When Geopolitics Starts to Behave Like an Asset Class

Author: Justin Kew & Martin Sacchi

For much of the post-Cold War era, geopolitics sat outside formal investment frameworks. It was treated as an exogenous shock — a source of volatility to be hedged, not a driver of durable returns. That assumption no longer holds. The combination of great-power competition, war in Europe, weaponised trade and energy, and the return of activist industrial policy has turned geopolitics into something that behaves increasingly like an asset class.

This shift is not ideological. It is visible in balance sheets, capex plans and capital flows. Defence budgets have reset structurally higher. Energy systems are being rebuilt with security, not just efficiency, as the organising principle. Supply chains are being re-engineered around trust and alignment rather than lowest cost. And governments are underwriting large parts of the industrial stack — from semiconductors to materials — at a scale that makes geopolitics directly investible.

From background risk to structural factor

Three developments explain why geopolitics has moved from the margins of portfolio construction to the centre.

First, policy scale has changed. Industrial policy in the US, Europe and Asia now involves explicit fiscal commitments measured in hundreds of billions of dollars. These programmes are not temporary stimulus; they are multi-year efforts to reshape production, technology ownership and strategic autonomy.

Second, defence has been re-normalised. Global military expenditure reached a record level in 2024, rising sharply in Europe, the Middle East and parts of Asia. More importantly for investors, the justification for higher spending has shifted from episodic conflict to long-term deterrence and industrial readiness. That change extends the duration and visibility of defence-related cash flows.

Third, energy and supply chains have been politicised by design. The energy transition is no longer only a climate project; it is also an industrial and security project. At the same time, trade policy, export controls and sanctions have turned supply-chain configuration into a strategic choice, not a purely commercial one.

Together, these forces have made geopolitics capital-intensive and persistent — the two conditions that allow it to be treated as an allocable investment theme rather than an unpriceable risk.

Why investors can no longer treat geopolitics as background noise

What makes geopolitics investible today is not the frequency of crises, but the way political decisions now reorder capital, technology and industrial capacity across borders. This cannot be captured by traditional macroeconomic models, which focus on growth, inflation and monetary policy in isolation, nor by sector analysts, who typically operate within national or industry silos.

Geopolitics operates differently. It reshapes markets through:

export controls and sanctions,

industrial subsidies and localisation rules,

defence procurement and alliance commitments,

energy security doctrines,

and strategic control of materials and supply chains etc

These mechanisms cut across asset classes, regions and sectors simultaneously. Understanding their impact requires connecting macro policy shifts to micro industrial outcomes, and tracing second- and third-order effects globally — from materials extraction and processing, through manufacturing and logistics, to end-market pricing power.

This is why geopolitics cannot be outsourced to headlines or treated as a tail risk. It requires a distinct analytical lens — one that blends economics, policy, security, technology and industrial organisation. For investors, ignoring this dimension increasingly means misunderstanding where capital is being directed, where constraints will emerge, and where long-duration returns will ultimately accrue.

Industrial policy: from theory to P&L

Industrial policy is now shaping profits, not just narratives. What began with semiconductors and clean energy has broadened into a full-stack effort that spans technology, manufacturing, infrastructure and — critically — materials.

Semiconductors: reshoring as a capex cycle

Semiconductors have become critical infrastructure. The US, EU, Japan, South Korea and India have all introduced subsidy regimes aimed at rebuilding domestic or allied fabrication capacity and reducing exposure to concentrated supply chains.

In Europe, the Chips Act has moved from legislation to execution, with state-aid approvals translating into concrete fab investments, pilot lines and supporting ecosystems. In the US, the combination of direct grants and tax credits has catalysed one of the largest industrial build-outs in decades.

For investors, the reshoring story is not confined to chip designers. The more durable opportunity often lies in second-order beneficiaries: construction and engineering firms, specialty materials and gases, power and water infrastructure, and equipment suppliers tied to long-lived facilities.

Green industrial policy: system build-out, not just deployment

Clean-energy policy has also evolved. The emphasis has shifted from headline deployment targets to system resilience: grids, storage, power electronics, interconnectors and industrial efficiency. This reflects a growing recognition that energy security and decarbonisation now sit on the same balance sheet.

The scale is significant. Global energy investment is running at record levels, with the majority directed toward low-carbon technologies and enabling infrastructure. This has created long-dated capex pipelines that resemble regulated infrastructure more than cyclical commodity bets.

Regional tech hubs: place-based policy creates local winners

Industrial policy is increasingly geographic. Subsidies and procurement come with location conditions, favouring clusters, science parks and manufacturing corridors. These hubs matter because they create spill-over effects: demand for power, logistics, housing, transport and skilled labour.

For investors, hub formation is less about narrative and more about underwriting local balance sheets and infrastructure assets that benefit from persistent public and private investment.

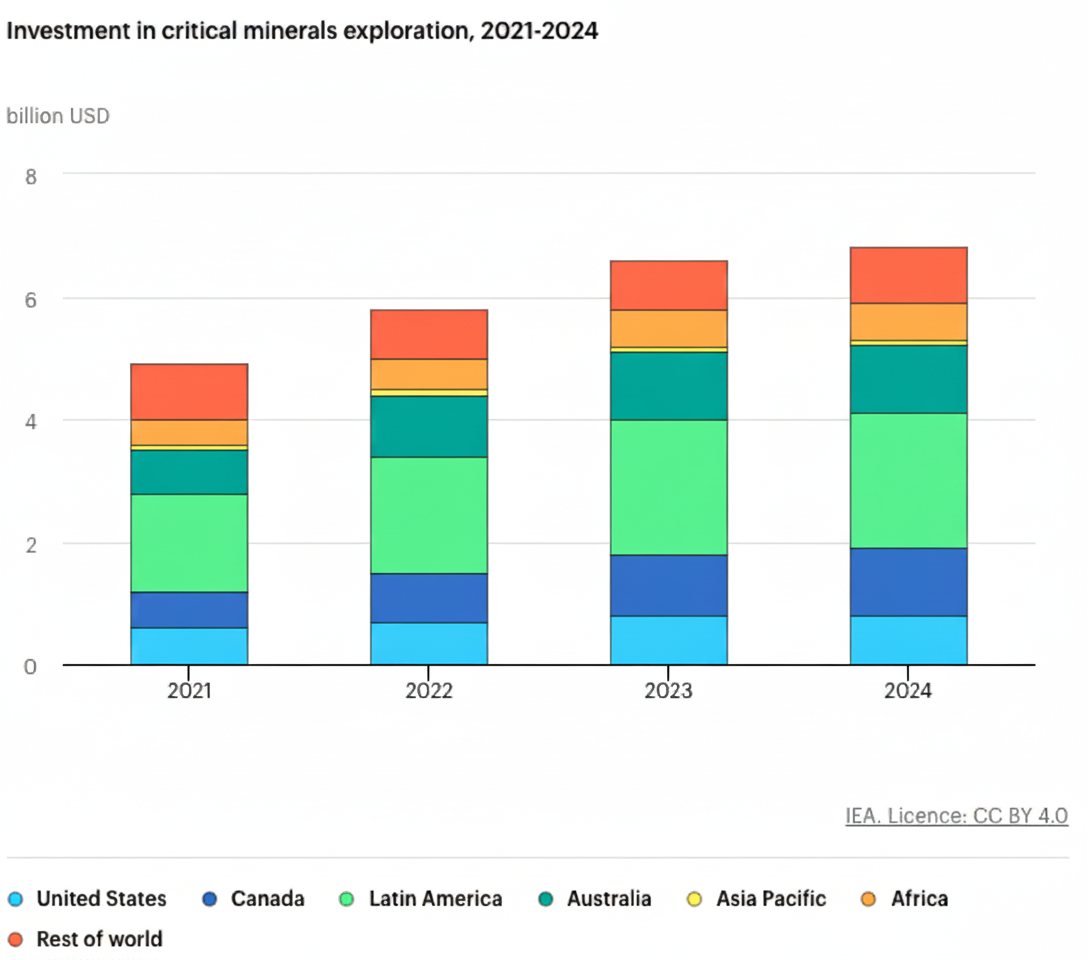

The missing pillar: materials and minerals as strategic assets

No industrial strategy — whether in defence, semiconductors or clean energy — is credible without secure access to materials and minerals. What were once treated as cyclical commodities are now recognised as strategic industrial inputs, sitting upstream of every major geopolitical priority: rearmament, energy security, technological sovereignty and supply-chain resilience. As a result, materials policy has become one of the clearest expressions of geopolitics as an investible force.

Europe’s approach to materials has shifted decisively from market reliance to strategic management. Through the Critical Raw Materials Act (CRMA) and the broader ResourceEU framework, Brussels has reframed access to raw materials as a matter of economic security rather than efficiency. The CRMA establishes explicit 2030 targets — at least 10% of extraction, 40% of processing and 25% of recycling to take place within the EU, alongside a cap limiting dependence on any single third country to 65% for strategic materials. ResourceEU complements this by coordinating trade policy, development finance, export credit and diplomatic partnerships with resource-rich countries. For investors, the signal is clear: materials assets embedded within EU-aligned extraction, processing and recycling ecosystems now benefit from policy support, faster permitting and greater demand visibility, while pure lowest-cost sourcing carries rising political and regulatory risk.

China’s materials strategy is defined not only by scale but by control of chokepoints, particularly in processing and refining. Over the past decade, China has consolidated dominant positions in rare earths, graphite and battery materials, and more recently has made this leverage explicit through export controls and licensing regimes on key inputs such as gallium, germanium and certain graphite products. These measures are not tactical supply disruptions; they are strategic signals that access to critical materials can be conditioned by geopolitical alignment. For global investors, this elevates materials risk from price volatility to supply security, forcing downstream industries — from defence electronics and semiconductors to EVs and wind turbines — to internalise geopolitical exposure. The consequence is a structural re-rating of non-China processing, refining and specialty-materials capacity elsewhere, even at higher cost.

In the United States, critical minerals policy has moved rapidly from a climate-transition concern to a national-security priority. Washington has deployed the Defense Production Act, Inflation Reduction Act incentives tied explicitly to non-China supply chains, Department of Energy loan guarantees, and bilateral mineral security partnerships to accelerate domestic and allied processing capacity. The objective is not autarky, but resilience: ensuring sufficient access to materials for defence systems, energy infrastructure and advanced manufacturing without reliance on adversarial jurisdictions. For investors, this has shifted the opportunity set away from pure extraction and toward processing, recycling, vertical integration and allied-jurisdiction supply chains, where public capital, policy backing and long-term offtake commitments reduce risk and extend asset duration.

Taken together, these regional strategies show why materials and minerals have become a core geopolitical asset class. Capital is no longer allocated solely on marginal cost or global liquidity, but on alignment, resilience and strategic relevance. This changes how materials assets are valued, which segments attract long-duration capital, and where supply-chain bottlenecks are most likely to translate into sustained pricing power. Investors who continue to view materials through a purely cyclical or commodity lens risk missing one of the most important structural shifts underpinning defence, energy and industrial policy in the coming decade.

China’s role: scale, integration and outward expansion

China sits at the centre of the geopolitics-as-asset-class story, not only as a competitor but as the benchmark against which other strategies are designed.

Across materials and minerals, China has spent more than a decade building dominance in refining and processing, particularly in rare earths, graphite and battery inputs. More recently, it has expanded outward, investing in upstream and midstream assets in Africa, Latin America and parts of Asia, often pairing capital with infrastructure and offtake agreements.

In semiconductors, China continues to pursue self-sufficiency through sustained state support across the ecosystem — from fabrication to equipment, materials and packaging. Export controls have reinforced, rather than weakened, the strategic priority attached to this effort.

In green industrial policy, China’s approach has combined domestic scale with internationalisation. As domestic capacity has surged, Chinese firms have increasingly invested overseas — particularly in emerging markets — to secure market access, manage trade friction and maintain utilisation.

And in regional hubs, China’s model integrates policy, finance, land and demand. That ability to build and replicate industrial clusters quickly is precisely what Western governments are now trying to emulate through their own hub-based strategies.

For investors, China’s role is less about direct allocation and more about constraint. Its scale and integration force higher policy intensity elsewhere, underpinning the durability of industrial and defence spending in the US and Europe.

Defence: from cyclical exposure to structural allocation

Defence spending is the most explicit expression of geopolitics as an asset class. The reset in global defence budgets reflects not only current conflicts but a broader reassessment of deterrence, alliance commitments and industrial readiness.

The investible universe extends beyond prime contractors. Dual-use technologies — space, secure communications, sensing, autonomy and cyber — sit at the intersection of civilian and military demand. Supply-chain depth, from propulsion to advanced materials and electronics, has become a priority as governments seek resilience rather than just capability.

For credit investors, defence has also taken on new characteristics. Long-dated sovereign contracts and explicit political backing can compress risk premia, particularly where production capacity is scarce.

Supply chains and emerging markets: the new geopolitical balance sheet

The re-engineering of supply chains has created a differentiated landscape in emerging markets. Some countries sit on the front line of geopolitical risk; others have become beneficiaries of trade diversion, near-shoring and friend-shoring.

Manufacturing hubs in Mexico, parts of central and eastern Europe, and south-east Asia have attracted new investment as firms diversify away from concentrated exposure. At the same time, energy-transition projects and materials processing facilities in emerging markets are drawing capital from a mix of Western, Chinese and Gulf sources.

For investors, this has turned emerging markets into a barbell: commodity and energy exporters on one side, manufacturing and services hubs on the other, with outcomes heavily shaped by alignment and policy credibility.

From narrative to allocation

Geopolitics has become investible because it now directs capital at scale and with persistence. Industrial policy, defence rearmament, energy system transformation and supply-chain realignment are reshaping profit pools across public and private markets.

The challenge for investors is not to trade headlines but to recognise where geopolitical decisions translate into durable cash flows: in infrastructure, manufacturing capacity, materials processing, defence ecosystems and aligned emerging markets.

Conclusion

Geopolitics is no longer an externality to markets; it is one of their organising principles. As governments intervene more deeply in production, technology and trade, the boundary between policy and profit has blurred.

For long-term investors, this does not mean abandoning traditional disciplines. It means acknowledging that security, resilience and alignment now shape capital allocation as decisively as growth and inflation once did. In that sense, geopolitics has become an asset class not because it is fashionable, but because it now sits on the balance sheet of the global economy itself.