Too Hot to Scale: Why Tropical Heat and Water Are the Real Constraints on Southeast Asia's Data Centre Boom

Every megawatt committed to Southeast Asian data centres is implicitly a bet on water rights that may not exist.

The narrative around the region's digital infrastructure is compelling: capacity running 70% below mature markets, AI-driven demand growing at 20% per year through 2028, and hyperscaler capital accelerating a build-out that was structurally overdue. But the investment case has been stress-tested against latency maps and power purchase agreements, not against wet-bulb temperatures and water allocation queues. That gap is closing, and not in investors' favour.

Why This Matters

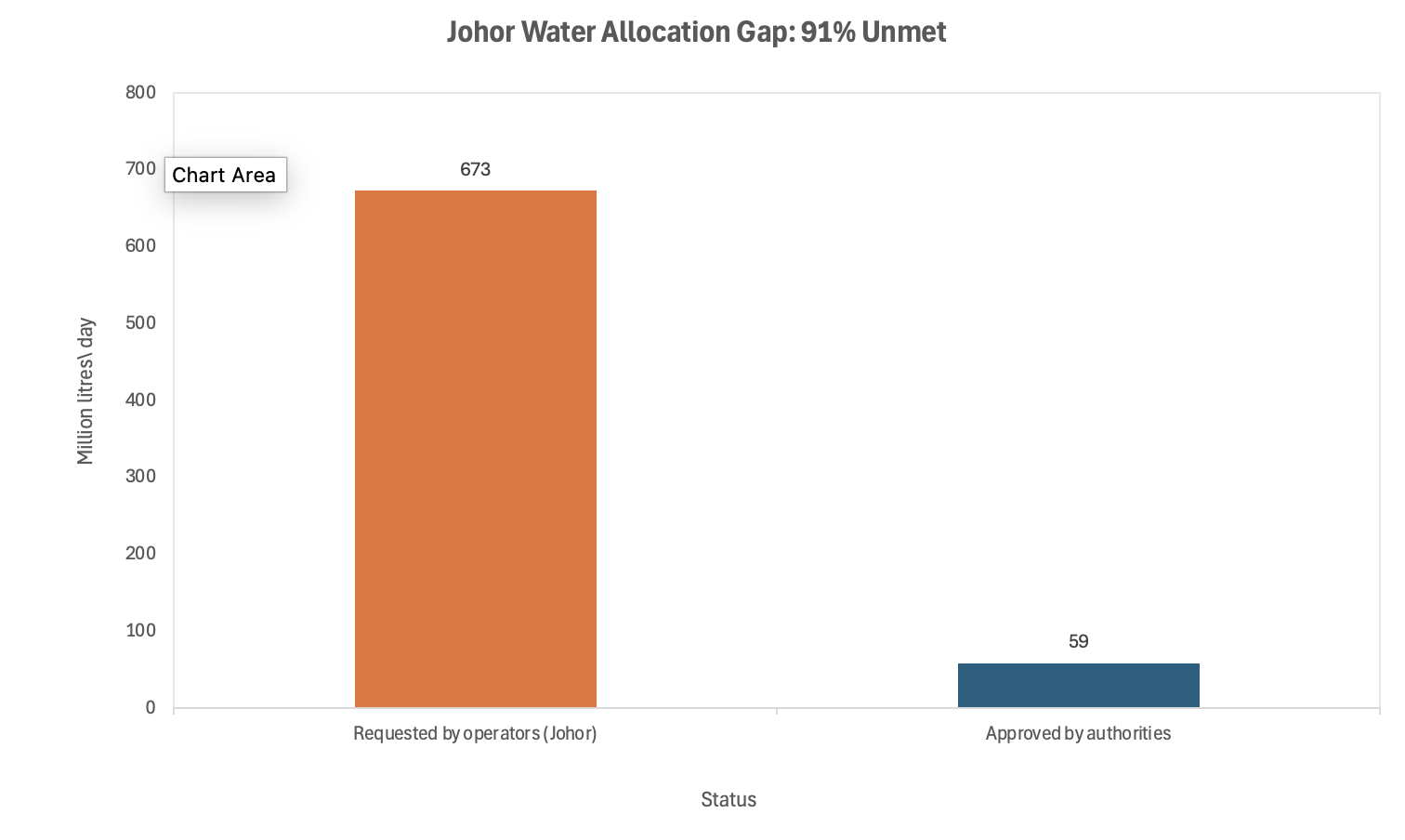

Stranded capex exposure: Johor approved just 59 million litres per day of the 673 million litres requested by prospective data centre operators; facilities built without secured water access carry operating constraints from day one.

Margin compression: Tropical operating conditions force Power Usage Effectiveness (PUE) above 1.5 in legacy designs, versus 1.2 to 1.3 in temperate-climate peers, directly eroding the cost structures underwritten at acquisition.

Regulatory gating: Malaysia's November 2025 halt on Tier 1 and Tier 2 data centre approvals signals that the constraint is no longer theoretical; it is now a formal barrier on capital deployment.

The Build Imperative

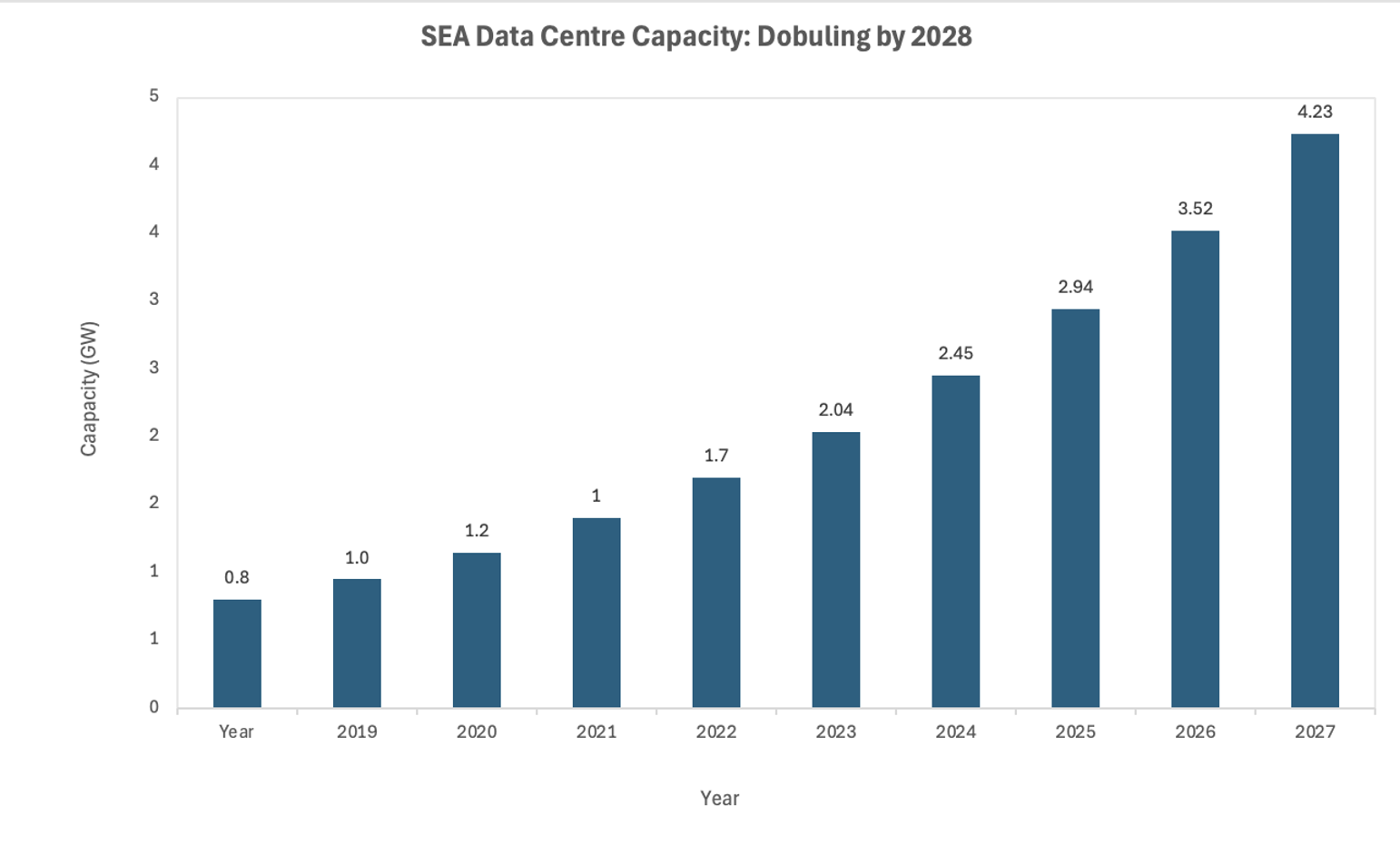

Southeast Asia's data centre capacity roughly doubled between 2019 and 2023, rising from approximately 0.8 gigawatts (GW) to 1.7 GW, and projected to reach over 4 GW by 2028. The region now hosts around 370 facilities, concentrated in Singapore, Indonesia and Malaysia. Structural drivers are durable: a digitising population of 680 million, cloud migration still in early innings across most Association of Southeast Asian Nations (ASEAN) economies, and AI workload growth redirecting capacity investment from constrained Western markets. Microsoft, Google and a widening field of infrastructure funds have committed multi-billion dollar allocations accordingly.

Sources: US-ASEAN Business Council; JLL; analyst estimates. Projections based on 20% compound annual growth rate from 2023 baseline.

The investment thesis is straightforward. The operational thesis is where the assumptions break.

The Physics Nobody Priced

Data centres prefer cold. Southeast Asia is warm, wet, and stays that way. Ambient temperatures range from 27°C to 35°C year-round, well above the 18°C to 27°C that conventional cooling infrastructure was designed to manage. The result is a structural energy penalty: facilities in tropical climates routinely operate at PUE of 1.5 or above, compared to 1.2 to 1.3 for best-in-class temperate-climate peers. Every unit of wasted energy is direct margin compression at the asset level.

The AI hardware transition sharpens this penalty sharply. Traditional server racks running central processing units (CPUs) draw 5 to 10 kilowatts (kW) each. Graphics processing unit (GPU) racks serving AI inference and training workloads draw 30 to 100 kW. This is not a linear upgrade: it is a step change in heat density that renders room-level air-cooling architectures functionally obsolete. Liquid cooling and direct-to-chip systems can manage these loads, but they require capital expenditure that most legacy co-location facilities in the region were not designed to absorb.

Singapore's Infocomm Media Development Authority (IMDA) has quantified one dimension of the problem: each 1°C increase in operating temperature yields up to 5% in energy savings, which is why the city-state's Tropical Data Centre Standard, launched in August 2025, pushes operators towards a 26°C operating threshold. The structural case is that this standard is an attempt to make a constrained environment workable, not a genuine elimination of the tropical cost penalty. It is the right direction. It does not make the underlying physics disappear.

Water as the Binding Constraint

The energy inefficiency shows up in operating cost models. The water constraint is less visible and, in the near term, more immediately binding.

Conventional evaporative cooling systems, the dominant technology in Tier 1 and Tier 2 facilities, consume water continuously to dissipate heat. A single large facility can draw up to 50 million litres per day: a volume comparable to the daily domestic supply of a mid-sized city. Malaysia's National Water Services Commission reviewed applications from 101 data centres operating across Selangor, Negeri Sembilan and Johor, and approved less than 18% of requests, citing the risk of diverting treated water from public supply. In Johor specifically, operators have requested 673 million litres per day across proposed facilities; approximately 59 million litres per day has been approved.

Sources: Malaysian National Water Services Commission; South China Morning Post (November 2025).

In November 2025, Johor halted new approvals for Tier 1 and Tier 2 data centres entirely, pending resolution of its water allocation framework. New water infrastructure is unlikely to arrive before mid-2027. This matters for an investor reason that goes beyond the facilities currently in the queue: it introduces a new category of asset bifurcation between operators holding secured water rights and those on provisional or contested allocations. The latter group carries contingent liability that is not yet reflected in most valuations.

Catalysts, Policy Outlook and Scenarios

The next twelve months will determine whether the constraint is managed or entrenched. The asymmetry of risks skews towards the downside: approvals are slow to reverse, water infrastructure takes years to build, and regulatory frameworks once enacted rarely soften quickly. Investors with uncommitted capital have a narrowing window to select assets before the bifurcation between compliant and non-compliant operators is fully priced into the market.

0 to 3 months: The immediate focus is Johor's approval pipeline. Tier 3 and Tier 4 facilities, which use more advanced and less water-intensive cooling, remain eligible for approval, creating a near-term sorting mechanism between operators with modern infrastructure and those relying on legacy designs. Singapore's implementation of the Tropical Data Centre Standard is producing early operational data: BDx became the first operator to qualify under the standard in March 2026, providing a performance benchmark that regulators across the region are watching.

3 to 12 months: ASEAN governments are moving, at differing speeds, towards mandatory Water Usage Effectiveness (WUE) and PUE disclosure requirements. Malaysia is expected to formalise its tiering framework into policy by late 2026, creating a two-speed market. Singapore's 300 megawatt (MW) Green Data Centre Roadmap capacity expansion will absorb selective operators, but the bar for entry, in both capital efficiency and sustainability credentials, is higher than the regional average. Hyperscaler lease renegotiations anchored to efficiency thresholds are likely to accelerate this bifurcation.

How the policy timeline resolves will determine which scenario dominates. The variables to watch are not macroeconomic; they are administrative: the pace of Johor's tiering framework formalisation, the adoption rate of liquid cooling among mid-market operators, and whether Singapore's Tropical Data Centre Standard produces performance data compelling enough to accelerate regulatory convergence across the region.

Base case: Water and energy constraints slow mid-market build-out, consolidate market share towards Tier 3 and Tier 4 operators with compliant infrastructure, and compress returns on legacy assets. Hyperscaler-anchored facilities with bespoke cooling and secured power purchase agreements outperform the broader market.

Upside case: Liquid cooling adoption accelerates beyond base expectations, new water recycling and alternative source technologies reduce the constraint materially, and a clear policy framework stabilises by mid-2027, restoring capital deployment visibility across the region.

Downside case: Water approvals remain politically contested, grid decarbonisation stalls and forces covenant breaches on green-labelled project debt, and a combination of regulatory friction and climate risk reprices the asset class broadly across ASEAN.

Conclusion

The capital flowing into Southeast Asian data centres is responding to a real structural demand signal. The error is not in identifying the opportunity; it is in pricing the physical operating environment as a manageable inconvenience rather than a structural cost and a gating constraint on scale.

Water is not a secondary risk factor. In Malaysia, it is already the primary regulatory barrier to new capacity. Heat is not merely an engineering challenge; it is a permanent margin drag on any facility not designed from the ground up for tropical conditions. The bifurcation between compliant and non-compliant assets is already underway. Investors who treat asset selection as a proxy for market exposure will carry that distinction in their returns. Those deploying capital into this market now need to answer one question before any other: who holds the water rights, and what are they contingent on?

References

Fortune – "SEA's AI Data Centre Boom Must Overcome Heat and Humidity" – March 2026

Fair Planet – "Too Hot to Compute: The Water Crisis Behind Southeast Asia's Data Centre Boom" – November 2024

South China Morning Post – "Southeast Asia's AI Data Centre Gold Rush Tests Power Grids in the Tropics" – March 2026

Business Times Singapore – "South-east Asia Reckons with Data Centres' Massive Water Consumption" – January 2026

South China Morning Post – "Data Centres in Malaysia's Johor Told to Wait for Water Until Mid-2027" – November 2025

Slashdot / W.Media – "Johor Stops Approving Tier 1 and Tier 2 Data Centres Due to Water Overuse" – November 2025

LinkedIn / Senol Gurvit – "PUE Challenges for Tropical Data Centres – Part 1" – January 2025

LinkedIn / Salleh – "Malaysia's Data Centre Boom Faces a New Reality: The Tropical Penalty" – December 2025

Sustainable Futures / Linklaters – "Singapore Announces at Least 300 MW Increase in Data Centre Capacity" – October 2025

GRESB – "Data Centres in Asia Pacific Are Thirsty and Feeling the Heat" – September 2025

Disclaimer: This article is for information and discussion only and does not constitute investment advice or a recommendation.