Regulation as Moat: Why Asia's Compliant Suppliers Are About to Capture Generational Returns

Author: Justin Kew, Martin Sacchi

Executive Summary

The European regulatory environment is undergoing major recalibration: 2025 has brought an “omnibus” reform intended to simplify various regulations predominantly around sustainability and supply-chain laws, creating both delay and concentration of impact. As a result, compliance burdens have narrowed, but regulatory pressure has intensified for large importers and high-emission supply chains.

For investors attuned to geo-politics and supply-chain arbitrage, this dynamic shift means that Asian manufacturers with compliance-ready infrastructure — low-carbon production, traceability, and scale — are emerging as rare but powerful winners. What looked like a broad regulatory wave has evolved into a selective structural moat.

The Changes so Far

CSRD Complexity & Delay

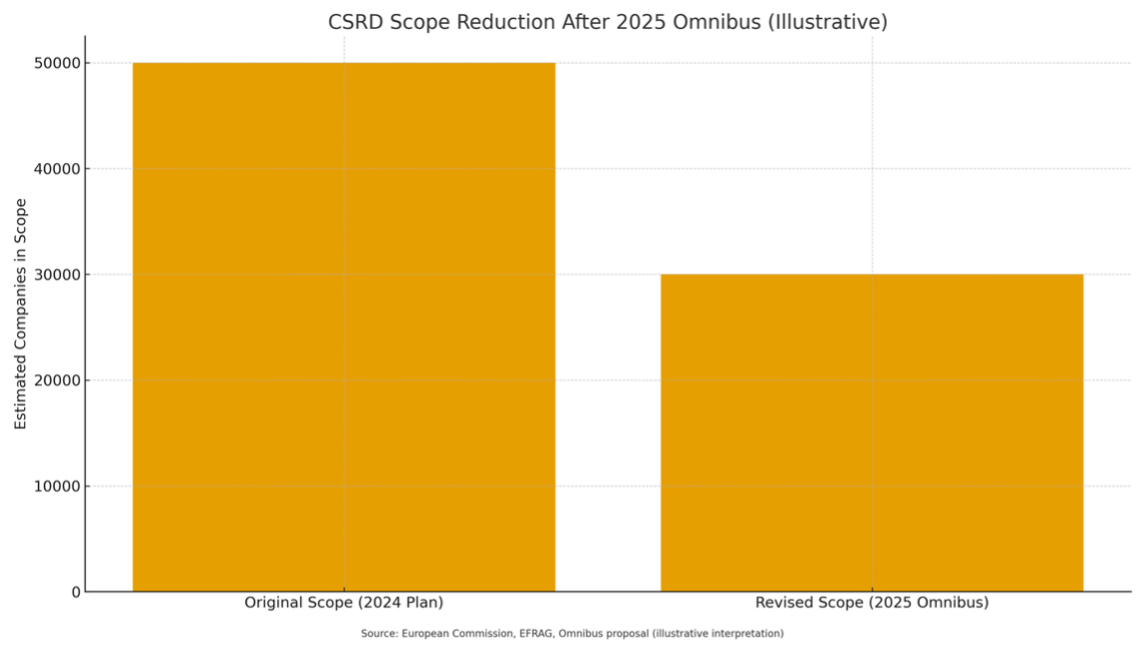

In 2025, the EU passed an Omnibus reform delaying some CSRD reporting waves: companies with 250+ employees (but not in first wave) will report only starting FY 2027, and many listed SMEs will be exempted.

While the first wave (large companies, >500 employees) remains on track (reporting FY 2024 data in 2025), the overall effect is a narrower pool of regulated firms than initially expected.

Revised sustainability standards (ESRS drafts) were released by EFRAG mid-2025, but public comment and final adoption remain ongoing — creating compliance uncertainty.

2. EUDR: Delay and Potential Weakening

The EU Parliament recently voted to delay and simplify enforcement of EUDR.

The proposed amendments may reduce compliance burdens for many importers/exporters, undercutting the broad-based impact originally anticipated.

As of today, EUDR’s enforcement remains uncertain — firms are in a de facto extension window.

3. CBAM Still On — But Shifted Towards Major Importers

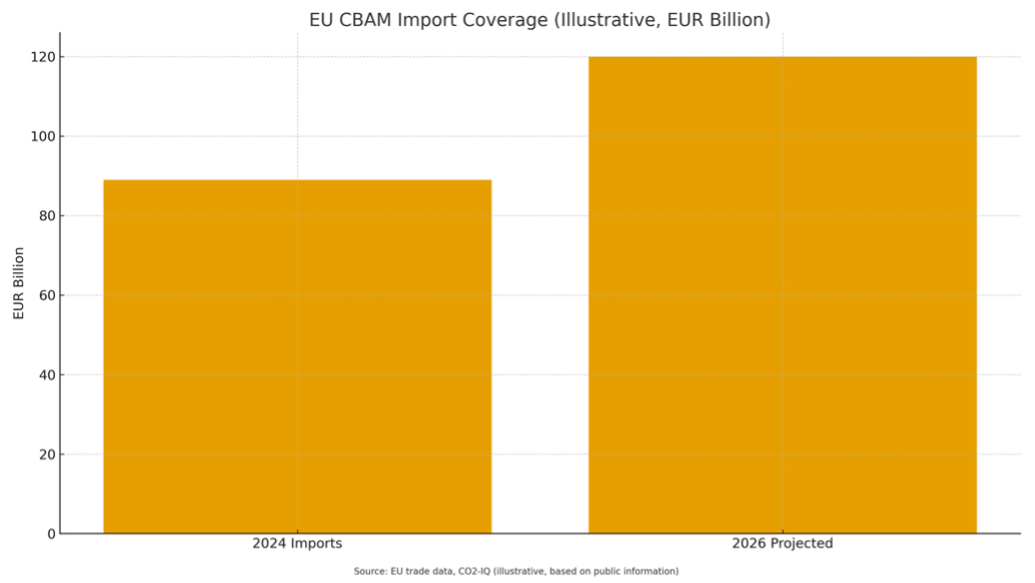

CBAM remains scheduled to enter full-fledged tariff phase from 1 January 2026.

The EU has agreed to exempt importers under 50 tonnes per year — meaning only large industrial-scale importers will bear the obligation.

According to 2024 trade data, roughly EUR 89 bn of imports are in CBAM scope; once fully enforced, these could incur ~€12 billion/year in carbon costs under medium-price scenarios.

Implication: compliance pressure shifts from catch-all broad risk to high-emission, high-volume traders and exporters.

The New Risk/Reward Allocation for Investors

Given the 2025 reforms, many companies—especially SMEs and small exporters—will likely be de-prioritized or exempted. This means the compliance burden is now concentrated. That concentration creates greater value for “compliance-ready winners.”

Key dynamics:

Large-scale Asian producers with capacity to manage audits, emissions reporting, and traceability are being repositioned as “safe-source” suppliers.

Regulation no longer spreads risk broadly; it creates a high barrier to entry, discouraging smaller, informal, non-compliant exporters.

Supply-chain reconfiguration will favour suppliers who pre-invest in data, verification, and low-emission processes.

This is not a broad fairness jungle — it’s a high-stakes bottleneck where compliance becomes a market moat.

The Investment Implications (2026–2032)

Large-scale Low-Carbon Metals & Mineral Exporters (India, Southeast Asia, Korea)

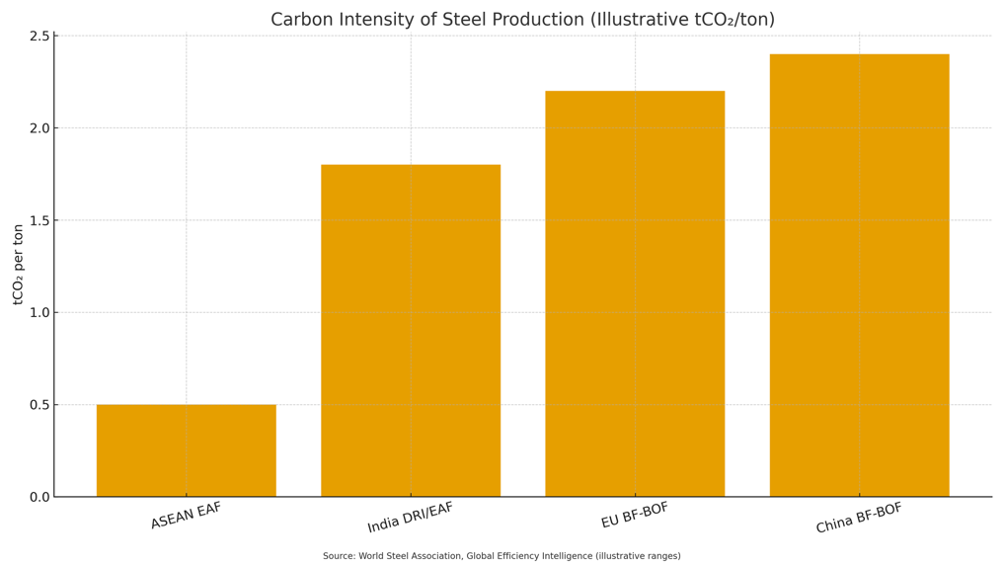

CBAM enforcement will favour high-volume, low-emission producers able to consistently document embedded emissions. Firms in India or Southeast Asia that are already transitioning to EAF / DRI-H₂ steel may claim pricing power.

2. Compliance- and Traceability-Focused Commodity Platforms

Because EUDR enforcement remains uncertain but carbon compliance is mandatory, traceability platforms (for metals, raw materials, forestry, agriculture) become high-value assets. Investors should prioritise technologies that offer emissions tracking, chain-of-custody verification, and documentation for large importers.

3. Industrial Parks & Large-Scale Manufacturing Hubs in Asia (Vietnam, India, Korea)

Companies/investors who build capacity around audited, emissions-compliant supply chain infrastructure gain a structural advantage — especially for commodity-intensive sectors exporting to the EU.

4. Premium OEMs & Exporters with ESG-Compliance Capabilities

Consumer-goods exporters (textiles, furniture, etc.) that internalize compliance costs may command pricing premium from EU clients unable to rely on smaller vendors.

Conclusion

The 2025 EU regulatory reshuffle has narrowed the field—but sharpened the stakes. What initially looked like a broad compliance wave has transformed into a selective structural squeeze: compliance now matters, but only for large-volume, emission-intensive supply chains.

This shift turns compliance into a strategic moat. For investors, Asian companies that have already invested in low-carbon processes, traceability, and regulatory-grade supply-chain transparency are now exceptionally well-positioned. The regulatory changes may have slowed for many—but they have intensified for those who matter.

If you want to capture generational returns from this pivot, focus not on mass-market wins, but on scale, compliance-readiness, and supply-chain resilience.