Sand, Scarcity and the Margin No One Has Priced

The most mundane material in construction is becoming one of its most constrained inputs, and capital markets have not noticed.

Why This Matters

Britain's brownfield-first housing agenda is built on contaminated ground. Every consent carries a mandatory remediation obligation, and the feedstock required to fulfil it is the same material that primary reserves can no longer reliably supply

The regulatory stack is fully in place: Part IIA EPA 1990, Environment Act 2021, updated LCRM guidance June 2025, mandatory Biodiversity Net Gain. Contaminated spoil is now legally expensive to handle carelessly

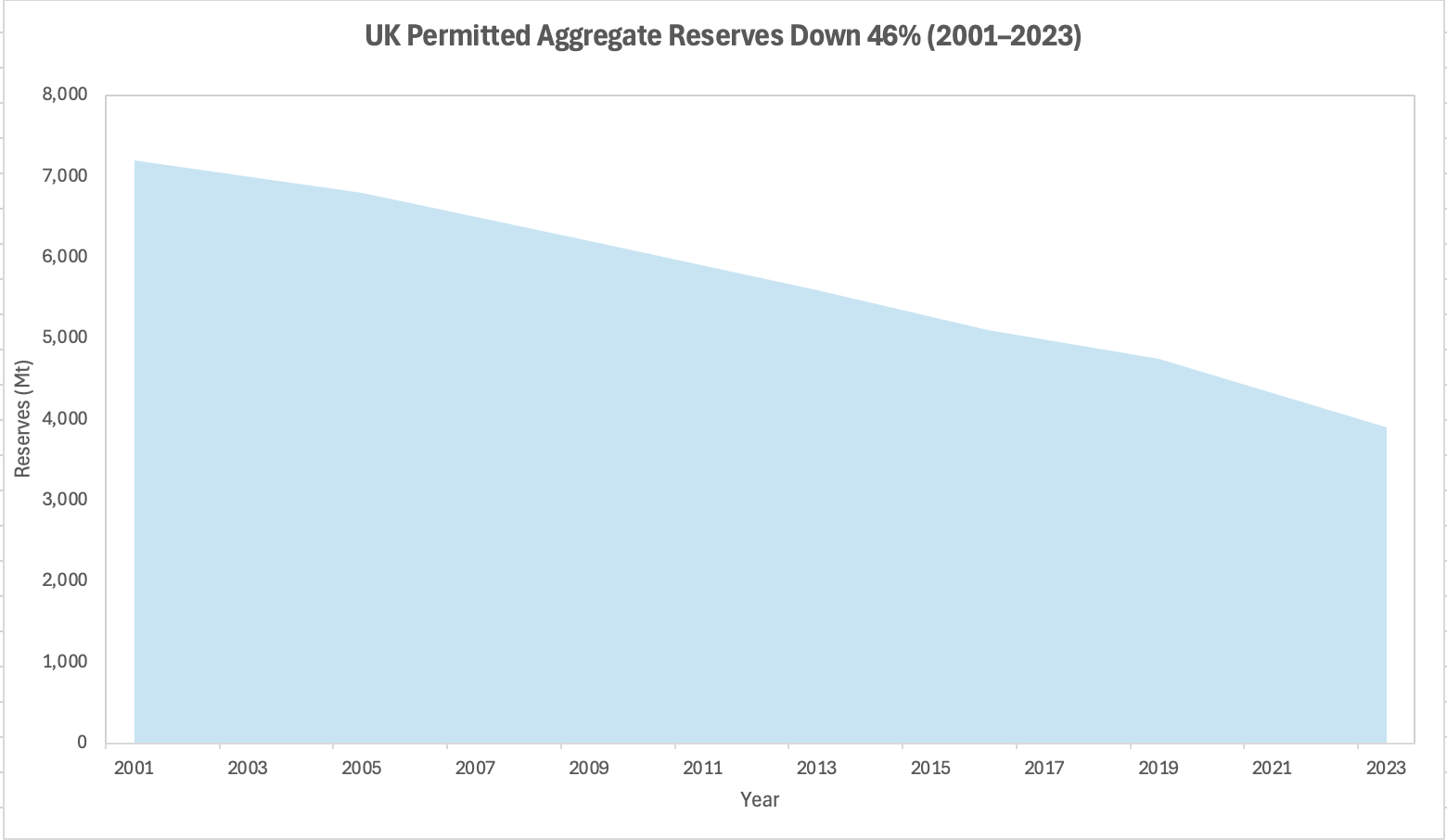

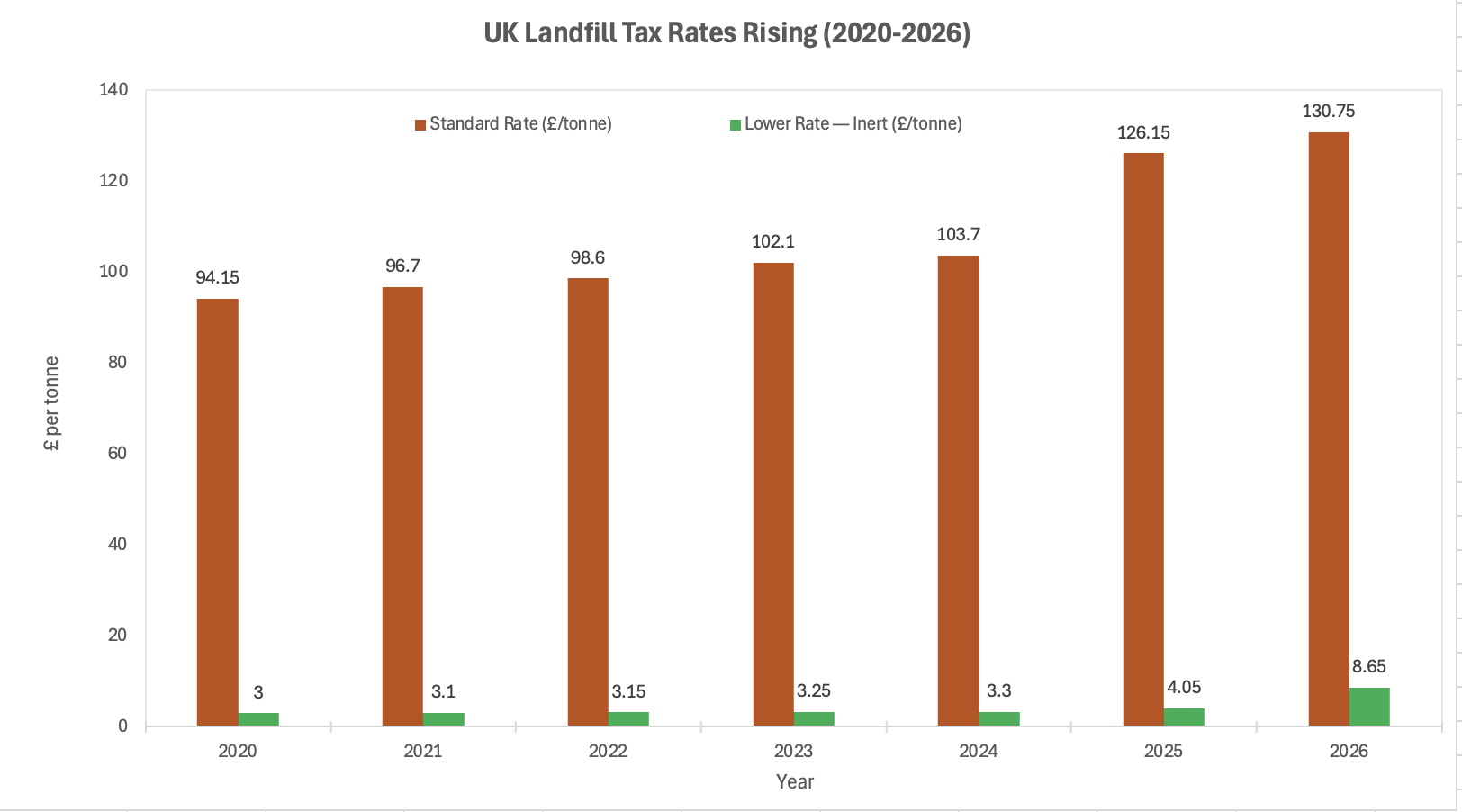

UK permitted reserves are down 46% since 2001, the right-specification quarries are not being replenished, and landfill tax doubles for inert materials from April 2026. The operators with permitted capacity and processing control are the only ones positioned to capture what follows

The Core Shift

Before a single brick is laid, Britain's construction pipeline faces a feedstock problem that predates any planning debate: a significant proportion of developable land in the UK is contaminated. Decades of industrial activity, from coal gas works and petrol stations to chemical plants, foundries and landfill, have left an estimated 300,000 to 400,000 potentially contaminated sites across England alone. Under the National Planning Policy Framework and Part IIA of the Environmental Protection Act 1990, developers are legally required to remediate land to a standard fit for its intended use before construction commences. That obligation is not discretionary. It is a pre-commencement planning condition on virtually every brownfield consent, and local planning authorities are increasingly applying the precautionary principle even to sites with only a historic industrial adjacency.

The regulatory burden has intensified materially since 2021. The Environment Act 2021 introduced mandatory waste hierarchy compliance, electronic waste tracking and producer responsibility obligations for construction and demolition waste, meaning every tonne of excavated spoil now carries a documented chain of custody requirement. The Land Contamination Risk Management guidance was updated by the Environment Agency in June 2025, shifting the regulatory framework explicitly toward proactive risk prevention rather than reactive clean-up. Biodiversity Net Gain, mandatory for major developments since February 2024 and extended further through December 2025 planning reforms, adds yet another layer of ground-condition assessment and remediation complexity to brownfield sites. The cumulative effect is a regulatory stack that makes contaminated spoil progressively more expensive and legally fraught to handle carelessly, and makes operators with licensed, compliant processing facilities progressively more valuable.

The remediation obligation creates a direct demand vector for processed aggregate. Contaminated excavation spoil cannot be redistributed on-site; it must be classified, treated or removed. Clean, specification-grade fill and capping material must be imported to replace it. Where soils are hydrocarbon- or heavy-metal-contaminated, engineered fill with precise grading and permeability characteristics is required. This is not bulk commodity aggregate. It is processed, permitted, traceable material commanding a margin premium over standard fill, and it is demanded at the exact moment that primary supply is tightening.

As Ed Conway, economics editor of Sky News and author of Material World (2023), argues: civilisation is quite literally built on sand, from the concrete and plate glass of modern cities to the silicon chips underpinning the digital economy, yet no country has nearly enough sand to operate without carefully managed extraction and substitution. Conway's central observation is that the physical foundations of economic activity are chronically underweighted in both policy and markets. In the UK context, that blind spot has a specific and measurable expression: a 46% collapse in permitted aggregate reserves since 2001, documented in the government-commissioned Aggregate Minerals Survey 2023, from approximately 7,200 million tonnes to 3,900 million tonnes. England and Wales recorded a decline of 396 million tonnes in permitted reserves between the 2019 and 2023 surveys alone. The Mineral Products Association has warned that proposed planning reforms, designed to accelerate housing consents, will do little to address the declining supply of the materials physically required to build those homes.

Source: BGS Aggregate Minerals Survey 2023 / MPA.

Recycled and secondary materials, principally construction, demolition and excavation waste, asphalt plannings and industrial by-products, now constitute approximately 31% of Britain's 240-million-tonne annual aggregate market, with 74.3 million tonnes processed in 2023. Britain is one of the highest-recycling-rate aggregate economies in Europe, yet two-thirds of supply still depends on primary extraction. The recycled share is large enough to matter structurally, but not large enough to cushion a primary-supply squeeze on its own.

The Non-Obvious Mechanism

The consensus treats recycled aggregate as low-grade and low-margin. That framing is becoming analytically obsolete. Three second-order dynamics are reshaping the economics in ways not yet reflected in operator valuations or infrastructure procurement models.

First, the landfill tax escalator is compressing the economics of the entire waste-disposal value chain. The standard rate reached £126.15 per tonne from April 2025 and rises to £130.75 from April 2026. More consequentially, the lower rate applied to inert materials such as excavation spoil and demolition rubble, the primary feedstock of recycled aggregate production, more than doubles from £4.05 to £8.65 per tonne from April 2026. Any demolition contractor or civil engineer who previously found it cost-effective to landfill inert waste now faces a materially higher hurdle. The captive-feedstock model of operators who co-locate waste acceptance with aggregate processing is acquiring genuine option value.

UK Landfill Tax standard and lower (inert) rates (£/tonne), 2020–2026. Standard rate hits £130.75 from April 2026; lower (inert) rate more than doubles to £8.65, removing the cost advantage of landfilling inert waste. Source: HMRC / GOV.UK.

Second, the quarry-site landfill exemption is itself under threat. The MPA has flagged that proposed revisions to landfill tax include removing the long-standing exemption for quarry sites from 2027. This would raise the cost floor for primary producers and further narrow the price gap between virgin and recycled material, accelerating the market share transition that recyclers are already capturing.

Third, the planning bottleneck that constrains primary reserve permits is not symmetric. New quarry consents require multi-year environmental assessments and increasingly hostile planning environments. Recycled aggregate facilities require only waste management permits and are categorised differently in the planning system. The processing side of the market can therefore scale faster than the primary side: a structural asymmetry that accumulates over time into permit scarcity at the quarry level and processing-capacity scarcity at the recycler level. Both are defensible moats.

Investor and Stakeholder Implications

Margin in the aggregate sector is a function of three variables: feedstock security, gate-fee income and logistics optionality. Operators who control all three are running a fundamentally different business from those who buy spot feedstock and sell into a commodity market. The former resembles a toll road; the latter resembles a trading book.

For listed construction materials companies, this is underappreciated in sell-side coverage. Analysts typically model aggregate volumes against construction output indices and apply a flat unit margin. They do not model reserve depletion rates, permit renewal risk or the compounding effect of landfill tax on gate-fee income. As primary reserve years-of-supply shorten, with England and Wales holding only 460 million tonnes of permitted sand and gravel reserves in 2019, the scarcity premium accruing to permitted sites will appear in land valuations and acquisition multiples before it appears in earnings.

For infrastructure procurement, the input cost model needs updating. Aggregate procurement assumptions embedded in 2022–2024 cost plans may be systematically under-pricing material costs through 2026–2030, particularly for large-volume civil projects in regions where local permitted reserves are most depleted. The UK recycled concrete aggregates market is projected to grow from USD 28.6 billion in 2025 to USD 64.9 billion by 2032 at a 12.4% CAGR, reflecting in part this structural repricing.

Near-Term Catalysts and Policy Outlook

Three catalysts are material over 2026.

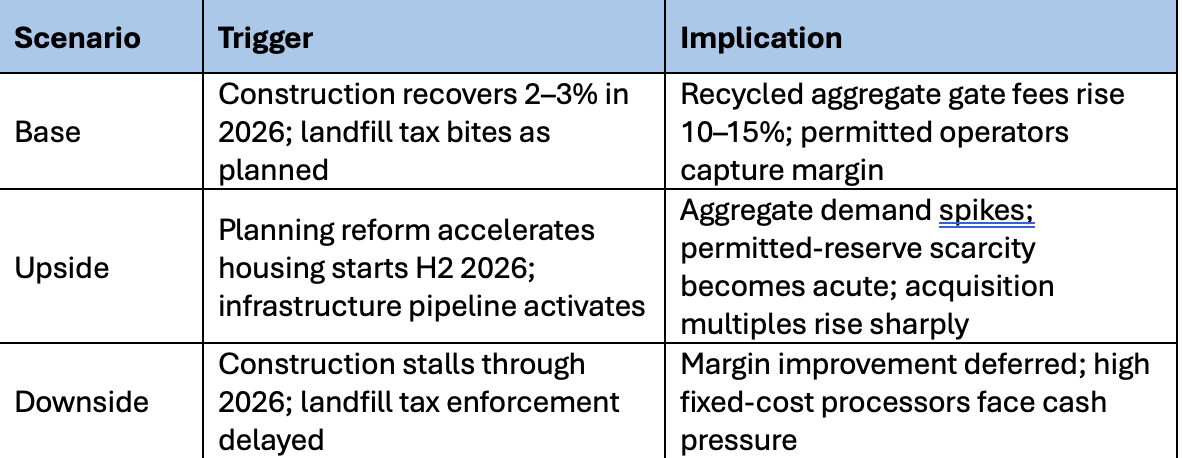

First, UK construction output. January 2026 ONS data recorded a 0.2% monthly rise, the first increase after three consecutive falls, with repair and maintenance driving recovery while private new housing remained under pressure. PwC forecasts real output growth accelerating to 3–4% in 2026–27, led by infrastructure spend in energy and water. If that recovery is front-loaded into Q2 2026, aggregate demand will snap back faster than procurement pipelines currently anticipate.

Second, the April 2026 landfill tax implementation. The doubling of the lower (inert) rate is the single most direct pricing signal the market has received for inert waste processing. Operators who have invested in permitted facilities capable of accepting, classifying and processing inert waste streams will see gate-fee income and feedstock economics move in their favour simultaneously.

Third, the government's response to AM2023. The MPA has called for urgent action, and the report has triggered a formal call for permitted aggregate reserves to be treated as a strategic planning matter rather than a local mineral authority discretion. Any policy statement indicating revised mineral planning guidance or mandatory reserve thresholds would be a direct re-rating catalyst for permitted operators.

Conclusion

The non-consensus read is this: sand scarcity is not a long-horizon thematic risk. It is a near-term operational margin story that is already playing out in the data, accelerated by fiscal policy, and entirely absent from mainstream capital markets pricing. The 46% decline in permitted UK reserves since 2001 is a documented fact from a government-commissioned survey. The landfill tax step-changes in 2025 and 2026 are enacted legislation. The construction demand recovery is forecast across PwC, RICS and Arcadis for 2026–27.

The structural read-across is that permitted aggregate sites, particularly those integrated with contaminated land remediation, recycled processing and gate-fee income, are transitioning from commodity infrastructure into permit-scarce, margin-defensible assets. Brownfield remediation policy is not a cyclical tailwind; it is the demand catalyst that makes the integrated operator model structurally durable regardless of where construction output sits in any given quarter.

As Conway observed, the physical foundations of civilisation are the last thing markets think about, until they can no longer ignore them. In the UK aggregate market, that moment of recognition is approaching. The cyclical overlay is that 2026 is the inflection year where policy-driven cost escalation, tightening regulation and demand recovery arrive simultaneously. What is mis-priced is not the macro trend. It is the operational leverage of operators who sit at the intersection of permitted capacity, waste acceptance, contaminated land treatment and logistics control. That intersection is where the margin is, and that margin is not yet in the models.

References

Ed Conway – Material World: The Six Raw Materials That Shape Modern Civilisation – Hutchinson Heinemann, 2023

British Geological Survey / MHCLG – Aggregate Minerals Survey 2023 (AM2023) – 2025

Mineral Products Association (MPA) – Government-funded report triggers call for action on falling aggregate reserves – August 2025

Mineral Products Association (MPA) – Record recycling rates amid calls for fresh official government data – September 2025

HMRC / GOV.UK – Landfill Tax: increase in rates from 1 April 2026 – November 2025

Hills Waste Solutions – Landfill Tax Increase for 2025 – March 2025

Environment Agency – Land Contamination Risk Management (LCRM) guidance – updated June 2025

Environment Act 2021 – legislation.gov.uk – November 2021

HM Government – Planning and Infrastructure Bill: next steps – 2025

Defra / MHCLG – Planning reforms: delivering homes, supporting farmers and protecting nature – December 2025

PwC – UK Construction Sector Forecast for continued growth – September 2025

Arcadis – UK Construction Market View Spring 2026 – 2026

RICS / Modus – What is the economic outlook for 2026? – November 2025

ONS – Construction output in Great Britain: January 2026 – March 2026

Mobility Foresights – UK Recycled Concrete Aggregates Market Size and Forecasts 2032 – January 2026

The Developer Live – Toxic towns: What if the houses are built on contaminated land? – August 2025

This article is for information and discussion only and does not constitute investment advice or a recommendation.