. The US recorded its third consecutive year of outflows. Europe, the historical anchor of sustainable finance and home to approximately 85 per cent of global sustainable fund assets, saw its first-ever annual redemption; the third quarter alone accounted for $51 billion of that figure as a wave of UK institutional redemptions landed within a single quarter.

The surface narrative attributes this to three forces: political backlash in the US following the Trump administration's rollback of climate disclosure rules and withdrawal from international climate commitments; regulatory complexity from the CSRD and the EU Taxonomy creating compliance friction; and a decade of underperformance in clean-energy equities eroding the return case for thematic sustainable funds. Each charge has some validity. None is sufficient as an explanation.

The more revealing data point lies below the headline. Morningstar's analysis confirms that Q3 and Q4 2025 outflows were substantially driven by large UK institutional investors reallocating their assets from standard pooled ESG funds into bespoke ESG segregated accounts, to gain direct control over security selection, engagement mandates, and exclusion policies. These institutions are not abandoning ESG as a risk framework. They are concluding that the off-the-shelf product wrapper no longer serves their purposes, and moving to structures that are harder to aggregate, less visible in flow databases, and free from the constraints of commingled vehicles. The reported outflow is largely a product-architecture story, not a conviction story.

Source: Morningstar – Global Sustainable Fund Flows, Q4 2025 Review

The Wrapper vs. the Risk

The distinction matters enormously for how allocators should read the signal. When institutional capital migrates from a pooled sustainable fund to a bespoke mandate, several things happen simultaneously. The capital remains broadly sustainability-oriented. But it becomes invisible to aggregate flow databases, less subject to standardised public reporting, and harder for third-party researchers to track or aggregate. The disciplining signal that pooled ESG capital sent to corporate balance sheets, via the cost-of-capital differential it helped create, diffuses.

Prior to the 2016 Paris Agreement, green and brown firms perceived their cost of capital as broadly equal. In the years that followed, green firms reported an average cost of capital approximately 100 basis points (bps) lower, a differential driven by mounting investor climate pressure. That premium was never large enough alone to drive the full energy transition. But it was a functioning market signal. As pooled ESG capital fragments and disperses into bespoke structures, the mechanism for delivering that signal weakens, precisely when the climate-physical exposure of the underlying economy is intensifying, not diminishing. Research further confirms that lowering the cost of capital for green firms, while directionally correct, produces only modest incremental emissions reductions, because these firms already operate with low emissions: the far larger lever is the pressure applied to brown assets. Removing that pressure, even temporarily, is not benign.

There is a parallel deterioration on the corporate data side. Peer-reviewed research confirms a persistent structural noise problem: companies have systematically optimised for ESG disclosure metrics rather than operational improvement, a dynamic confirmed as a durable "window-dressing effect" in recent literature. The ratings divergence across providers is well documented. Less discussed is the prior problem: the underlying data companies submit has been shaped by the incentive to score well, not to decarbonise efficiently. The information base on which capital was meant to make rational pricing decisions has been partially compromised by the very institutions that capital was designed to evaluate.

Mis-Priced and Mis-Located

The consequential portfolio question for 2026 is not where ESG capital has gone. It is where the transition risk has been left behind.

The answer sits largely on European corporate balance sheets, precisely where the CSRD is now forcing it into public view. Wave 2 of the directive covers approximately 49,000 large EU companies with more than 250 employees and either €50 million in net revenue or €25 million on the balance sheet, requiring mandatory sustainability disclosures covering fiscal year 2025, with audited reports due in 2026. Wave 1 already brought large public-interest entities with over 500 employees into scope. Together, these cohorts cover the bulk of investable European corporate credit and equity. For the first time, the quantitative sustainability exposure of these companies is mandatory, auditable, and comparable across issuers.

The mis-pricing opportunity runs in two directions.

First, assets whose ESG scores deteriorated under the current rating regime may have been incorrectly penalised. If the scoring system captured disclosure quality rather than genuine transition risk, some brown-labelled names carry lower structural exposure than their ratings imply; conversely, some green-labelled names may carry higher exposure than the premium attached to them warrants. The arrival of standardised, audited CSRD data creates a genuine re-rating catalyst, not a marginal refinement.

Second, the temporary retreat of disciplining capital has created a window. Brown assets across European energy, materials, and heavy industrials have received a mild cost-of-capital reprieve as ESG-constrained buyers exited pooled vehicles. That reprieve will narrow as CSRD data quality improves, bespoke mandates rebuild systematic frameworks, and the EU Taxonomy tightens the boundary between eligible and ineligible activities. Allocators who can identify which companies are genuinely reducing transition exposure, rather than optimising disclosure compliance, are sitting on a pricing asymmetry with a defined catalyst.

The Divergence Trade

The capital allocation signal from diverging regulatory regimes is now one of the structurally clearer trades available to a global allocator. The US and the EU are running incompatible sustainable finance frameworks, and the divergence is widening with each policy cycle.

In the US, the Trump administration has unwound climate disclosure rules, withdrawn from global climate coalitions, and signalled a durable orientation toward fossil fuel expansion. US sustainable fund outflows have been consistent across three consecutive years. The domestic regulatory framework for transition risk is, in practice, absent. For US-listed assets, transition risk is currently under-priced in public markets.

In the EU, the trajectory is the opposite. The CSRD is expanding in scope. The Carbon Border Adjustment Mechanism (CBAM) is advancing toward full implementation. The EU Taxonomy continues to define eligible activities with increasing specificity. European institutional mandates are, on balance, becoming more precise, not less demanding. The cost of non-compliance, regulatory, reputational, and financial, is rising.

Source: EU Commission – Corporate Sustainability Reporting Directive; Socious – CSRD Timeline 2026

Three scenarios frame the near-term trade.

Base - A persistent transatlantic premium: European brown assets face a structurally higher cost of capital than comparable US peers, creating a valuation discount that contains a genuine risk premium, not a free lunch.

Upside - A CSRD-driven re-rating: As Wave 2 audited sustainability data arrives in H1 2026, currently discounted European assets with credible transition plans are repriced upward as transition quality becomes verifiable rather than claimed.

Downside: Regulatory fragmentation: A material weakening of CSRD through the EU's Omnibus reform package, currently under consultation, removes the data catalyst and extends the mis-pricing window indefinitely.

The Omnibus consultation is the variable most allocators are under-weighting. If the EU dilutes CSRD scope under competitiveness pressure, the primary mechanism for converting ESG conviction into auditable balance-sheet data is delayed. The reprieve for brown assets becomes structural rather than cyclical, and the window for the re-rating trade closes before it fully opens.

Conclusion

The ESG collapse narrative is analytically convenient and structurally wrong. Capital is not abandoning transition risk as a framework; it is abandoning product structures that have proven insufficient for the task. The problem is not that investors no longer believe the transition is happening. It is that the instruments built to price it has fragmented faster than replacement architecture has emerged.

The non-consensus read is this: the withdrawal of pooled ESG capital from visible flow data is not evidence that the green cost-of-capital premium is dead. It is evidence that the premium has temporarily lost its delivery mechanism. The CSRD, for all the political turbulence around its eventual scope, is the most significant structural force working to restore that mechanism by injecting mandatory, auditable data into a market that has survived too long on voluntary, incentive-distorted disclosure.

The risk that senior allocators should hold is not that ESG is finished. It is that transition exposure has been orphaned from the capital designed to price it, and that the window of mispricing, in both directions, is wider and more persistent than current consensus allows. The trade is not about conviction. It is about information arbitrage, and the catalyst is regulatory, not political.

References

Morningstar – Global Sustainable Fund Flows: Q4 2025 in Review – February 2026

Morningstar – ESG Funds: 2025 Closes With Continued Outflows Amid Persistent Headwinds – February 2026

Morningstar – Global ESG Funds Suffer Outflows in Q1 2025 – April 2025

Morningstar – Global ESG Fund Flows Rebound in Q2 2025 – January 2026

TodayESG / Morningstar – Q3 2025 Global Sustainable Fund Report – December 2025

Singapore Green Finance Centre / Gormsen, Huber, Oh – The Effects of Financing Green and Brown Sectors – 2025

Socious – CSRD Timeline 2026: Key Deadlines Every Company Should Know – April 2026

IntegrityNext – CSRD Timeline and Reporting Deadlines – 2025

Normative – The CSRD Explained – 2025

ScienceDirect – The Contradictory Impact of ESG Performance on Corporate Governance – December 2024

Phys.org – How Greenwashing Creates False Stability for Companies – January 2026

This article is for information and discussion only and does not constitute investment advice or a recommendation.