The Founders Who Refused to Choose: How Sustainable Luxury Became a Private Markets Thesis

The most interesting luxury founders in the market today are not choosing between beauty and proof. They are building businesses on the premise that, without both, neither holds.

Why This Matters

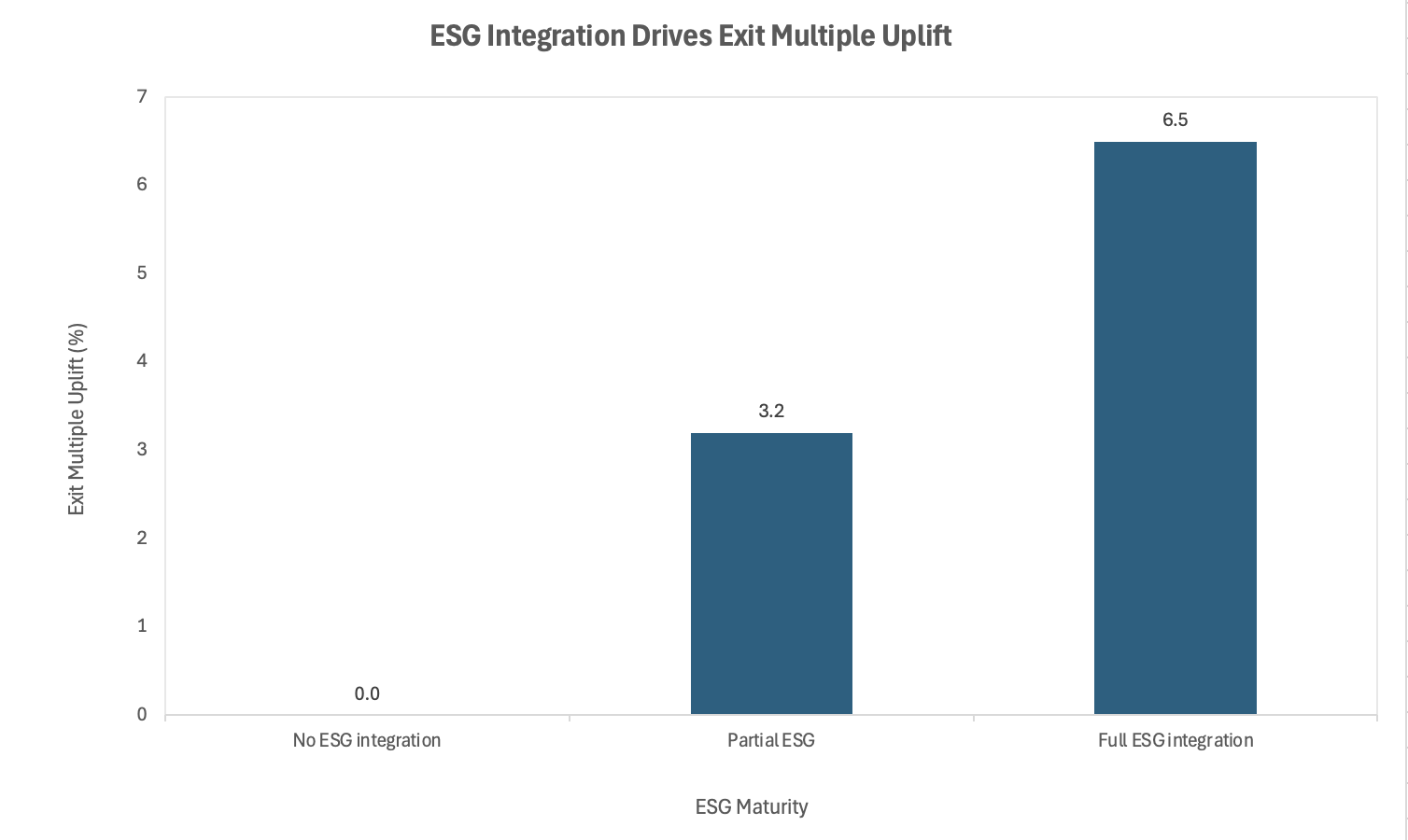

Proof of impact is migrating from compliance to valuation input: PE portfolio companies with full environmental, social and governance (ESG) integration achieve 6–7% higher exit multiples.

The sustainable luxury beauty market is growing at roughly 18% per annum, reaching USD 15.7 billion in 2024, and is projected to exceed USD 30 billion by 2028.

The EU's Empowering Consumers for the Green Transition Directive (ECGT) takes effect in September 2026, banning generic green claims and forcing a structural reset in how brands communicate and price sustainability credentials.

The Core Shift

For two decades, sustainable luxury operated on a tension that was never honestly resolved: brands wanted the moral positioning without the operational discipline that would make it defensible. The result was a market full of beautiful objects with implausible claims.

That tension is collapsing, driven by a cohort of founders who treat verification not as a cost centre but as a moat. These are not activists in the protest-march sense, nor are they purely architects of aesthetic form. They sit at the intersection: people who understand that an object's claim to last a hundred years and its claim to have caused minimal harm in production are, structurally, the same argument. The global personal luxury goods market grew at roughly 11% compound annual growth rate (CAGR) between 2019 and 2024, profits nearly tripling, but the next growth leg is not volume. It is credibility per unit sold.

The sustainable luxury beauty segment illustrates the trajectory most clearly. At USD 15.7 billion in 2024 and tracking towards USD 30 billion by 2028 at an ~18% CAGR, it is outpacing the broader luxury market by a factor of nearly two. The mechanism is not consumer altruism. It is the convergence of aesthetic ambition and third-party verification into a single purchase signal.

Source: DataIntelo / industry estimates.

The Non-Obvious Mechanism

The consensus view is that sustainability in luxury is a consumer preference story. It is, but that framing stops one step too early. The more structural read is that verifiable sustainability is becoming a pricing architecture: it determines not just whether a consumer will pay a premium but how durable that premium is across cycles.

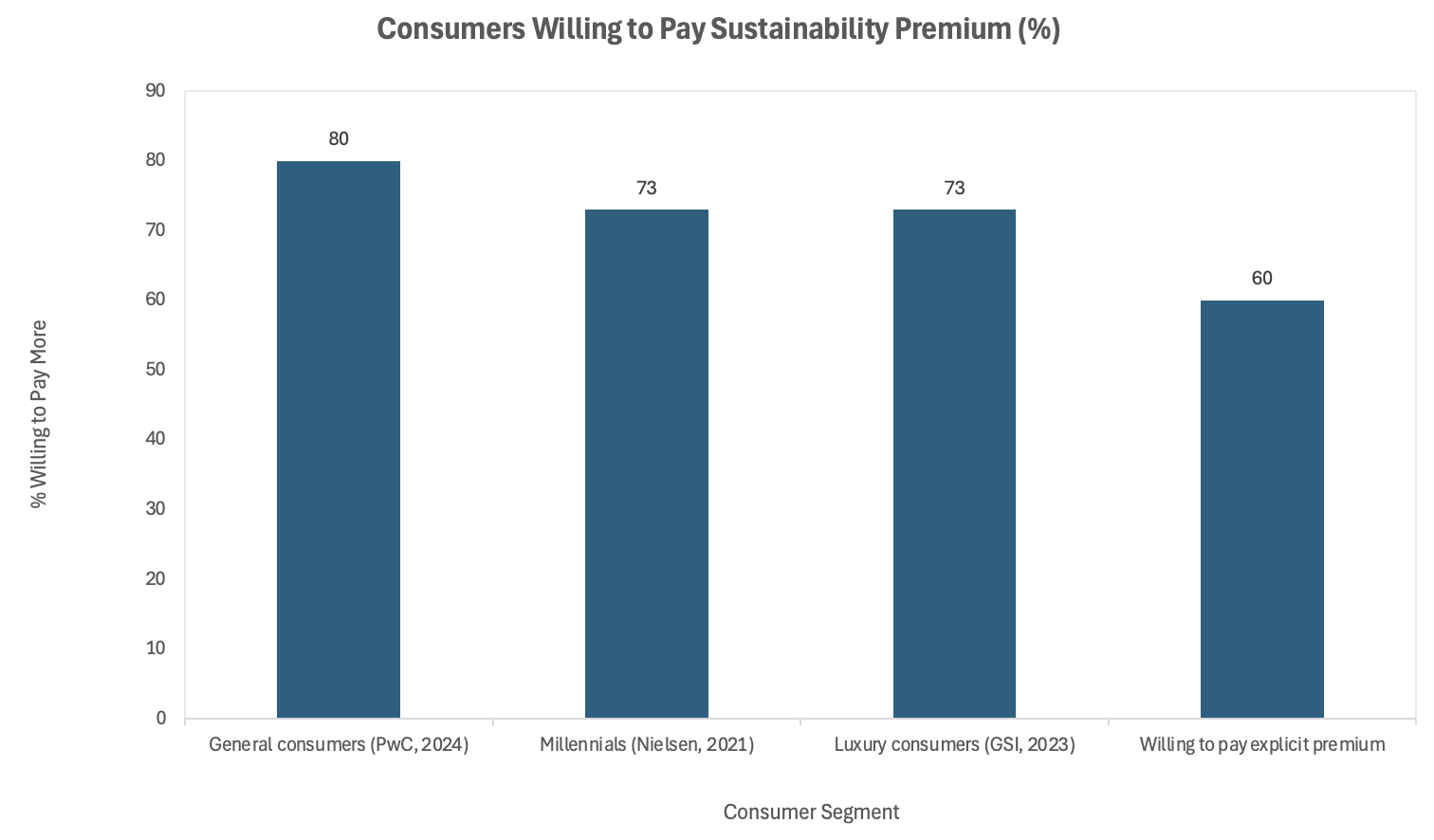

This is where the founders who refuse to choose create a genuine competitive advantage. Brands built on provable claims, blockchain traceability of raw materials, certified supply chains, and independently audited carbon data, generate a form of pricing stickiness that heritage alone cannot replicate. When 80% of consumers signal willingness to pay more for sustainably produced goods, and 73% of luxury consumers specifically name sustainability as a purchase preference, the founders who can substantiate those claims are capturing a demand pool that soft-branded competitors cannot access at equivalent price points.

Source: PwC Voice of Consumer Survey 2024; Nielsen 2021; Global Sustainability Institute 2023.

The second-order effect consensus has not fully priced is this as verification infrastructure matures, the cost of greenwashing failure rises asymmetrically. Brands that built on vague claims, natural-ish, responsible-ish, planet-friendlyish, face compounding reputational and regulatory liability. Founders who built on proof face compounding pricing power.

Investor Implications

For CIOs and deal principals in private markets, the investment case rests on three structural shifts that are not yet fully reflected in comparable valuations.

ESG maturity is now a quantifiable exit variable, not a qualitative narrative. Research from Alvarez and Marsal and PwC consistently shows that PE portfolio companies with full ESG integration achieve 6–7% higher valuation multiples at exit. That is not a rounding error on a deal; at typical luxury sector entry multiples, it represents material IRR accretion. Sixty-three per cent of US investors report they would pay a premium for a target demonstrating high ESG maturity.

Source: Alvarez and Marsal 2025; PwC PE ESG Survey.

The deal pipeline is skewing towards founders who built proof into the architecture from day one, rather than retrofitting it in the 18 months before exit. The difference in diligence risk is substantial: a brand with independently certified supply chains, audited scope three emissions, and verifiable ingredient provenance requires no remediation spend and carries lower regulatory exposure. These are not soft differentiators; they are balance sheet items.

The competitive dynamics within the luxury segment are shifting in favour of smaller, founder-led businesses precisely because they can move faster on supply chain transformation than large conglomerates managing legacy infrastructure. Private equity firms including L Catterton, Carlyle, and Blackstone have already signalled allocation interest in premium beauty and wellness with verifiable sustainability credentials. The window to enter at founder-stage valuations, before institutional capital compresses the entry multiple, is narrowing.

Near-Term Catalysts and Policy Outlook

The next 12 months represent the highest asymmetry of regulatory risk versus opportunity the sustainable luxury sector has produced; those positioned on verified claims face a structural tailwind, those reliant on vague language face compounding liability.

0–3 month window: The Green Claims Directive has effectively been paused following the European Commission's withdrawal announcement in June 2025. This removes one layer of near-term compliance pressure, but does not eliminate it. The ECGT, already transposed into law, comes into force in September 2026. Brands and their investors should be treating the current period as preparation time, not relief.

3–12 month window: UK greenwashing enforcement is intensifying independently of the EU, with the Competition and Markets Authority (CMA) increasing scrutiny of environmental claims across fashion and beauty. The convergence of EU and UK frameworks creates a dual-jurisdiction compliance burden for cross-border luxury brands. Founders who built on proof face no incremental cost; founders who built on assertion face material legal and reputational exposure heading into 2026 reporting cycles.

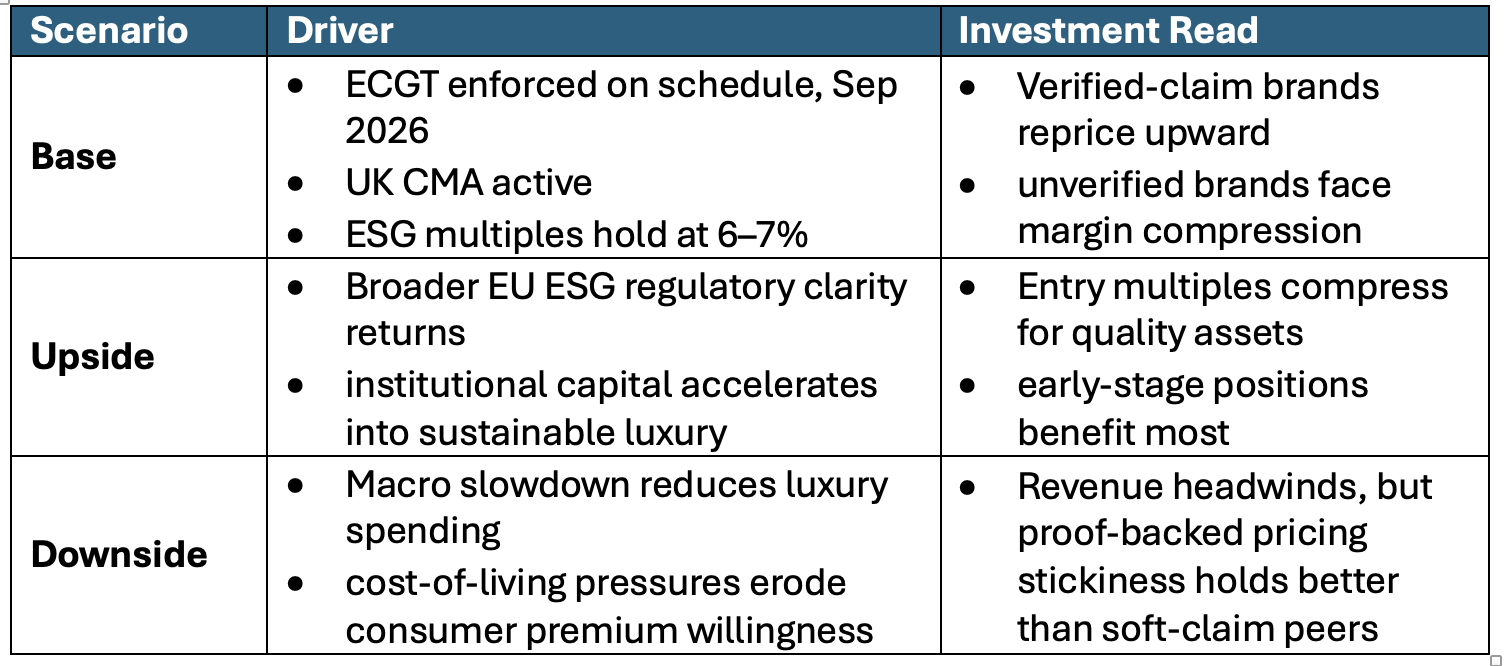

The risk asymmetry heading into late 2026 is clear: regulatory downside for unverified claims, valuation uplift for verified ones. The scenario matrix below reflects the most plausible range of outcomes.

Conclusion

This is not a taste cycle. The structural case for founders who refuse to choose between beauty and proof is that they are building the only category of luxury business where the valuation argument and the regulatory argument point in the same direction.

The cyclical read is that luxury markets are in a modest growth phase: McKinsey's 2025 State of Luxury report flags a slowdown and calls for bold strategic repositioning rather than volume plays. The structural read sits beneath that: the brands that will capture disproportionate value in the next five years are those where the object's claim to endure and its claim to have been made responsibly are provably the same claim. In private markets terms, that convergence is an exit story with a regulatory backstop.

The geopolitical overlay matters here too. Affluent Asian consumers, the segment driving the next volume leg, are showing nuanced but real willingness to pay for verified sustainability, particularly where it intersects with craft and provenance. Founders who can narrate both the aesthetic and the supply chain, not as separate chapters but as a single argument, will find that capital, across private equity, family offices, and emerging markets distribution partners, is increasingly listening.

References

London Business School StartHub – Beyond Affluence: How Luxury Brands Sustain Value in a Shifting Market – 2025

DataIntelo – Sustainable Luxury Beauty Market Report – 2024

PwC – Voice of Consumer Survey – 2024

Alvarez and Marsal – How to Create Value from ESG: A Blueprint for Private Equity – 2025

PwC – Unlocking Hidden Value: The Critical Role of ESG in PE Deals – 2025

News.Sustainability-Directory – Private Equity ESG Due Diligence Now Drives Deal Value and Exit Multiples – 2025

Senken / EcoClaim – EU ECGT Directive: Enforcement Begins September 2026 – 2026

Latham and Watkins – European Commission Announces Intention to Withdraw EU Green Claims Directive – 2025

McKinsey and Company – The State of Luxury Goods in 2025 – 2025

Global Sustainability Institute cited in PradeepGlobal – High-End Beauty, Low Impact – 2025

ScienceDirect – How do Crazy Rich Asians Perceive Sustainable Luxury? – 2023

Steptoe – Green Claims: Regulatory and Litigation Focus in the EU and UK – 2026

This article is for information and discussion only and does not constitute investment advice or a recommendation.