The Industrialisation of Defence: How Capital Is Being Rewired

Author: Justin Kew

Executive Summary

Jamie Dimon from JPMorgan launched its new $1.5 trillion Security and Resiliency Initiative this week in the US, signals a structural shift in global capital allocation. For the first time in decades, a major global financial institution has explicitly placed defence, advanced manufacturing and resilience at the centre of its long-term investment strategy. It mirrors a broader reality: defence, industrial capacity and sustainability have converged into a unified investment theme across the US, EU and Asia.

The rise of China’s defence-industrial base, persistent munitions shortages in the West, and the geopolitical fracturing of supply chains have triggered a re-rating of the entire security ecosystem. This is no longer about cyclical defence budgets; it is an industrial policy super-cycle.

We wanted to share three investible themes now reshaping capital flows:

European deep-tech defence & dual-use VC — 5× growth in six years but still under-owned.

Heavy capex bottlenecks — shipyards, propulsion, munitions and electronics capacity are now investible industrial assets.

“Security & Sustainability” under SFDR — defence is no longer off-limits; dual-use and resilience infrastructure now fit sustainable mandates.

The new macro regime: security as a capital allocation framework

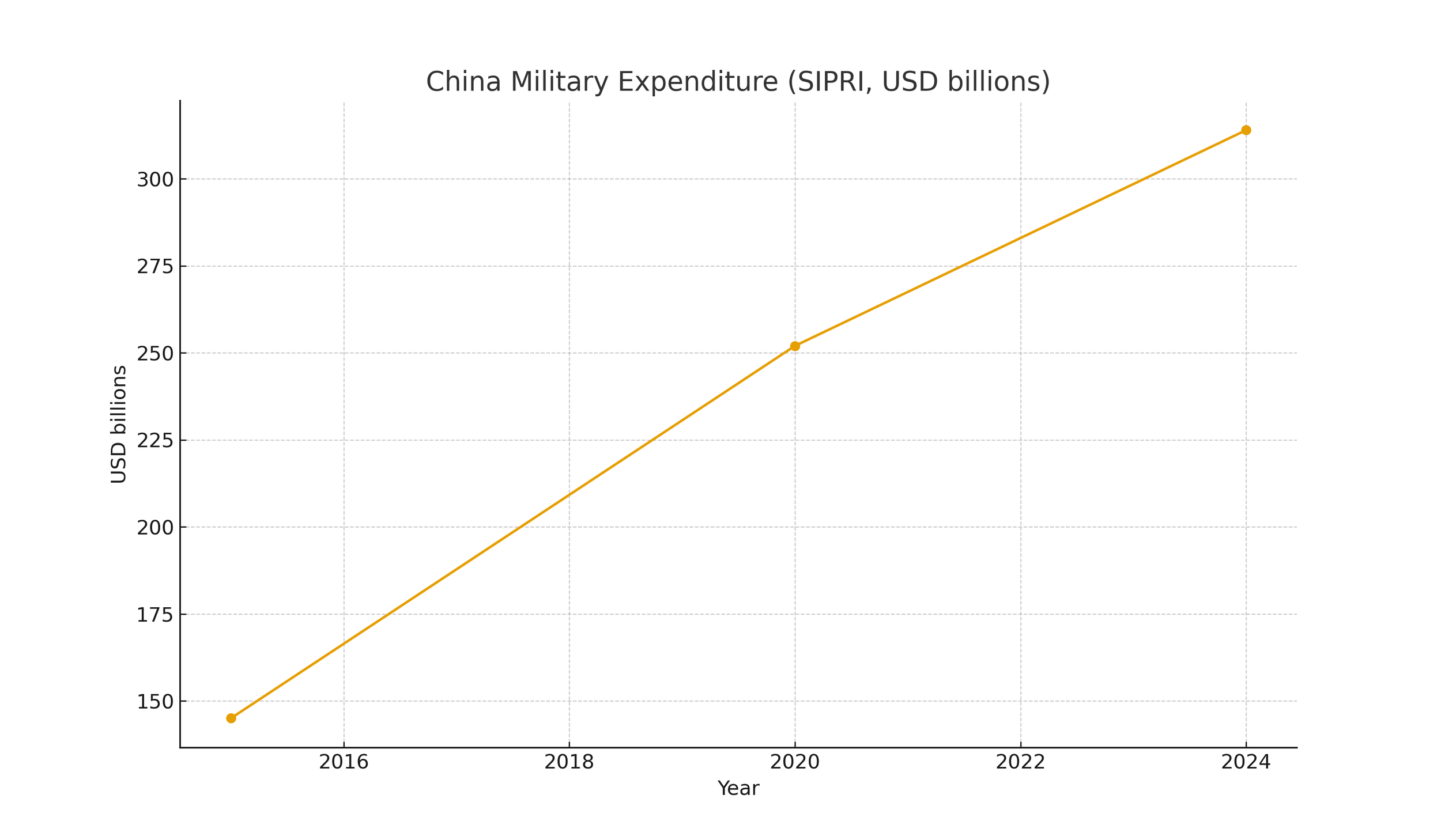

Global military spending reached $2.718 trillion in 2024, up 9.4 percent year-on-year and 37 percent above 2015. Europe’s aerospace and defence turnover rose to €325.7 billion, with defence up 13.8 percent. China increased official military spending to $314 billion, marking its 30th consecutive year of increases.

The geopolitical environment has shifted from episodic crises to a structural national-security paradigm. Defence can no longer be analysed through the narrow lens of annual budgets. Instead, secular drivers matter:

conflict in Europe

Chinese military modernisation

Pacific theatre tensions

semiconductor and critical-minerals vulnerabilities

climate-driven resilience needs

political alignment across major Western capitals

The conclusion: capital markets must now price defence as a long-duration growth sector, not a procurement cycle.

China’s military-industrial expansion: the benchmark for Western strategy

China’s recent military parade showcased hypersonic systems, drone swarms, AI-enabled ISR, and integrated maritime–aerospace assets. But the real signal is industrial:

shipbuilding tonnage > US + EU combined

vertically integrated propulsion, naval and missile production

civilian–military fusion across semiconductors, materials and manufacturing

subsidised deep-tech scale-up with guaranteed demand

China demonstrates the strategic advantage of industrial capacity, not merely technology. Western governments understand this — hence the push towards rebuilding manufacturing bases, scaling yards, expanding munitions lines and securing energy/industrial inputs.

The US pivot: JPMorgan demonstrated defence as mainstream capital

Dimon’s initiative focuses on the most fragile nodes of the US industrial base:

nuclear-submarine supply chains

propulsion

shipyards

munitions

advanced manufacturing robotics

critical-supplier tier upgrades

This is not venture capital. This is institutional capital entering heavy industrial assets, a domain long considered too slow, too political and too low-return. The Pentagon is explicitly courting private capital; Dimon simply made the move visible.

This matters for Europe because the US has now validated defence as an institutional asset class.

Europe’s response: EDIS, EDIP and the Made in Europe rule

The EU’s European Defence Industrial Strategy (EDIS) and the proposed European Defence Industry Programme (EDIP) are direct attempts to rebuild Europe’s industrial backbone.

Key pillars include:

joint procurement incentives

scaling domestic production

secure supply chains

munitions and air-defence production targets

“Made in Europe” requirements for EU-funded platforms

Europe is openly shifting from a procurement mindset to an industrial-capacity mindset, matching the US in intent but not yet in scale.

The investible gap is clear: Europe needs capital — both public and private — to modernise shipyards, propulsion, materials, electronics and deep-tech infrastructure.

Private markets are now the fastest-growing part of defence

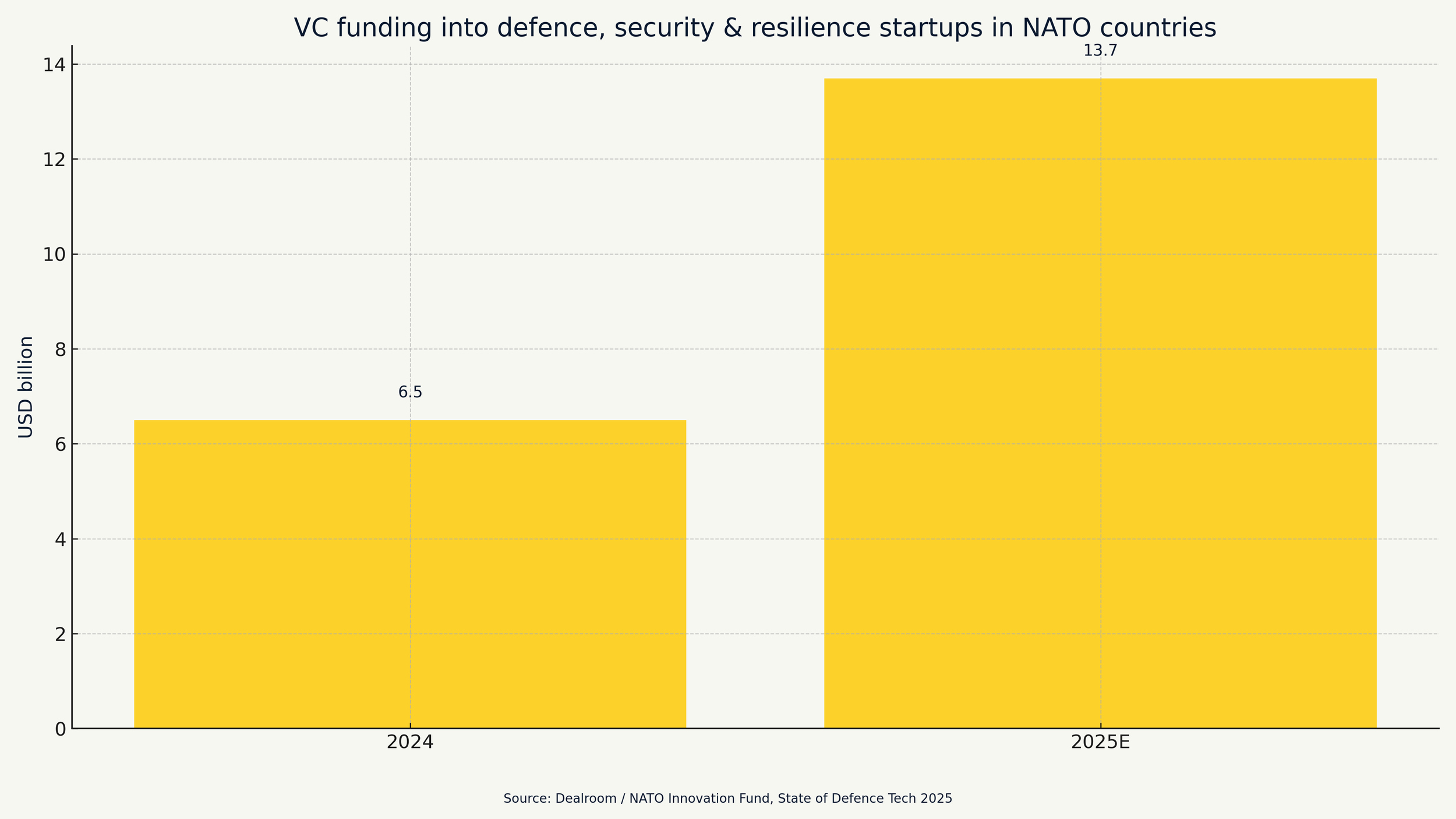

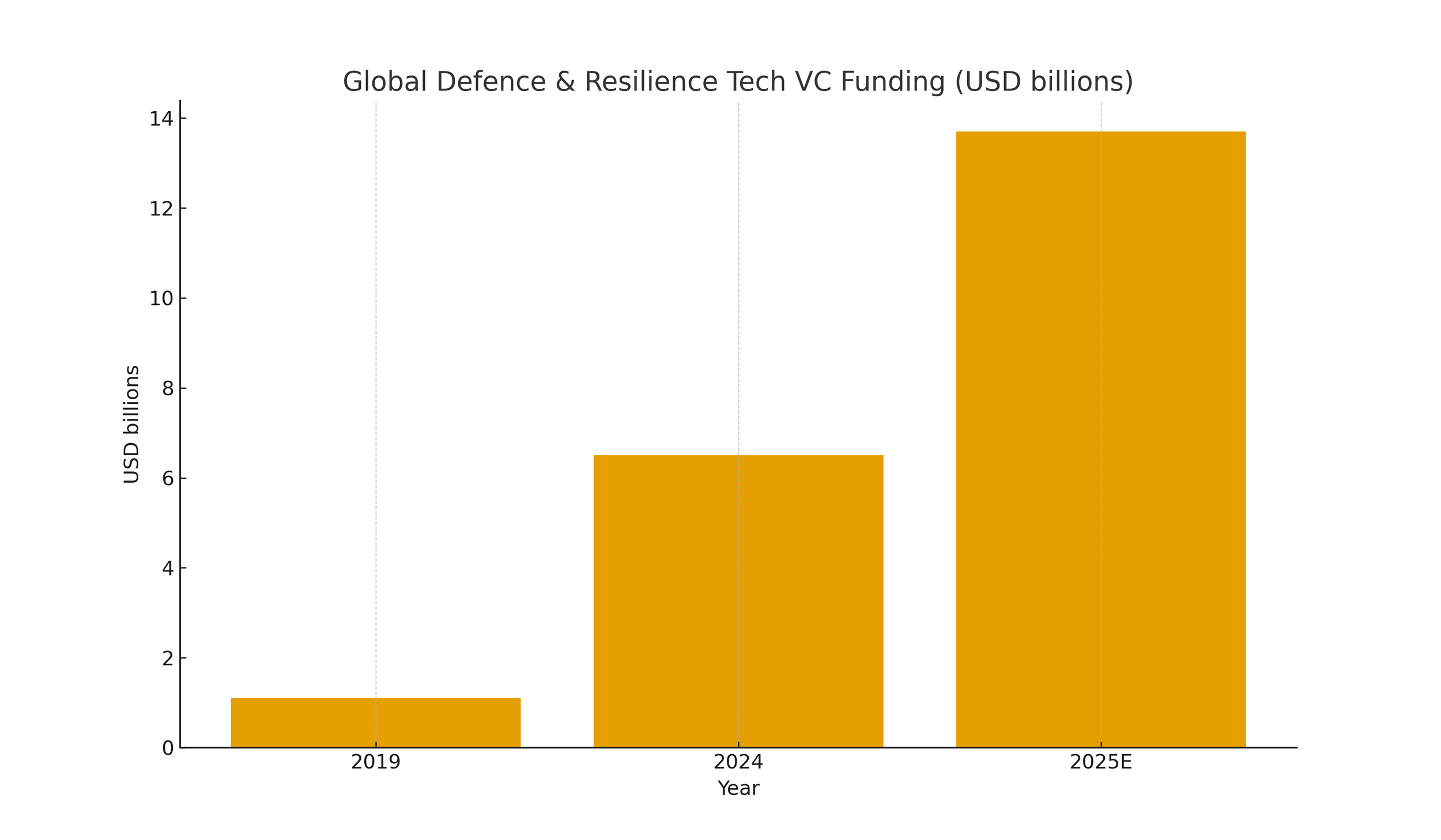

According to Dealroom/NATO Innovation Fund data:

$5.2B was invested in defence/security/resilience startups in 2024 (5× growth since 2019).

Europe captured ~$1.5–2.3B, up from near-zero in 2019.

2025 is on track for $13.7B in NATO-aligned defence/DSR VC investments.

This is where three clear investible themes emerge:

European deep-tech defence & dual-use VC (structural catch-up)

Europe is significantly under-exposed relative to the US. This creates a valuation arbitrage in autonomy, ISR/ sensors, space &. satellites, advanced materials, robotics & propulsion and secure comms & quantum navigation. Europe will need its own Andurils, Shield AIs and SpaceXs.

Heavy capex bottlenecks as investible infrastructure

Europe lacks some key components that supports defence industry from munition lines to naval yards, propulsion factories, semiconductor capacity and critical component manufacturing

These are not defence companies — they are industrial capacity assets, increasingly co-funded by EDIP and national budgets. Returns may resemble infrastructure-style profiles with policy certainty rather than venture volatility.

SFDR, sustainability and the emergence of “Security & Sustainability”

EU guidance now clarifies:

defence is not excluded from SFDR (Art. 8 or 9) unless involving banned weapons

dual-use tech is inherently compatible with sustainability

resilience is now part of the EU’s sustainability taxonomy logic

This opens a pathway for funds like European pension funds, institutional allocators, sovereign wealth funds and long-horizon capital to enter defence and resilience systematically. :

Conclusion

A multi-decade industrial policy cycle is underway across the US, EU and China. Defence is emerging as a core pillar of strategic industrial capacity, not merely government spending. The investible opportunity is shifting toward:

deep tech (dual-use, autonomy, ISR, advanced materials)

industrial bottlenecks (shipyards, propulsion, electronics, munitions capacity)

sustainability-aligned defence under SFDR

Investors who recognise defence as a structural industrial-policy theme — not a budget line — will be positioned for a secular rerating that few market participants are yet pricing correctly.