Fiscal Signal, Not Fiscal Stimulus: How Policy Credibility Is Repricing ASEAN Manufacturing Risk

The question is no longer which ASEAN country offers the lowest labour cost. It is which government has built enough fiscal credibility to sustain the infrastructure, regulation, and carbon architecture that modern manufacturing actually requires.

Why This Matters

Divergence is accelerating: ASEAN governments are not moving together. Fiscal consolidators are cutting the capital budgets that industrial competitiveness depends on; structural spenders are building moats. The gap between the two is widening faster than FDI data currently shows.

The sorting mechanism is misread: Investors still screen on tax holidays and land costs. The real differentiator is power reliability, carbon compliance credibility, and skilled-labour pipeline: all of which are functions of sustained fiscal commitment, not one-cycle incentive packages.

Stranded industrial park risk is underpriced: A meaningful share of second- and third-tier industrial zones across the region carry occupancy assumptions built on a China+1 demand wave that is now maturing. Where fiscal support for connectivity and energy transition is absent, those valuations have not adjusted.

The Core Shift

For most of the 2010s, ASEAN fiscal policy toward manufacturing was largely permissive: special economic zones (SEZs), concessionary land, and tiered corporate tax rates were the primary instruments. Governments competed on price. The implicit assumption was that low-cost, export-oriented assembly would deliver sufficient growth to justify the foregone revenue.

That model is under structural pressure from three directions simultaneously. First, the China+1 demand wave, which accelerated sharply after 2018 and again post-2022, has raised factor costs across the front-running destinations. Vietnam's industrial land prices in the north have risen materially; Indonesia's Batam and Karawang corridors are tightening. Second, the United States tariff architecture, including the reciprocal tariff framework introduced in 2025, has created both urgency and uncertainty for manufacturers making 10-to-15-year location decisions. The investment case now requires governments to demonstrate durability, not just cost. Third, the energy transition is inserting a new cost variable: manufacturers with Scope 3 supply chain commitments cannot locate in grids where coal accounts for 60 to 70 per cent of generation without absorbing either a carbon cost or a reputational risk.

The fiscal response has been uneven. The ASEAN+3 Fiscal Policy Report 2026 documents a split between economies prioritising near-term consolidation under external financing pressure and those deploying targeted capital expenditure into the infrastructure layers that manufacturing competitiveness depends on. Malaysia, under its revised fiscal framework, and Indonesia, through the downstream industrialisation push anchored in nickel and critical minerals processing, represent the structural-spender cohort. Several smaller economies, constrained by elevated post-pandemic debt-to-GDP ratios, are trimming capital budgets precisely when the private sector needs public co-investment to de-risk long-duration commitments. The market has not yet priced this divergence cleanly. Industrial real estate yields across ASEAN remain compressed relative to the underlying policy differentiation. That mispricing will not persist.

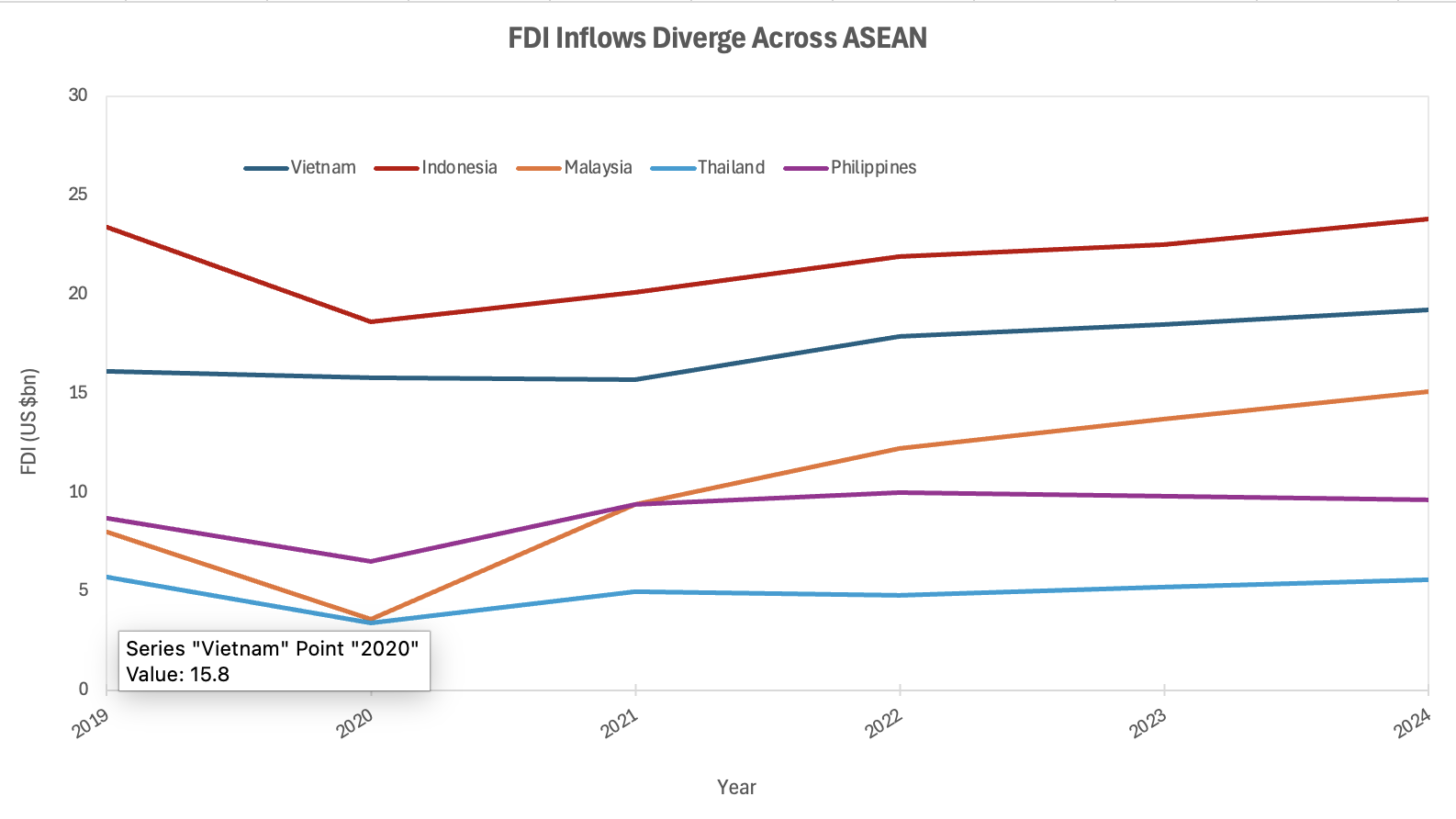

Sources: UNCTAD ASEAN Investment Report 2025; AMRO AREO 2025

Malaysia's acceleration from 2021 reflects sustained fiscal commitment to manufacturing infrastructure; Thailand and the Philippines have stagnated.

The Non-Obvious Mechanism

The conventional investor screen — tax incentive generosity, headline FDI inflows, and announced project pipelines — captures the demand side of the equation. It misses the supply-side constraint that will determine which locations retain tenants beyond the initial incentive period.

The actual sorting mechanism is tripartite. Power reliability and cost come first. Advanced manufacturing, whether in semiconductors, electric vehicle (EV) components, or precision engineering, is highly energy-intensive and increasingly requires access to credible renewable power purchase agreements (PPAs) for supply chain compliance purposes. The ASEAN Power Grid (APG) initiative has moved from aspiration to early-stage execution, with cross-border interconnection agreements signed between several member states. But grid quality at the industrial zone level is a function of domestic capital investment, and that investment is directly correlated with fiscal space and government prioritisation. Industrial parks in locations where the grid is unreliable or where renewable capacity is absent are not merely less attractive; for a growing class of multinational manufacturers, they are disqualifying.

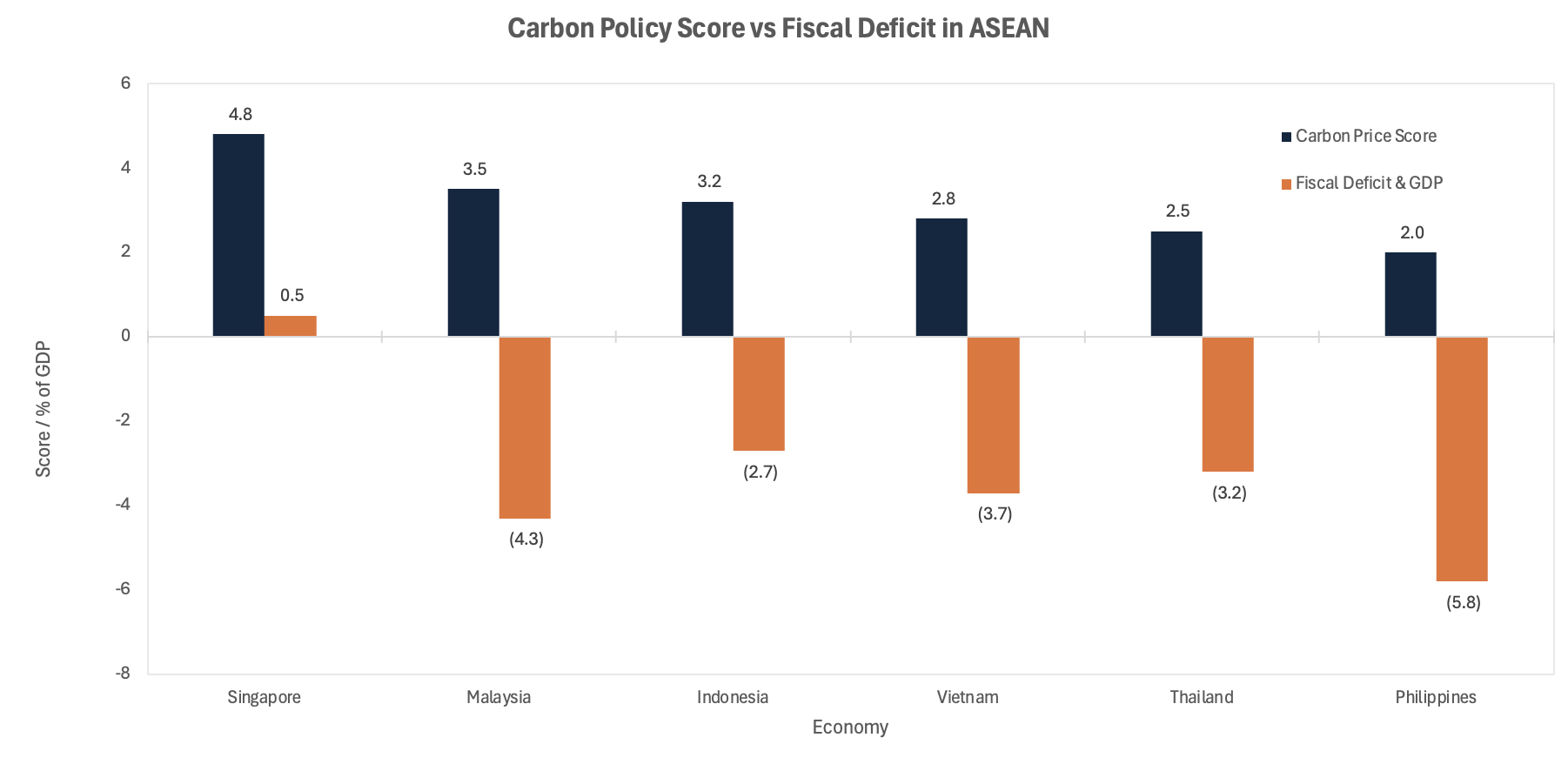

Carbon pricing credibility comes second, and this is the variable most consistently overlooked in current allocator frameworks. ASEAN carbon markets are diverging sharply. Singapore's carbon tax is on a legislated upward path. Indonesia has launched its carbon exchange. Malaysia is developing its domestic framework. Vietnam's emissions trading scheme (ETS) pilot has begun. The trajectory is clear, but the pace and credibility differ significantly by jurisdiction. A manufacturer deciding today between two industrial zones in competing jurisdictions is, in effect, making a 15-year bet on relative carbon cost trajectories. The zone in the jurisdiction with a credible, escalating carbon price will face higher near-term costs but will embed compliance infrastructure early. The zone where carbon pricing remains performative faces a cliff-edge adjustment risk later. Investors in industrial real estate have not modelled this asymmetry adequately.

Sources: AMRO Fiscal Policy Report 2026; Asian Business Review April 2026

The third leg is the skills and institutional layer. Industrial policy without the technical and vocational education and training (TVET) infrastructure to supply it with qualified workers produces stranded capital, not competitive clusters. The World Economic Forum's January 2026 cluster analysis identifies skills availability as a primary bottleneck constraining the upgrade of ASEAN industrial zones from assembly to higher-value manufacturing. Governments that are investing fiscally in this layer — Malaysia's TVET expansion, Indonesia's vocational school reform — are compounding an advantage that cannot be replicated by a competitor offering lower land costs.

Investor and Stakeholder Implications

The cash flow implications for industrial real estate holders are material and directional. Zones in fiscally credible, infrastructure-investing jurisdictions will see occupancy resilience and rent escalation capacity as tenant quality improves. Zones in under-invested locations will face a two-stage problem: first, difficulty attracting the higher-value tenants that drive rental growth; second, accelerating vacancy from existing lower-value tenants as their own customers impose supply chain compliance requirements. The stranded asset dynamic is not a tail risk; it is the central scenario for a subset of the market that is currently valued as though the China+1 wave is permanent and undifferentiated.

For infrastructure debt investors, the APG and domestic grid expansion represent genuine opportunities, but only where the fiscal and regulatory framework provides the revenue visibility required to support long-duration debt. The distinction between a government that has embedded infrastructure spending in a credible medium-term fiscal framework and one that has announced a pipeline without funding clarity is the entire investment case. Spread compression in the former is justified; in the latter, current pricing does not compensate for execution risk.

The balance sheet absorbing the transition risk in the stranded scenario is diffuse but identifiable: domestic bank lenders to industrial developers, pension funds with unlisted infrastructure exposure, and the sovereigns themselves through contingent liabilities on state-linked industrial entities. None of these balance sheets are currently reserving for the scenario where a material share of second-tier industrial zone capacity becomes economically unviable within a 10-year horizon.

Near-Term Catalysts and Policy Outlook

The risk asymmetry over the next 12 months is skewed toward negative surprises for the consensus position. The consensus is broadly constructive on ASEAN manufacturing FDI as a structural theme; the downside scenario is underweighted.

0–3 month window: The US tariff negotiation posture toward ASEAN remains live and asymmetric. Countries with larger bilateral trade surpluses, notably Vietnam, face continued pressure. Any deterioration in the tariff framework would accelerate the differentiation between locations with deep domestic and regional demand linkages and those dependent on trans-Pacific export models. Fiscal responses to external shocks in this window will be the first revealed signal of which governments have genuine policy space.

3–12 month window: The AEC Strategic Plan 2026–2030, adopted in May 2025, contains specific commitments on energy connectivity and digital infrastructure. Delivery against these commitments, or the absence of it, will begin to show in capital budget allocations and project announcements by Q3 2026. Carbon market developments in Vietnam and Indonesia will also reach decision points that reveal the credibility gap between stated policy and funded implementation.

The three scenarios below are not symmetric: the base case requires policy execution to proceed roughly as signalled, while both the upside and the downside hinge on a single variable moving faster than consensus expects.

Base case: Fiscal divergence continues at a gradual pace. Front-runners, principally Malaysia, Vietnam's tier-one zones, and Indonesia's downstream industrial corridors, retain the bulk of quality FDI. Second-tier locations experience slower absorption but do not face acute vacancy crises within a two-year horizon. Carbon and grid costs begin to differentiate tenant economics but have not yet forced repricing of industrial real estate valuations.

Upside: Accelerated APG interconnection agreements and a credible regional carbon border adjustment framework create a clear tiering of investment destinations. Capital reallocates toward the structural winners faster than the base case; infrastructure debt spreads compress in high-credibility jurisdictions. The more likely read in this scenario is that the winners gain at the expense of the middle tier, not the bottom.

Downside: A deterioration in the US trade framework toward ASEAN, combined with fiscal slippage in one or more front-runner economies, triggers a reassessment of the structural case. Industrial real estate valuations in over-supplied corridors correct. Domestic bank exposure to industrial developers becomes a regional financial stability question. This scenario is not the consensus, but it is not adequately priced in current spreads.

Conclusion

The structural case for ASEAN manufacturing is intact, but it has become a stock-picker's market at the sovereign level. The era of undifferentiated exposure to the China+1 theme is over. What replaces it is a framework in which fiscal credibility, energy transition execution, and carbon policy coherence are the primary variables determining which industrial locations compound value and which become liabilities on someone's balance sheet.

The cyclical read-across from trade disruption is a secondary consideration. Tariffs create urgency for relocation decisions; they do not determine quality of destination. Geopolitically, the US-China structural tension is durable enough that ASEAN retains its strategic relevance as a manufacturing corridor for another decade. The question is purely allocative: which jurisdictions within the region have used this window to build defensible industrial infrastructure, and which have harvested the FDI inflow without funding the foundations beneath it.

The answer is already visible in the fiscal data. The market has simply not finished reading it.

References

ASEAN Secretariat — AEC Strategic Plan 2026–2030 — May 2025

AMRO — ASEAN+3 Fiscal Policy Report 2026 — April 2026

AMRO — Strengthening Fiscal Management Amid Emerging Headwinds — April 2026

World Economic Forum — Industrial Transformation in ASEAN: A Cluster-Driven Model — January 2026

World Economic Forum — How Industrial Clusters Can Power ASEAN's Low-Carbon Future — January 2026

Lowy Institute — Resilience in a Conditional Trade Order: ASEAN's 2026 Challenge — April 2026

ASEAN Secretariat — ASEAN's Power Grid: The Next Investable Infrastructure Opportunity — March 2026

Asian Business Review — ASEAN Carbon Markets Diverge as Policy Turns to Execution — April 2026

Source of Asia — ASEAN's Role in Global Supply Chain Rebalancing — March 2026

UNCTAD — ASEAN Investment Report 2025 — October 2025

This article is for information and discussion only and does not constitute investment advice or a recommendation.