The Dual-Infrastructure Trap: Why ASEAN's AI and Manufacturing Boom Is Built on an Energy Fault Line

Capital is flowing into ASEAN at record pace. The energy system that must sustain it is not keeping up.

ASEAN is positioning itself as the world's next great node for artificial intelligence (AI) infrastructure and advanced manufacturing. Foreign direct investment (FDI) is surging, hyperscalers are signing gigawatt-scale electricity supply agreements, and semiconductor firms are extending supply chains from Johor to Ho Chi Minh City. The region's digital economy is projected to reach $2 trillion by 2030. Yet beneath this headline momentum lies a structural fault line that most capital allocation frameworks have not yet fully priced: the infrastructure being built to handle tomorrow's compute loads and manufacturing throughput runs, in large part, on a power grid that is still predominantly coal and gas fired, chronically under-invested, and years behind the demand curve.

Why This Matters

Divergence is accelerating: ASEAN governments are not moving together. Fiscal consolidators are cutting the capital budgets that industrial competitiveness depends on; structural spenders are building moats. The gap between the two is widening faster than FDI data currently shows.

The sorting mechanism is misread: Investors still screen on tax holidays and land costs. The real differentiator is power reliability, carbon compliance credibility, and skilled-labour pipeline — all of which are functions of sustained fiscal commitment, not one-cycle incentive packages.

Stranded industrial park risk is underpriced: A meaningful share of second- and third-tier industrial zones across the region carry occupancy assumptions built on a China+1 demand wave that is now maturing. Where fiscal support for connectivity and energy transition is absent, those valuations have not adjusted.

The Core Shift

The structural driver is well established: supply chain reconfiguration triggered by US-China tension, accelerated by the post-pandemic rethink of single-source dependency, and now deepened by the AI arms race. ASEAN is the net beneficiary. The ASEAN-6, namely Indonesia, Malaysia, the Philippines, Singapore, Thailand, and Vietnam, are rapidly positioning themselves as critical nodes in the global AI and compute ecosystem. Singapore anchors chip design, financing, and high-value research and development (R&D). Malaysia, particularly the Johor corridor, has emerged as the hyperscale absorber for demand that Singapore's land and power constraints cannot accommodate. Vietnam and Thailand are consolidating semiconductor packaging and testing; Indonesia, with its vast resource base and domestic market, is building the foundations of a broader digital supply chain.

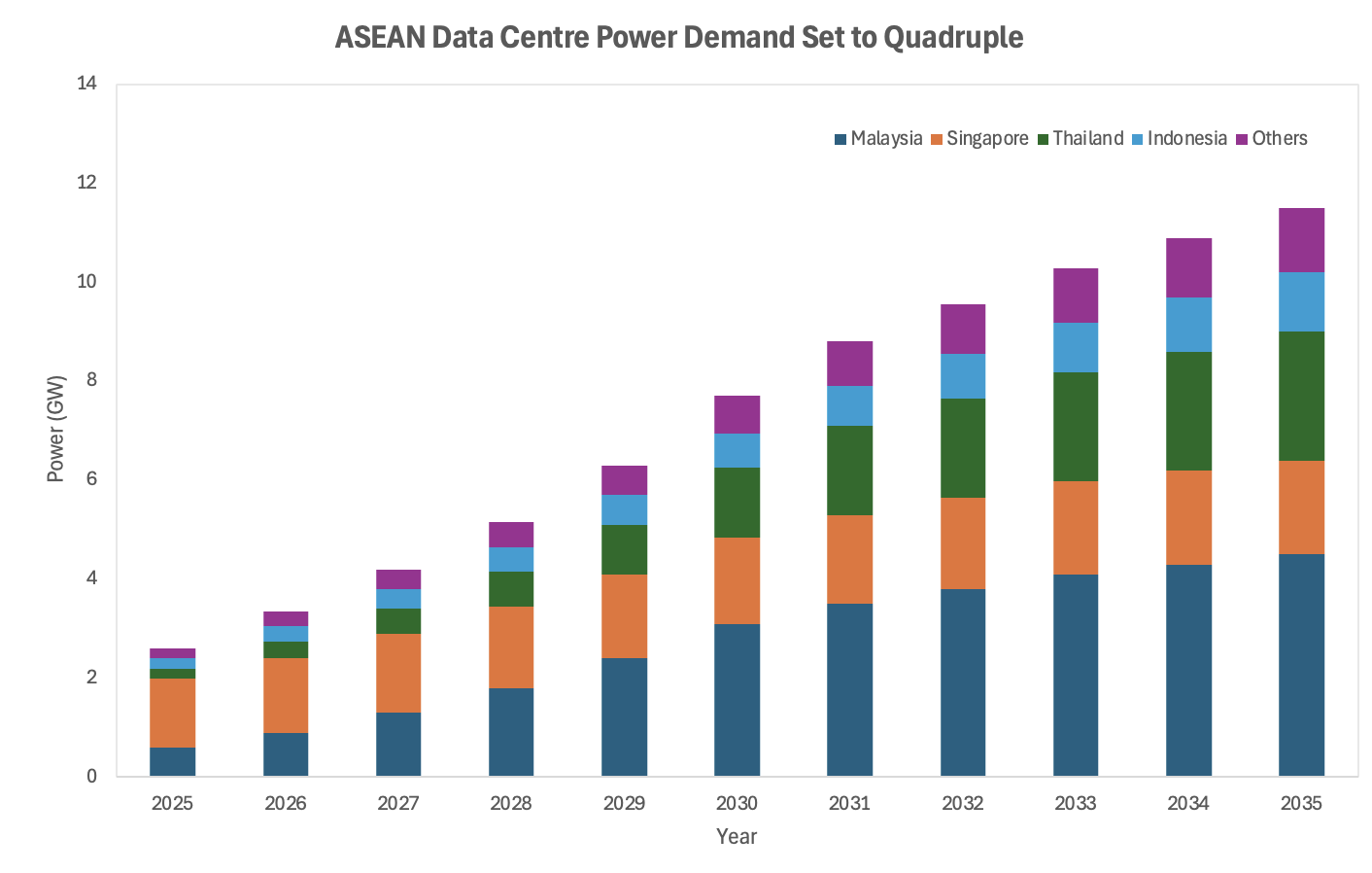

The numbers are unambiguous. As of September 2025, Malaysia's state utility Tenaga Nasional Berhad (TNB) had signed 49 electricity supply agreements with data centre developers, representing 7.1 GW of future demand. By 2030, official projections put Malaysian data centre electricity demand at 7.7 GW; by 2040, as much as 20.9 GW. Data centres now consume 3% of electricity on Malaysia's Peninsular grid, a threefold increase in a single year. This is not a pipeline story. Construction is underway, power is being drawn, and the grid is already responding.

Simultaneously, ASEAN's manufacturing story is being rewritten. Electronics, semiconductors, and advanced assembly are integrating into a more coordinated regional ecosystem, with companies that previously treated individual ASEAN markets as standalone destinations now building cross-border supply chains. AI could uplift ASEAN gross domestic product (GDP) by 10–18%, equivalent to up to $1 trillion, by 2030. The two booms, digital infrastructure and manufacturing, are converging. Both are electricity-intensive. Neither can be sustained without a reliable, affordable, and increasingly clean power supply.

The Non-Obvious Mechanism

The consensus framing treats the energy constraint as a delivery risk: will there be enough power? The more consequential read is structural: the energy system's current composition actively undermines the investment thesis for both booms.

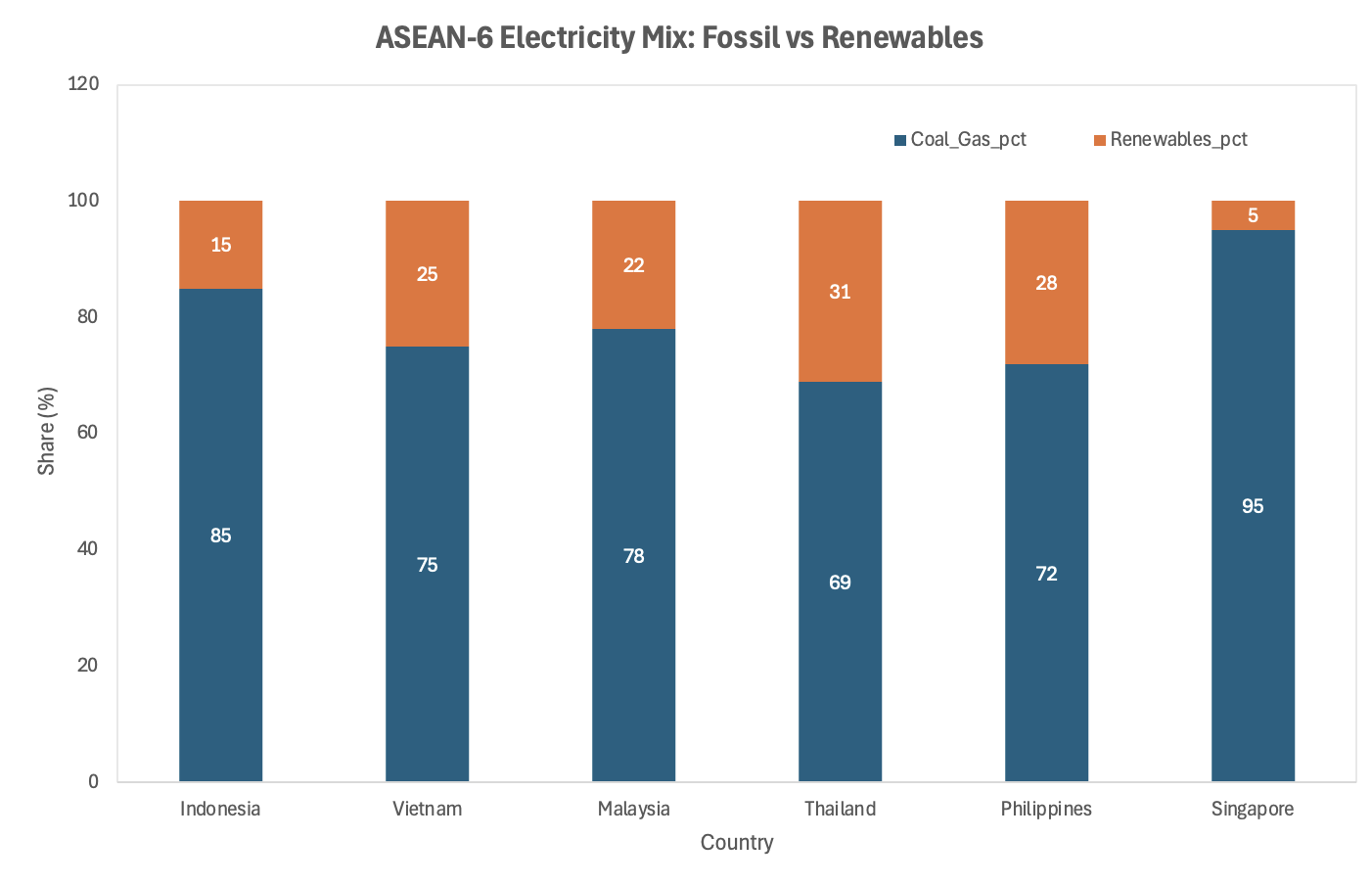

Consider the hyperscaler position. Microsoft, Google, and Amazon have net-zero commitments. Their data centres in ASEAN are being served, today and for the foreseeable future, by grids that are over 70% fossil-fired across most of the ASEAN-6. Over 70% of Southeast Asia's electricity comes from coal and gas. Malaysia's grid is dominated by coal and gas; the Philippines and Indonesia are similarly exposed. Singapore, ironically, is among the most fossil-dependent at approximately 95% gas generation, though it imports its constraints rather than generating them locally.

Source: Ember, Energy Tracker Asia

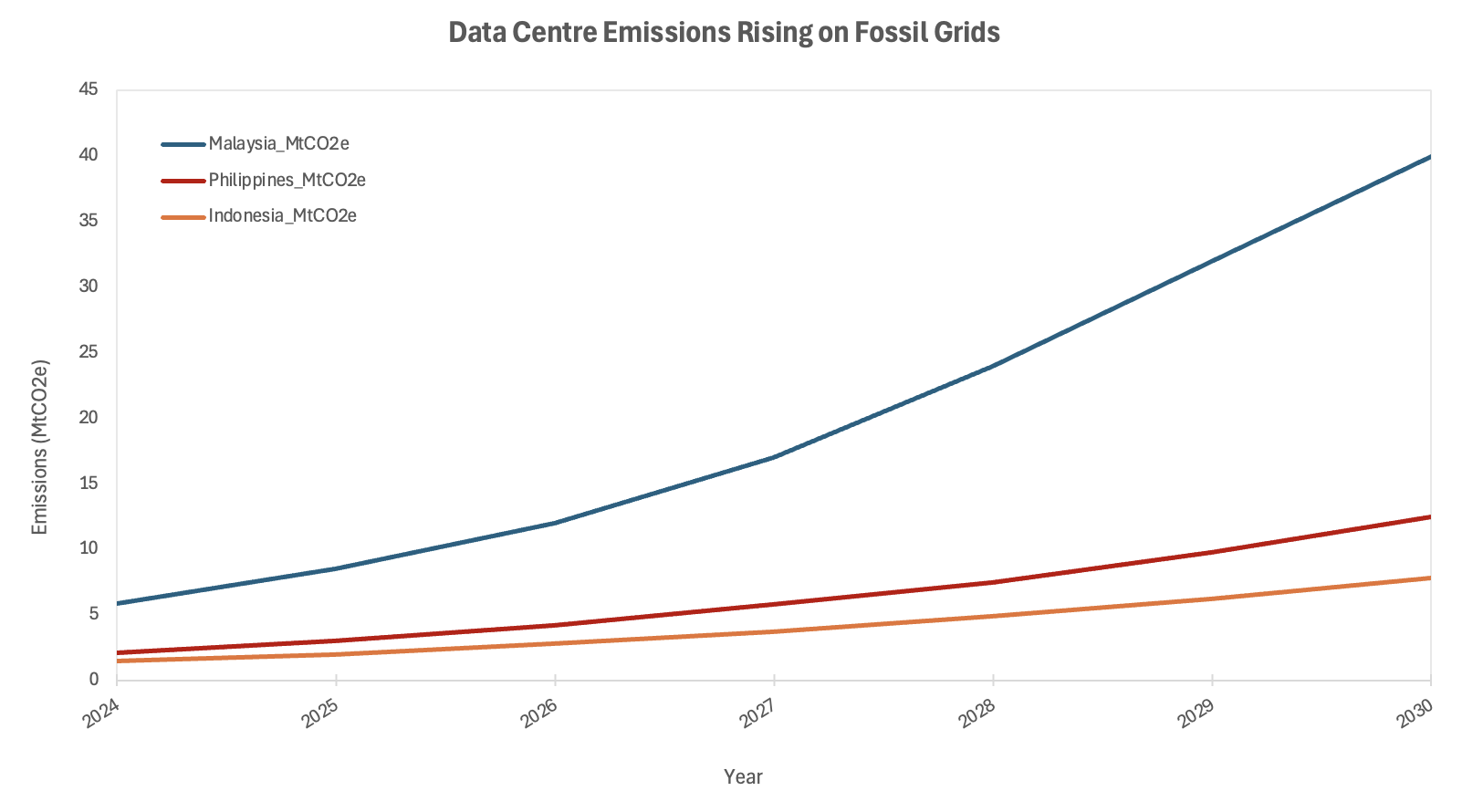

The emissions consequence is not abstract. Without decisive intervention, Malaysia's data centre sector alone could generate 40 MtCO2e annually by 2030, a sevenfold increase from 5.9 MtCO2e in 2024. The Philippines and Indonesia face proportionally similar trajectories given their coal-heavy generation mix. ASEAN's AI-driven surge in data centre electricity demand is forecast to add up to 80 terawatt-hours (TWh) annually by 2030 without clean energy access, risking a direct lock-in of coal and gas-based emissions at scale.

Source: Ember Energy 2025

The second-order mechanism that consensus has not followed to its conclusion is this: if hyperscalers cannot credibly demonstrate that their ASEAN facilities run on clean energy, the investment rationale for siting AI infrastructure here weakens. The region risks winning the data centre race on cost and geography, only to lose it on sustainability credentials within a five-year window as corporate carbon accounting tightens. The trap is not that the power fails. It is that the power discredits the asset.

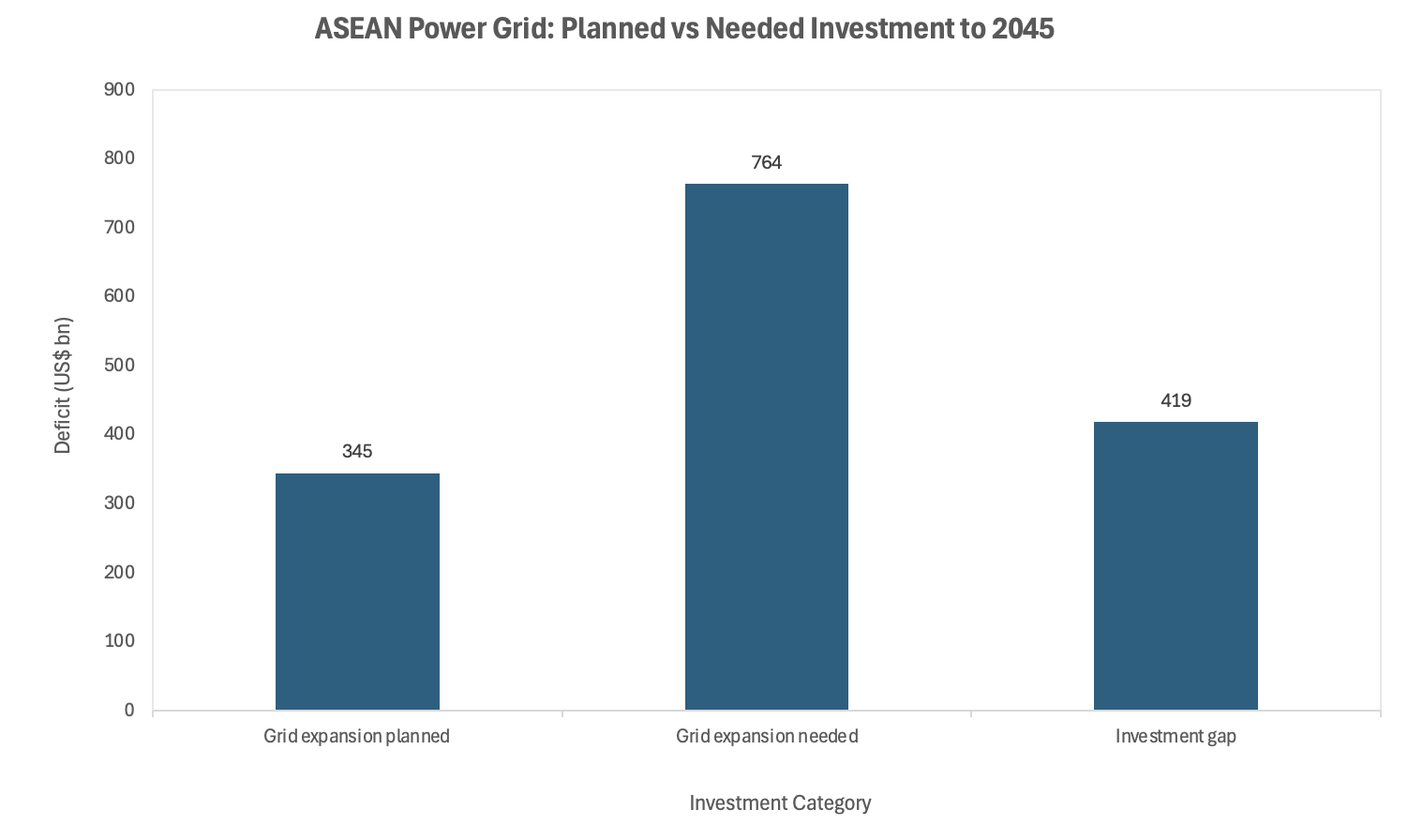

For manufacturing, the mechanism is distinct but structurally related. Energy-intensive advanced manufacturing, whether in semiconductor fab, electric vehicle (EV) components, or precision engineering, requires not just power availability but price predictability and grid reliability. ASEAN's transmission infrastructure covers only 45% of the scale needed to facilitate the energy transition. A grid that cannot integrate variable renewable energy (VRE) at scale is also a grid that cannot guarantee the stable, uninterrupted supply that advanced manufacturing requires. The fault line runs under both investments simultaneously.

Investor and Stakeholder Implications

The capital allocation read-across from this structural tension is layered. For direct infrastructure investors, the near-term opportunity is clear and the risk is manageable: data centre real estate investment trusts (REITs), hyperscale operators, and colocation providers are signing long-term power purchase agreements (PPAs) and absorbing the carbon liability onto their own balance sheets rather than waiting for grid decarbonisation. This is rational in the short term but creates concentrated exposure to future carbon pricing, regulatory shifts, and reputational risk as corporate sustainability reporting tightens under International Sustainability Standards Board (ISSB) and EU Corporate Sustainability Reporting Directive (CSRD) frameworks.

Source: Wood Mackenzie 2025

The more interesting risk sits one layer back: in the utilities and grid operators. TNB in Malaysia is signing supply agreements faster than it can deliver clean generation behind them. The path of least resistance, extending the operational life of existing coal and gas plant rather than accelerating retirement, is the most likely near-term outcome unless policy forces the contrary. Malaysia has committed to halving coal capacity by 2035 and retiring it entirely by 2044. That timeline is ambitious given the current data centre demand trajectory. A delay to coal retirement of even three to five years would materially alter both the emissions profile and the cost structure of the Peninsular grid.

Vietnam's revised Power Development Plan 8, launched in April 2025, targets 74% renewable energy installed capacity by 2050 through offshore wind, rooftop solar, battery energy storage systems (BESS), and nuclear power. The ambition is credible; the execution risk is high. Grid infrastructure in Vietnam remains constrained, and the country's data localisation regulations are simultaneously driving demand for domestic data centre capacity before the grid can support it cleanly.

For private equity and infrastructure funds, the risk-adjusted opportunity is in the seam between digital demand and energy supply: grid-scale battery storage, cross-border transmission infrastructure, and corporate PPAs for industrial and hyperscale offtakers. These are bankable structures where the demand signal is firm and the policy direction, even if uneven, is broadly supportive. The ASEAN Power Grid (APG) Financing Facility and the push for a Submarine Power Cable Framework are translating regional ambition into investable structures, albeit slowly. Investors who can work across jurisdictions and absorb the regulatory fragmentation premium will find limited competition.

For manufacturing-focused strategic investors, the energy constraint should already feature in site selection criteria. A factory in Johor drawing power from a coal-heavy peninsular grid is not simply a carbon liability; it is exposed to rising carbon border adjustment mechanism (CBAM) costs as the European Union's instrument matures and other markets follow. The more likely read is that energy sourcing will become a site selection variable of comparable weight to labour cost and logistics within the next three to five years.

Near-Term Catalysts and Policy Outlook

The asymmetry of risks over the next 12 months is skewed to the downside for incumbents and to the upside for those already positioned in clean infrastructure. The pace of demand is outrunning the pace of clean supply, and the gap is widening quarterly.

0–3 month window: The Philippines assumes the ASEAN Chairmanship in 2026, with Singapore to follow in 2027. Both terms will shape the operational architecture of the APG and the pace of cross-border transmission development. Near-term focus will be on the Lao PDR-Thailand-Malaysia-Singapore Power Integration Project Phase 2, currently doubling maximum capacity to 200 MW across two simultaneous routes. Any acceleration in this bilateral framework, or formal endorsement of the Submarine Power Cable Framework, would be a positive signal for cross-border renewable investment.[14][15]

3–12 month window: The ASEAN Plan of Action for Energy Cooperation (APAEC) 2026–2030, endorsed in October 2025, sets targets of a 40% reduction in energy intensity, a 30% renewable energy share in total primary energy supply (TPES), and 45% renewable energy share in installed power capacity by 2030. The distance between these targets and the current trajectory, where coal covered approximately 35% of incremental demand growth through 2026 and renewables only 40%, means that the targets function more as policy anchors than binding commitments. The critical watch point is whether Malaysia, Indonesia, and Vietnam move to enforce cleaner generation standards on new data centre connections, or continue to allow fossil-backed supply agreements in exchange for investment attraction.

The direction of policy is broadly set; the speed of execution is not. Whether ASEAN closes the clean energy gap in time to sustain its AI and manufacturing investment thesis hinges less on targets than on the decisions governments make in the next 12 to 18 months on grid access rules, PPA frameworks, and the pace of coal retirement. Three outcomes are plausible from here.

Base case: Grid decarbonisation lags demand by five to seven years. Malaysia and Vietnam expand gas generation as a bridging fuel, partially satisfying hyperscaler clean energy requirements through bundled renewable energy certificates (RECs) and offshore PPAs rather than physical clean delivery. Emissions from the data centre sector rise sharply through 2028 before plateauing as new solar and wind capacity comes online. The investment case for ASEAN AI infrastructure remains intact but increasingly dependent on corporate carbon accounting conventions rather than actual grid decarbonisation.

Upside: A combination of policy-driven corporate PPA frameworks, accelerated APG interconnection, and falling offshore wind costs in Vietnam and the Philippines enables material clean energy access for data centres by 2028–2029. BESS deployment at scale provides the grid stability needed for advanced manufacturing, and ASEAN captures a meaningful share of the "clean AI" narrative that hyperscalers need for their own net-zero reporting. This is possible but requires regulatory coordination that ASEAN has historically found difficult to execute at speed.

Downside: Carbon border adjustment mechanisms from the EU and potentially from Japan and South Korea materialise faster than ASEAN grids can decarbonise. Several hyperscalers pause new capacity commitments pending clean energy assurances, triggering a partial slowdown in data centre FDI. Simultaneously, a cyclical oversupply of data centre capacity in Johor, already a risk given speculative pipeline volumes, forces write-downs. The energy fault line becomes the narrative frame through which ASEAN's broader investment story is reassessed.

Source: CFA Institute/ ASEAN Study, 2026

Conclusion

ASEAN's dual boom in AI infrastructure and advanced manufacturing is structurally sound in its demand logic but operationally vulnerable in its energy foundation. The region is not facing a sudden crisis; it is accumulating a slow-building exposure that will not register on quarterly earnings calls but will reshape capital allocation frameworks over a five-to-seven-year horizon.

The structural read is this: ASEAN is not in a typical infrastructure cycle where demand eventually pulls supply into equilibrium. It is in a race between two competing lock-in dynamics. The first is the lock-in of fossil fuel capacity, extended by data centre demand that cannot wait for the clean grid that does not yet exist. The second is the lock-in of clean infrastructure, enabled by falling technology costs, rising policy pressure, and the commercial necessity of hyperscalers to credibly claim carbon neutrality. Which dynamic wins will determine whether ASEAN's position in the global AI economy is durable or contingent.

The geopolitical overlay sharpens the argument. The US-China supply chain fracture is driving capital into ASEAN regardless of the energy constraint. That creates a short window, perhaps three to five years, in which ASEAN governments can define the terms under which digital infrastructure is built. Enforce clean energy requirements now, and the region builds a durable competitive position. Defer to investment attraction at any cost, and the energy fault line becomes the story.

The investors who will benefit are not those betting on the boom. They are those who have understood that the boom's bottleneck is the grid, and have positioned accordingly.

References

ASEAN Exchanges – AI & Compute Infrastructure: Building ASEAN's Digital Backbone – March 2026

Ember Energy – From AI to Emissions: Aligning ASEAN's Digital Growth with Energy Transition Goals – May 2025

Wood Mackenzie – Southeast Asian Data-Centre Power Demand Is Set to Explode – December 2025

TransitionZero – Malaysia Data Centres: Can Clean Energy Keep Up? – February 2026

Energy Tracker Asia – Data Centres at a Crossroads: Clean Power or Carbon Risk? – June 2025

CFA Institute – How Investors Are Backing Energy Connectivity Across ASEAN – April 2026

World Economic Forum – Building Energy Integration into Regional Power Systems – February 2026

ASEAN Secretariat – ASEAN Guide for Sustainable Data Centre Development – December 2025

APERC – Coal Report 2025 – February 2026

ASEAN Centre for Energy – APAEC 2026–2030 Endorsement – October 2025

Mott MacDonald – Embracing Responsible AI to Transform Infrastructure Development in ASEAN – December 2025

TNB / The Star – ASEAN Power Grid to Drive the Region's Next Chapter – March 2026

Morgan Stanley – Powering AI: The 100GW Opportunity – 2026

Geopolitical Monitor – ASEAN's 2026 Bottleneck: Policy Shocks and Power Limits – January 2026

This article is for information and discussion only and does not constitute investment advice or a recommendation.