The Summit That Was Never About Trade

Markets priced the Beijing summit as a tariff reset. They were wrong about what was actually for sale.

The first US presidential visit to China since 2017 lasted two days and generated a communiqué heavy on agricultural purchase commitments and light on everything that actually matters. Hedge fund portfolio managers who traded the headline, a partial tariff rollback and vague language on "strategic stability", were reading the press release and ignoring the contract. The real negotiation ran across five simultaneous tracks: Taiwan arms sales, semiconductor and artificial intelligence (AI) controls, Iran's nuclear stockpile, the Strait of Hormuz, and, almost incidentally, trade. Each track carries a distinct risk premium, a different time horizon, and an asymmetric payoff structure. Getting them confused is a portfolio risk in itself.

Why This Matters

Cost-of-capital error: Markets continue to treat trade normalisation and strategic rivalry as the same variable; they are not, and the mispricing is embedded in volatility surfaces across Asian equities, credit spreads, and energy derivatives.

Chokepoint asymmetry: A Hormuz de-escalation engineered through Beijing's leverage over Tehran is worth more to the global economy than any tariff schedule revision, yet carries no communiqué text and no algorithmic trigger.

Semiconductor timeline mismatch: Export-control tightening operates on a 12–36 month compounding lag; the summit's AI safety dialogue language, however modest, resets the clock on when enforcement credibility next gets tested.

The Core Shift

The summit did not occur in a vacuum. It was shaped by three prior shocks: Trump's tariff escalation to above 140% in mid-2025, which Beijing partially broke using rare earth restrictions; the US-Israeli military strikes on Iran, which closed the Strait of Hormuz and sent Brent crude above $115 a barrel; and a fragile October 2025 trade truce that neither side fully trusted but neither wanted to break. Each of these shocks had already moved the balance of leverage before the two leaders sat down.

Xi arrived with structural confidence. China's control over rare earth processing and permanent magnet supply chains, inputs indispensable for US missile replenishment after the Iran campaign, gave Beijing a coercive tool that Trump had twice flinched from testing. The United States, meanwhile, arrived with depleted advanced munitions stockpiles, higher domestic fuel prices from the Hormuz blockade, and a political calendar that made a visible "win" on trade attractive regardless of what it cost elsewhere. That is the backdrop against which each of the five tracks must be read.

The Non-obvious Mechanism

The trade track is not merely less important than the other four: it is being used to subsidise concessions on them. A visible tariff rollback and a headline Chinese commitment to purchase Boeing aircraft and US agricultural products gives the Trump administration a domestic narrative that absorbs political attention and reduces the scrutiny applied to what was quietly exchanged on Taiwan, semiconductors, and energy.

This pattern has a precedent. The $83.7 billion West Virginia memorandum of understanding from Trump's 2017 Beijing visit exceeded that state's entire gross domestic product and never materialised; the function it served was political cover, not capital allocation. The current trade language likely performs the same role, and a practitioner reading the communiqué should weight it accordingly.

The deeper mechanism is leverage substitution. Beijing is trading a short-term economic concession, opening some market access and moderating rare earth throttling, for a longer-term strategic gain: US pre-negotiation on Taiwan arms sales, a softer AI enforcement posture, and a tacit acknowledgement that China can play a constructive role in Gulf energy security. The economic concession depreciates over 12 months; the strategic gains compound over 10 years. For a PM with a 12-month horizon, the relevant question is not whether the trade deal holds but whether the strategic substitution holds long enough to suppress volatility.

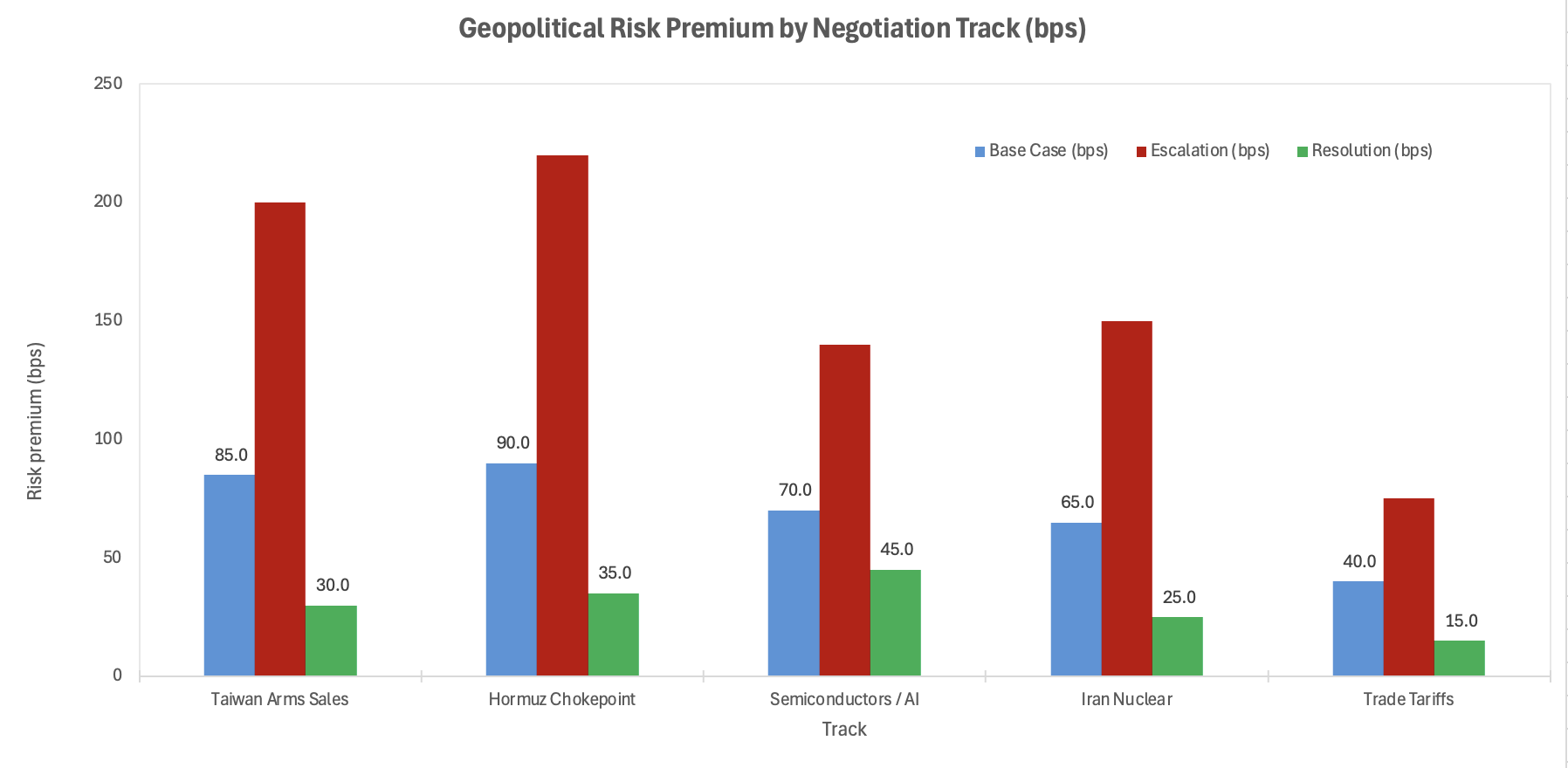

Illustrative incremental cost of capital, in basis points, associated with each Beijing summit negotiation track under three scenarios (resolution, base case, escalation). Values are scenario‑based and intended to show relative ranking rather than precise levels. They are guided by empirical work linking changes in political and geopolitical risk measures to sovereign and commodity risk premia during recent Middle East crises, for example the relationship between declines in ICRG political stability scores and wider sovereign spreads, and documented geopolitical risk premia in energy futures around conflict episodes.

Source: PRS Group, Caldara–Iacoviello Geopolitical Risk index, Gamboa & Romero (CEMLA), Cheng et al., author’s estimates.

Investor Implications

Taiwan and regional equities: Trump publicly confirmed he would discuss US arms sales with Xi, and a bipartisan Senate coalition had been pressing for formal notification of a $14 billion package covering Patriot PAC-3 missiles, NASAMS and asymmetric capabilities. Any informal understanding that slows the pace of US arms approvals in exchange for Chinese behavioural restraint near the island would reduce the near-term military escalation premium embedded in Taiwan Strait-exposed sectors, particularly Taiwanese technology hardware, insurance, and shipping. The risk is directional and not symmetric: a breakdown in that understanding carries a much larger repricing than its maintenance provides a relief rally.

Semiconductors, AI and the export-control clock: The US retains roughly an eight-month lead over China in frontier AI capability, and that gap is the primary variable determining whether Beijing has an incentive to comply with any AI safety dialogue framework. The summit is expected to formalise a dialogue, but without a parallel tightening of export-control enforcement, the dialogue is primarily a delay mechanism that China's diplomatic corps has consistently sought. For semis PMs, the signal to watch is not the communiqué language but the subsequent enforcement actions, licensing approvals, and whether the Commerce Department's revised semiconductor review policy from January 2026 is tightened or quietly relaxed.

Energy, Hormuz and the electro-state thesis: China is the largest buyer of Iranian crude, and the Hormuz blockade, a direct consequence of US-Israeli strikes, has disrupted Chinese supply chains while simultaneously accelerating the geopolitical case for electrification over petroleum dependency. If Beijing uses its leverage over Tehran to facilitate a partial Hormuz reopening or Iranian de-escalation, Trump secures an energy narrative at low direct cost, and China secures secondary sanctions relief and energy price normalisation. The broader structural point is that every week Hormuz remains partially closed, the economic case for the electro-state, China's solar, battery, and EV export model, strengthens relative to the petrostate model that underpins US energy diplomacy. That is a second-order consequence most sell-side energy research has not adequately followed to its conclusion.

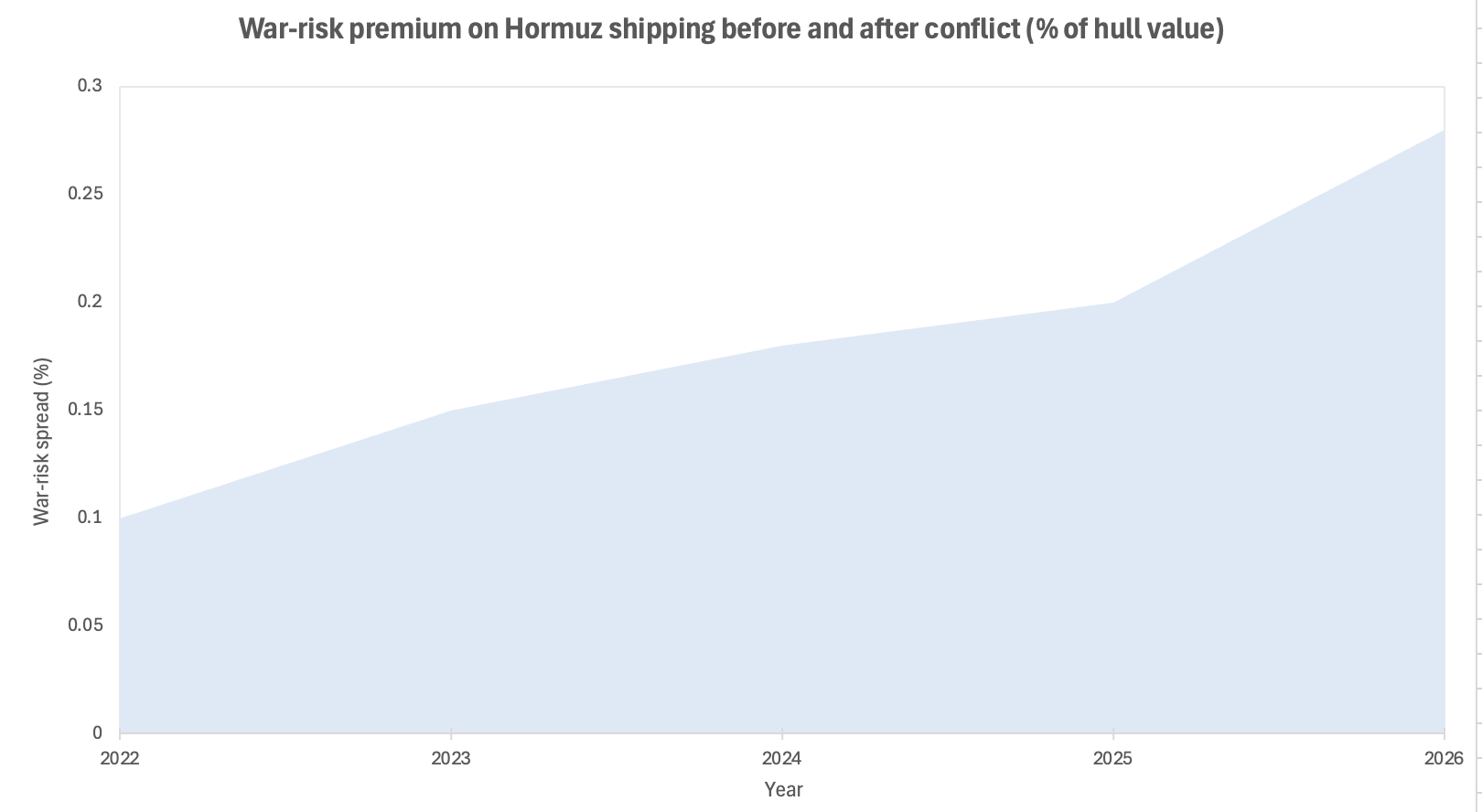

Marine war‑risk cover for vessels transiting the Strait of Hormuz has been repriced sharply. Brokers highlight 25–50% increases in premiums for key Middle East corridors since the latest escalation according to April 2026 market reviews, and that repricing feeds directly into freight rates and working capital needs for commodity traders.

Illustrative marine war‑risk premium (% of insured hull value) for tankers transiting the Strait of Hormuz before and after the recent conflict. Levels are indicative and scaled to reflect April 2026 broker and EY geostrategic analysis that war‑risk premiums for high‑risk Middle East corridors have risen by roughly 25–50% since the latest escalation.

Source: EY Geostrategic Analysis (April 2026), London marine market commentary, author’s estimates.

Near-term Catalysts and Policy Outlook

The next 12 months carry more downside risk than upside from a summit that has already been partially priced. The asymmetry favours the cautious.

0–3 month window: Markets will trade the communiqué. Algorithmic flow will key off tariff rollback language, any Chinese investment headline, and whether Taiwan is explicitly mentioned or conspicuously absent from the joint statement. The more reliable signal for practitioners is operational: watch for enforcement discretion on export licences, any change in the tempo of US arms notification to Congress, and whether the US Navy's Hormuz posture shifts in response to visible Iranian behavioural change.

3–12 month window: Each track will be stress-tested by a local event. A naval incident near Taiwan, an Iranian-linked attack on shipping, an enforcement case against a Chinese AI firm, or domestic political noise in either country will expose the depth, or absence, of the understandings reached in Beijing. The structural case is that the summit constrains escalation at the margin but does not resolve the underlying rivalry; episodic volatility spikes should be expected as each track hits its own stress point.

The following scenarios frame the risk distribution before those stress tests arrive.

Base case: Partial tariff relief, modest but credible language on avoiding full decoupling, slightly tighter but more predictable semiconductor controls, and quiet Chinese signalling toward Iran that reduces visible Gulf escalation. Equity and credit markets lean risk-on, but dispersion between clean-demand and contested-supply-chain names widens.

Upside: Deeper tariff rollbacks, an informal understanding on US arms sales pacing and PLA activity near Taiwan, and a more visible Chinese role in brokering Iranian restraint and Hormuz de-escalation. Geopolitical risk premia compress more materially, particularly in Asian equities, shipping, and energy-intensive sectors.

Downside: Talks break down on semiconductor or Taiwan language, or a subsequent incident exposes the absence of a real understanding, triggering renewed sanctions, export controls, or a kinetic close call that moves from brinkmanship to loss of life. Valuation support from the trade headline evaporates, volatility spikes, and cost of capital rises disproportionately for firms embedded in US-China technology and energy chokepoints.

Conclusion

The summit is a staging point in an emerging dual-system world, not a resolution of it. For hedge fund PMs, the operative question is not whether the tariff deal holds but whether the tacit understandings on Taiwan, semiconductors, Iran, and Hormuz hold long enough to suppress the volatility that markets have not yet fully priced. The trade communiqué is the cover story; the five negotiation tracks are the book. Confusing the two is not a political misreading: it is a portfolio risk.

The balance sheets best positioned to absorb the residual risk are those with diversified demand exposure, limited dependence on leading-edge semiconductors, and no structural reliance on Hormuz transit. The balance sheets most exposed are those that priced the summit as a clean trade reset and built positions accordingly.

References

Council on Foreign Relations, Rush Doshi, Chris McGuire, Heidi E. Crebo-Rediker, David Sacks, David M. Hart – At the Trump-Xi Summit, China Will Have the Upper Hand – May 2026

Bloomberg – Trump Says He Will Discuss Taiwan Arms Sales at Xi Summit – 11 May 2026

Financial Times – Trump's Plan to Discuss Taiwan Arms Sales with Xi Rattles Allies – 12 May 2026

US Senate Foreign Relations Committee – Ahead of Beijing Summit, Shaheen, Tillis Urge President Trump on Taiwan Arms – 10 May 2026

Table Media – Trade, Hormuz, Semiconductors: The Big Bargaining in Beijing – 12 May 2026

South China Morning Post – Will Delay in Trump-Xi Summit Affect US Arms Sales to Taiwan? – 16 March 2026

US Department of Commerce – Revised Semiconductor Licence Review Policy for China – 12 January 2026

Disclaimer: This article is for information and discussion only and does not constitute investment advice or a recommendation.