Water Is the New Export Control – Why Hydro‑Geopolitics Will Redraw the Agri and Mining Value Chain

Author: Justin Kew

Water is shifting from a background input to an explicit constraint on trade, industrial location and national security, with a trajectory that will push water‑rich jurisdictions to behave more like energy exporters – and water‑poor ones to treat agri and mining supply chains as strategic vulnerabilities.

Executive framing

The combination of climate volatility, depleting aquifers and politically salient droughts is turning physical water availability into a de facto export control on water‑intensive goods, from soy and beef to copper and lithium. As basins cross ecological thresholds, governments are beginning to ration water between food security, domestic consumption, energy and export sectors, often under public pressure and with little warning. The result is a slow but powerful rewiring of where high‑water‑content value is created, which balance sheets bear hydrological risk, and how “secure” agri and energy transition metals really are.

Why this matters

Water‑stress trajectories will re‑order comparative advantage in agriculture and mining faster than most cash‑flow models assume.

Hydro‑geopolitics is shifting from river‑basin disputes to implicit controls on “virtual water” embedded in traded crops and metals.

Capital mis‑pricing will emerge where earnings depend on stressed basins but risk premia are still set on country or commodity, not catchment.

What is changing

A structural rise in water stress

UN and FAO data show that agriculture accounts for around 70–72% of global freshwater withdrawals, making it the dominant claimant on finite resources. Climate change is tightening this constraint by reducing renewable water in many regions through altered rainfall, glacier retreat and more frequent droughts, while episodic floods damage storage and conveyance infrastructure rather than easing chronic scarcity.

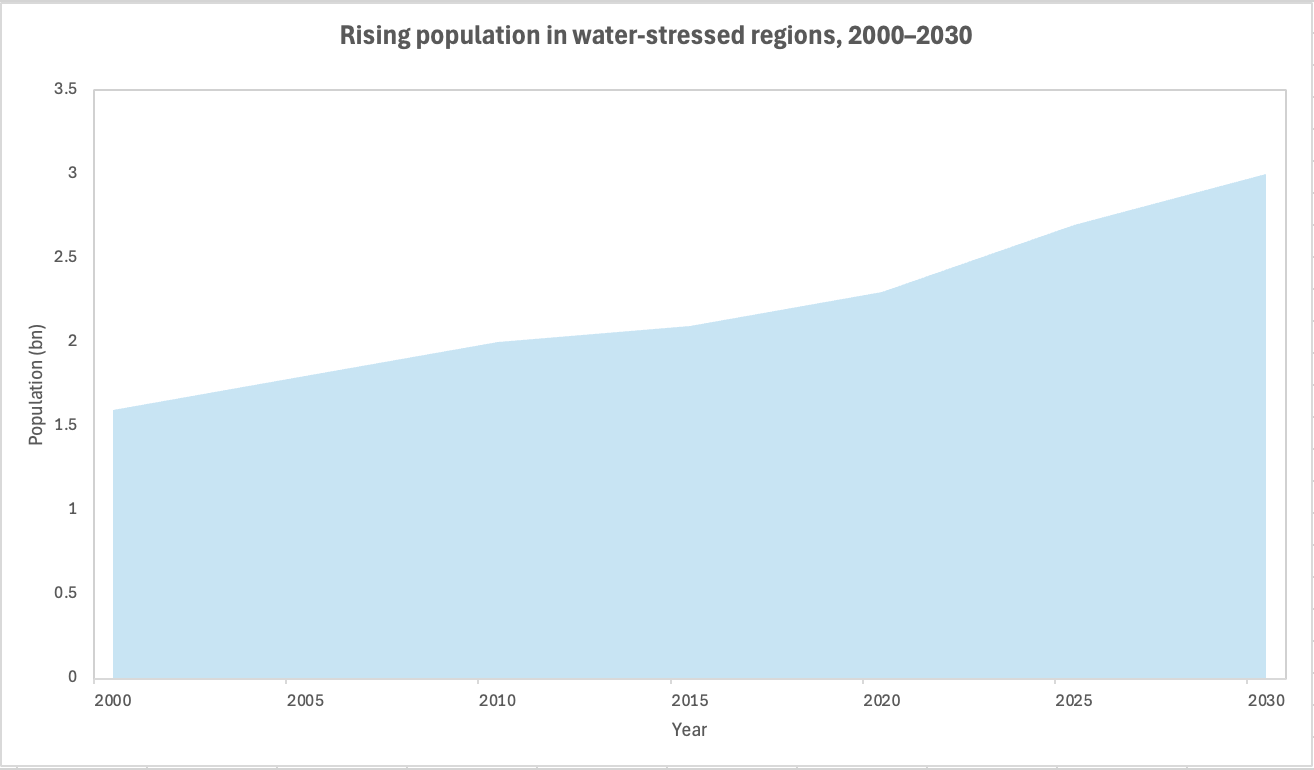

Chart 1: Projected growth reflects increasing scarcity concerns. The number of people living in water-stressed regions is projected to almost double between 2000 and 2030

UN assessments suggest that the population living in water‑stressed regions could almost double between 2000 and 2030, from roughly 1.6 to about 3.0 billion people. As stress rises, governments in regions such as southern Europe, North Africa and parts of South America are already imposing water‑use restrictions that hit irrigated agriculture, hydropower, and industrial users simultaneously.

Water‑intensive export models under pressure

Many agri exporters rely on effectively exporting “virtual water” – the water embedded in crops and livestock – from increasingly stressed basins. At the same time, mining and processing for energy transition materials (copper, lithium, nickel) depend on stable access to water for ore processing, dust suppression and, in the case of brine lithium, for the evaporative concentration process itself.

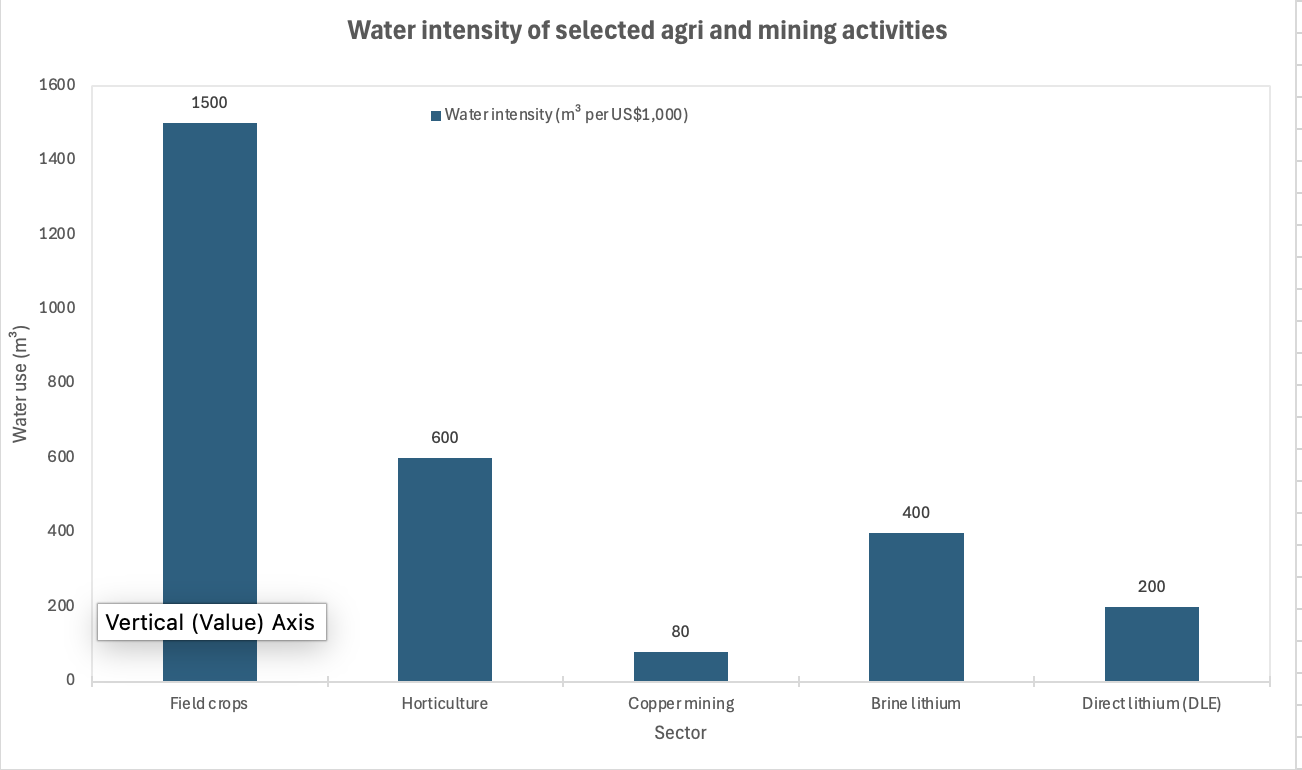

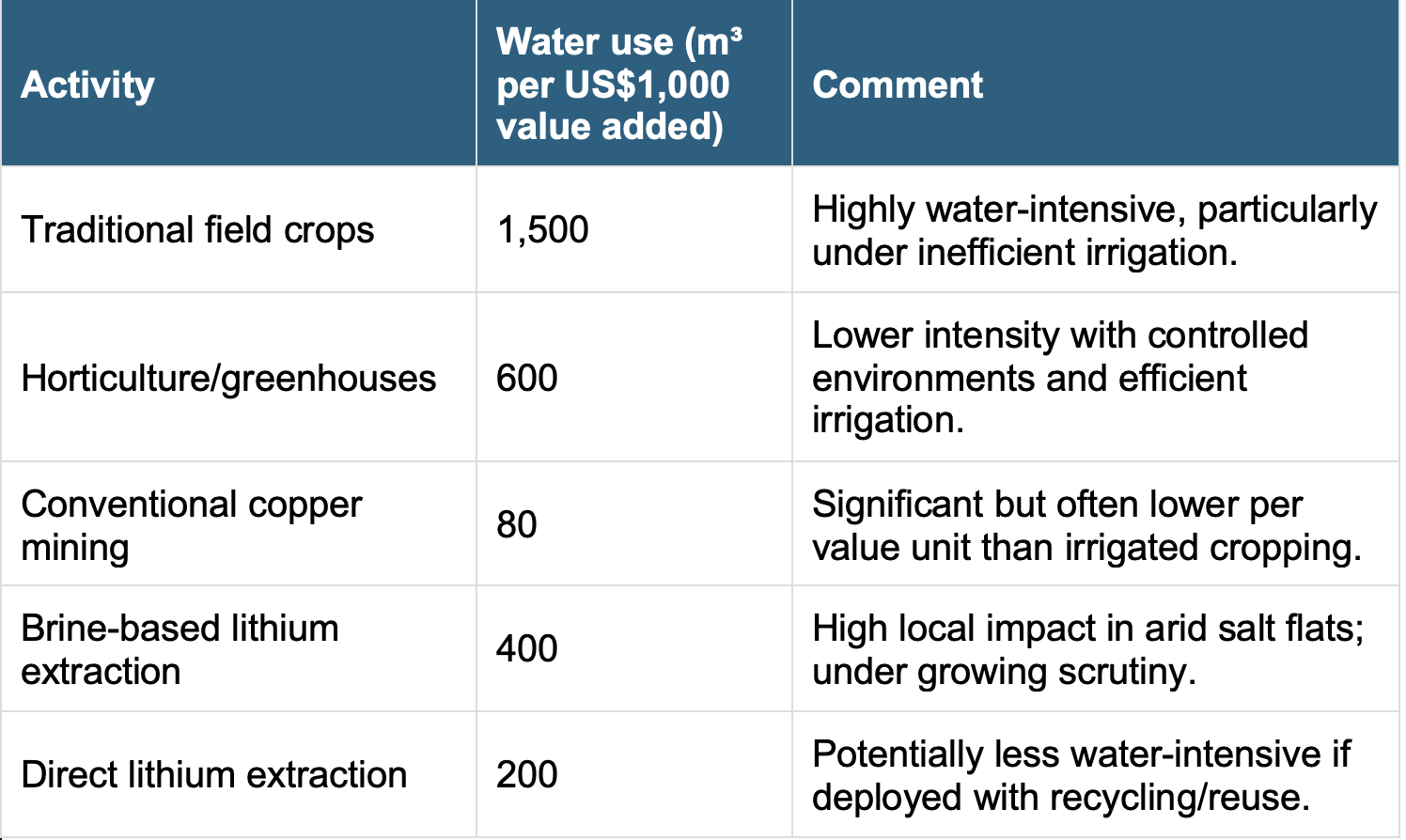

Chart 2: Indicative comparison of water intensity across agriculture and mining shows traditional field crops and brine-based lithium as especially water intensive per unit of value added

Traditional field crops can consume on the order of thousands of cubic metres of water per 1,000 USD of value added, far above many conventional mining operations, while brine‑based lithium extraction can be materially more water‑intensive than copper mining and emerging direct lithium extraction technologies sit in between. This asymmetry means that marginal shifts in water policy can re‑order which sectors are politically allowed to grow within a given basin.

The non‑obvious mechanism: water as de facto export control

From river disputes to value‑chain rationing

Hydro‑geopolitics has long centred on transboundary river control – from the Nile and the Tigris‑Euphrates to the Mekong and Indus – with upstream dam‑building used to project power. The emerging shift is that domestic basin management – caps, allocation rules, ecological flow requirements – is starting to function as an implicit restriction on the volume and composition of exports that rely on that water, even without formal trade measures.

Instead of blocking the export of a commodity explicitly, governments can reprioritise water towards domestic food security, urban use and politically sensitive industries, forcing export‑facing agri and mining projects in stressed basins to curtail output, invest heavily in reuse/desalination, or relocate. Because these decisions are framed as environmental or social protection, they can be deployed rapidly and are harder to challenge through trade regimes than classic export controls.

Water basins as the new “export licence”

In practice, the hydrological unit – the river basin or aquifer – becomes the binding constraint that operates like an export licence. Once a basin’s sustainable withdrawal is set and ecological flows are mandated, every tonne of soy, copper concentrate or battery‑grade lithium produced for export competes with domestic constituencies for the same limited entitlement.

This mechanism produces second‑ and third‑order effects:

It shifts bargaining power within countries away from national trade ministries toward basin‑level regulators, utilities and communities that control water permits and social licence.

It makes corporate water‑use efficiency and onsite recycling not just a cost issue but a licence to operate in export‑oriented value chains.

It encourages water‑rich states to internalise more value by exporting higher‑value intermediate or finished goods rather than raw, water‑heavy commodities, reinforcing resource nationalism trends.

What investors are missing

Country risk over basin risk

Most risk frameworks still treat water as an “ESG factor” or physical risk, handled via country‑ or asset‑level qualitative overlays, rather than as a core driver of future cash‑flow volatility. The reality is that two projects in the same jurisdiction can face very different hydrological risk if they sit on different basins, and two assets in different countries can share almost identical water‑supply risk if they tap the same cross‑border aquifer or river system.

This leads to systematic under‑pricing of risk where:

Export‑oriented agri portfolios are concentrated in a handful of stressed basins with tightening allocation regimes.

Transition‑metal assets (e.g. lithium brines, copper porphyries) depend on water‑use permits that are time‑limited, politically contestable, and exposed to climate‑driven reductions in recharge.

Virtual water trade as a strategic vulnerability

Trade in virtual water embedded in crops and commodities is large and growing, yet it rarely features explicitly in national security or corporate resilience discussions outside water‑scarce states. Import‑dependent economies for animal feed, fertiliser‑intensive crops or battery metals are therefore exposed not just to price and logistics shocks but to sudden volume constraints if exporting basins hit hydrological or political thresholds.

The variant view is that future disruptions are more likely to arrive through localised basin‑level rationing, moratoria or permit non‑renewals than through headline export bans, and that these will propagate along value chains in non‑linear ways. For example, incremental tightening of ecological flow rules in a single basin can simultaneously reduce irrigation for a key feed crop and constrain water‑intensive refining or smelting capacity, amplifying the shock through livestock, fertiliser and metals markets.

Why this matters now: near‑term catalysts

Converging shocks in the 2020s

The mid‑2020s are already characterised by overlapping droughts in major food and energy producing regions, with record temperatures and low rainfall degrading river flows from the Amazon and La Plata to the Zambezi. In parallel, several major emerging‑market basins – including parts of South America, North Africa and South Asia – are pursuing new hydropower and irrigation projects that will re‑divide flows between upstream and downstream users.

These trends intersect with:

Accelerating demand for copper, lithium and other transition metals, often sourced from arid regions where mining competes directly with communities and agriculture for water.

Rising investment in desalination, water reuse and advanced treatment technologies, particularly in water‑stressed regions such as California, the Middle East and parts of Europe, which will re‑shape the cost curve and feasibility of “decoupling” production from freshwater basins.

Policy and regulatory inflection points

Upcoming hydrological plans, water‑allocation reforms and environmental‑permitting overhauls in key basins act as catalysts for repricing. For instance, tighter basin‑level plans can embed minimum ecological flows that permanently remove a tranche of water from economic use, while new permitting regimes can lengthen project timelines for large mines and agri‑processing facilities.

Investors should treat such processes – often labelled as “river basin management plans”, “water security strategies” or “national water resource plans” – as forward indicators of where export‑oriented activity will be structurally capped or reprioritised. The lag between consultation and enforcement can give a false sense of security; once implemented, the adjustment in allocation can be abrupt for individual users.

Policy outlook: base, upside, downside

Base case: increasingly binding basin plans

In the base case, more countries adopt basin‑level water plans that explicitly rank uses (drinking water, ecosystem, food, energy, industry, exports) and set declining abstraction caps aligned with climate projections. Over the next five to ten years, this drives progressive tightening of allocations in stressed basins, longer and more complex permitting for new agri and mining projects, and increased pressure for on‑site water reuse and efficiency investment.

Upside case: technology‑enabled decoupling

In an upside scenario, rapid deployment of desalination, wastewater reuse, advanced membranes and more efficient irrigation reduces the marginal water intensity of both agriculture and mining. This could allow some water‑stressed exporters to sustain or even grow high‑value production without proportionately increasing freshwater withdrawals, particularly where renewable power is available to support energy‑intensive treatment.

Downside case: weaponisation and abrupt curbs

In a downside case, geopolitical tensions elevate water from an implicit constraint to an explicit tool, with upstream states or water‑rich countries using dams, basin plans or export licensing to exert pressure on downstream users or trade partners. Under such conditions, sudden curbs on agri or metals exports from specific basins – justified on environmental or security grounds – could trigger sharp price spikes and scramble supply chains, with limited scope for short‑term substitution.

Indicative chart: “Hypersensitive basins: share of national export value generated in high‑water‑stress catchments (illustrative)” – showing that in several exporting countries, a significant portion of agri and mining export value is concentrated in basins with high or extremely high water stress, implying disproportionate vulnerability to allocation changes.

Sector, supply‑chain and asset‑level implications

Agriculture and agri‑trade

Water‑intensive field crops, especially those grown under irrigation in arid or semi‑arid regions, face rising constraints. This will progressively favour:

Shifts towards less water‑intensive crops or cultivation methods in stressed basins, particularly where policy explicitly links water pricing or permits to crop choice.

Relocation of export‑oriented production to water‑abundant regions, even where labour or logistics are less favourable, as hydrological security becomes a key determinant of long‑term competitiveness.

Livestock value chains are indirectly exposed through feed, with regions importing feed from stressed basins vulnerable to upstream water rationing. Storage, processing and logistics nodes in those basins may also face growing scrutiny over their water rights and their contribution to local stress.

Mining, metals and the energy transition

For mining, water scarcity can delay projects, force process redesigns, and increase operating costs via water procurement, treatment and community compensation. Lithium brine operations in arid salt flats face particular pressure to reduce water consumption and shift to less water‑intensive technologies, alongside rising expectations for transparent monitoring of local hydrological impacts.

Copper and other base metals operations in dry regions increasingly need to secure alternative water sources, such as seawater desalination, pipeline infrastructure, or closed‑loop processing, which can materially alter the cost structure and emissions profile of production. Assets without credible water‑sourcing strategies or social licence in stressed basins risk being stranded or forced into lower‑than‑designed utilisation.

Supply‑chain architecture and financing

At the supply‑chain level, companies may re‑optimise networks to reduce exposure to single‑basin water risk – for example, by diversifying sourcing across basins, investing in multi‑origin blending, or moving refining closer to water‑secure locations. Financiers and insurers are likely to increase focus on basin‑level risk, conditioning capital or coverage on robust water‑management plans and resilience measures.

A useful way to think about mis‑priced risk is to compare sectors by indicative water intensity per unit of value added:

Geopolitical Outlook

Water as a lever in regional politics

In several regions, water control has already been used as a bargaining chip, either implicitly through dam operations or explicitly through treaty renegotiation. As climate pressures mount, upstream states can gain leverage by modulating flows, affecting not only downstream agriculture and hydropower but also mining and industrial clusters that depend on predictable water regimes.

At the same time, water‑scarce but capital‑rich states may use investment in desalination and overseas farmland or mining assets as a hedge against domestic water constraints, deepening the link between hydro‑security and foreign direct investment. This could lead to new alignments and tensions around “water corridors”, similar in strategic importance to energy transit routes.

Water‑rich states as strategic suppliers

Water‑abundant regions with stable governance – including parts of the Americas, northern Europe and some tropical basins – are positioned to emerge as strategic suppliers of water‑intensive agri products and metals processing. If these states choose to internalise more value by prioritising higher‑value exports and restricting low‑margin, high‑water‑intensity goods, the effective global supply of certain commodities from secure basins could shrink, even if aggregate output appears sufficient.

Conclusion

Water should be treated less as a background environmental constraint and more as an emergent export control regime operating at the basin level, with its own politics, timelines and enforcement mechanisms. Structurally, this implies a re‑ordering of comparative advantage in both agriculture and mining over the next decade, favouring water‑secure basins and technologies that decouple production from freshwater stress, while penalising business models that implicitly assume free, perpetual access to local water.

Cyclically, hydrological shocks will continue to show up as “temporary” drought‑related disruptions, but the underlying direction is towards codified basin‑level caps and allocation hierarchies that permanently change how much export‑oriented activity is possible from stressed regions. For decision‑makers, the central question is not just how prices will respond to such shocks, but which balance sheets – sovereign, corporate, community – will end up absorbing the emerging hydro‑geopolitical risk embedded in agri and mining value chains.

This article is for information and discussion only and does not constitute investment advice or a recommendation.

References:

UN‑Water – UN World Water Development Report 2024 – 2024.

FAO – Water resources management for the four betters – 2023.

Earth.org – Why Global Water Security Matters in 2024 – 2024.

European Commission JRC – Global drought threatens food supplies and energy production – 2024.

EU External Action Service – The Nile and beyond: geopolitics of water – 2020.

Palacios et al. – Sharing water in the international Tagus River basin – 2024.

Post Factum – Fresh Water Geopolitics – 2025.

Dentons – Chile’s newly announced National Lithium Strategy – 2023.

Mining Report – Chile, Salt Lakes and Lithium: Current Production Status – 2023.

Global Mining Review – Chile’s national lithium strategy brings risks and opportunities – 2023.

Global Water Market (K.M. Millauer Consulting) – Latest Trends in the Global Water Market: 2024 Insights – 2024.

Rural21 – 2024’s water crisis – how droughts and floods are changing our world – 2025.

Pollution & Sustainability Directory – Geopolitical Water Conflict – 2025.