Industrial Policy Is the New QE: Where the Next Trillion of Capex Will Flow

Author: Justin Kew, Martin Sacchi

Industrial policy has replaced monetary policy as the dominant driver of capital formation

For more than a decade, quantitative easing (QE) was the primary force shaping global liquidity and asset prices. That era is fading. In its place, a new capital-allocation regime has emerged—one where governments, not central banks, are now the most powerful allocators of industrial capital.

Across the US, EU, and Asia, industrial-policy mega-programmes are deploying over USD 1 trillion in incentives, subsidies, tax credits, and direct capex commitments. Unlike QE—which inflated financial assets—this policymaking cycle is driving real-economy capex, transforming supply chains, manufacturing footprints, energy systems, and technology ecosystems.

The strategic goal is clear: rebuild industrial capacity, secure supply chains, accelerate decarbonisation, and strengthen regional economic sovereignty.

For investors, this represents the most important capital-allocation shift since 2008.

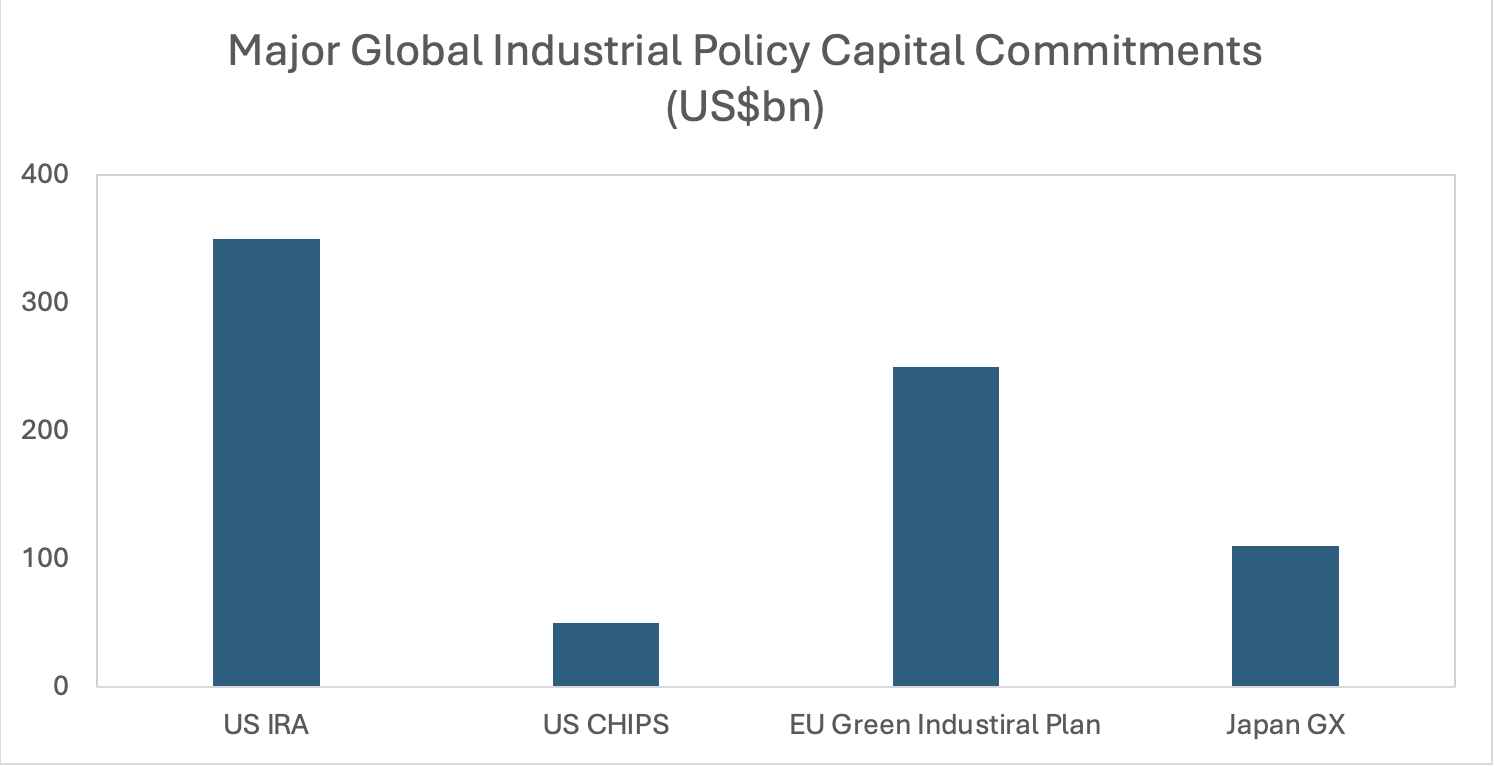

The Scale: More than US$1trillion already committed

The world’s largest economies are deploying unprecedented industrial-policy packages:

United States – Inflation Reduction Act (IRA): US$369bn: Incentives primarily targeted at clean energy, EVs, batteries, hydrogen, and domestic manufacturing.

United States – CHIPS and Science Act: US$52.7bn: Semiconductor R&D, new fabs, supply-chain reshoring.

European Union – Green Deal Industrial Plan: EUR 250bn: Net-Zero Industrial Act, Critical Raw Materials Act, and decarbonisation incentives.

Japan – GX (Green Transformation) Programme: JPY 20 trillion: A decade-long investment cycle in hydrogen, storage, nuclear, and grid resilience.

These packages alone exceed US$800 billion. When national co-investment, private-sector matching, and downstream infrastructure capex are included, the near-term effective spend surpasses USD 1 trillion.

Where will the next trillion of capex will flow?

1. Transmission, Grid Infrastructure, and Storage

Industrial electrification, EV penetration, AI data-centre growth, and heat pump adoption mean grid reinforcement is the bottleneck of the transition.

The IEA estimates US$600bn/year is needed by 2030 for global grid expansion.

Investment opportunity: utilities with aggressive capex cycles, grid-equipment manufacturers, cable producers, storage-integrated IPPs.

2. Semiconductors & Strategic Manufacturing

More than 50 semiconductor fabs announced since 2021 (SEMICO data).

The US and EU are in a multi-year race to localise high-end chip production.

Investment opportunity: equipment manufacturers, advanced packaging, materials supply chains, and “friend-shoring” in ASEAN.

3. Clean Energy & Hydrogen Ecosystems

The IRA alone is catalysing US$110bn+ in private clean-energy capex

Japan and Korea’s hydrogen strategies are accelerating regional adoption.

Investment opportunity: electrolysers, hydrogen transport, ammonia value chains, storage, fuel-cell ecosystems.

4. EV Batteries & Critical Minerals

China retains dominance, but IRA kicked off the process and recent various new policies from current US presidency administration and the EU is accelerating the reshoring incentives, leading to the shifting of investment towards the US, Canada, Indonesia, and Australia.

Investment opportunity: battery manufacturing, recycling, precursor materials, critical-metals processing.

5. Geopolitical Supply-Chain Rewiring

Friend-shoring and dual-sourcing create opportunities for ASEAN, India, Mexico, and Eastern Europe.

Over US$200bn in manufacturing FDI has already moved out of China since 2018 (UNCTAD).

Investment opportunity: industrial parks, logistics, secondary manufacturing hubs, embedded-carbon traceability platforms.

Why This Matters for Investors?

QE inflated asset valuations; industrial policy will reshape real-economy cashflows.

The opportunity is not to simply buy “green” or “tech”, but to identify policy-supported capex bottlenecks where scarcity creates pricing power.

Winners will be firms directly tied to:

grid and transmission expansion

battery and storage capacity

semiconductors and next-gen manufacturing

critical materials

energy-transition infrastructure

Asia-EU supply-chain linkages

This is the new macro regime. Industrial policy is the new QE—but with hard assets, not liquidity.

Conclusion

The era dominated by Quantitative Easing (QE), which primarily inflated financial assets and global liquidity, is now fading. In its place, a powerful new capital-allocation regime driven by Industrial Policy has emerged. Governments across the US, EU, and Asia are deploying over $1 trillion in incentives and subsidies to strategically rebuild industrial capacity, secure supply chains, and accelerate decarbonisation. This massive shift represents the most significant capital-allocation change since 2008. Unlike QE, this new macro regime is driving real-economy capex into hard assets, transforming foundational sectors like grid infrastructure, advanced manufacturing, and critical minerals. For investors, success hinges not merely on buying "green" or "tech," but on identifying the policy-supported capex bottlenecks—such as transmission expansion and battery capacity—where scarcity generates true pricing power and reshapes real-economy cashflows. Industrial policy is the new QE, but this time, the focus is on tangible economic transformation.

Sources

US Congressional Budget Office (2023), Inflation Reduction Act Score

US Department of Commerce (2023), CHIPS Act Funding

European Commission (2024), Net-Zero Industry Act / Green Deal Industrial Plan

Japan METI (2024), GX Roadmap

IEA (2023–2024), Electricity Grids and Clean Energy Investment Outlook

SEMICO Research (2023), Global Fab Announcements

UNCTAD World Investment Report (2024)