Rare Earth, Real War: The Invisible Commodity Conflict Reshaping Every Portfolio That Owns Technology

The next technology market correction may not come from rates, earnings, or regulation. It may come from a mineral export licence.

Rare earth elements (REEs) sit inside almost every device in a technology portfolio company's product range: the permanent magnets in electric motors, the phosphors in displays, the components in radar, sonar, and precision-guided systems. For two decades, institutional investors treated REE supply as an operating assumption, not an investment risk. China's sequenced use of export controls since 2023 has ended that assumption. The question is not whether this reshapes valuations — it already has begun — but how much of that repricing institutional capital has yet to absorb.

Why This Matters

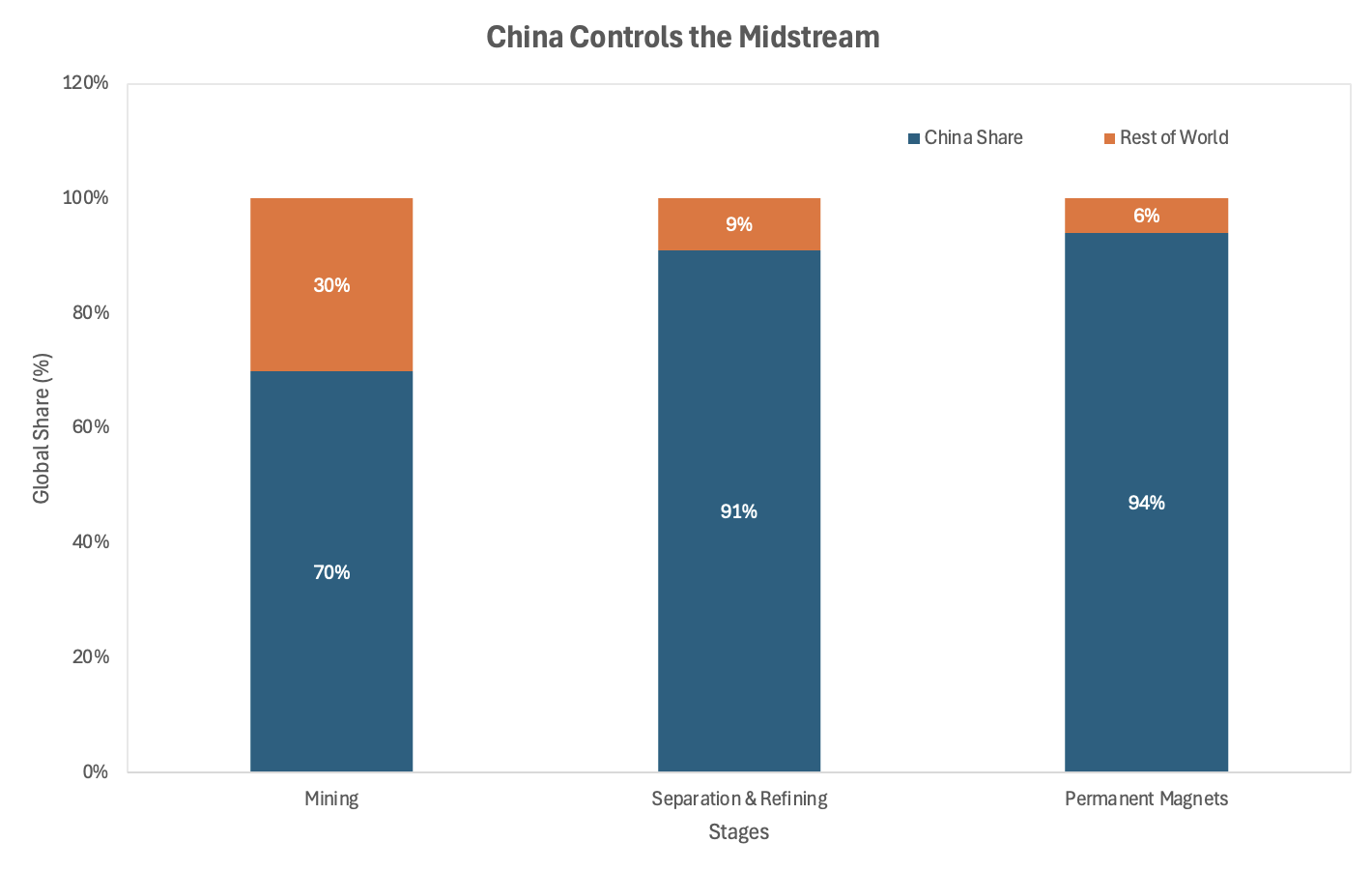

Chokepoint control: China controls approximately 91% of global REE separation and refining, and 94% of sintered permanent magnet production; no Western technology hardware company currently operates independently of that supply chain

Weaponised leverage: In April 2025, China imposed export restrictions on seven REEs and introduced extraterritorial licensing provisions that extend jurisdiction to products made outside China using Chinese technology

Unpriced risk: The suspension of broader controls runs only until November 2026; technology hardware valuations have not yet priced the cost of a permanent tightening

The Weaponisation of the Midstream

The conventional framing of rare earth risk focuses on mining geography. That is the wrong lens. China accounts for approximately 70% of global REE mining, but its decisive advantage lies one stage further downstream. The International Energy Agency estimated that, as of 2024, China controlled around 91% of global separation and refining production and 94% of sintered permanent magnet production. Even where a deposit sits in Canada, Australia, or Greenland, the ore must typically travel through Chinese processing infrastructure before it reaches a magnet manufacturer. The chokepoint is not the mine; it is the separation circuit.

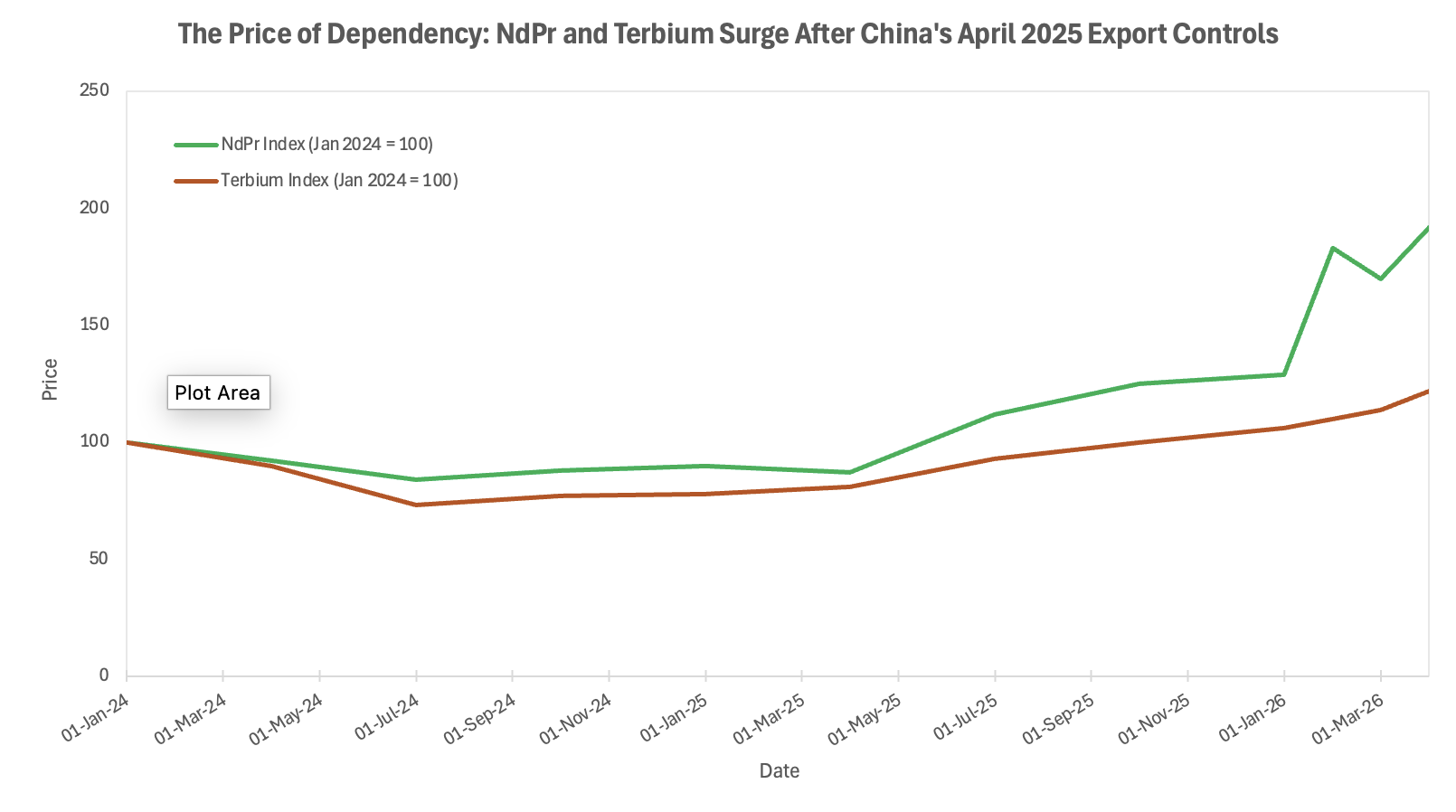

China's use of that chokepoint has escalated methodically. In December 2023, Beijing banned the export of REE extraction and separation technologies, removing the means by which Western competitors might replicate its midstream capability. In April 2025, it imposed export restrictions on seven REEs — including terbium, dysprosium, and samarium — and related magnets, in direct retaliation for United States tariff escalations. The controls require special export licences, creating an instrument of discretionary supply disruption that Beijing can activate and suspend at will. S&P Global confirmed in January 2026 that supply bottlenecks from these controls were set to persist throughout the year.

Chart: China's share of the global REE supply chain by stage (2024). Mining: 70%; Separation & Refining: 91%; Permanent Magnets: 94%. Source: International Energy Agency.

The Extraterritorial Trap

The October 2025 expansion of China's controls introduced a dimension that sell-side research has largely understated. Beijing extended its jurisdiction extraterritorially: any product manufactured outside China using Chinese REE technology, or containing Chinese-origin material above a 0.1% threshold, now falls within the licensing regime. A magnet made in Germany or Japan, using Chinese processing know-how under a legacy licence arrangement, is potentially a controlled item.

This is not a tariff. It is an assertion of supply-chain sovereignty with no precedent in modern commodity markets. It means that diversifying the geography of manufacturing does not, by itself, remove exposure. The exposure follows the technology, not the flag on the factory. For institutional investors, this distinction matters: portfolio companies reporting "diversified manufacturing" may carry concentrated supply-chain risk that does not appear in standard environmental, social and governance (ESG) or operational due diligence frameworks. China suspended these broader controls in November 2025 until November 2026 as part of a temporary trade accommodation, but the legal architecture remains in place. The suspension is a pause, not a concession.

What This Means for Technology Portfolios

The structural implication for institutional capital is underappreciated for a specific reason: REE exposure is a Tier 2 and Tier 3 supply-chain risk, not a Tier 1 input cost visible on income statements. A large-cap technology hardware company does not buy neodymium directly; it buys a motor from a supplier who buys a magnet from a manufacturer who buys separated REE oxides from a refiner. The risk is several layers removed from consolidated financial statements, which is precisely why it is not yet reflected in valuations.

Sources: Fastmarkets (Dec 2024 NdPr assessment); Rare Earth Mining Market Outlook, March–April 2026; S&P Global, Jan 2026

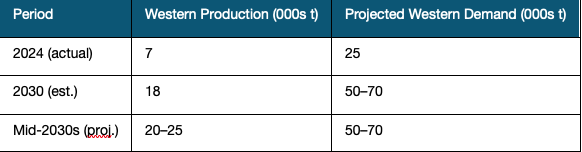

A 20% reduction in REE supply could generate over $100 billion in downstream losses across technology, defence, and clean energy sectors. Western producers currently separate approximately 7,000 tonnes of REEs annually — MP Materials and Lynas Rare Earths accounting for the bulk — against a McKinsey projection of 50,000 to 70,000 tonnes of annual Western demand by the mid-2030s. That gap does not close in a single budget cycle. The more likely read is that technology hardware companies with opaque supply chains will face a progressive cost increase and, in a scenario of renewed Chinese restriction, periodic production disruptions. Companies with genuine supply-chain resilience — those with long-term offtake agreements or vertical integration into processing — should attract a structurally lower cost of capital. Those without will face a discount the market has not yet fully applied.

Source: S&P Global; McKinsey & Company.

Catalysts and the Policy Outlook

The next eighteen months will define whether rare earth supply-chain risk becomes a persistent cost embedded in technology valuations or an acute shock that reprices them abruptly

0–3 month window (April–June 2026): The April 2026 US-EU Memorandum of Understanding (MOU) on critical minerals cooperation signals a coordinated Western response to supply concentration, but the distance between an MOU and operational supply is measured in years, not quarters. China's April 2026 Announcement 18 — the most recent expansion of REE export controls — reintroduced restrictions on medium and heavy REEs including terbium and dysprosium. The near-term risk is further incremental tightening ahead of the November 2026 suspension deadline.

3–12 month window (July–November 2026): MP Materials is evaluating a $1.2 billion permanent magnet campus in Texas, backed by a $400 million Department of Defense investment. Lynas projects rare earth oxide (REO) production growth of approximately 53% in its 2026 fiscal year and is targeting heavy rare earth separation at scale by 2027–2028. These are material developments, but both remain small relative to Chinese capacity. The critical catalyst is whether China allows the November 2025 suspension to lapse. If it does, technology hardware supply chains face simultaneous constraint across defence, electric vehicle (EV), and semiconductor sub-sectors.

The three scenarios below reflect not a range of economic outcomes but a range of political decisions: Beijing's choice of whether to let the November 2026 suspension lapse, and Washington's capacity to offer a credible alternative before it does.

Base case: China renews the suspension into 2027 as a negotiating instrument, keeping prices elevated but supply flowing. Technology hardware valuations absorb a modest cost-of-supply premium without acute disruption.

Upside: A durable US-China trade framework includes explicit REE carve-outs. Western processing investment accelerates materially. The supply-chain discount narrows for diversified technology companies; upstream Western producers re-rate.

Downside: China allows the November 2026 suspension to expire and enforces the extraterritorial provisions aggressively. Technology hardware production is disrupted across multiple sub-sectors simultaneously. Valuations reprice sharply and abruptly.

Conclusion

Rare earth supply risk is structural, not cyclical. It has been building since Beijing began its coordinated state investment in REE processing in the 1980s; what is new is that the instrument is now being used. The suspension of controls through November 2026 has created a temporary window in which the discount that should attach to Chinese-dependent technology supply chains remains largely unapplied.

The geopolitical overlay reinforces this read. China's use of export controls is not an aberration driven by a specific tariff dispute; it is the normalisation of commodity leverage as a foreign-policy instrument. The October 2025 extraterritorial provisions confirm that Beijing intends to maintain strategic oversight of REE flows regardless of where processing eventually occurs. Breaking China's stranglehold on separated rare earths is likely to take at least a decade, according to analysts cited by Al Jazeera. An MOU signed in Washington does not accelerate a separation circuit being built in Malaysia.

For institutional allocators, the practical question is not whether to exit technology hardware — the sector's long-term structural case remains intact. It is whether current technology positions price the risk of periodic, policy-induced supply disruption correctly. In most portfolios, they do not.

References

International Energy Agency — Rare Earth Industry in China: Separation and Refining Dominance — 2024

Centre for Strategic and International Studies (CSIS) — The Consequences of China's New Rare Earths Export Restrictions — April 2025

European Parliament Think Tank — China's Rare-Earth Export Restrictions — November 2025

Clark Hill — China Hits "Pause" on Rare-Earth Export Controls — November 2025

S&P Global Market Intelligence — Rare Earth Supply Bottlenecks Set to Persist in 2026 — January 2026

S&P Global Market Intelligence — Rare Earth Supply Chains: Funding, Policy and China's Edge — April 2026

The Northern Miner — West Speeds Up Pursuit of China in Supply Chain Race — February 2026

Fortune — Beijing's Dominance in Rare Earth Processing Leaves Others Behind — March 2026

Al Jazeera — Despite US Push, China Poised to Dominate Rare Earths for Years — October 2025

Investing News Network — Rare Earths Market Forecast: Top Trends for 2026 — April 2026

Reuters — As Trump Reins in China Tech Curbs, Beijing's Export Controls Come of Age — February 2026

GlobeNewswire / ResearchAndMarkets — Valuation Implications of Domestic Rare Earth Supply Chain Reshoring — January 2026

US Department of State — 2026 Critical Minerals Ministerial — February 2026

YouTube/AP — US and EU Sign Preliminary Partnership Deal to Secure Critical Minerals Supply Chains — April 2026

This article is for information and discussion only and does not constitute investment advice or a recommendation.