Cognitive Capital: How AI Pricing Tiers are Quietly Restructuring Economic Advantage

The real AI divide is not about jobs. It is about who can afford to think at scale.

The public debate around generative artificial intelligence (AI) has been almost entirely consumed by questions of employment: which roles will be automated, which workers will be displaced, and which governments will intervene. That framing, while not wrong, is looking at the wrong variable. The more durable structural consequence of AI is not the elimination of labour but the stratification of cognitive capacity. Access to computation is quietly becoming a new form of capital, one whose compounding returns are already visible in pricing structures, model architectures and enterprise procurement patterns.

Why This Matters

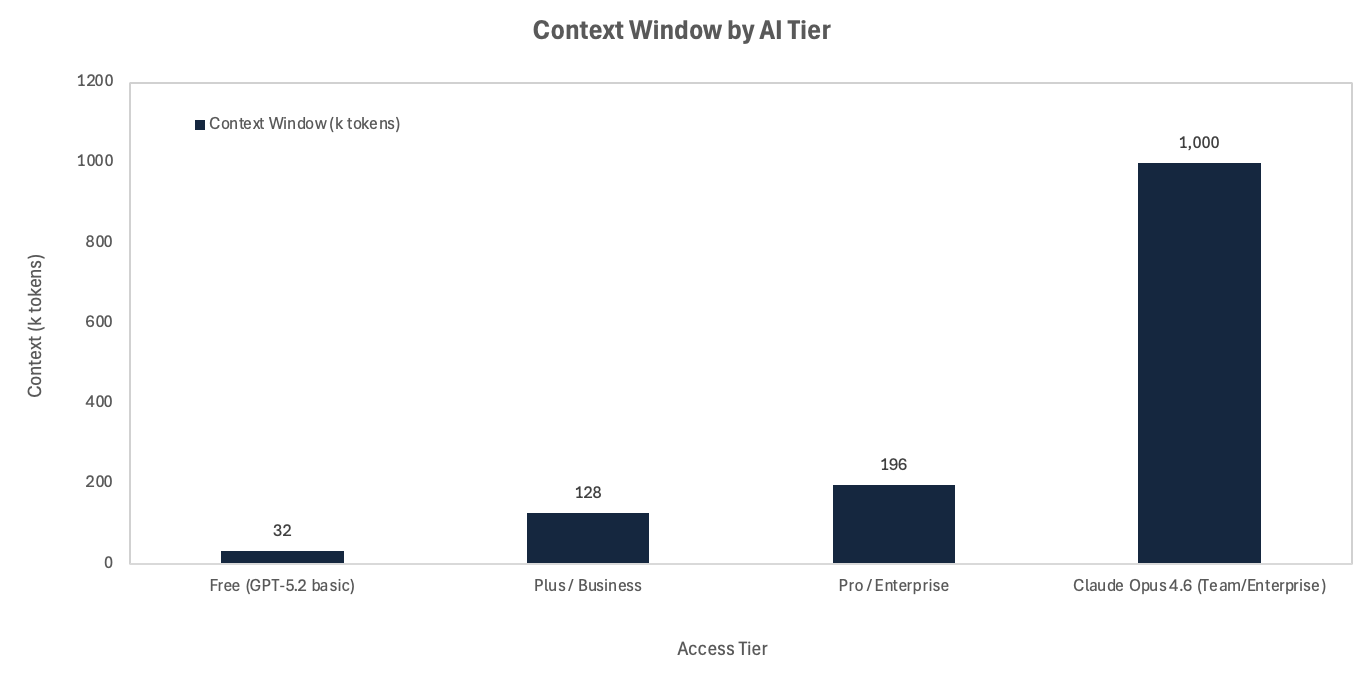

Compute access, not compute power, is the new moat: The frontier model gap between free-tier and premium users is now quantifiable. A free ChatGPT user operates on a 32,000-token context window; a Claude Opus 4.6 enterprise user runs on one million tokens. That is a 31-fold difference in how much information an intelligence system can hold and reason across simultaneously.

Compounding divergence, not linear disadvantage: The productivity gap does not scale at one-to-one. Premium access to extended context, parallel agent frameworks and faster inference creates non-linear returns. A well-resourced team running multi-agent workflows closes analytical cycles in hours that a single-session free-tier user cannot replicate in days.

Policy is at least three years behind: Regulators are still debating content moderation and model safety. The structural inequality baked into usage-based pricing tiers is not yet part of any serious regulatory agenda in the United States, European Union or United Kingdom.

The Core Shift

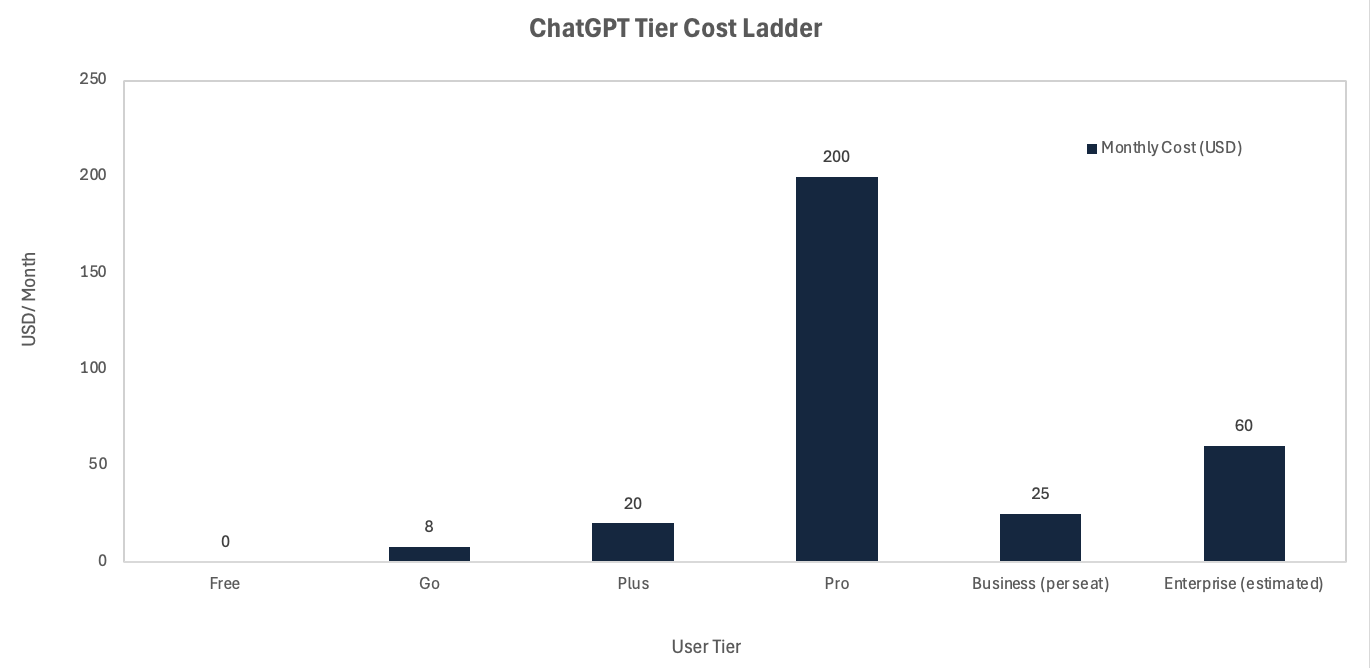

The pricing architecture of frontier AI is not incidental. OpenAI now operates seven distinct pricing tiers, from a $0 free plan to a $200 per month Pro tier, with enterprise access priced custom above a 150-seat floor. The functional gap between those tiers is not merely speed or convenience: it is cognitive depth. Enterprise plans grant access to GPT-5.5 Thinking at 196,000 tokens of context, administrative controls, data-handling guarantees, and priority inference throughput. Anthropic's Claude Opus 4.6, available at standard pricing to Team and Enterprise subscribers, introduced a one million token context window with parallel Agent Teams, enabling multiple AI agents to work simultaneously on coordinated subtasks. Free and entry-level tiers access none of this.

Source: OpenAI

The structural consequence is that cognitive throughput is now a purchased variable. A Pro or Enterprise user does not merely get the same answer faster: they get qualitatively different answers from qualitatively different reasoning processes.

The Non-Obvious Mechanism

The mechanism that consensus has not followed to its conclusion is compounding. A single premium query is marginally better than a free one. But the advantage does not accumulate linearly across a workflow. An enterprise team deploying parallel Agent Teams can decompose a complex research task, run simultaneous threads across a one million token corpus, and synthesise conclusions in a single session. A free-tier user, constrained to 32,000 tokens and sequential reasoning, must manually break the same task into fragments, losing coherence across sessions. The productivity gap compounds with every cycle. Over a quarter, the divergence in analytical output between a well-resourced AI user and an under-resourced one is likely an order of magnitude, not a percentage point.

Source: OpenAI, Anthropic

This matters beyond individual productivity. Capital allocation decisions, competitive intelligence, legal analysis, clinical research and financial modelling are all domains where context depth translates directly into decision quality. The firms and funds that have embedded premium AI into their analytical infrastructure are not simply working faster. They are reasoning over larger information sets with greater coherence. That is a durable structural advantage, and it is invisible to those who benchmark AI by headline model capability rather than by operational access tier.

Investor Implications

For institutional allocators, three implications follow directly.

Infrastructure layer as the equity-access trade: The companies building token-efficient architectures, model compression pipelines and open-source alternatives are not merely cost plays. Mistral, Meta's Llama stack and emerging fine-tuning infrastructure are, in structural terms, the democratising layer in a two-tier cognitive economy. For allocators seeking asymmetric exposure to AI's second-order effects, this is a more differentiated position than owning further upstream in the hyperscaler stack. McKinsey estimates that global data centre investment will need to reach $5.2 trillion by 2030 to meet AI demand, but the more capital-efficient opportunity may be in the compression and efficiency layer that makes compute accessible at lower cost.

Enterprise AI adoption as a balance-sheet signal: The bifurcation in business AI adoption between OpenAI and Anthropic is already measurable in enterprise procurement data. Firms embedding premium AI into core workflows are compounding analytical advantage; those still running free or Plus-tier access are not. For equity analysts, AI tier adoption should be treated as a proxy for operational leverage, not merely a cost line.

The open-source arbitrage: Meta's Llama and Mistral's model family are currently the most credible structural counterweights to premium-tier lock-in. They enable organisations with technical capacity but constrained budgets to run frontier-quality inference at near-zero marginal cost. The gap between open-source and frontier closed-source models is narrowing faster than pricing structures are falling, creating a window in which well-capitalised early movers can extract disproportionate value.

Near-Term Catalysts and Policy Outlook

The near-term risk asymmetry is skewed towards acceleration of the divide, not its closure. Pricing compression in free and mid tiers is happening, but capability expansion at the premium tier is happening faster.

0–3 month window: OpenAI's April 2026 price cuts to Business tier ($20 per seat, down from $25) signal volume acquisition at the enterprise layer, not democratisation of frontier capability. The more significant development is the general availability of Claude Opus 4.6's one million token context window at standard pricing from March 2026, which widens the functional gap between standard and premium access precisely as it removes the cost barrier at the top.

3–12 month window: Multi-agent frameworks are the next inflection. As Agent Teams and parallel reasoning become standard enterprise features, the productivity gap between tiers will widen further. Policy signal is still weak: regulatory conversations in the EU and UK remain focused on model risk and content, not access equity. The more likely read is that token access becomes a policy issue in 2027 to 2028, modelled on the broadband universal service debates of the early 2000s.

The scenario distribution for the next twelve months is as follows.

Base case: Capability differentiation between tiers widens gradually. Open-source alternatives close the gap at the mid-market level, but frontier enterprise capabilities remain behind paywalls. No meaningful regulatory intervention.

Upside: A major open-source model release (Llama 4 or equivalent) achieves near-parity with GPT-5.5 at zero marginal cost, compressing the premium tier's practical advantage and accelerating enterprise adoption of self-hosted infrastructure. Allocators positioned in the inference efficiency layer benefit disproportionately.

Downside: Regulatory fragmentation creates jurisdiction-specific access constraints, particularly in the EU. Enterprise procurement of US-origin frontier models faces compliance friction, slowing adoption and widening the capability gap between well-resourced multinational firms and domestically constrained operators.

Conclusion

The structural read is straightforward: AI is replicating the dynamics of every prior general-purpose technology, where early infrastructure advantages compound into durable economic moats before policy catches up. The cyclical noise is the pricing compression narrative, which conflates falling input costs at the commodity layer with equitable access at the frontier. They are not the same thing. The geopolitical overlay adds a further layer: compute concentration among US hyperscalers, combined with export controls on advanced chips, means that the cognitive capital divide has a national dimension as well as a socioeconomic one. For allocators, the actionable frame is not which frontier model wins, but who controls the efficiency and access layer that determines how broadly frontier capability diffuses. That layer is undervalued, under-regulated and structurally necessary. The broadband parallel is instructive: it took a decade for policy to catch up with infrastructure reality. Capital that recognises the pattern early, and positions accordingly, will not need to wait for the policy cycle to complete.

References

OpenAI – API Pricing and Tier Structure – April/May 2026

Fritz.ai – ChatGPT Pricing in 2026: Every Plan, Tier, and Hidden Cost Explained – April 2026

Finout – OpenAI Pricing in 2026 for Individuals, Orgs and Developers – 2026

Anthropic / Amplifli Labs – Claude Opus 4.6 Enterprise Release – March/April 2026

Cursor Forum – Anthropic 1M Context General Availability Announcement – March 2026

McKinsey – The Cost of Compute: A $7 Trillion Race to Scale Data Centres – April 2025

Brookings Institution – The Future of Data Centers – January 2026

MindStudio / RAMP Data – Anthropic vs OpenAI Business Adoption in 2026 – May 2026

This article is for information and discussion only and does not constitute investment advice or a recommendation.