The Heritage Revival Trade: Why Sustainable Fashion's Most Underpriced Opportunity Is Cultural, Not Just Environmental

The sustainable fashion conversation has spent a decade counting carbon. It has barely started counting culture.

Most capital flowing into sustainable fashion is chasing the same metrics: recycled inputs, lower emissions, circular take-back schemes. The environmental thesis is real but increasingly crowded, and the pricing reflects it. The underpriced variable sits one layer deeper: cultural legitimacy. Heritage craft, regional textile tradition, and the identity economy embedded in them represent a long-duration, structurally supply-constrained asset class that most family office portfolios have neither named nor sized.

Why This Matter

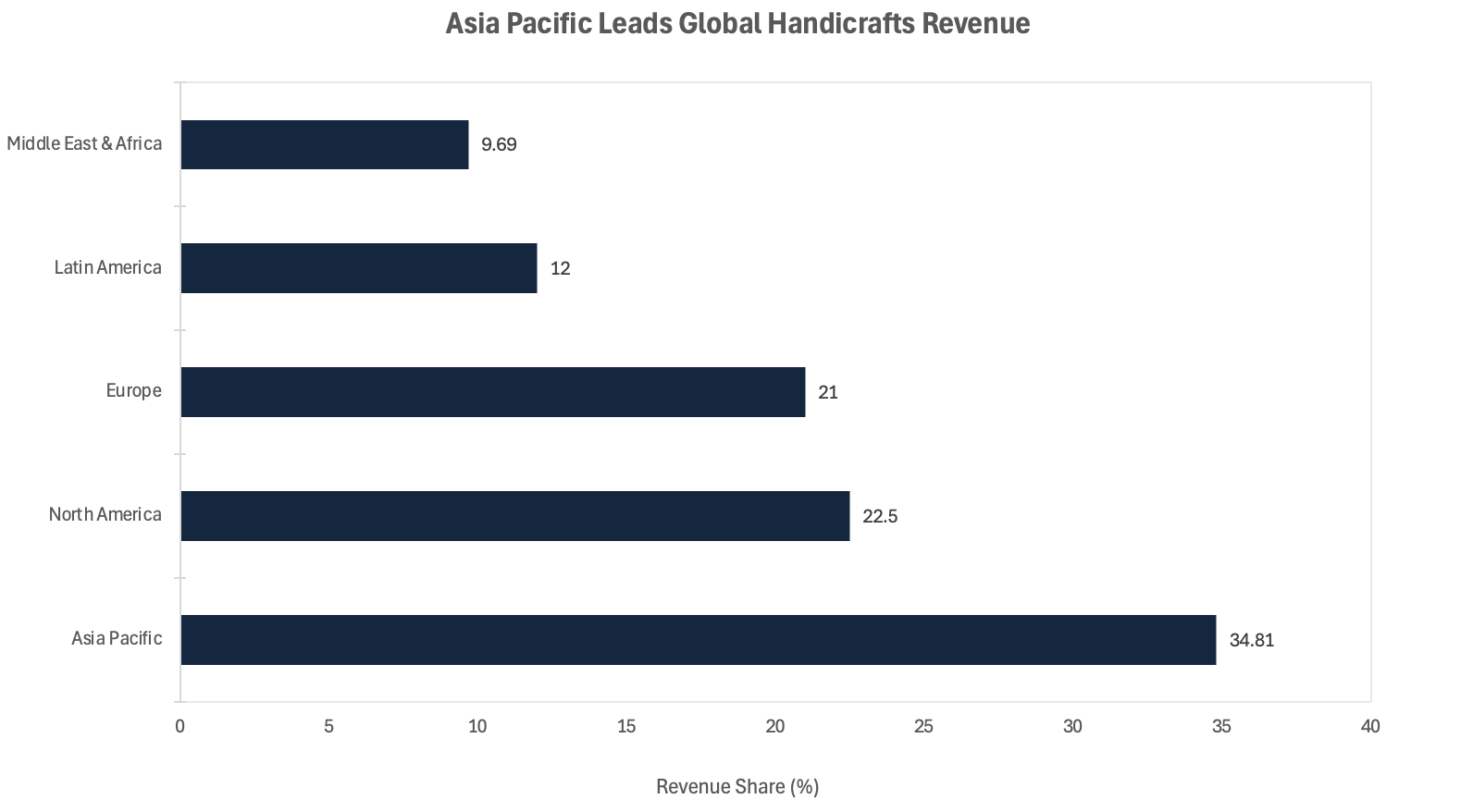

Market scale: The global handicrafts market reached USD 739.95 billion in 2024 and is on course for USD 983 billion by 2030; Asia Pacific commands the largest regional share at 34.81% of global revenue

Pricing power: Products with verified artisan provenance command 20–30% price premiums over comparable non-heritage goods, and heritage brands demonstrate materially higher five-year value retention than infrastructure-first competitors

Capital formation: Singapore added approximately 600 new single-family offices in 2024 alone, a 400% increase on 2020; yet the cultural asset angle remains largely uncaptured in formal portfolio construction

The Core Shift

The sustainable fashion market has been defined, thus far, by its supply chain. Brands competed to reduce water use, eliminate polyester, and certify organic cotton. That framing served a purpose: it created measurable proxies for a consumer values shift that was real but hard to price. It also created a race to the middle. When every brand's sustainability story is structurally similar, differentiation collapses, and so does pricing power.

What is changing now is the demand signal, not just the supply logic. Consumers across Southeast Asia, the Gulf, and Western diaspora communities of South and Southeast Asian origin are not simply paying for environmental compliance. They are paying for identity. The batik shirt that carries a Javanese provenance, the Kashmiri shawl woven to a 200-year-old pattern, the Peranakan-embroidered piece that signals a specific lineage: these are not fashion items with sustainability credentials. They are cultural artefacts with fashion utility.

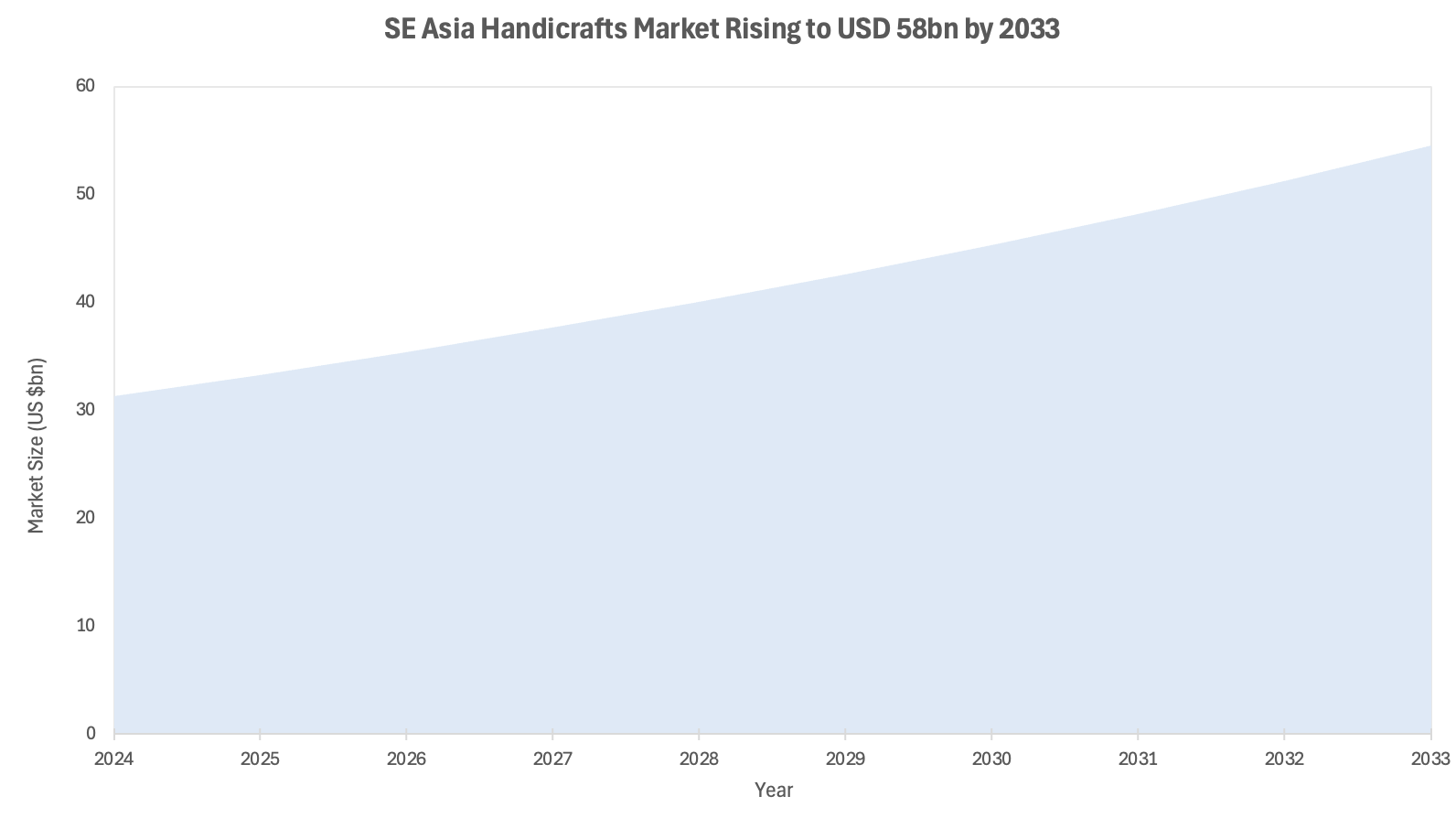

The Southeast Asia handicrafts market reached USD 31.3 billion in 2024 and is projected to reach USD 58 billion by 2033, a compound annual growth rate (CAGR) of 6.37%. The global handicrafts market, at USD 739.95 billion in 2024, is projected to expand to USD 983.12 billion by 2030, with Asia Pacific commanding the largest regional revenue share. These are not niche numbers. They describe a structural market of considerable depth, not yet efficiently intermediated by institutional capital.

Source: IMARC Group, 2025. Figures based on 6.37% CAGR from 2024 base of USD 31.3bn.

The Non-Obvious Mechanism

The conventional read on heritage craft is supply-side romanticism: artisans are disappearing, traditions are dying, preservation is a philanthropic imperative. That framing is not wrong, but it is incomplete. It misses the structural dynamic that makes this a capital opportunity rather than a charitable cause.

The non-obvious mechanism is identity compression. As global incomes rise and cultural homogenisation accelerates, the scarcity premium on authentic cultural goods increases non-linearly. This is not a taste preference; it is an economic consequence of urbanisation, diaspora mobility, and the social signalling function of consumption. When a second-generation Malaysian-British professional wears a hand-woven songket piece to a formal event in London, she is not making a fashion statement. She is asserting cultural continuity in a context where that continuity is under pressure. The item's value derives not from its material or its carbon footprint but from its irreproducibility as a cultural signal.

This creates a structural pricing floor that is independent of fashion cycles. Analysis of luxury brand transactions confirms that heritage brands demonstrate materially higher five-year value retention compared to infrastructure-first luxury competitors; the Valentino maison sold for €258 million in 1998, whilst Golden Goose attracted €2.5 billion valuation offers in 2025. The more direct inference: cultural provenance embedded in a heritage piece functions as a store of identity value that the market has not yet fully priced. The second mechanism is supply inelasticity. You cannot scale hand-woven ikat the way you scale a recycled polyester hoodie. Artisan knowledge takes decades to accumulate and is not recoverable once a generation of weavers retires, creating a structurally constrained supply curve against a growing demand signal。

Source: Grand View Research / Alibaba Seller Blog, 2024. North America, Europe, Latin America and MEA shares are indicative estimates based on standard regional breakdowns.

Investor Implications

For family offices and high-net-worth (HNW) allocators with cultural or geographic proximity to Southeast Asia or South Asia, this is not an abstract thesis. It is a capital allocation question that sits across several portfolio categories simultaneously.

Three structural implications stand out. First, the artisan-economy supply chain is a real asset with brand-equity characteristics. Investing in heritage craft platforms, whether vertically integrated brands, artisan cooperatives, or cultural commerce infrastructure, offers exposure to a supply-constrained asset with compounding provenance. Products with verified artisan stories command 20–30% price premiums today; as authentication technology matures and cultural consumption grows, that premium is more likely to widen than compress.

Second, the cost of capital advantage held by culturally proximate investors is material and time-limited. A family office in Singapore or Kuala Lumpur sourcing a heritage textile brand in Central Java or Tamil Nadu holds informational, relational, and reputational advantages that a European impact fund cannot replicate. That edge has a shelf life: as the thesis becomes consensus, valuations will reflect it. The window to enter at pre-institutional pricing is, by most structural reads, a three-to-five-year window. Third, the risk-adjusted return profile is more favourable than it appears on conventional metrics. Heritage craft businesses are typically capital-light in their early stages, operationally close to their founders, and protected from competitive disruption by the very inimitability that defines their cultural value. The principal risks, artisan succession, counterfeiting, and platform dependency, are identifiable and, in the most sophisticated cases, manageable through structural investment terms.

More than 50% of family offices in Southeast Asia are now deploying capital with explicit environmental and social objectives. The more useful reframe is not environmental, social and governance (ESG) but identity-capital economics: the thesis is that cultural assets compound value over long cycles in ways that conventional impact instruments do not.

Near-Term Catalysts and Policy Outlook

0–3 months: US tariff escalation throughout 2025 accelerated the China+1 sourcing shift, redirecting global procurement towards Southeast Asian artisan producers. The beneficiaries include Vietnam's textile sector, Indonesia's craft exporters, and India's handloom industry. Several Southeast Asian governments, including Indonesia and India, maintain active craft export promotion programmes that function as partial risk mitigation for early-stage investors.

3–12 months: The generational wealth transfer now accelerating across Asia is the structural tailwind most directly relevant to this thesis. Singapore added approximately 600 new single-family offices in 2024 alone, taking the total above 2,000, a 400% increase on 2020 figures. Next-generation principals in these offices are reshaping allocation priorities towards identity-relevant assets, with over 50% of Southeast Asian family offices now deploying capital with clear environmental and social objectives. The convergence of this capital formation with a maturing heritage craft investable universe represents the clearest near-term deployment opportunity.

Scenarios:

Base: Heritage craft platforms in Southeast Asia attract increasing allocations from culturally proximate family offices. Valuations remain below Western luxury comparables. The pricing gap narrows over a five-to-seven-year horizon as authentication infrastructure matures and export channels deepen.

Upside: A named acquisition by a Western luxury conglomerate, LVMH, Kering, or a comparable, of a Southeast Asian or South Asian heritage brand catalyses a rerating of the entire category. This is not speculative: Western luxury groups have systematically acquired heritage craft DNA for decades, and the remaining uninvested geographies are narrowing.

Downside: Artisan succession failure in key craft communities, exacerbated by rural-to-urban migration, constrains supply more rapidly than demand moderates. In this scenario, the investment thesis is still directionally correct but operational risk at platform level becomes the binding constraint.

Conclusion

Sustainable fashion's investment thesis has been framed almost entirely around environmental compliance. That framing captured real value early; it is now crowded, increasingly regulatory in character, and converging towards commodity. The cultural thesis, grounded in identity economics, supply inelasticity, and the compounding value of authentic provenance, is structurally distinct and not yet reflected in valuations.

For family offices with cultural proximity to Southeast Asia or South Asia, the case is sharper still. The informational advantage is real, the entry window is open, and the long-duration nature of the asset matches the multigenerational investment horizon that defines the best family office capital. The structural question is not whether this category will be priced properly. It is whether your portfolio is positioned before that happens or after.

References

Grand View Research – Handicrafts Market Size And Share | Industry Report, 2030 – 2025

IMARC Group – Southeast Asia Handicrafts Market Size, Share, Trends, 2033 – 2025

Alibaba Seller Blog – 2026 Southeast Asia Textile Crafts Export Strategy White Paper – February 2026

LinkedIn / Armando Zuccali – The Heritage Resilience Hypothesis: Evidence from Luxury Brand Transactions – January 2026

Gunung Capital – Stewarding Legacy Through Sustainability: The Evolving Role of Southeast Asia's Family Businesses – June 2025

CFA Institute – How Next-Gen Investors Are Reshaping Family Offices in Southeast Asia – April 2026

BCG – The Asia Generational Wealth Report 2025: Succession in a New Era – November 2025

LinkedIn / Kevin B K Tan – The Human Legacy of Wealth and How Family Offices Are Shaping Cultural Legacy – October 2025

Lighthouse Canton – Asia's Family Offices Shift Gears as Generational Wealth and Portfolio Strategy Evolve – July 2025

London Business School StartHub – Beyond Affluence: How Luxury Brands Sustain Value in a Shifting Market – November 2025

This article is for information and discussion only and does not constitute investment advice or a recommendation.