From Coral to Circuit Boards: The South China Sea's Hidden Tax on Capital

The world's most consequential investment risk is not sitting in a central bank statement or an earnings call. It is rusting on a coral reef in the South China Sea.

The BRP Sierra Madre, a World War Two-era vessel deliberately grounded on Second Thomas Shoal (Ayungin Shoal) in the Spratly Islands since 1999, is the single most structurally fragile node in the global semiconductor supply chain. That claim sounds excessive. It is not. The shoal sits inside the Philippines' Exclusive Economic Zone (EEZ), within one of the most contested maritime corridors on earth, and directly upstream of Taiwan's semiconductor manufacturing complex. Senior allocators with Asia or technology exposure are not pricing this adequately. This article explains why.

Why This Matters

Hidden portfolio exposure: Every portfolio long advanced semiconductors, artificial intelligence (AI) infrastructure, or Asian technology carries latent exposure to a rusting warship that China is methodically trying to dislodge.

Not a binary event: The risk is not a Taiwan invasion scenario. It is a grey-zone escalation that gradually reprices contingency insurance across the entire global fabless-foundry model without a single shot being fired.

Positioning window: The structural case for Association of Southeast Asian Nations (ASEAN) diversification plays and US domestic fabrication is building; the window to position ahead of consensus is still open, but it is narrowing.

The Geography of Risk

Second Thomas Shoal is not strategically significant because of what it is. It is significant because of where it sits. The shoal lies approximately 105 nautical miles from the Philippine island of Palawan, well within Manila's 200-nautical-mile EEZ, and roughly 1,000 nautical miles from the Chinese coastline. Under the 2016 Permanent Court of Arbitration ruling, China's claims to the feature have no legal basis. Beijing has ignored that ruling entirely.

The South China Sea carries approximately one-third of global maritime shipping by volume, with an estimated $3.4 trillion in trade transiting the waterway annually. Japan routes 19.1% of all its goods trade through these waters; China routes 39.5%. The sea lane running past the Spratly Islands is the principal corridor connecting Northeast Asian manufacturing and Taiwan's semiconductor complex to Middle Eastern energy and European markets. A sustained interruption is not a trade disruption. It is a capital event.

The BRP Sierra Madre is the Philippines' physical claim on this ground. Deliberately grounded on the shoal in 1999 and staffed by a rotating detachment of Philippine Marines, the vessel has been structurally deteriorating for years. By early 2025, it was described by analysts as "on the verge of breaking apart." China's coast guard has used water cannons and ramming manoeuvres to obstruct Philippine resupply missions, with one June 2024 incident resulting in a Filipino naval member losing a thumb. In August 2025, following a Chinese naval collision at Scarborough Shoal, Beijing shifted significant maritime militia and coast guard assets to Second Thomas Shoal, deploying an armed swarm in close proximity to the Sierra Madre. The shoal is not approaching a crisis. It is already in one.

The Non-Obvious Mechanism

The standard framing treats Second Thomas Shoal as a Philippines-China bilateral dispute, occasionally elevated to a US-China flashpoint via the 1951 Mutual Defense Treaty. That framing misses the operative investment risk.

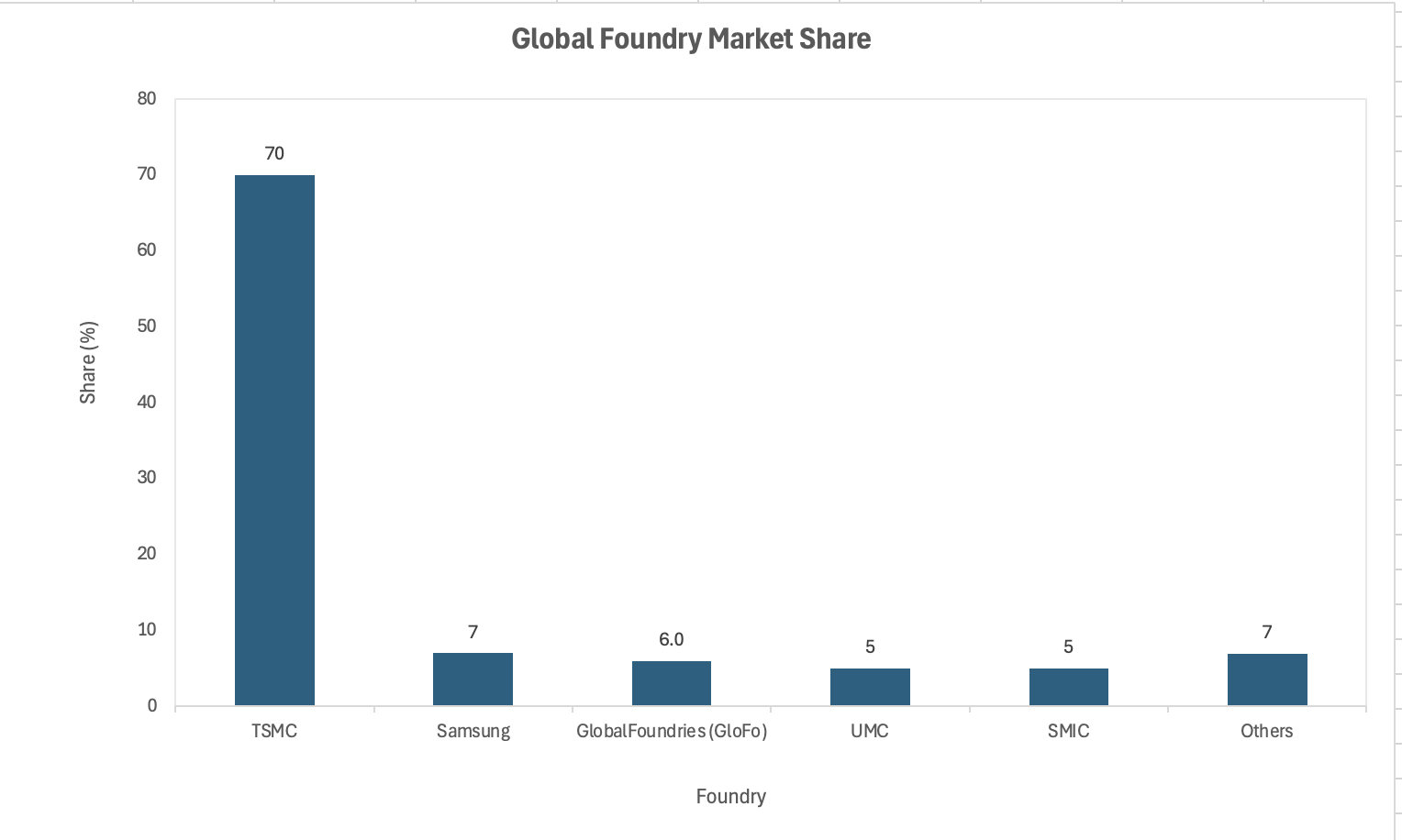

The non-obvious mechanism runs as follows. Taiwan Semiconductor Manufacturing Company (TSMC) holds above 70% of global foundry market share, with Samsung Electronics sitting at approximately 7%, a gap of more than 60 percentage points. TSMC produces above 90% of the world's most advanced chips at or below 5 nanometres (nm), and remains the sole foundry capable of producing at the 2nm scale and below. This is not a competitive concentration problem. It is a single-point-of-failure problem embedded in every AI data centre, advanced defence system, and consumer electronics supply chain on earth. TSMC's most advanced processes remain in Taiwan. Taiwan's trade, energy supply, and logistical connectivity all run through or adjacent to the South China Sea.

Source: Chosun Biz / Industry Data, March 2026

Grey-zone escalation at Second Thomas Shoal does three things that a Taiwan invasion scenario does not: it is deniable, it is incremental, and it does not automatically trigger treaty obligations. That makes it the more likely near-term pathway for Beijing to reshape the strategic calculus in the region. Each escalation step — blocking resupply missions, deploying armed militia swarms, engineering the structural collapse of the Sierra Madre by attrition. This tests the credibility of the US-Philippines Mutual Defense Treaty and probes the willingness of the current US administration to hold its alliance commitments in Asia. Every successful probe lowers the implied cost to Beijing of the next step.

The investment implication is not a binary risk event. It is a repricing of the probability distribution around the Taiwan contingency, executed gradually and with plausible deniability. Insurance markets, corporate treasury hedging, and risk premia in Taiwan-linked technology equities do not currently reflect this. That is the risk not yet reflected in valuations.

What This Means for Capital Allocation

The structural case for diversification away from Taiwan-only semiconductor dependency has been building since at least 2022. What Second Thomas Shoal does is compress the timeline for when that diversification premium gets priced into capital markets.

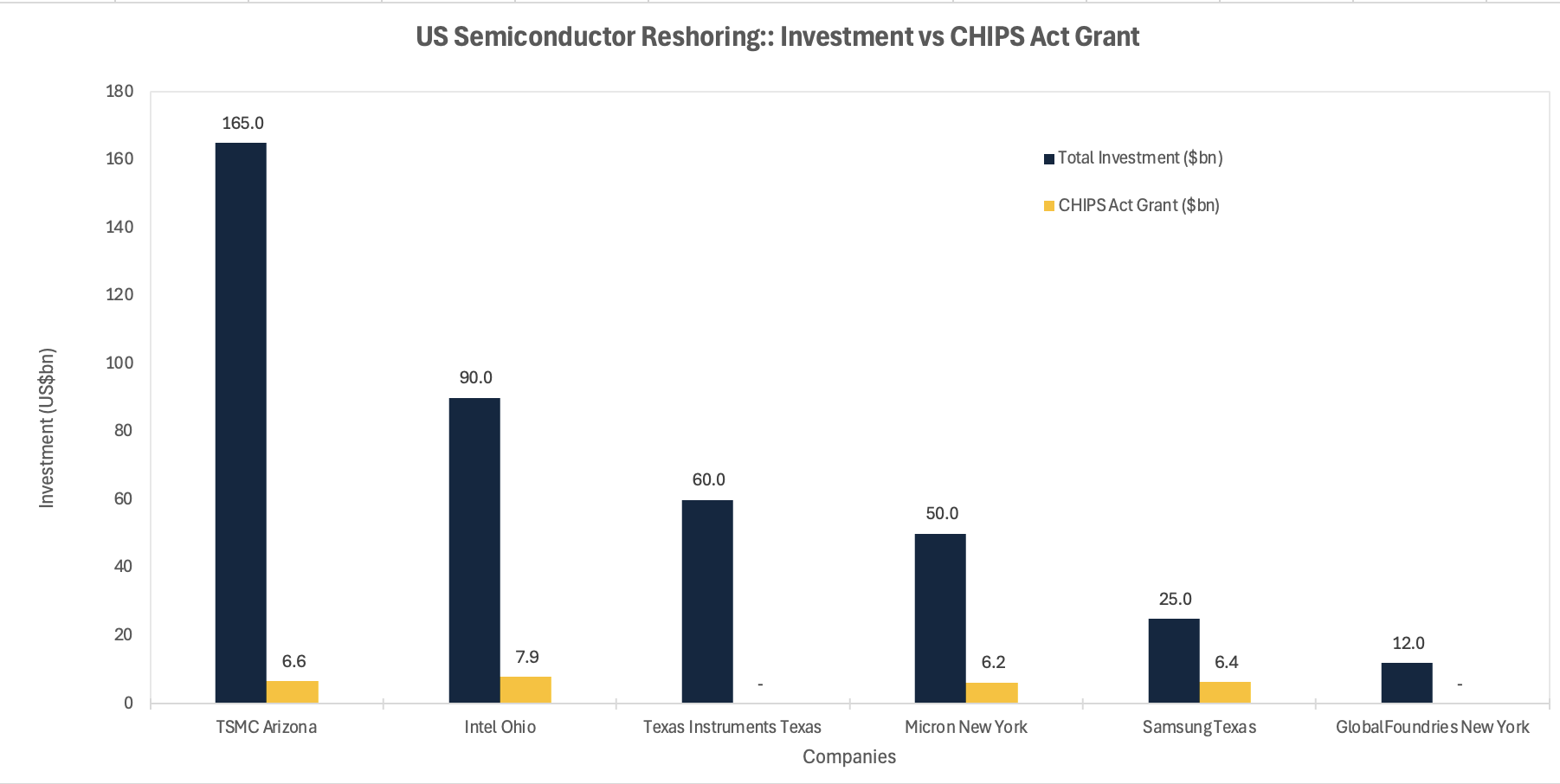

TSMC's Arizona expansion, comprising three greenfield fabs in Phoenix receiving $6.6 billion in Chips and Science Act (CHIPS Act) grants and $5 billion in loans, with total committed investment exceeding $65 billion, is the most concrete near-term beneficiary. The first Arizona fab (4nm node) entered volume production; the second (3nm) and third are on schedule. The reshoring premium for US-based advanced fabrication capacity is structural, not cyclical, and it compounds with each escalation event in the South China Sea.

Source: CHIPS Act / Company Announcements / IDTechEx 2025

The Philippines is underappreciated in this context. Manila is an established hub in the global semiconductor value chain, concentrated in assembly, testing, and packaging — the back-end processes that are no less critical than fabrication. US manufacturer Onsemi was deepening its Philippine footprint as recently as April 2026. Philippine semiconductor exposure is therefore a dual play: operational upside from US-Asia supply chain rebalancing, and geopolitical optionality from being the country at the centre of the South China Sea dispute. The risk is obvious. The upside is underweighted.

For allocators with passive emerging-markets (EM) exposure, the hidden risk is concentration in Asian technology without explicit Taiwan-risk accounting. Passive EM indices carry significant TSMC and Taiwan-adjacent weight. The risk committee question is not whether to short TSMC. It is whether the portfolio has sufficient diversification across the semiconductor value chain to absorb a six-to-twelve-month disruption scenario without structural drawdown.

Near-Term Catalysts and Policy Outlook

The risk horizon here is asymmetric in a specific way: the downside is discontinuous and the upside is merely gradual. A deterioration event at Second Thomas Shoal does not give markets a week to reprice; it gives them hours. Against that backdrop, the 0–3 month window carries disproportionate weight relative to the 3–12 month window, not because long-term structural trends matter less, but because the near-term trigger is physical and observable in a way that most geopolitical risks are not. Watch the Sierra Madre, not the diplomatic calendar.

0–3 month window (to end July 2026): The structural condition of the BRP Sierra Madre is the immediate trigger variable. Any visible deterioration, or any Philippine attempt to begin reinforcement works, risks a direct Chinese interdiction response. The current US administration's posture on Asian alliance commitments remains the key uncertainty: verbal affirmation of the Mutual Defense Treaty has not been matched by consistent operational signalling. Watch for ASEAN foreign ministers' communiqués in this window and any joint US-Philippines maritime patrol announcements as credibility signals.

3–12 month window (to end Q1 2027): TSMC Arizona's second fab (3nm node) is expected to enter production within this window: the first genuine data point on whether US onshoring can absorb meaningful leading-edge volume. CHIPS Act disbursements for the broader semiconductor ecosystem, including memory, packaging, and materials, will provide a forward read on US industrial policy durability. Meanwhile, China's coast guard legislation, operationalised from 2021, gives Beijing a domestic legal framework to escalate interdiction operations without formal military action. Any incident resulting in Philippine casualties would constitute a treaty-triggering test.

Reducing this to three scenarios risks false precision, but the exercise is useful for one specific reason: it forces a clean separation between what is already in motion (grey-zone attrition, structural decay, partial reshoring) and what remains genuinely contingent (US alliance credibility, Chinese timing, the pace of TSMC Arizona's ramp). The scenarios below should be read not as forecasts but as a framework for identifying which variables to monitor and which portfolio positions are exposed to each outcome.

Base case — Grey-zone attrition holds: China continues blocking resupply missions; the Sierra Madre deteriorates but no seizure occurs; the tacit provisional arrangement at the shoal intermittently holds. The South China Sea risk premium builds slowly and without a single trigger event. TSMC Arizona's reshoring premium compounds quarter by quarter. ASEAN back-end semiconductor diversification accelerates as corporates quietly reduce Taiwan concentration without declaring it publicly.

Upside — Deterrence stabilises: A sustained US-Philippines joint maritime presence establishes credible deterrence at Second Thomas Shoal; China redirects grey-zone pressure elsewhere in the region; TSMC Arizona's 3nm ramp exceeds production expectations within the 3–12 month window. The Taiwan-risk discount compresses, tech equity valuations recover, and ASEAN semiconductor plays re-rate as the diversification premium partially unwinds.

Downside — Structural collapse triggers seizure: The Sierra Madre's physical deterioration reaches a point of no return; a Chinese interdiction operation forces a direct test of the US-Philippines Mutual Defense Treaty; maritime insurance rates spike across South China Sea corridors. The cost of capital in Taiwan-dependent technology reprices sharply and rapidly, passive EM indices absorb structural drawdown, and supply chain insurance becomes a systemic line item on corporate balance sheets rather than a tail-risk provision.

Conclusion

The structural read is straightforward, even if the timeline is not. Second Thomas Shoal is not the cause of semiconductor supply chain vulnerability. It is the variable that determines how quickly that vulnerability becomes a market-pricing event. The concentration of advanced chip manufacturing in Taiwan, the slow erosion of deterrence credibility in the South China Sea, and the partial but incomplete progress on US reshoring are three independent trends converging on the same risk. Individually, each is a known variable. Together, and against the backdrop of a rusting warship that Beijing is methodically waiting to outlast, they constitute an underpriced, structurally significant capital risk.

The view a cautious sell-side analyst would not publish: the BRP Sierra Madre's physical condition is a more reliable leading indicator for Taiwan-risk premium than TSMC's earnings guidance or any diplomatic communiqué from Beijing. When the ship goes, the probability distribution shifts, and it shifts fast. The time to position for that scenario is before consensus reaches the same conclusion.

References

MERICS – China Security and Risk Tracker Q2 2024 – 2024

Table.media – Tensions in the South China Sea – May 2025

CSIS / ChinaPower – How Much Trade Transits the South China Sea? – 2017 (updated)

CSIS – Rocking the Boat: The Philippines Trade Strategy Amid Rising Geoeconomic Tensions – March 2025

International Crisis Group via SCMP – Any Philippine Move to Build Permanent Shoal Structure Risks China's Retaliation – October 2024

Sinocism – Second Thomas Shoal Approaching a Crisis? – October 2023

Truman Project – Saving Taiwan's Silicon Scientists – September 2025

Chosun Biz – Taiwan Chip Concentration Stokes Global Risk as TSMC Widens Lead Over Samsung – March 2026

ScienceDirect – From Vulnerabilities to Resilience: Taiwan's Semiconductor Industry and Geopolitical Challenges – May 2025

AMTI/CSIS – Divergence and Tacit Understanding in the China-Philippines Provisional Arrangement at Second Thomas Shoal – March 2026

NIST / US Department of Commerce – TSMC Arizona CHIPS Act Award – 2024

SDxCentral – TSMC to Receive $11.6bn in US CHIPS Act Funding – April 2024

BNC Philippines – Philippines as Semiconductor Hub, Onsemi Expansion – April 2026

SeaLight / Powell & Carouso – Flashpoint: Second Thomas Shoal (Again!) – August 2025

This article is for information and discussion only and does not constitute investment advice or a recommendation.